United Kingdom Cohabitation Agreement Signing And Execution Checklist

Execution Step | Purpose | Practical Actions | Good Practice Level | Common Pitfalls |

|---|---|---|---|---|

Preparation | ||||

Confirm the document is a cohabitation agreement, not a will, prenup, tenancy, or transfer deed. | Prevents the agreement being used for issues it cannot safely deal with alone. | List the intended topics and identify any separate deeds, wills, or Land Registry forms needed. | Strongly recommended | Trying to change property title, inheritance wishes, or mortgage liability by agreement wording alone. |

State the governing law and intended jurisdiction clearly. | Avoids uncertainty where partners live, own assets, or may move across UK nations. | Specify England and Wales, Scotland, or Northern Ireland as appropriate and take local advice. | Strongly recommended | Assuming one UK legal system applies automatically to all assets and disputes. |

Identify each partner by full legal name, current address, and date of birth. | Reduces doubt about who is bound by the agreement. | Check passports, driving licences, or other ID and match names to property documents. | Recommended | Using nicknames, former names, or addresses that do not match ownership records. |

Check both partners have mental capacity to understand and sign. | Supports validity and reduces later arguments that a party could not consent. | Avoid signing during illness, intoxication, distress, or medication effects seek medical confirmation if needed. | Strongly recommended | Signing when a partner is unwell, impaired, or unable to explain the agreement back. |

Ensure the agreement is negotiated and signed voluntarily. | Reduces the risk of challenge based on pressure, duress, or undue influence. | Allow time, use separate communications, and avoid threats about housing, children, or finances. | Strongly recommended | Presenting a final agreement shortly before a move, purchase, or separation deadline. |

Confirm each partner is an adult with legal ability to contract. | Helps ensure the agreement is enforceable as a contract or deed. | Check both parties are at least 18 or obtain specialist advice if not. | Strongly recommended | Ignoring special rules where one party is under 18. |

Create a clean final version before signature. | Prevents disputes about drafts, amendments, or incomplete pages. | Number pages, lock the file, remove comments, and mark the document as final. | Recommended | Signing a draft with comments, tracked changes, blank schedules, or missing attachments. |

Review | ||||

Check defined terms, dates, property addresses, and schedule references. | Makes the agreement easier to interpret if a dispute arises. | Cross-check every definition, clause number, address, title number, and appendix reference. | Recommended | Leaving inconsistent names, old addresses, undefined terms, or incorrect title numbers. |

Preparation | ||||

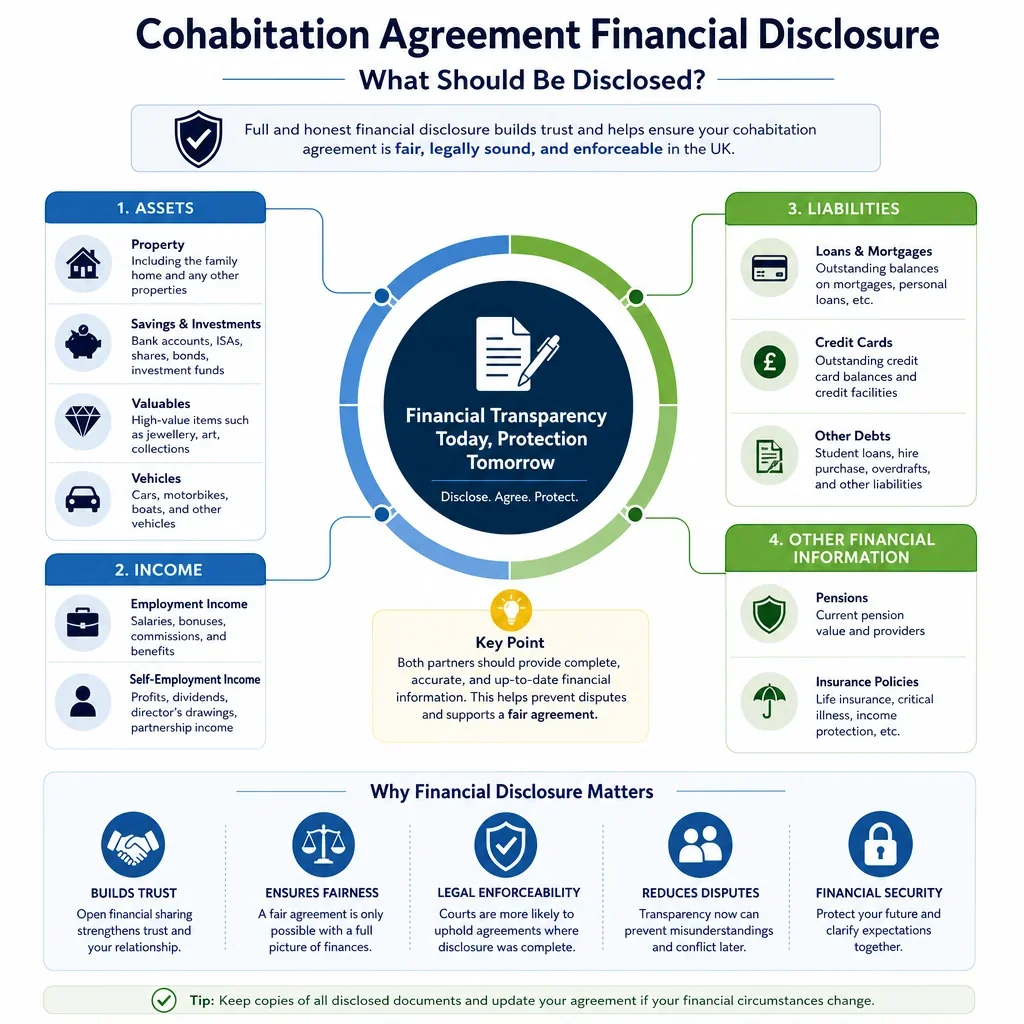

Exchange financial disclosure before signing. | Shows each partner understood the financial context before agreeing terms. | Exchange summaries of assets, debts, income, savings, pensions, property interests, and expected contributions. | Strongly recommended | Hiding debts, omitting pensions, undervaluing assets, or relying only on verbal statements. |

