AI Generated British Promissory Note

PDF & Word - 2026 Updated

Docaro Pricing

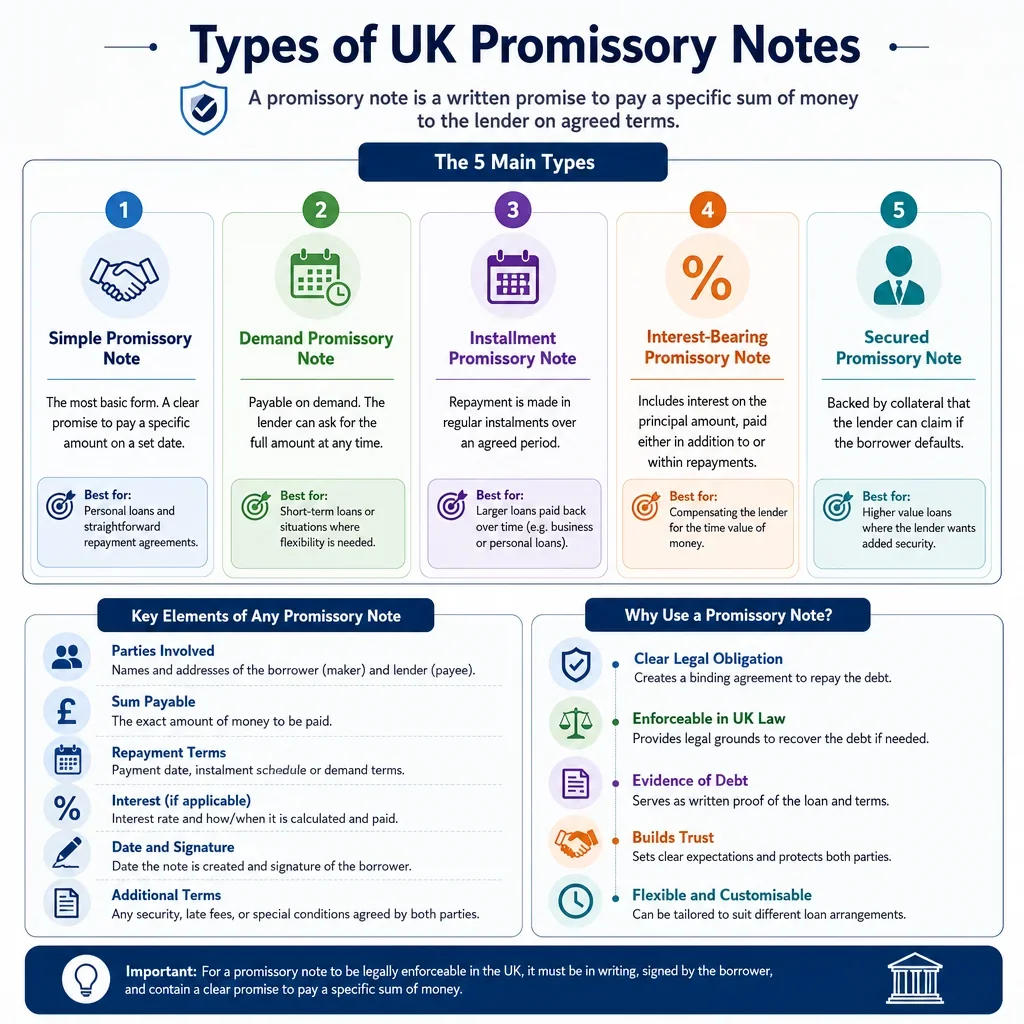

When do you need a Promissory Note in the United Kingdom?

British Legal Rules for a Promissory Note

Using the wrong structure for a promissory note can render it unenforceable or lead to unintended legal obligations under UK law.

