AI Generated British Personal Guarantee

PDF & Word - 2026 Updated

Docaro Pricing

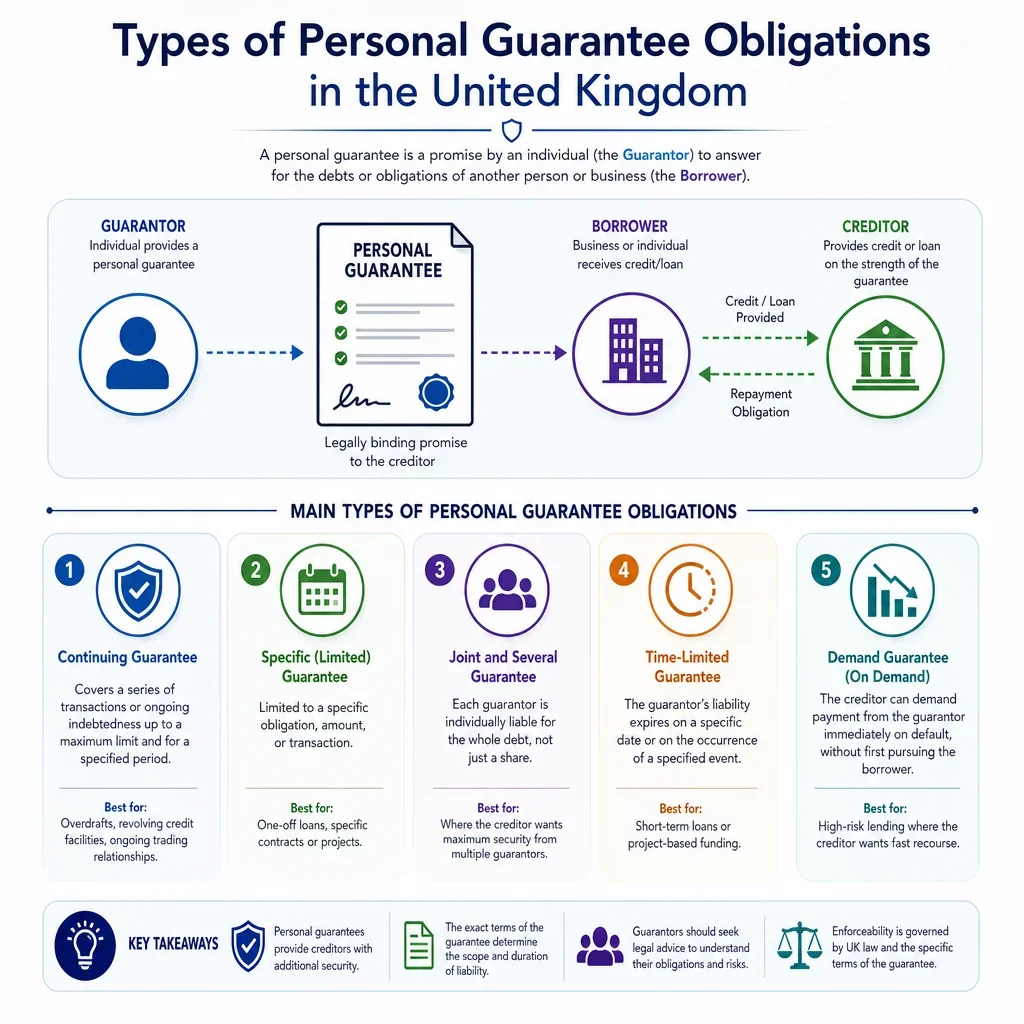

When do you need a Personal Guarantee in the United Kingdom?

British Legal Rules for a Personal Guarantee

Using the wrong type of guarantee agreement can expose the guarantor to unlimited liability or render the document unenforceable.