Attach or securely store financial disclosure schedules. | Creates evidence of what was disclosed at the signing date. | Add dated schedules and initial each page or store signed copies with the agreement. | Strongly recommended | Referring to disclosure that cannot later be located or proved. |

Check Land Registry title records for any shared home. | Aligns the agreement with legal ownership and registered restrictions. | Download title register and plan record title number, proprietors, charges, and restrictions. | Strongly recommended | Assuming contribution records match the registered legal title. |

Use a declaration of trust where beneficial property shares need formal recording. | Separates property ownership evidence from broader relationship terms. | Prepare a separate deed or clear trust clause and ensure it matches title and mortgage documents. | May depend on circumstances | Relying on informal emails or unequal contributions without a trust record. |

Check mortgage terms and lender consent requirements. | Avoids breaching mortgage conditions or misunderstanding joint liability. | Review the mortgage offer and ask the conveyancer or lender before signing property-related terms. | May depend on circumstances | Assuming the agreement can release one partner from mortgage liability without lender approval. |

Check any tenancy agreement before signing cohabitation terms. | Avoids conflict between relationship terms and the landlord-tenant contract. | Review rent liability, deposit, permitted occupiers, notices, and ending the tenancy. | May depend on circumstances | Promising a right to stay that the tenancy or landlord does not allow. |

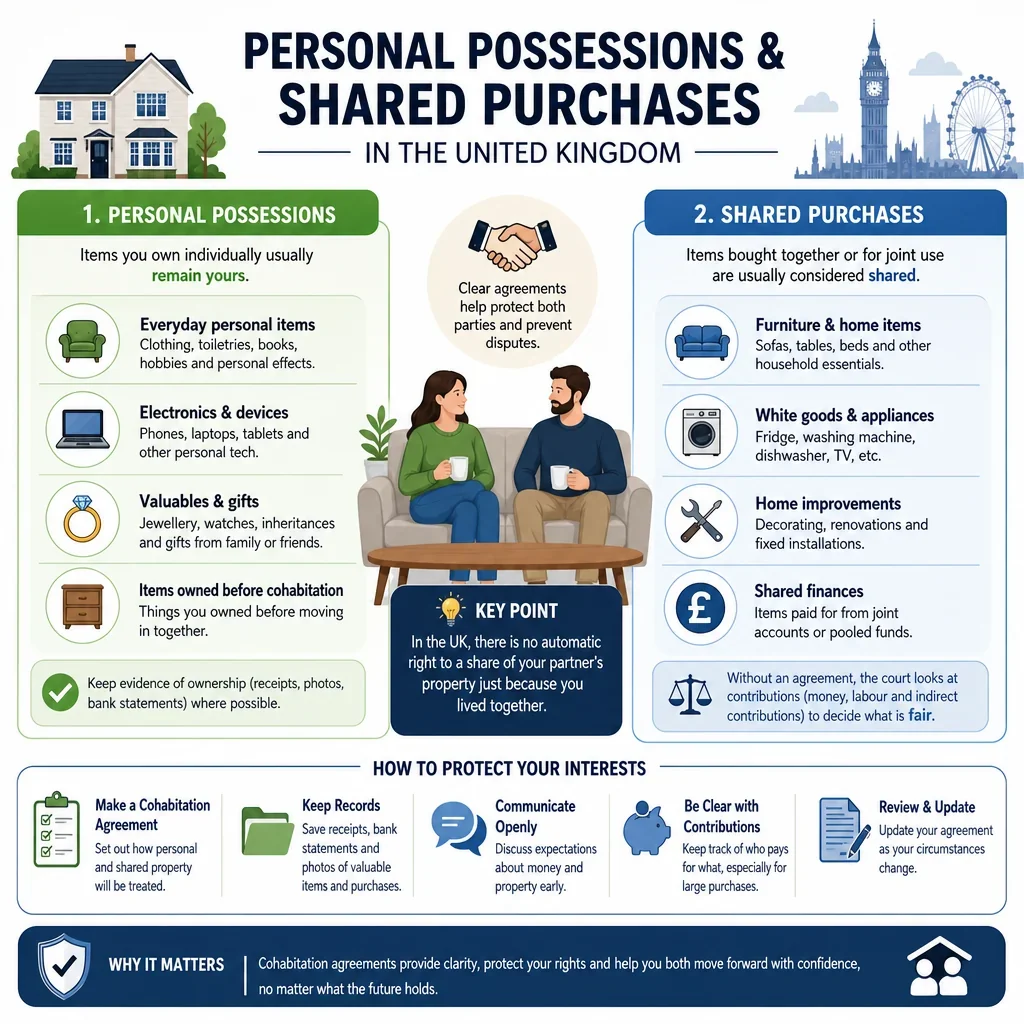

Record agreed contributions to mortgage, rent, bills, repairs, and savings. | Clarifies whether payments create repayment rights, ownership claims, or shared expenses only. | Use a schedule showing amounts, review dates, bank accounts, and treatment on separation. | Recommended | Leaving major contributions undocumented or calling all payments "rent" without explanation. |