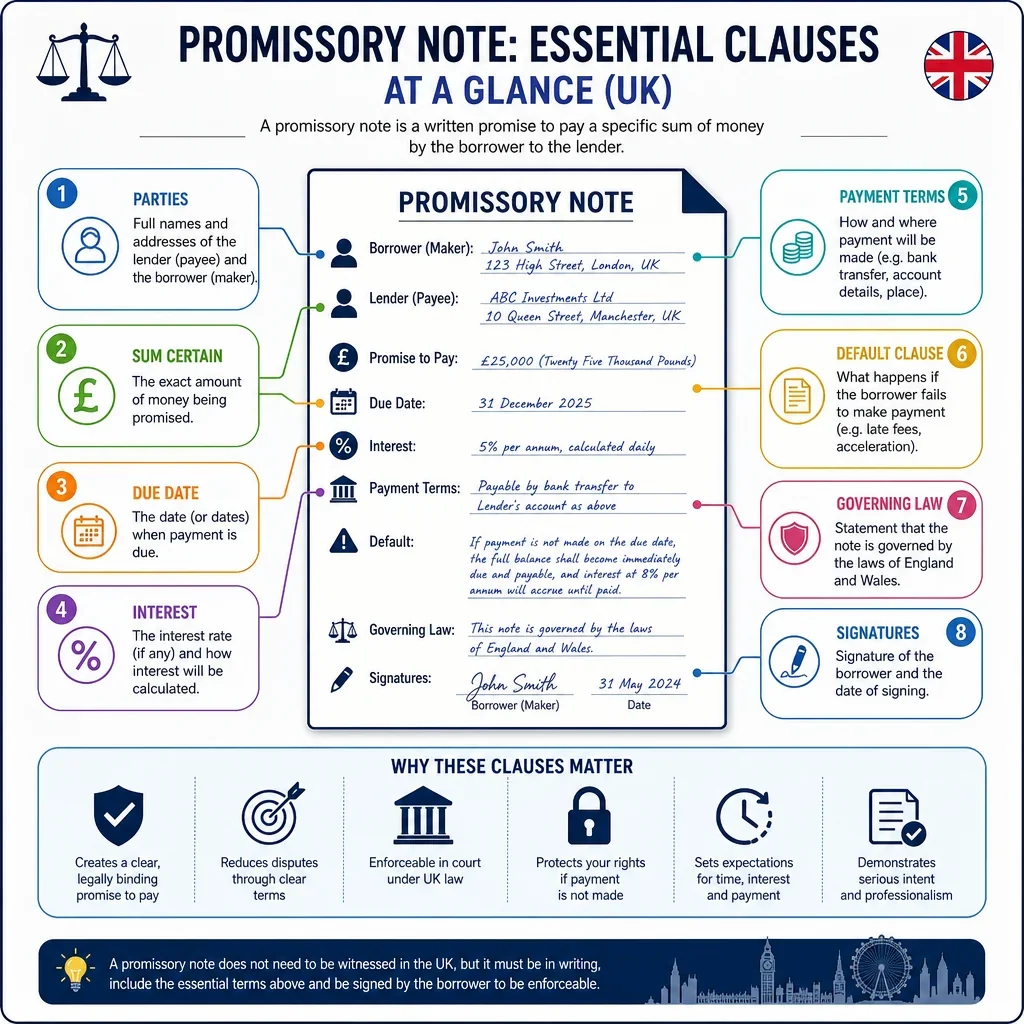

What a Proper Promissory Note Should Include

- Parties InvolvedClearly state the names and contact details of the lender and borrower to identify who is making and receiving the payment.

- Loan AmountSpecify the exact sum of money being borrowed, including the currency, to avoid any confusion over the principal amount.

