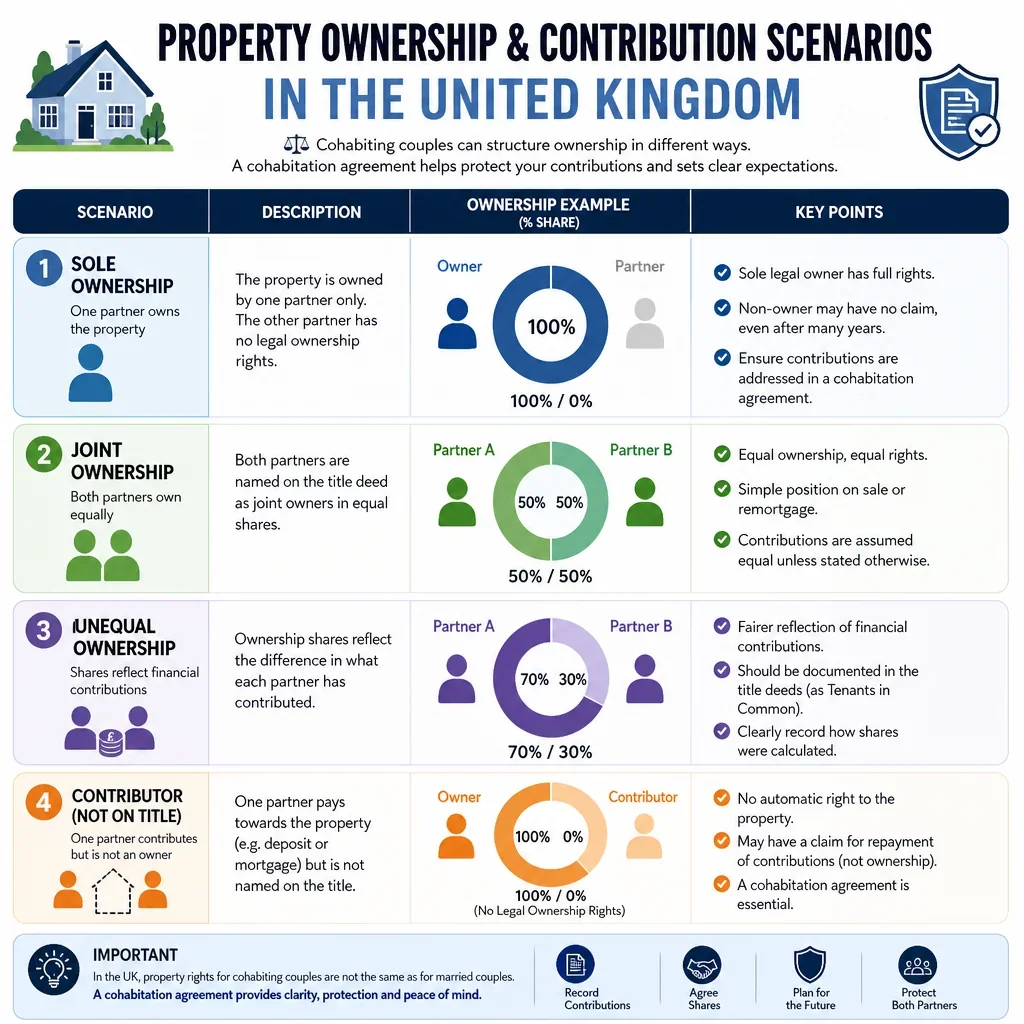

Property Ownership And Contribution Scenarios In The United Kingdom

Key Issue | Contribution Examples | Agreement Points | Record-Keeping Importance | Jurisdiction Relevance |

|---|---|---|---|---|

Sole owner with non-owner contribution | ||||

Whether payments create a beneficial interest or are treated as occupation costs. | Monthly mortgage transfers, overpayments, payments described as "rent" or "house money". | State whether payments give ownership, reimbursement, or no property interest. | High | England and Wales |

Whether paying bills affects ownership expectations. | Council tax, utilities, broadband, insurance, groceries. | Classify bills as living expenses and separate them from ownership contributions. | Medium | UK-wide general relevance |

Whether a lump sum is a loan, gift, repayment contribution, or ownership contribution. | £10,000 mortgage reduction, arrears clearance, product fee payment. | Record purpose, repayment date, interest, and effect on beneficial ownership. | High | UK-wide general relevance |

Whether the non-owner can remain in the property after separation. | Non-owner paid towards mortgage and repairs while living in the home. | Set notice period, moving-out obligations, and temporary occupation payments. | High | England and Wales |

