AI Generated British Facility Agreement

PDF & Word - 2026 Updated

Docaro Pricing

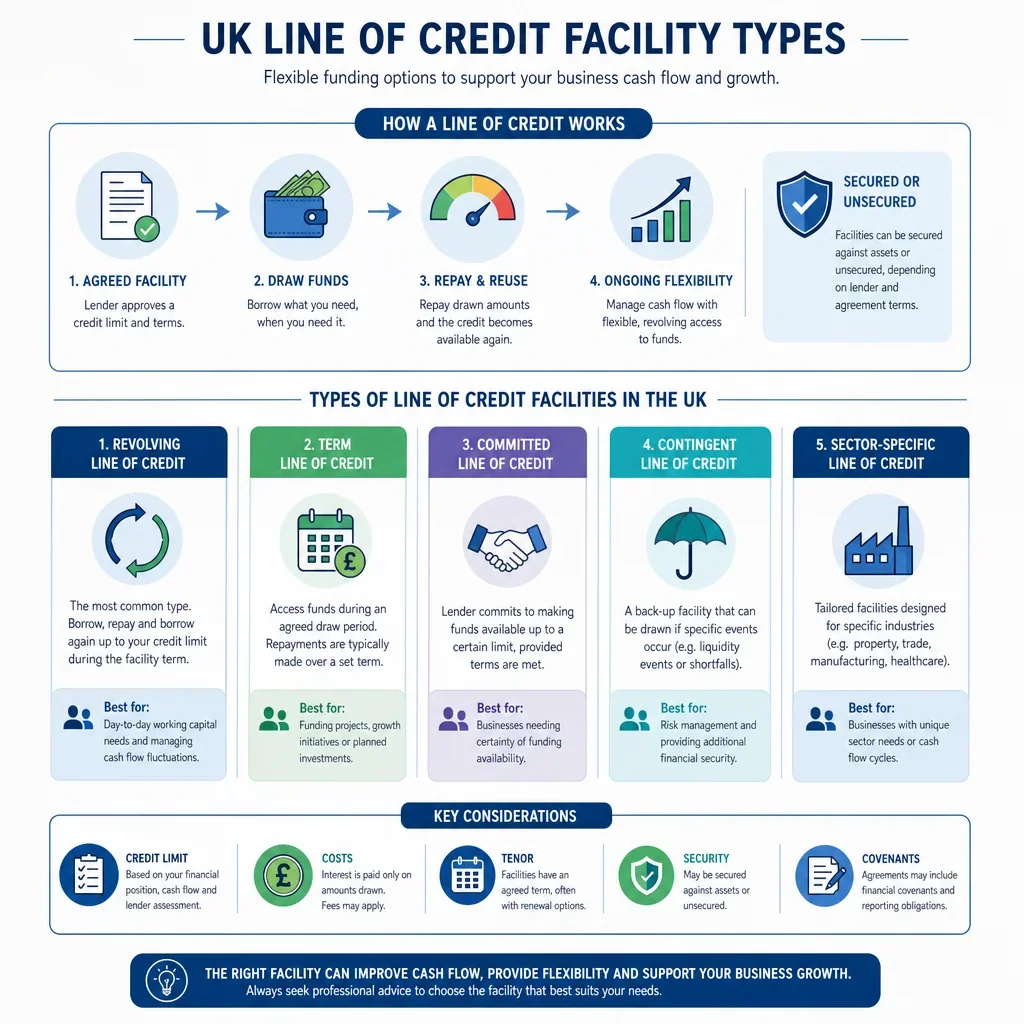