Review | ||||

Review any child-related clauses carefully. | Avoids terms that conflict with child welfare principles or statutory child support rules. | Limit clauses to practical intentions and take advice on child maintenance or parenting arrangements. | Strongly recommended | Assuming private clauses can override a court welfare decision or statutory maintenance assessment. |

Do not rely on the agreement to permanently exclude statutory child maintenance. | Reflects that child maintenance may be assessed through the statutory scheme. | Add wording acknowledging that statutory child maintenance rights may still apply. | Strongly recommended | Drafting a clause that says neither parent can ever claim child maintenance. |

Preparation | ||||

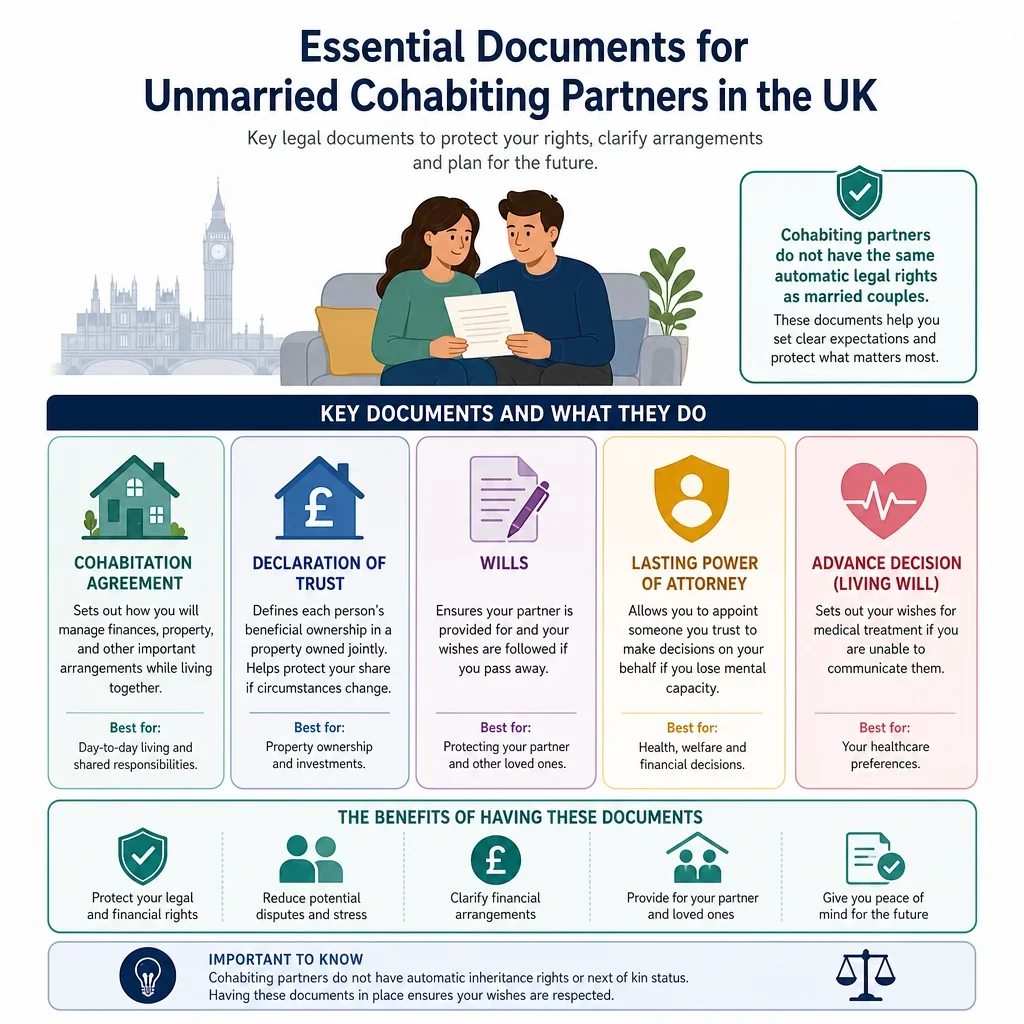

Check whether wills, nominations, and inheritance plans need updating. | Cohabiting partners do not automatically have the same inheritance rights as spouses. | Make or update wills, pension nominations, life policies, and death-in-service nominations. | May depend on circumstances | Assuming a cohabitation agreement works as a will or transfers assets on death. |

Review | ||||

Consider potential claims for reasonable financial provision after death. | Highlights that long-term cohabitants may have possible estate claims in some circumstances. | Take estate planning advice if the agreement addresses death, housing, or financial support. | May depend on circumstances | Ignoring estate claims where partners are financially dependent or have lived together for years. |

Preparation | ||||

Check tax implications of transfers, gifts, shared property, and separation payments. | Prevents unexpected SDLT, CGT, income tax, or inheritance tax consequences. | Ask a tax adviser before agreeing transfers, sale rights, gifts, or occupation payments. | May depend on circumstances | Treating a private agreement as tax-neutral without checking HMRC rules. |

Check whether living together affects benefits or Universal Credit. | Helps partners understand financial consequences of cohabitation beyond the agreement. | Review benefit rules and report changes in household circumstances where required. | May depend on circumstances | Assuming private financial arrangements avoid benefit reporting duties. |

Review | ||||

Review whether each partner understands the agreement in plain English. | Supports informed consent and reduces later misunderstanding. | Ask each partner to explain key clauses, payment obligations, and separation consequences. | Recommended | Signing dense legal wording that one partner has not genuinely understood. |