Joint owners with equal shares | ||||

Confirm equal beneficial ownership despite different day-to-day payments. | One partner earns more and pays larger mortgage instalments. | Confirm 50:50 ownership, payment responsibilities, and sale proceeds split. | Medium | England and Wales |

Avoid later disputes about equal ownership and equal liabilities. | Equal deposit, equal mortgage, equal legal fees. | Record 50:50 shares and equal responsibility for mortgage, insurance, and repairs. | Medium | UK-wide general relevance |

Whether missed contributions alter ownership shares or create debt. | Redundancy, maternity leave, illness, career break. | Set payment holiday rules, reimbursement, and whether shares remain equal. | High | UK-wide general relevance |

Joint tenancy may pass automatically to the survivor on death. | Equal purchase but different wishes for inheritance. | Consider tenancy type, wills, severance, and death-related buyout provisions. | High | England and Wales |

Joint owners with unequal shares | ||||

Set clear beneficial shares that differ from legal title. | 70:30 deposit split and 70:30 mortgage payments. | Record percentage shares and use a declaration of trust where appropriate. | High | England and Wales |

Whether shares change as partners make different ongoing contributions. | One pays deposit both later pay mortgage equally. | Choose fixed shares or formula-based shares and define calculation method. | High | UK-wide general relevance |

Whether purchase costs affect ownership or are separate expenses. | Stamp duty, LBTT, LTT, conveyancing fees, survey, broker fee. | State whether costs are reimbursable, shared, or reflected in ownership shares. | High | UK-wide general relevance |

Joint mortgage liability may not match private ownership shares. | Both named on mortgage, but one pays 80% monthly. | Record internal payment split and indemnity for unequal mortgage responsibility. | High | UK-wide general relevance |

Deposit paid by one partner | ||||

Whether the deposit is returned before profits are divided. | One partner pays full £50,000 deposit from savings. | Ring-fence deposit, then split remaining equity by agreed percentages. | High | UK-wide general relevance |

Whether the deposit is intended as a personal contribution or shared gift. | Savings transferred from one partner into joint conveyancing account. | State whether the payer gives up reimbursement or keeps a protected share. | High | UK-wide general relevance |

Preserve pre-owned equity introduced into the new home. | Net sale proceeds from one partner's former property used as deposit. | Identify source of funds and repayment priority on sale or separation. | High | UK-wide general relevance |

Who bears the repayment risk for borrowed deposit funds. | Personal loan, employer loan, family loan used for deposit. | Allocate loan repayment responsibility and effect on equity division. | High | UK-wide general relevance |

Mortgage paid by both partners | ||||

Whether income-based contributions affect ownership shares. | One pays 60% and the other pays 40% of monthly instalments. | State whether unequal payments change shares or are simply household budgeting. | High | UK-wide general relevance |

Whether capital overpayments create extra equity entitlement. | Annual bonus used to reduce mortgage balance. | Define overpayments as gift, loan, protected contribution, or share adjustment. | High | UK-wide general relevance |

Capital repayment and interest may be treated differently by agreement. | One pays interest the other pays capital repayment element. | Define which payments build equity and which are occupation costs. | High | UK-wide general relevance |

How released equity and increased debt should be shared. | Remortgage releases cash for business, debts, or car purchase. | Record recipient, purpose, repayment responsibility, and effect on net equity. | High | UK-wide general relevance |

Renovations funded by one partner | ||||

Whether improvement costs increase that partner's equity share. | Extension, loft conversion, new kitchen, structural works. | Define reimbursement, share increase, or no adjustment for improvements. | High | UK-wide general relevance |

Distinguish maintenance from value-enhancing improvements. | Boiler replacement, roof repairs, damp treatment, decorating. | Classify routine repairs separately from capital improvements. | High | UK-wide general relevance |

Whether unpaid labour has an agreed financial value. | Project management, decorating, carpentry, landscaping. | State whether labour is valued, ignored, or reimbursed by agreed formula. | Medium | UK-wide general relevance |

Whether unauthorised works should be reimbursed or excluded. | One partner commissions expensive works without written agreement. | Require written consent and budget approval for reimbursable works. | High | UK-wide general relevance |

Family contribution to property | ||||

Whether family money is a gift to one partner, both partners, or a loan. | Parents provide £25,000 towards deposit. | Record donor intention, recipient, repayment terms, and equity effect. | High | UK-wide general relevance |

Family loans can create debt disputes after separation. | Interest-free parental loan repayable on sale. | Specify borrower, repayment trigger, priority, interest, and evidence. | High | UK-wide general relevance |