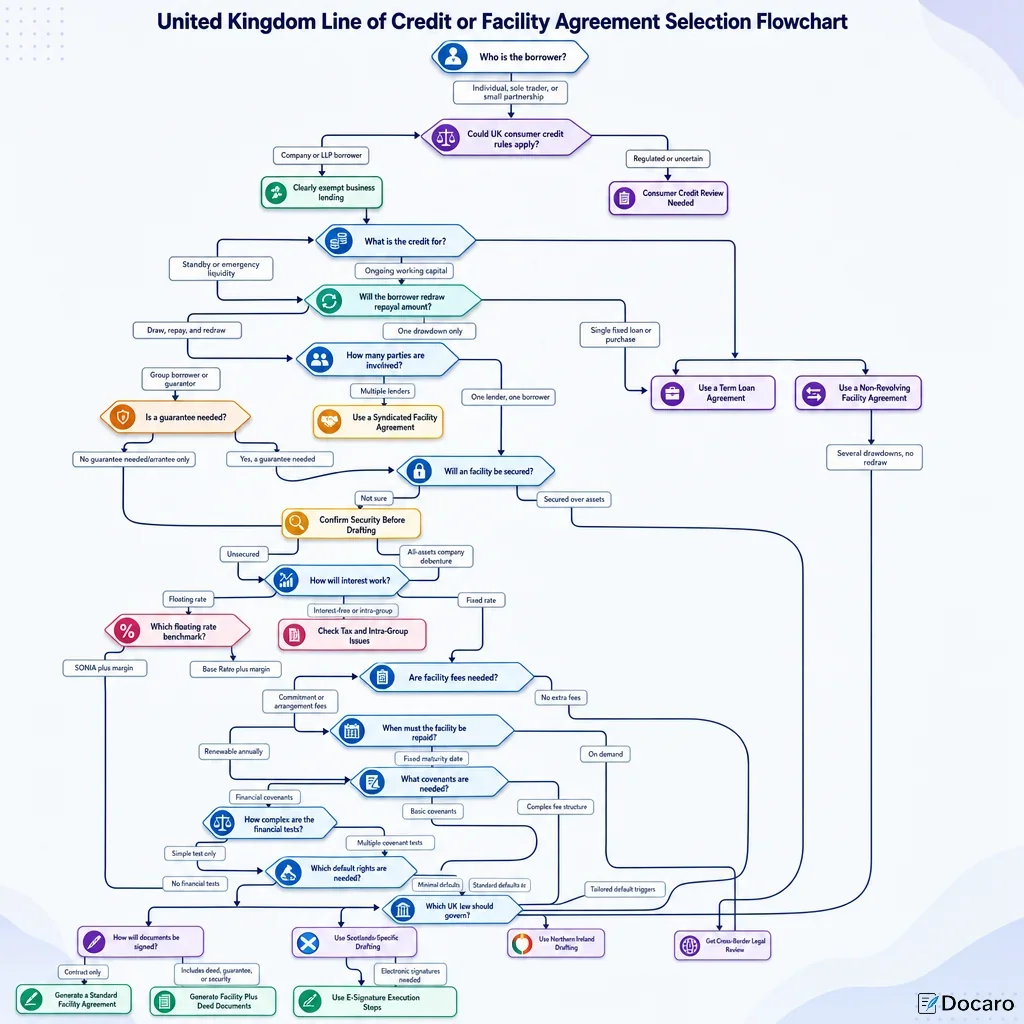

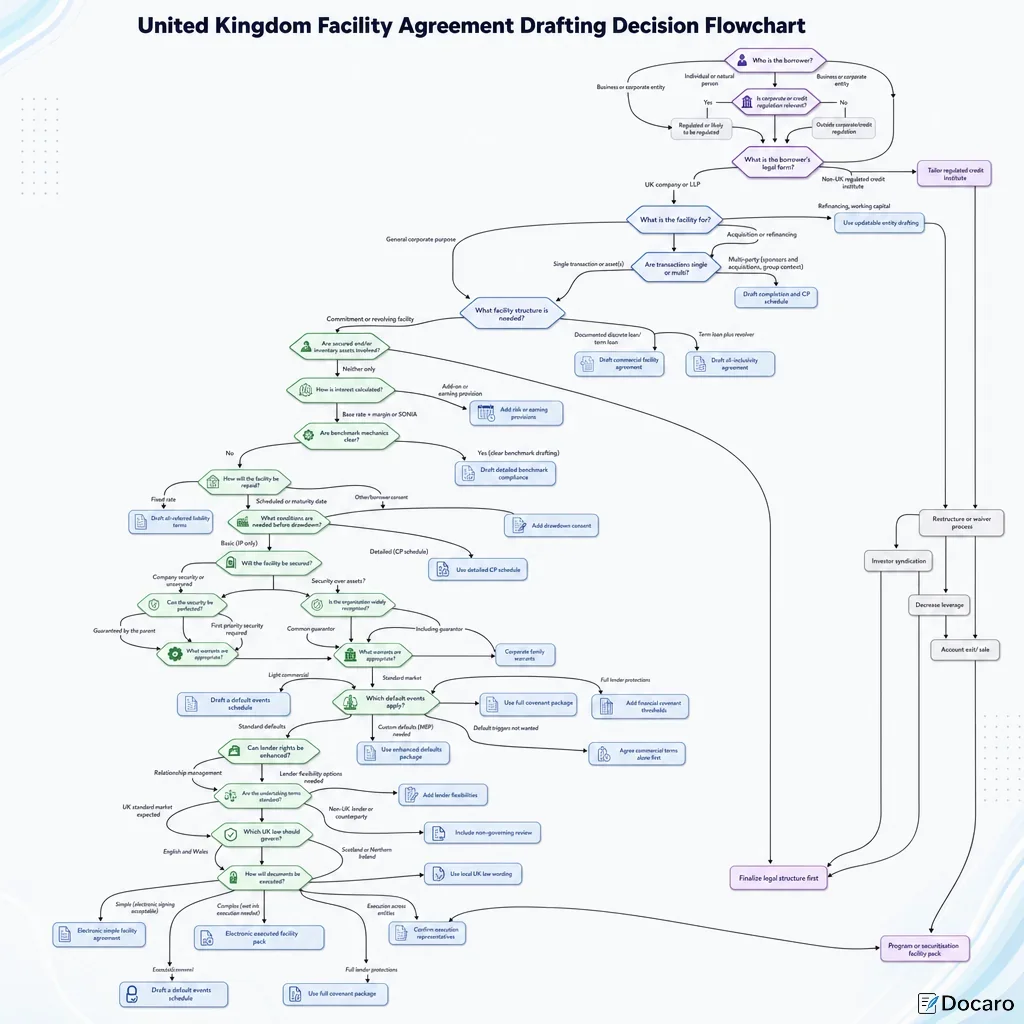

When do you need a Facility Agreement in the United Kingdom?