Arrange translation or interpreter support if needed. | Shows that language barriers did not prevent informed agreement. | Use an independent translator, keep translated copies, and record interpreter details. | May depend on circumstances | Relying on one partner to translate important legal terms for the other. |

Make reasonable adjustments for disability, neurodiversity, or communication needs. | Helps ensure both partners can participate fairly in the signing process. | Use accessible formats, extra time, breaks, support persons, or specialist advice where needed. | May depend on circumstances | Treating accessibility needs as an afterthought on the day of signing. |

Independent advice | ||||

Each partner should obtain separate independent legal advice. | Reduces challenges based on lack of understanding, unfairness, or pressure. | Use different solicitors and ensure advice is given before signature. | Strongly recommended | Using one solicitor for both partners or getting advice only after signing. |

Keep evidence that independent legal advice was given. | Creates a paper trail if the agreement is later challenged. | Ask each solicitor for a short advice certificate or retain advice letters securely. | Strongly recommended | Being unable to prove what advice was given or when it was received. |

Ensure advisers are independent and free from conflicts of interest. | Protects the reliability of the advice and the fairness of the process. | Use separate firms where possible and disclose any prior adviser relationship. | Recommended | One adviser acting for both parties where interests may differ. |

Review | ||||

Allow a reasonable review period before signing. | Helps show consent was considered, not rushed or pressured. | Circulate the final draft days or weeks before signing, especially before major transactions. | Strongly recommended | Signing on completion day, moving day, or after one partner has already relied on the terms. |

Confirm there are no undisclosed side agreements or promises. | Reduces later disputes about verbal assurances outside the written document. | Include an entire agreement clause and list any linked documents explicitly. | Recommended | Relying on text messages, conversations, or family promises not reflected in the agreement. |

Remove clauses that attempt to waive non-waivable legal rights or encourage illegality. | Improves the chance that the remaining agreement is respected. | Ask solicitors to check exclusion clauses, child support terms, tax wording, and occupation rights. | Strongly recommended | Including extreme terms that may undermine the whole document. |

Include a severance clause for invalid or unenforceable provisions. | May preserve valid parts if one clause fails. | Add concise wording allowing invalid provisions to be removed where legally possible. | Recommended | Assuming a severance clause can save an agreement with fundamentally unfair or unclear terms. |

Preparation | ||||

Decide whether the agreement should be executed as a deed. | A deed may be appropriate for property promises, declarations, or no-consideration obligations. | Ask a solicitor whether deed execution is needed and use deed wording if chosen. | May depend on circumstances | Calling a document a deed without meeting deed execution requirements. |

Signing | ||||

If using a deed, state clearly that it is executed and delivered as a deed. | Supports compliance with deed formalities in England and Wales. | Use an execution block stating "signed as a deed" and "delivered on the date above". | Strongly recommended | Using ordinary contract wording where a deed is intended. |

Sign in the correct signature blocks only after all schedules are complete. | Creates clear evidence that the final complete document was accepted. | Sign the execution page, initial schedules if desired, and avoid signing loose replacement pages later. | Recommended | Signing before blanks, figures, or schedules are finalised. |

Date the agreement accurately when it becomes effective. | Clarifies commencement, disclosure timing, and review triggers. | Insert the completion date only once all parties have signed and any delivery requirement is met. | Recommended | Backdating, leaving the date blank, or using different dates on copies without explanation. |

Use wet-ink signatures where a simple, low-risk execution method is preferred. | Provides straightforward evidence of signature and witnessing. | Print the full final document, sign in ink, and keep the original signed version. | May depend on circumstances | Printing different versions for each party or losing the signed original. |

Use electronic signatures only with a reliable process. | Electronic signatures can be valid, but evidence and witnessing must be managed carefully. | Use an audit-trail platform, confirm signer identity, and retain completion certificates. | May depend on circumstances | Using informal image signatures without identity checks or audit evidence. |

Witnessing | ||||

If electronically signing a deed, arrange physical witness presence. | In England and Wales, deed witnessing generally still requires the witness to be present. | Have the witness watch the signer apply the e-signature and then sign the attestation. | Strongly recommended | Witnessing remotely by video call where formal physical presence is required. |

Use an independent adult witness for each deed signature. | Supports formal execution and reduces suspicion of improper signing. | Choose a neutral adult who is not the other partner and has no benefit under the agreement. | Strongly recommended | Using the other partner, a child, a beneficiary, or someone not actually present. |

Record full witness details beside each witnessed signature. | Makes it easier to prove execution if the witness is later needed. | Ask the witness to add full name, address, occupation, signature, and date. | Recommended | Unreadable signatures, missing addresses, or witnesses who cannot later be traced. |

Ensure the witness sees the party sign. | Helps satisfy attestation requirements for an individual executing a deed. | Sign while the witness is physically present and have the witness sign immediately after. | Strongly recommended | Asking a witness to sign later after being told the document was already signed. |

Signing | ||||

State whether counterparts are permitted if parties sign separate copies. | Avoids uncertainty where partners sign at different locations or times. | Include a counterparts clause and collate all signed counterparts into one complete record. | May depend on circumstances | Keeping mismatched signed copies with different schedules or dates. |

Avoid handwritten amendments if unavoidable, initial every change. | Prevents disputes about whether post-signature changes were agreed. | Reprint the final version instead if a change is made, both parties and witnesses should initial it. | Recommended | Making margin changes after one person has already signed. |

Use a controlled signing order and checklist. | Reduces missing signatures, un-witnessed signatures, and incomplete copies. | Check final version, signatures, witnesses, dates, schedules, and delivery before closing the signing meeting. | Recommended | Discovering later that one signature, witness detail, or schedule was missed. |