A guarantor may face liability without gaining ownership. | Parent guarantees mortgage or provides security savings account. | Record indemnity, release plan, ownership position, and repayment obligations. | High | UK-wide general relevance |

Whether inherited funds remain protected or become shared equity. | Inheritance used for deposit, extension, or mortgage repayment. | Identify inherited funds and state reimbursement or share protection. | High | UK-wide general relevance |

Joint owners with unequal shares | ||||

Court applications may concern property rights, sale, and beneficial interests. | Dispute over sale or shares after unequal contributions. | Include sale triggers, valuation process, buyout rights, and agreed shares. | High | England and Wales |

Sole owner with non-owner contribution | ||||

Scottish cohabitants may seek financial provision after separation in limited circumstances. | Non-owner contributes money, childcare, or household support. | Address property ownership, payments, compensation expectations, and separation terms. | High | Scotland |

Joint owners with unequal shares | ||||

Property and trust disputes may require court determination of ownership interests. | Unequal deposit or mortgage payments despite joint ownership. | Set express ownership shares and evidence contributions clearly. | High | Northern Ireland |

Mortgage paid by both partners | ||||

Indirect contributions may create different expectations from bank records alone. | One pays mortgage the other pays childcare, food, and utilities. | Define whether indirect contributions support ownership, reimbursement, or no adjustment. | High | UK-wide general relevance |

Joint owners with unequal shares | ||||

Mortgage, rent, staircasing, and service charges may be funded unequally. | One pays staircasing premium both pay rent and service charge. | Allocate staircasing costs, future shares, rent, service charges, and sale proceeds. | High | England and Wales |

Renovations funded by one partner | ||||

Major works and service charges can be substantial non-mortgage property costs. | Section 20 works, reserve fund demand, service charge arrears. | State who pays leasehold charges and whether payments affect equity. | High | England and Wales |

Deposit paid by one partner | ||||

Discount entitlement and purchase funding may belong to different people. | Tenant partner qualifies for discount other partner funds deposit. | Record treatment of discount value, deposit, legal title, and sale proceeds. | High | England and Wales |

Sole owner with non-owner contribution | ||||

Existing equity should be distinguished from later shared contributions. | Owner already has £100,000 equity before cohabitation starts. | Set start valuation and define effect of future payments on equity. | High | UK-wide general relevance |

Deposit paid by one partner | ||||

Buyout funding may create a protected contribution in the new arrangement. | One partner funds payment to remove an ex-partner from title. | Record buyout amount, ownership shares, and reimbursement on later sale. | High | UK-wide general relevance |

Joint owners with unequal shares | ||||

Losses and mortgage shortfall may not follow profit-sharing assumptions. | Property sold for less than mortgage and sale costs. | State how negative equity, fees, and shortfall debts are shared. | High | UK-wide general relevance |

Joint owners with equal shares | ||||

Sale costs can materially reduce distributable equity. | Estate agent fees, conveyancing fees, EPC, early repayment charge. | Deduct agreed costs before equity split and allocate early repayment charges. | Medium | UK-wide general relevance |

Renovations funded by one partner | ||||

Business-funded improvements or use may complicate ownership and tax expectations. | Garden office, studio conversion, dedicated consulting room. | Record funding source, use rights, tax responsibility, and reimbursement terms. | High | UK-wide general relevance |