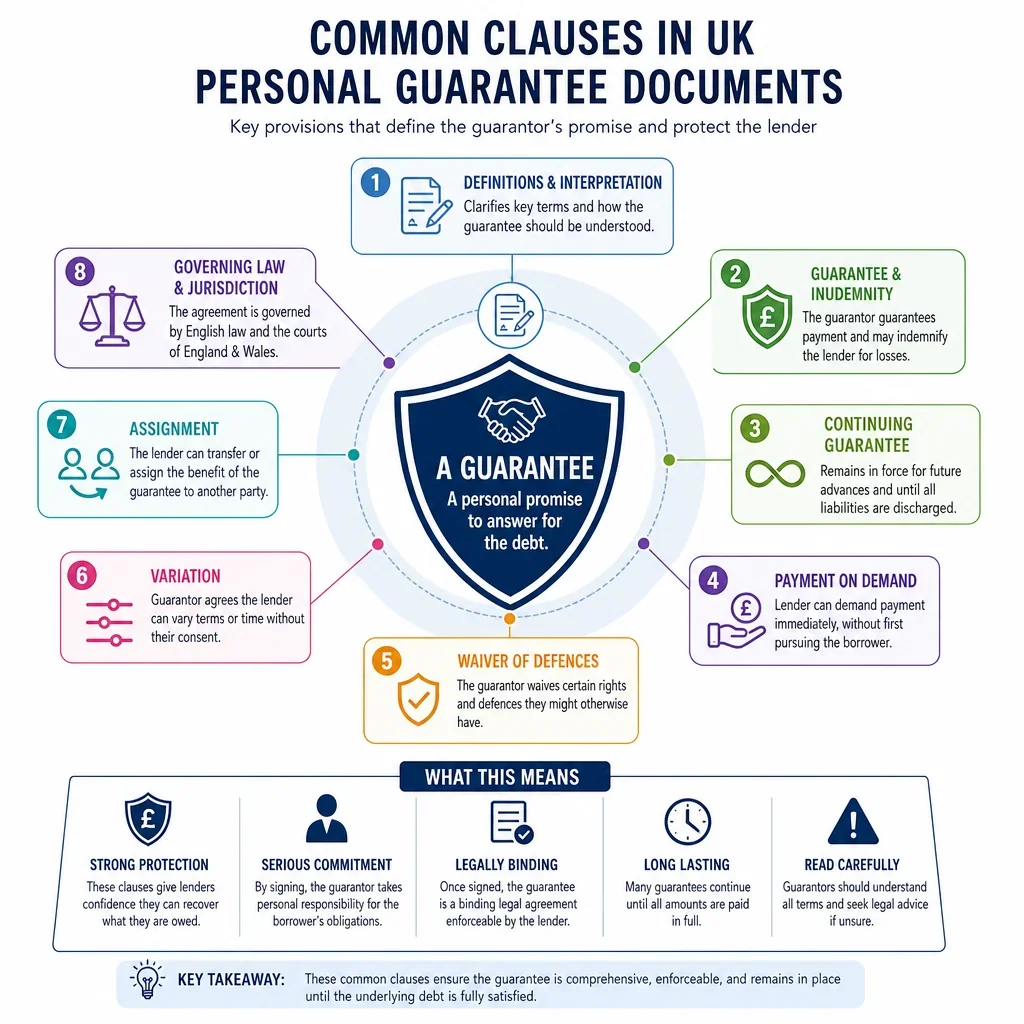

What a Proper Personal Guarantee Should Include

- Guarantor's IdentityClearly state the full name, address, and contact details of the person providing the guarantee.

- Guaranteed DebtSpecify the exact loan or debt amount, including any interest or fees, that the guarantor is responsible for.

- Borrower's DetailsIdentify the borrower, including their name and any relevant business or personal information.

- Guarantee TypeExplain whether the guarantee is limited to a certain amount or covers all obligations, and if it's continuing for future debts.

- Trigger for PaymentDescribe when the guarantor must step in to pay, such as if the borrower defaults on payments.

- Duration and EndSet out how long the guarantee lasts and under what conditions it can be cancelled or revoked.

- Rights of the CreditorOutline the lender's rights to demand payment from the guarantor and pursue legal action if needed.

- Legal JurisdictionState that the agreement follows UK law and specify the courts that handle any disputes.

- SignaturesRequire signatures from the guarantor, borrower, and lender to make the document legally binding.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Personal Guarantee Template

Below is a free template example of a Personal Guarantee for use in the United Kingdom generated by our AI model.