If executed as a deed, confirm delivery of the deed. | A deed must be delivered to take effect. | Include delivery wording and record whether delivery is immediate or conditional. | Strongly recommended | Signing a deed but leaving no evidence of when it was delivered or effective. |

Witnessing | ||||

Do not treat a witness as a legal adviser. | Keeps witnessing separate from advice and consent issues. | Use solicitors for advice and witnesses only to confirm signature and presence. | Recommended | Assuming a witnessed signature proves fairness, disclosure, or legal advice. |

Signing | ||||

Verify signer identity at or before signing. | Reduces fraud risk and strengthens evidence of execution. | Check photo ID and proof of address, especially for remote or electronic signing. | Recommended | Relying on email access alone to prove who signed. |

Storage | ||||

Handle financial documents and ID securely. | Protects sensitive personal and financial data exchanged for the agreement. | Use encrypted storage, limit sharing, and delete unnecessary duplicate files. | Recommended | Emailing passports, bank statements, and valuations without secure handling. |

Store the signed original securely. | Ensures the agreement can be produced if needed. | Keep the original with a solicitor, secure home file, safe, or document storage provider. | Strongly recommended | Only keeping an unsigned PDF or losing schedules attached to the original. |

Give each partner a complete signed copy. | Ensures both partners can check their rights and obligations later. | Provide identical PDFs or photocopies including signatures, witness details, and schedules. | Recommended | One partner keeping the only copy or copies missing annexes. |

Maintain clear version control after signing. | Prevents confusion between drafts, signed copies, and later amendments. | Label the signed version, archive drafts separately, and record amendment dates. | Recommended | Relying on a newer unsigned draft instead of the executed agreement. |

Store advice letters, disclosure records, and negotiation history with the agreement. | Preserves evidence of fairness, disclosure, and informed consent. | Keep key emails, disclosure schedules, valuations, advice certificates, and signing notes. | Strongly recommended | Keeping the agreement but deleting the evidence that made it reliable. |

Share the agreement only with relevant advisers or institutions where necessary. | Balances confidentiality with practical implementation. | Provide extracts or copies to solicitors, conveyancers, accountants, or executors where relevant. | May depend on circumstances | Oversharing sensitive terms or failing to tell a conveyancer about property provisions. |