Joint owners with unequal shares | ||||

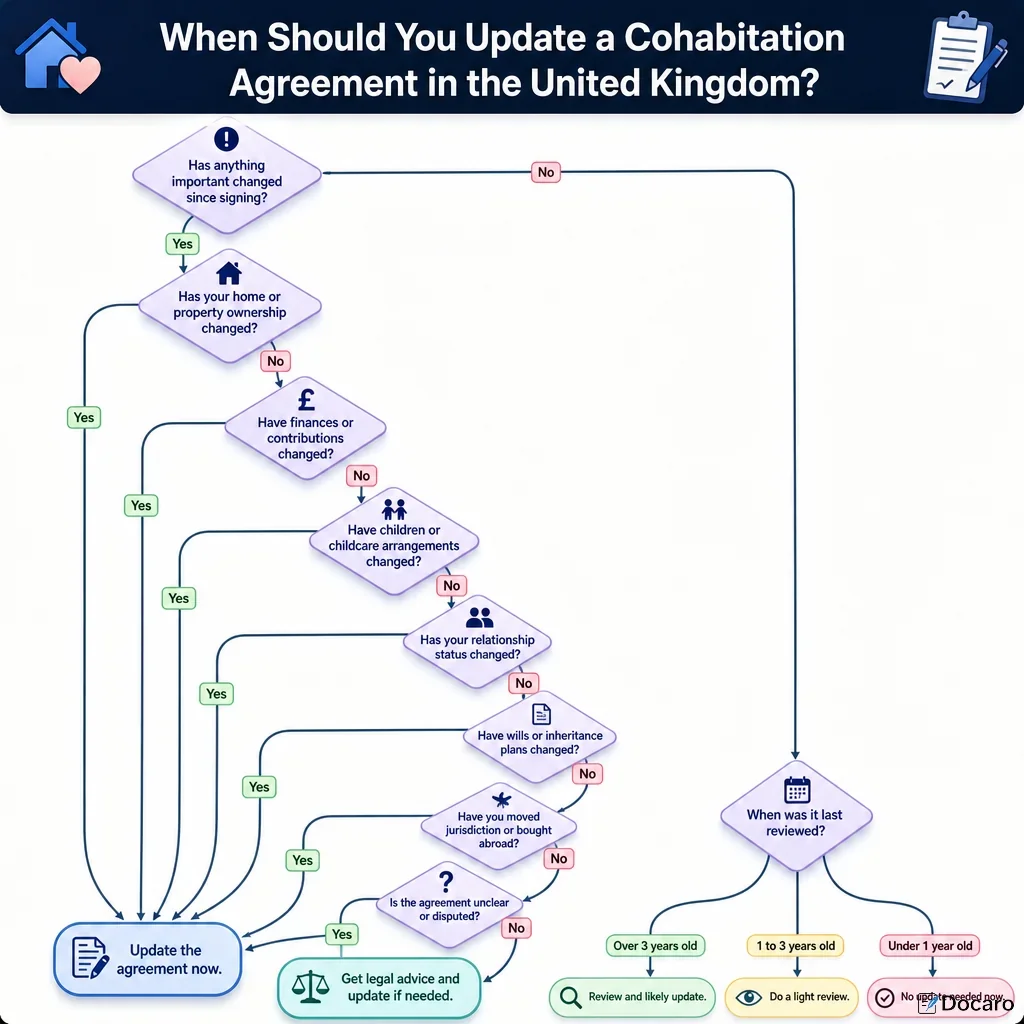

Cohabitation terms may need review if partners marry or enter civil partnership. | Unequal deposit and agreed shares during cohabitation. | Include review trigger on engagement, marriage, civil partnership, or children. | Medium | UK-wide general relevance |

Joint owners with equal shares | ||||

Separation may require temporary occupation arrangements where children live in the home. | One parent remains with children and pays reduced mortgage share. | Set occupation period, payment split, sale trigger, and child-related review dates. | High | UK-wide general relevance |

Rental income and related costs should be allocated consistently with ownership. | Lodger rent used for mortgage or repairs. | State who may grant occupation and how income, tax, and costs are shared. | Medium | UK-wide general relevance |

Renovations funded by one partner | ||||

Insurance payouts and excess payments may affect reimbursement expectations. | One partner pays excess and uninsured repair costs after flood damage. | Allocate insurance premiums, excesses, payouts, and uninsured repair costs. | High | UK-wide general relevance |

Sole owner with non-owner contribution | ||||

Local tax payments usually need separating from property ownership contributions. | Council tax, rates in Northern Ireland, water charges in Scotland. | Treat local charges as occupation expenses unless expressly agreed otherwise. | Medium | UK-wide general relevance |

Joint owners with unequal shares | ||||

Adding a partner to title should reflect agreed beneficial shares and consideration. | Non-owner added after paying lump sum or taking mortgage liability. | Record transfer value, new shares, mortgage liability, and prior equity protection. | High | England and Wales |

Deposit paid by one partner | ||||

Government bonuses or savings products may be contributed by one partner only. | Lifetime ISA withdrawal and government bonus used for deposit. | Record contributed amount and whether bonus is personal or shared equity. | High | UK-wide general relevance |

Mortgage paid by both partners | ||||

Arrears payments may rescue the property but create repayment expectations. | One partner pays arrears, default fees, and lender charges. | State whether arrears payments are reimbursed or alter equity shares. | High | UK-wide general relevance |

Joint owners with unequal shares | ||||

Tenants in common can hold distinct beneficial shares. | 60:40 ownership recorded to reflect unequal deposit. | Align cohabitation agreement with declaration of trust and wills. | High | England and Wales |