The clauses in your actual Personal Guarantee will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

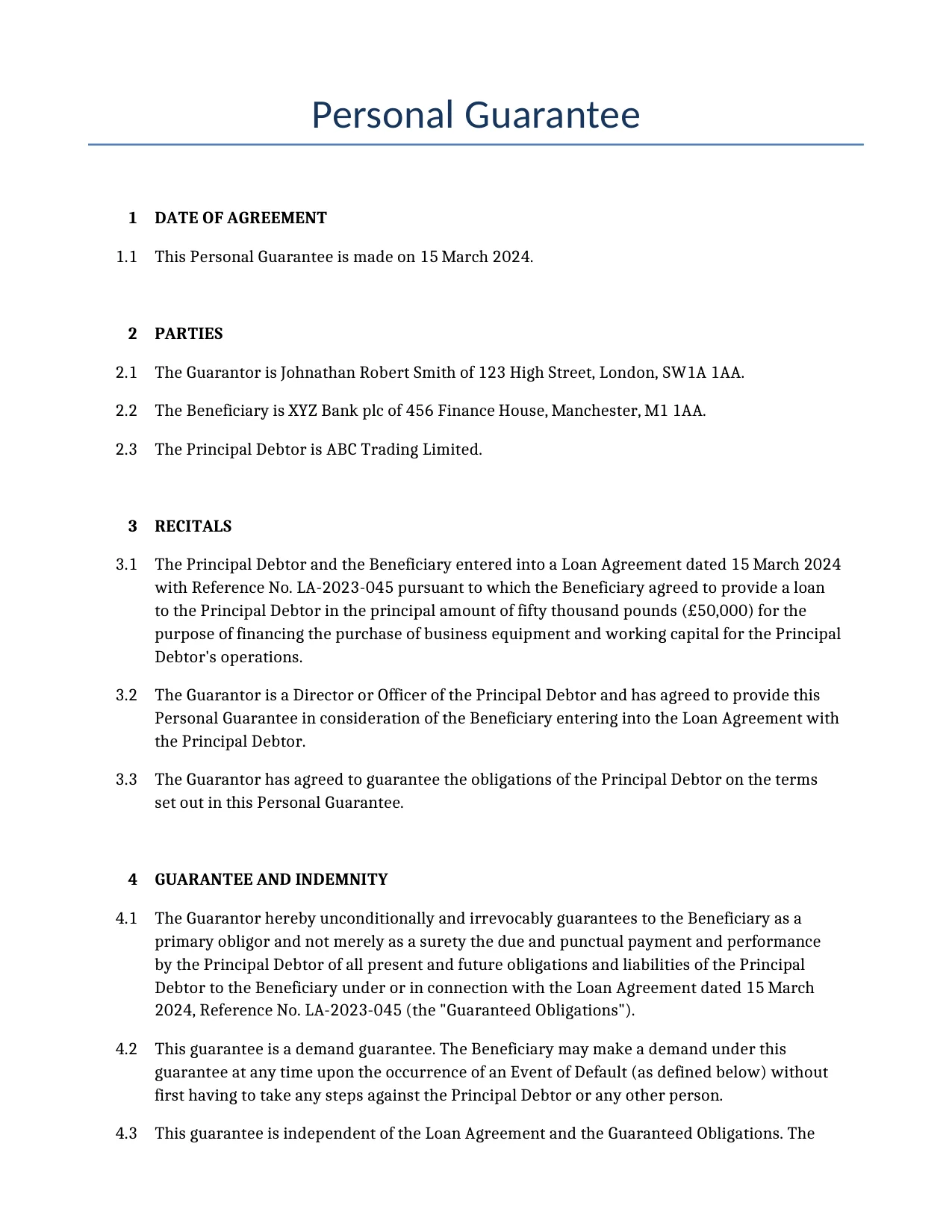

Personal Guarantee for Loan Agreement LA-2023-045

1DATE OF AGREEMENT

This Personal Guarantee is made on 15 March 2024.

2PARTIES

The Guarantor is Johnathan Robert Smith of 123 High Street, London, SW1A 1AA.

The Beneficiary is XYZ Bank plc of 456 Finance House, Manchester, M1 1AA.

The Principal Debtor is ABC Trading Limited.

3RECITALS

The Principal Debtor and the Beneficiary entered into a Loan Agreement dated 15 March 2024 with Reference No. LA-2023-045 pursuant to which the Beneficiary agreed to provide a loan to the Principal Debtor in the principal amount of fifty thousand pounds (£50,000) for the purpose of financing the purchase of business equipment and working capital for the Principal Debtor's operations.