Future review | ||||

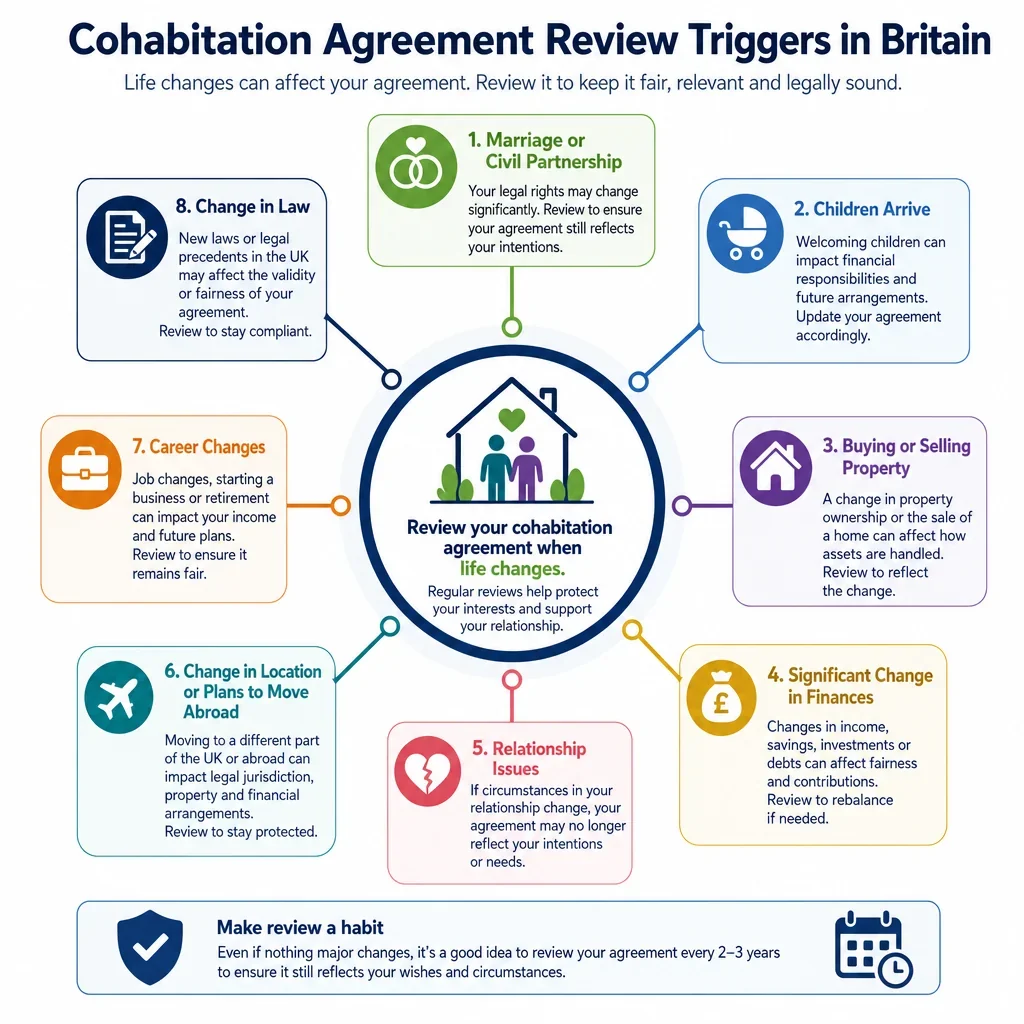

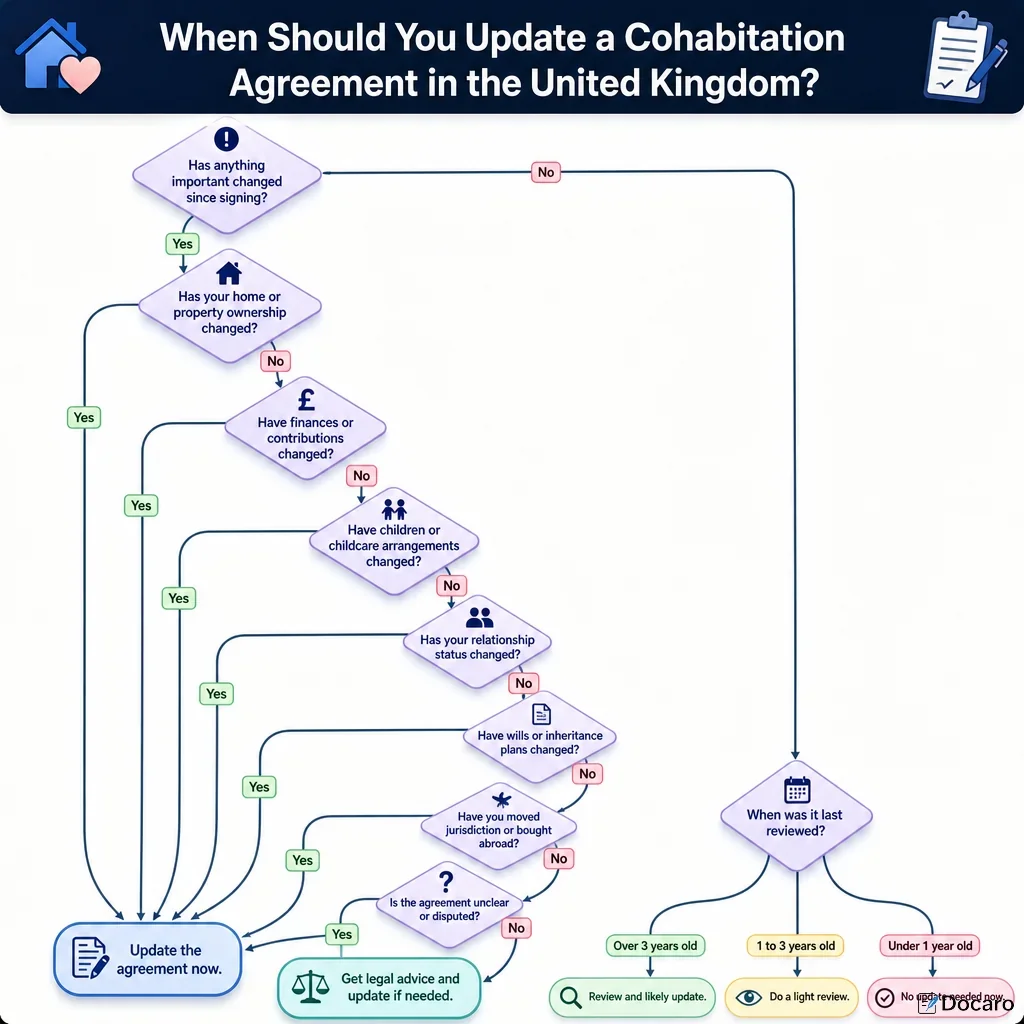

Amend the agreement using a signed written variation. | Keeps changes clear and prevents informal variations being disputed. | Prepare a deed of variation or written amendment and sign with the same care as the original. | Strongly recommended | Changing important terms by text message, verbal agreement, or marked-up copy only. |

Schedule periodic reviews of the agreement. | Keeps terms aligned with current finances, property, and family circumstances. | Review every 2 to 3 years or at another agreed interval. | Recommended | Relying on an old agreement after circumstances have materially changed. |

Review the agreement before or after buying a home together. | Property ownership and mortgage liability often change the risk profile. | Update title references, contributions, sale rights, mortgage terms, and trust declarations. | Strongly recommended | Keeping pre-purchase wording that no longer reflects ownership or funding. |

Review the agreement when children are born, adopted, or move into the household. | Children can affect housing needs, financial dependency, and practical fairness. | Reconsider housing, childcare costs, work changes, child maintenance, and emergency arrangements. | Strongly recommended | Leaving child-related consequences to clauses drafted before the child existed. |

Review the agreement before marriage or civil partnership. | Marriage or civil partnership changes financial rights and may require a prenup or postnup. | Take family law advice and consider replacing or supplementing it with a nuptial agreement. | Strongly recommended | Assuming cohabitation terms will govern divorce or dissolution finances unchanged. |

Use the agreement as a reference point on separation, but take advice before acting. | Helps implement agreed exit arrangements while avoiding unlawful self-help. | Check notice, occupation, sale, debt, and dispute resolution clauses before taking steps. | Recommended | Changing locks, withholding property, or stopping payments without checking legal rights. |

Review after inheritance, redundancy, disability, business sale, or major income change. | Significant changes may affect fairness and reliance on the original disclosure. | Update disclosure, contributions, support arrangements, and property improvement funding. | May depend on circumstances | Letting one partner rely financially on outdated assumptions for years. |