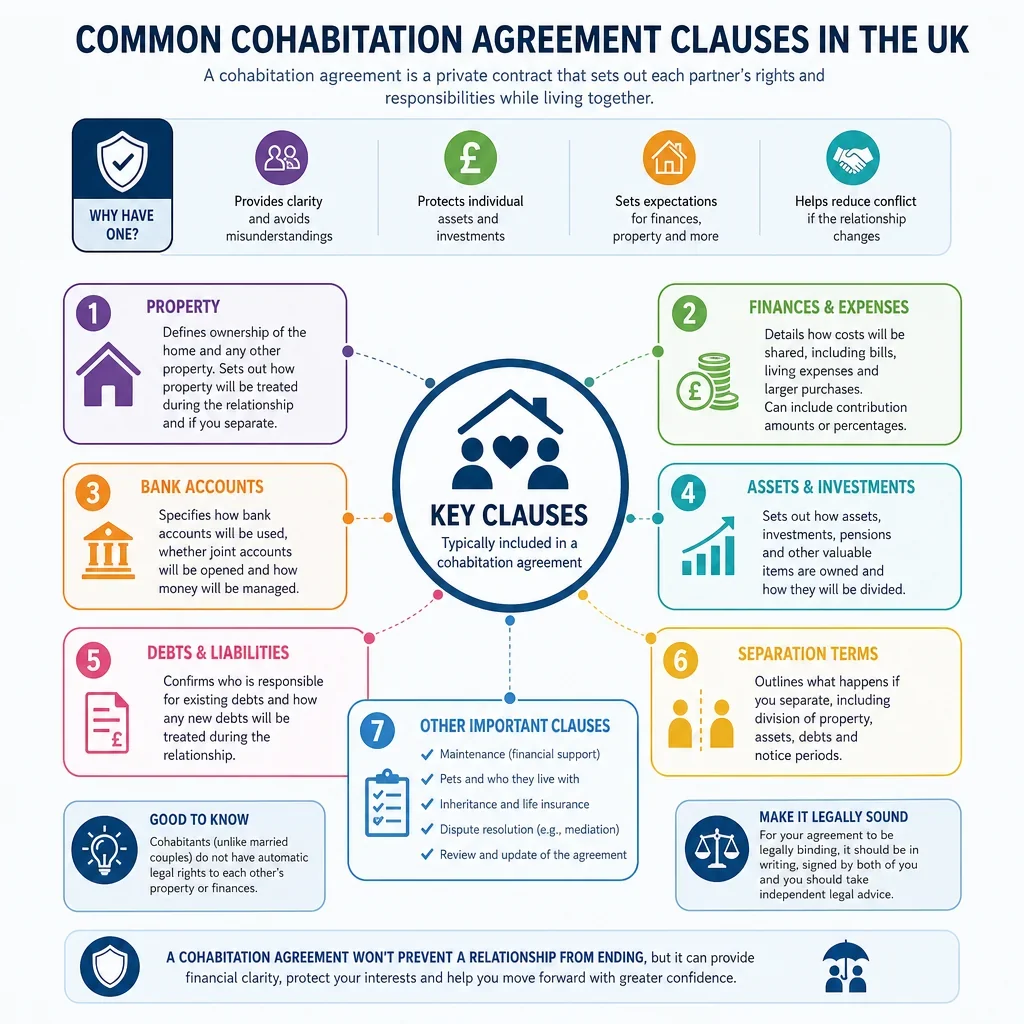

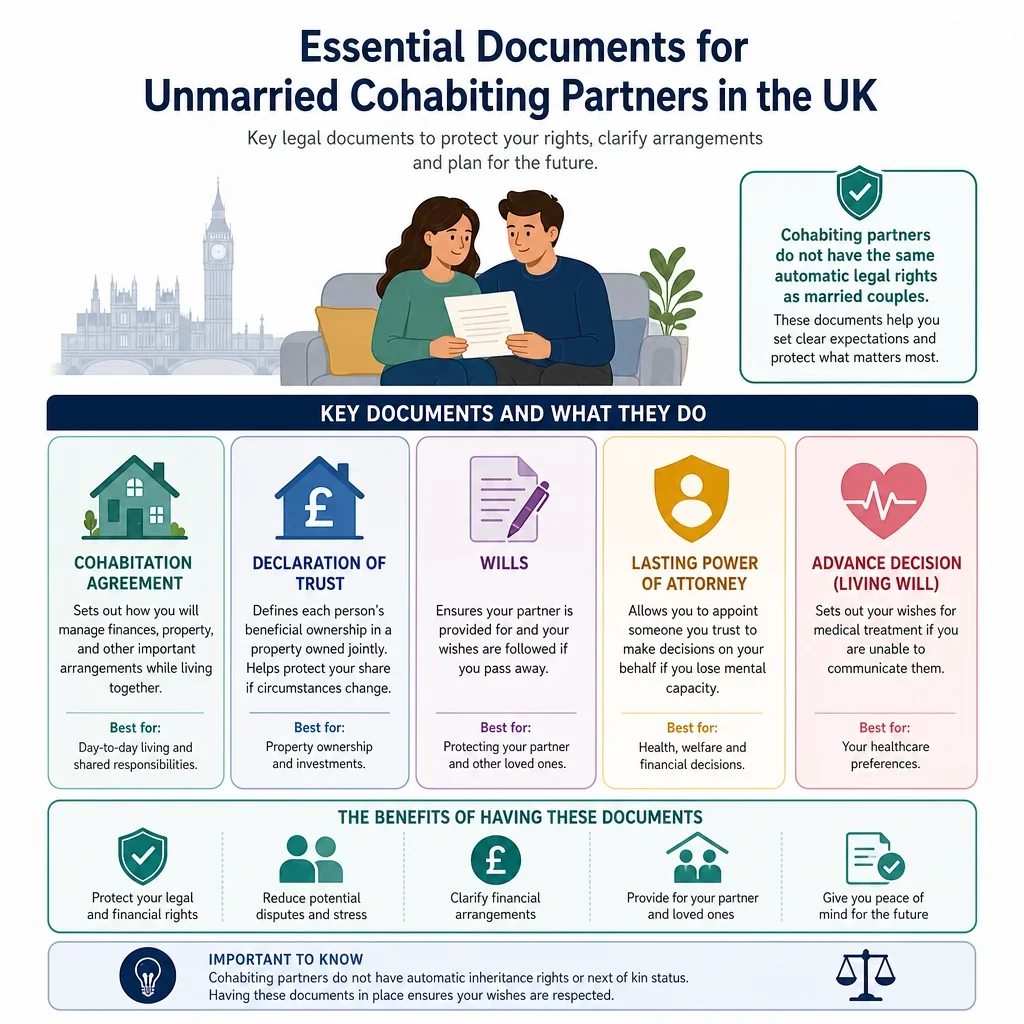

Why Should Cohabiting Partners Record Property Contributions In The UK?