The Guarantor is a Director or Officer of the Principal Debtor and has agreed to provide this Personal Guarantee in consideration of the Beneficiary entering into the Loan Agreement with the Principal Debtor.

The Guarantor has agreed to guarantee the obligations of the Principal Debtor on the terms set out in this Personal Guarantee.

4GUARANTEE AND INDEMNITY

The Guarantor hereby unconditionally and irrevocably guarantees to the Beneficiary as a primary obligor and not merely as a surety the due and punctual payment and performance by the Principal Debtor of all present and future obligations and liabilities of the Principal Debtor to the Beneficiary under or in connection with the Loan Agreement dated 15 March 2024, Reference No. LA-2023-045 (the "Guaranteed Obligations").

This guarantee is a demand guarantee. The Beneficiary may make a demand under this guarantee at any time upon the occurrence of an Event of Default (as defined below) without first having to take any steps against the Principal Debtor or any other person.

This guarantee is independent of the Loan Agreement and the Guaranteed Obligations. The Guarantor shall not be discharged by any invalidity, illegality or unenforceability of the Loan Agreement or any Guaranteed Obligation (whether or not known to the Beneficiary) and the Guarantor waives any right to assert any such invalidity, illegality or unenforceability as a defence to any claim under this guarantee.

If the Principal Debtor fails to pay any amount when due under the Loan Agreement or fails to perform any obligation thereunder the Guarantor shall on demand by the Beneficiary forthwith pay or perform that amount or obligation as if the Guarantor were the principal obligor.

The Guarantor shall indemnify the Beneficiary against any loss or liability suffered by the Beneficiary arising from any failure by the Principal Debtor to pay or perform any of the Guaranteed Obligations.

The Guarantor shall pay to the Beneficiary upon the Beneficiary's first written demand all amounts due under this guarantee without the Beneficiary being required to take any steps against the Principal Debtor or to give any prior notice to the Principal Debtor.

5CONTINUING GUARANTEE

This guarantee is a continuing guarantee and shall remain in full force and effect until all present and future obligations of the Principal Debtor to the Beneficiary under the Loan Agreement have been irrevocably discharged in full.

This guarantee shall apply to all present and future obligations of the Principal Debtor to the Beneficiary whether arising under the Loan Agreement or any variation or replacement thereof or any new facility provided by the Beneficiary to the Principal Debtor.

6GUARANTEED OBLIGATIONS

The obligations guaranteed under this Personal Guarantee are the principal amount of fifty thousand pounds (£50,000) advanced under the Loan Agreement together with any accrued interest, fees, costs and associated expenses.

7PAYMENT TERMS

All payments to be made by the Guarantor under this Personal Guarantee shall be made in GBP (British Pounds) in immediately available funds on the date of demand by the Beneficiary without any set-off, counterclaim or deduction.

If the Guarantor fails to pay any amount due under this Personal Guarantee on the due date interest shall accrue on the overdue amount at the rate of eight per cent (8%) per annum above the base rate of the Bank of England from time to time (both before and after judgment) until payment is made in full. This rate complies with the Late Payment of Commercial Debts (Interest) Act 1998 and is not a penalty under the principles established in Dunlop Pneumatic Tyre Co Ltd v New Garage and Motor Co Ltd [1915] AC 79 and Cavendish Square Holding BV v Talal El Makdessi [2015] UKSC 67.

8NO DISCHARGE OR VARIATION

The liability of the Guarantor under this Personal Guarantee shall not be discharged, impaired or affected by any variation to the terms of the obligations of the Principal Debtor (including without limitation changes to the loan amount, interest rate or extensions of repayment terms), any release or partial release granted to the Principal Debtor, any time or indulgence granted to the Principal Debtor, any insolvency or bankruptcy of the Principal Debtor, or any other act, omission, event or circumstance which but for this provision would discharge, impair or affect the liability of the Guarantor.

9WAIVER OF DEFENCES

The Guarantor hereby irrevocably waives all common law, equitable and statutory defences available to a guarantor or surety under English law (including without limitation any defences under the Statute of Frauds, any right to require the Beneficiary to first proceed against the Principal Debtor, any defence of election of remedies, any defence arising from any variation of the Loan Agreement, any defence of set-off or counterclaim, and any defence that would be available to the Principal Debtor). This waiver is without prejudice to the Guarantor's right to raise any defence that this guarantee is unenforceable due to fraud or misrepresentation by the Beneficiary.