Review after major renovations or unequal capital contributions. | Clarifies whether improvements affect ownership, reimbursement, or sale proceeds. | Record funding source, invoices, agreed effect, and whether a trust deed update is needed. | Recommended | Assuming paying for renovations automatically changes beneficial shares. |

Review | ||||

Check the dispute resolution process before signing. | Provides a practical route for disagreements without immediate litigation. | Include negotiation, mediation, expert valuation, and court fallback wording as appropriate. | Recommended | Making mediation mandatory in urgent property, safety, or injunction situations. |

Agree valuation methods for property, businesses, or valuable items. | Reduces disputes about buyouts, sale prices, and reimbursement amounts. | Specify independent valuers, valuation date, cost sharing, and what happens if values differ. | May depend on circumstances | Using vague wording such as "market value" without a process. |

Record arrangements for pets and valuable personal belongings. | Avoids emotional disputes over non-property-title items. | List ownership, care costs, insurance, microchip details, and collection arrangements. | May depend on circumstances | Assuming informal pet care promises will be easy to enforce. |

Check clauses affecting businesses, shares, or partnerships. | Prevents relationship terms conflicting with company or partnership documents. | Review articles, shareholder agreements, partnership deeds, loans, and director guarantees. | May depend on circumstances | Promising share transfers that company documents or tax advice do not support. |

Preparation | ||||

Record responsibility for debts, loans, overdrafts, and guarantees. | Clarifies internal responsibility even where creditors can still pursue liable borrowers. | List debts, account numbers, borrowers, guarantors, payment responsibility, and indemnity terms. | Recommended | Assuming the agreement binds banks, lenders, landlords, or credit card providers. |

Set rules for joint accounts and shared savings. | Reduces disputes over withdrawals, overdrafts, and remaining balances. | Agree permitted use, contribution amounts, withdrawal limits, closure, and separation balance split. | May depend on circumstances | One partner emptying the account or creating an overdraft before separation terms are applied. |

Check insurance policies linked to the agreement. | Ensures life, home, contents, and income protection cover matches financial promises. | Review policyholders, beneficiaries, insured values, premium responsibility, and cancellation rights. | May depend on circumstances | Promising financial protection but not maintaining the policy needed to fund it. |

Review pension nominations and survivor benefit forms. | Cohabiting partners may need nominations to access pension death benefits. | File or update expression of wish forms and keep copies with estate documents. | May depend on circumstances | Assuming the cohabitation agreement automatically redirects pension death benefits. |

Review | ||||

Check clauses about who can stay in or leave the home. | Housing terms must be practical and should not ignore court powers or safety issues. | Take advice on occupation, notice periods, domestic abuse risk, and court orders if relevant. | Strongly recommended | Assuming a private agreement allows immediate eviction or lock changes. |

Preparation | ||||

Screen for domestic abuse, coercive control, or financial abuse before signing. | Protects consent and safety where one partner may be pressured or controlled. | Use separate advice appointments and pause signing if pressure, fear, or control is identified. | Strongly recommended | Signing jointly in circumstances where one partner cannot speak freely. |

Signing | ||||

Plan remote signing logistics before the signing date. | Avoids execution defects where parties are in different places. | Agree platform, counterpart wording, witness arrangements, file naming, and completion steps. | May depend on circumstances | Assuming a video call alone solves witnessing, identity, or delivery issues. |

Remove blanks and incomplete schedules before signing. | Prevents later insertion of disputed terms, figures, or assets. | Insert "not applicable" where needed and confirm all figures and schedules are complete. | Strongly recommended | Signing with blank contribution amounts, missing property details, or empty asset lists. |

Protect page integrity of the signed document. | Reduces risk of page substitution after signature. | Number pages "page X of Y", staple or bind originals, and initial key schedules if desired. | Recommended | Loose unsigned pages that can be replaced without detection. |

Storage | ||||

Keep an execution audit trail. | Helps prove who signed, when, how, and on what version. | Keep completion emails, e-sign certificates, witness details, and signed PDF metadata. | Recommended | Downloading only a flattened PDF and losing the signing certificate or audit log. |

Consider whether any Land Registry restriction is needed. | May help protect recorded beneficial interests in registered land. | Ask a conveyancer whether a Form A or other restriction is appropriate. | May depend on circumstances | Assuming a private agreement is visible to buyers, lenders, or the Land Registry. |

Tell executors or attorneys where the agreement is stored if death or incapacity clauses matter. | Ensures the document can be found when needed. | Record storage location with wills, LPAs, and emergency financial documents. | May depend on circumstances | A carefully signed agreement being undiscoverable after death or incapacity. |

Review | ||||

Check consistency with any lasting power of attorney arrangements. | Avoids practical conflict if a partner later loses capacity. | Review LPAs, attorney powers, home occupation plans, and financial management clauses. | May depend on circumstances | Assuming a cohabitation agreement lets a partner manage finances without an LPA. |

Preparation | ||||

For Scotland, check Scottish execution and cohabitant rights rules. | Scotland has distinct cohabitant claim rules and signing practice. | Use a Scottish solicitor for agreements governed by Scots law or involving Scottish property. | Strongly recommended | Using an England and Wales template for Scottish property or Scots law rights. |

For Northern Ireland, take local advice on property, family, and deed execution rules. | Northern Ireland has separate courts, legislation, and property practice. | Use a Northern Ireland solicitor if either partner lives there or relevant property is there. | Strongly recommended | Assuming England and Wales procedures apply throughout the UK. |