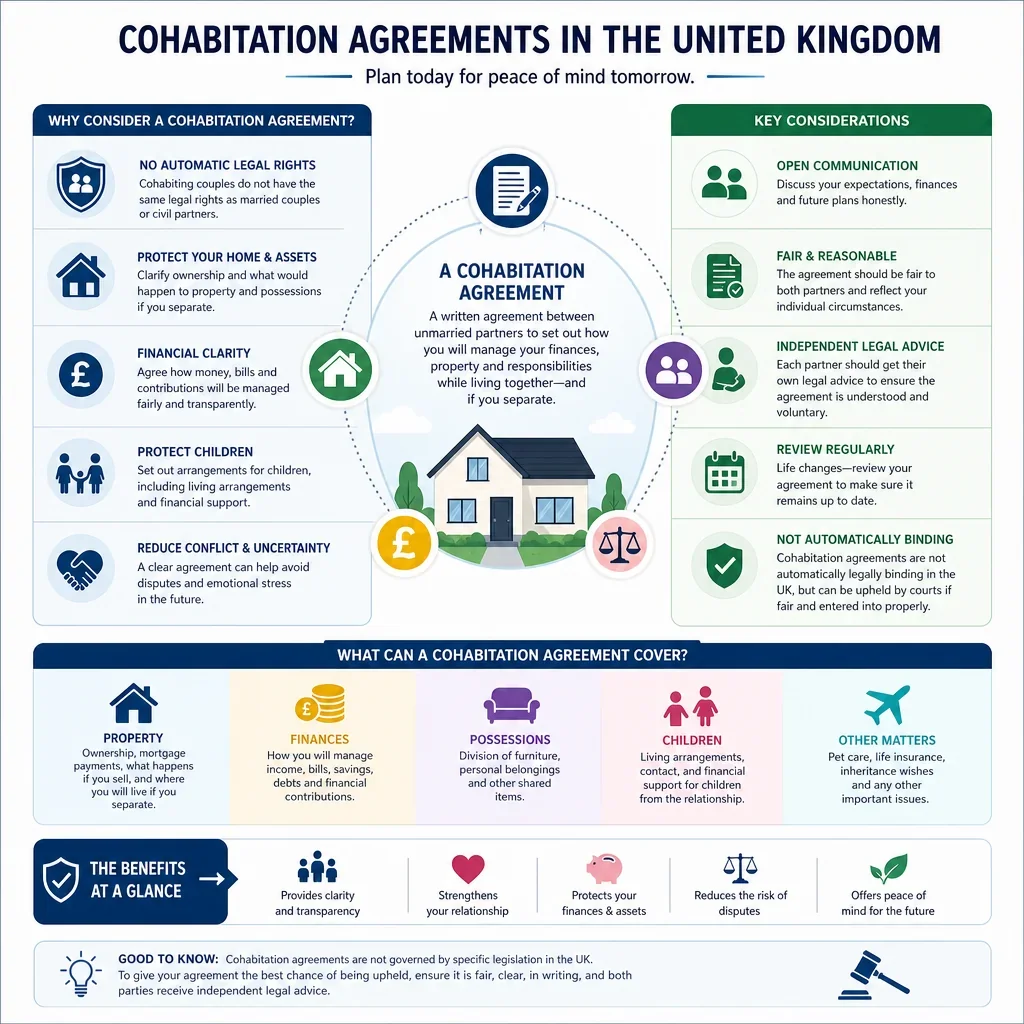

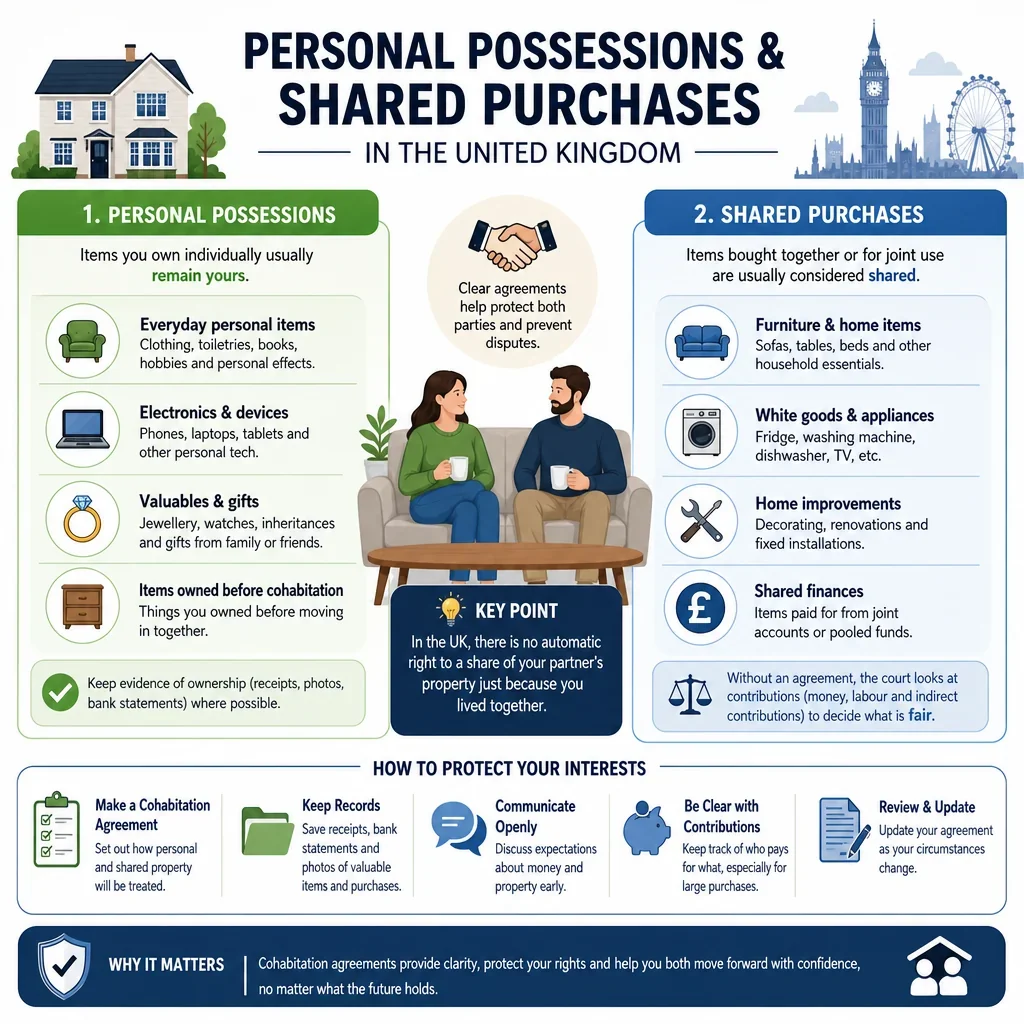

Cohabiting partners do not automatically receive the same property rights as married couples or civil partners. A cohabitation agreement can reduce disputes by stating who owns the home, who is responsible for mortgage and repair costs, and whether contributions create a repayment right, a beneficial share, or no ownership interest.