The Guarantor hereby waives any right to set off any claims that the Guarantor may have against the Beneficiary against any amount due under this Personal Guarantee.

10SUBROGATION AND POSTPONEMENT

The Guarantor shall not exercise any rights of subrogation or any other rights that may arise as a result of the Guarantor making any payment under this Personal Guarantee until the Beneficiary has received full and irrevocable satisfaction of all claims against the Principal Debtor.

The rights postponed under this clause include all subrogation rights and rights including security interests.

11REPRESENTATIONS AND WARRANTIES

The Guarantor represents and warrants that the Guarantor has the full legal capacity and authority to enter into this Personal Guarantee, that this Personal Guarantee constitutes the Guarantor's valid, legally binding and enforceable obligations in accordance with its terms, and that the execution and delivery of this Personal Guarantee have been duly authorised by all necessary action.

The Guarantor represents and warrants that the Guarantor has received independent legal advice on the terms and effect of this Personal Guarantee from a solicitor independent of the Beneficiary before executing this document as a deed.

The Guarantor represents and warrants that there has been no undue influence, duress or misrepresentation in relation to the Guarantor's entry into this Personal Guarantee.

The Guarantor represents and warrants that there are no current or pending bankruptcy or insolvency proceedings against the Guarantor.

The Guarantor represents and warrants that the Guarantor's most recent financial statements are dated 31 December 2023 and that they fairly represent the Guarantor's financial position as at that date.

The Guarantor represents and warrants that there are no existing defaults, breaches or encumbrances related to the Guarantor's obligations under this Personal Guarantee and that there are no existing agreements that conflict with the Guarantor's obligations under this Personal Guarantee.

12COVENANTS OF THE GUARANTOR

The Guarantor covenants to notify the Beneficiary of any adverse financial changes within 14 days of becoming aware of the same where an adverse financial change shall mean any event or circumstance that results in a significant deterioration in the Guarantor's financial position including but not limited to a reduction in net worth by more than 20 per cent or insolvency proceedings.

The Guarantor covenants to provide to the Beneficiary copies of the Guarantor's financial statements annually with the first such financial report to be submitted on or before 31 December 2024.

The Guarantor covenants to comply with all applicable laws in all material respects.

The Guarantor covenants that it shall not create or permit to subsist any security over any of its assets without the prior written consent of the Beneficiary (negative pledge).

The Guarantor covenants to maintain adequate insurance over its assets and business with reputable insurers.

13EVENTS OF DEFAULT

Each of the following events shall constitute an event of default under this Personal Guarantee: (a) failure by the Principal Debtor or the Guarantor to pay any amount due under the Loan Agreement or this Personal Guarantee; (b) insolvency, bankruptcy or the making of any administration or winding-up order in respect of the Principal Debtor or the Guarantor; (c) material adverse change in the financial condition of the Principal Debtor or the Guarantor; (d) any breach by the Guarantor of any representation, warranty or covenant in this Personal Guarantee; and (e) any cross-default under the Loan Agreement.

Upon the occurrence of an event of default the Beneficiary shall give written notice to the Guarantor and the Guarantor shall have seven days from the date of such notice to remedy the default if capable of remedy.

Upon the occurrence of an event of default all amounts due under this Personal Guarantee shall become immediately due and payable on demand.

14ENFORCEMENT AND REMEDIES

The Beneficiary shall have the right to accelerate the full guaranteed amount upon the occurrence of an Event of Default.

The Beneficiary shall provide written notice to the Guarantor before enforcing this Personal Guarantee.

Interest shall accrue on the guaranteed amount during enforcement proceedings at the rate specified in clause 7.2.

15COSTS AND EXPENSES

The Guarantor shall pay to the Beneficiary on demand all costs, charges and expenses incurred by the Beneficiary in enforcing this Personal Guarantee including legal fees and solicitor costs, court filing fees and litigation expenses and reasonable administrative and incidental costs.

All costs and expenses claimed by the Beneficiary under this clause must be reasonable in amount and necessarily incurred.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Personal Guarantee in the United Kingdom

United Kingdom Reference Legislation

Personal Guarantee FAQs

Document Generation FAQs

Related Articles