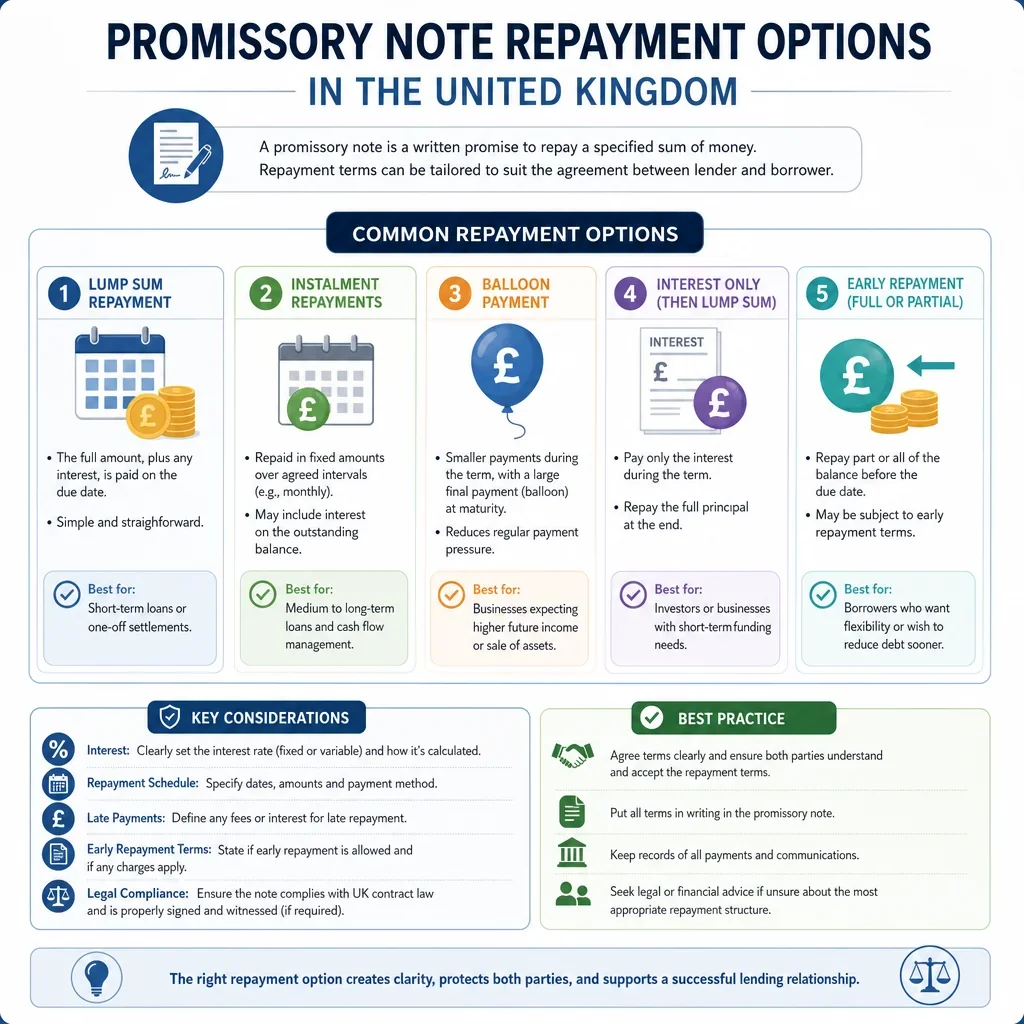

- Repayment DateSet a clear due date by which the full amount must be repaid, or outline a schedule for instalments if applicable.

- Interest DetailsDescribe if any interest will be charged, the rate, and how it will be calculated on the outstanding amount.

- Payment MethodIndicate how the repayment will be made, such as by bank transfer, cheque, or cash, and where to send it.

- Default ConsequencesExplain what happens if payments are late, like extra fees or legal action, to encourage timely repayment.

- SignaturesInclude spaces for both the lender and borrower to sign and date the document, making it legally binding.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Promissory Note Template

Below is a free template example of a Promissory Note for use in the United Kingdom generated by our AI model.

The clauses in your actual Promissory Note will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Promissory Note