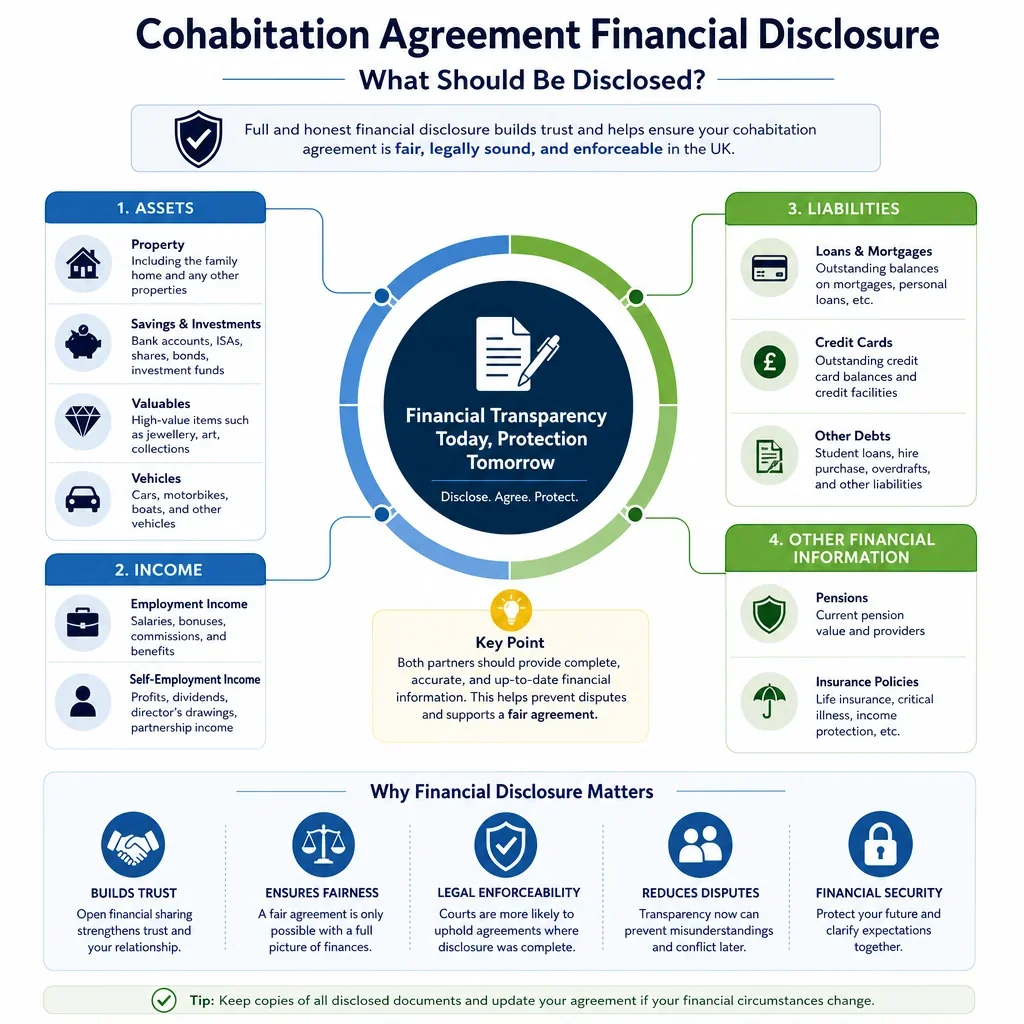

Which Property Contributions Most Need Written Evidence?

- High-risk situations include deposits paid by one partner, unequal mortgage payments, renovations funded by one partner, and family gifts or loans.

- Bank transfers, invoices, loan letters, declarations of trust and solicitor correspondence can be important evidence if ownership or repayment is later disputed.

- Where legal title and contributions differ, partners should record whether they intend equal ownership, unequal shares, reimbursement only, or no beneficial interest.

Do The Rules Differ Across The UK?

Yes. England and Wales often focus on trusts and beneficial ownership principles, Scotland has distinct rules on cohabitants and property claims, and Northern Ireland has its own property and family law context. A UK-wide cohabitation agreement should be adapted to the jurisdiction where the property is located.

What Should A Cohabitation Agreement Say About The Home?

Useful terms include ownership shares, treatment of deposits, mortgage and bill responsibilities, renovation costs, family contributions, buyout rights, sale procedure, valuation method, and what happens if one partner leaves or the relationship ends.

FAQs

You Might Also Be Interested In