Signing | ||||

Consider notarial or local formalities for overseas assets or foreign residence. | Helps avoid problems where the agreement must be recognised abroad. | Take local legal advice and use a notary or apostille if required for foreign use. | May depend on circumstances | Assuming a UK-signed document automatically affects overseas property or bank accounts. |

Review | ||||

Have any AI-generated draft reviewed before signing. | Checks that the draft reflects the parties, assets, jurisdiction, and current law. | Give the draft, disclosure, and instructions to separate solicitors for review. | Strongly recommended | Signing generated wording without checking enforceability, omissions, or local law fit. |

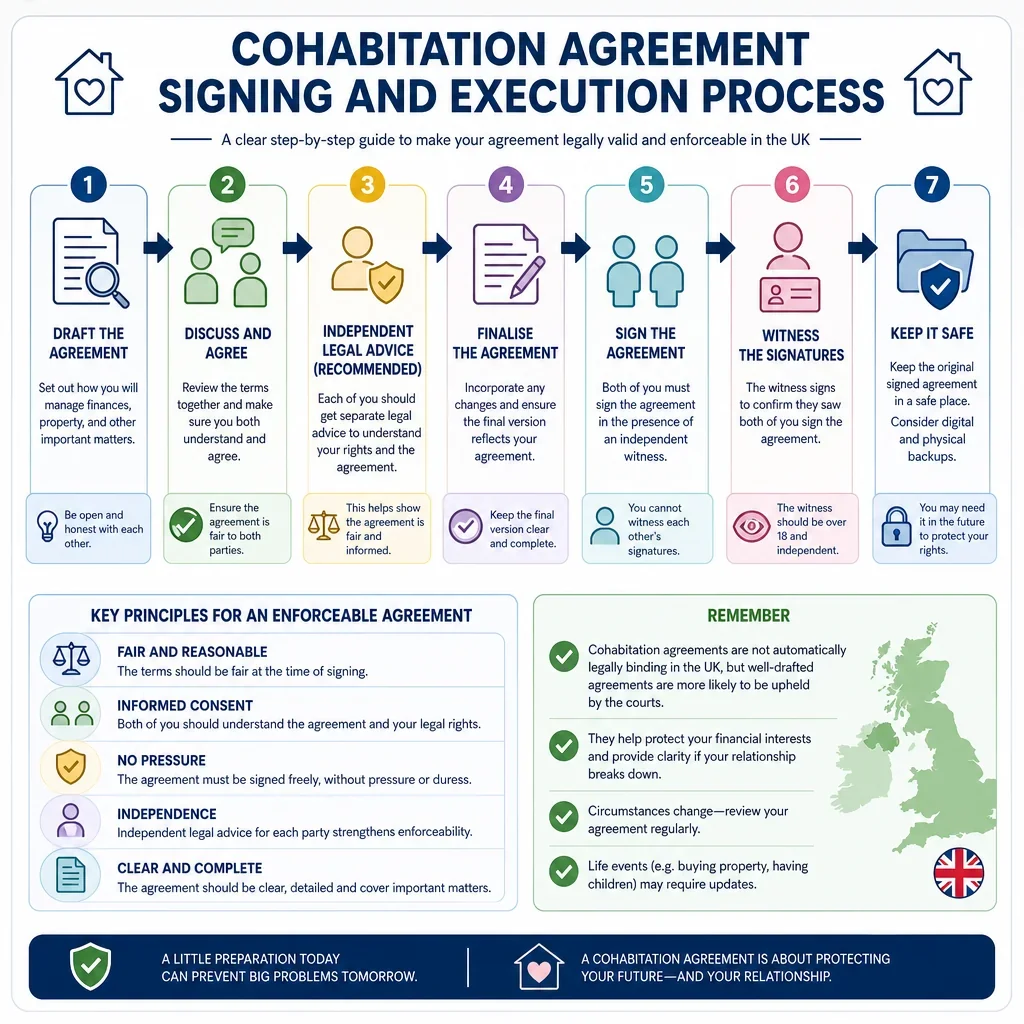

How Should A Cohabitation Agreement Be Signed In The UK?

A cohabitation agreement is more reliable if each partner signs only after full financial disclosure, enough time to review the terms, and separate legal advice. Unlike a will, there is no single statutory signing formula for a cohabitation agreement, so the focus is on showing ordinary contract requirements: clear terms, genuine consent, fairness, and proper evidence of execution.

Does A Cohabitation Agreement Need Independent Legal Advice?

Independent legal advice is strongly recommended. It helps reduce later arguments about pressure, misunderstanding, unfairness, or one partner not appreciating the effect of the agreement. Each partner should ideally use a different solicitor, receive advice before signing, and keep evidence of that advice with the signed agreement.

Who Should Witness A Cohabitation Agreement?

If the agreement is executed as a deed, each signature should be witnessed by an independent adult who is physically present when the party signs. A witness should not be the other partner, a beneficiary under the agreement, or someone with an obvious conflict. The witness should add their full name, address, occupation, and signature.

What Practical Steps Reduce The Risk Of A Future Dispute?

- Do not sign under pressure: build in a cooling-off period and avoid last-minute signing before a house purchase, birth, or wedding.

- Record disclosure: attach or keep schedules of assets, liabilities, income, property contributions, and pension interests where relevant.

- Use wet-ink or carefully managed electronic signing: deeds may be signed electronically in England and Wales if formalities are met, but witnessing still requires care.

- Keep originals safely: each partner should have a complete signed copy, with any deed originals stored securely.

- Review after major changes: property purchases, children, major renovations, separation, illness, or large inheritance can make old terms unreliable or unfair.

FAQs

You Might Also Be Interested In