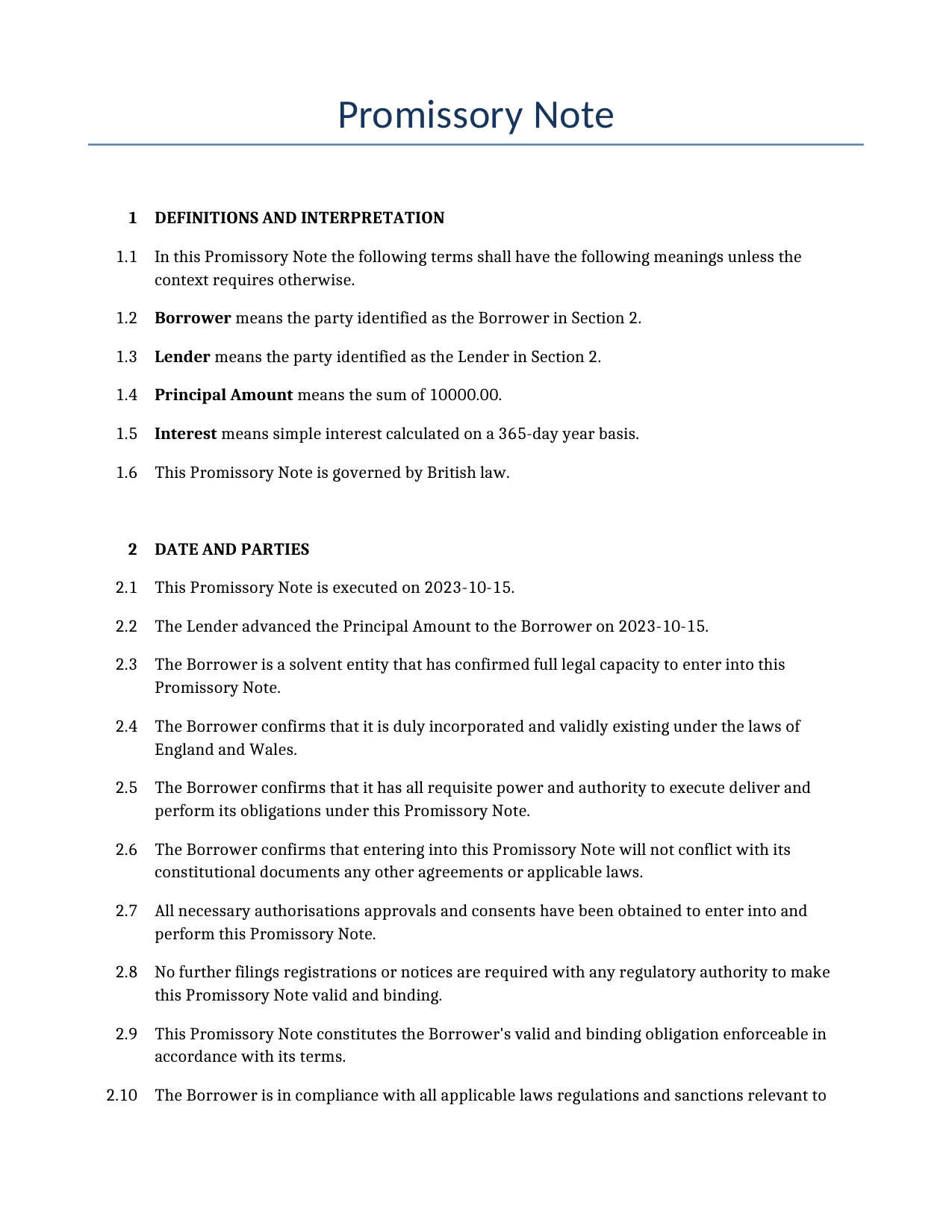

1DEFINITIONS AND INTERPRETATION

In this Promissory Note the following terms shall have the following meanings unless the context requires otherwise.

Borrower means the party identified as the Borrower in Section 2.

Lender means the party identified as the Lender in Section 2.

Principal Amount means the sum of 10000.00.

Interest means simple interest calculated on a 365-day year basis.

This Promissory Note is governed by British law.

2DATE AND PARTIES

This Promissory Note is executed on 2023-10-15.

The Lender advanced the Principal Amount to the Borrower on 2023-10-15.

The Borrower is a solvent entity that has confirmed full legal capacity to enter into this Promissory Note.

The Borrower confirms that it is duly incorporated and validly existing under the laws of England and Wales.

The Borrower confirms that it has all requisite power and authority to execute deliver and perform its obligations under this Promissory Note.

The Borrower confirms that entering into this Promissory Note will not conflict with its constitutional documents any other agreements or applicable laws.

All necessary authorisations approvals and consents have been obtained to enter into and perform this Promissory Note.

No further filings registrations or notices are required with any regulatory authority to make this Promissory Note valid and binding.

This Promissory Note constitutes the Borrower's valid and binding obligation enforceable in accordance with its terms.

The Borrower is in compliance with all applicable laws regulations and sanctions relevant to entering into this Promissory Note.

There are no pending or threatened legal proceedings that could materially affect the Borrower's ability to perform under this Promissory Note.

3PROMISE TO PAY

The Borrower hereby promises to pay to the Lender the Principal Amount together with Interest in accordance with the terms of this Promissory Note.

Interest shall accrue on the Principal Amount at the rate specified in Section 4 from 2024-01-01.

4INTEREST

Interest shall be simple interest calculated on a 365-day year basis.

Interest shall be payable in accordance with the Repayment Terms set out in Section 5.

5REPAYMENT TERMS

The Borrower shall repay the Principal Amount and Interest in instalments.

The repayment schedule shall commence on 2024-01-01.

The repayment shall be fully completed by 2024-12-31.

The total amount of the full repayment shall be 1050.0.

6PREPAYMENT

The Borrower may make prepayments of the Principal Amount or Interest under this Promissory Note.

7LATE PAYMENT CHARGES

A grace period shall apply for late payments by the Borrower.

8DEFAULT AND REMEDIES

The following events shall constitute a default by the Borrower namely failure to pay principal or interest and insolvency or bankruptcy.

Upon default by the Borrower the entire debt shall become immediately due.

The Lender is authorised to take legal action to recover the debt upon default.

The Lender shall give notice to the Borrower before enforcing remedies.

9COSTS AND EXPENSES

The Borrower shall pay the Lender's reasonable costs and expenses including legal fees court fees and collection agency fees.

The Borrower shall pay such costs immediately upon the Lender's demand.

10FORCE MAJEURE

Neither party shall be liable for any failure to perform its obligations under this Promissory Note if such failure is caused by a force majeure event including acts of God pandemics or epidemics or government actions.

The affected party shall provide written notice of a force majeure event within a specified period.

The affected party shall take reasonable steps to mitigate the effects of the force majeure event.

This force majeure clause shall apply symmetrically to both the Borrower and the Lender.

11REPRESENTATIONS AND WARRANTIES

The Borrower represents and warrants that all statements set out in Section 2 are true and accurate as at the date of this Promissory Note.

12CONFIDENTIALITY

The Lender and the Borrower shall keep the terms of this Promissory Note confidential.

13ASSIGNMENT

The Lender may assign or transfer this Promissory Note to another party with prior notice and only to financial institutions.

The Borrower shall not assign or transfer its obligations under this Promissory Note.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Promissory Note in the United Kingdom

United Kingdom Reference Legislation

Promissory Note FAQs

Document Generation FAQs

Related Articles