British Legal Rules for a Facility Agreement

Using the wrong structure for a line of credit agreement can lead to unenforceable terms or unintended regulatory non-compliance.

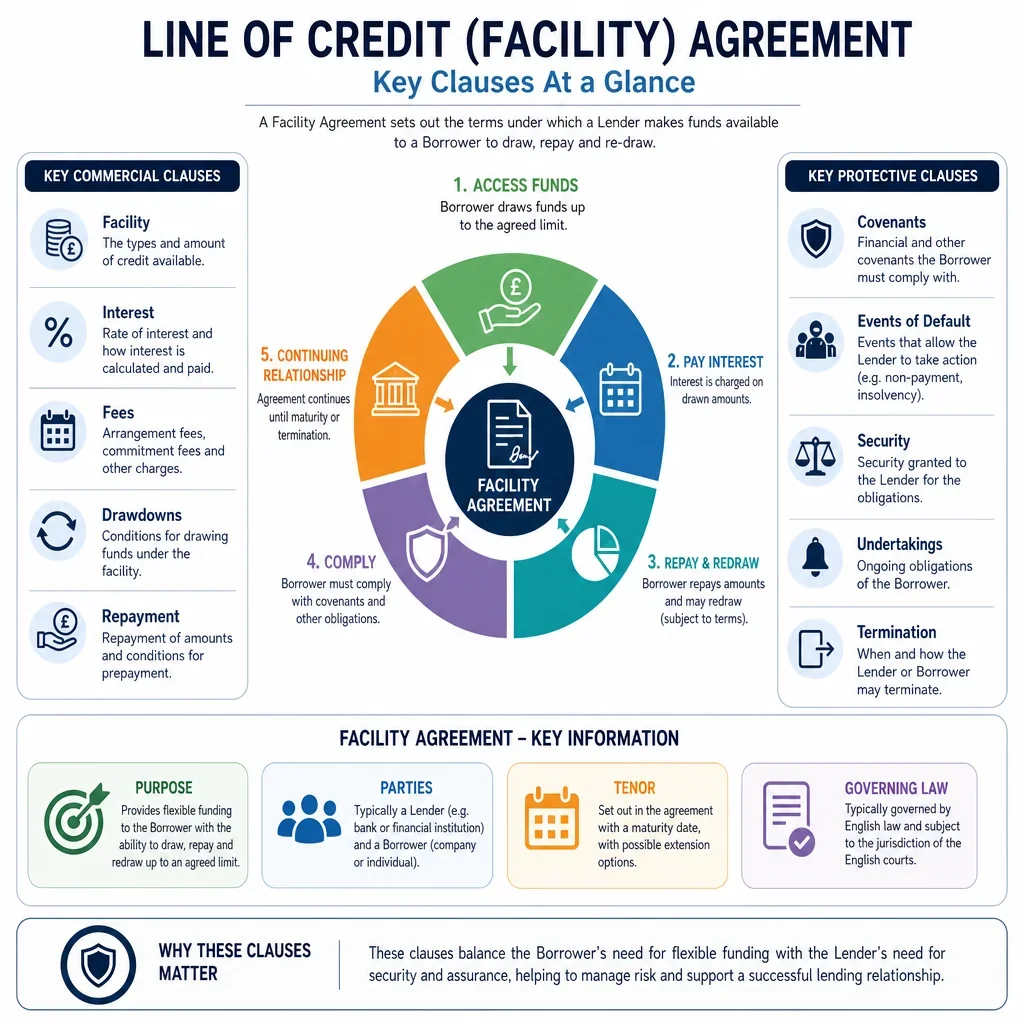

What a Proper Facility Agreement Should Include

- Parties InvolvedClearly identifies the lender and borrower with their full names and addresses.

- Loan Amount and PurposeSpecifies the maximum amount available and how the funds can be used.

- Interest and FeesDetails the interest rate, how it's calculated, and any additional charges.

- Repayment TermsOutlines when and how the borrowed amount must be repaid.

- Security and CollateralDescribes any assets pledged to secure the loan, if applicable.

- Default ConditionsLists events that trigger a default, like missed payments.

- Rights and RemediesExplains what the lender can do if the borrower defaults.

- Governing LawStates that English law applies and where disputes will be resolved.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Facility Agreement Template

Below is a free template example of a Facility Agreement for use in the United Kingdom generated by our AI model.

The clauses in your actual Facility Agreement will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

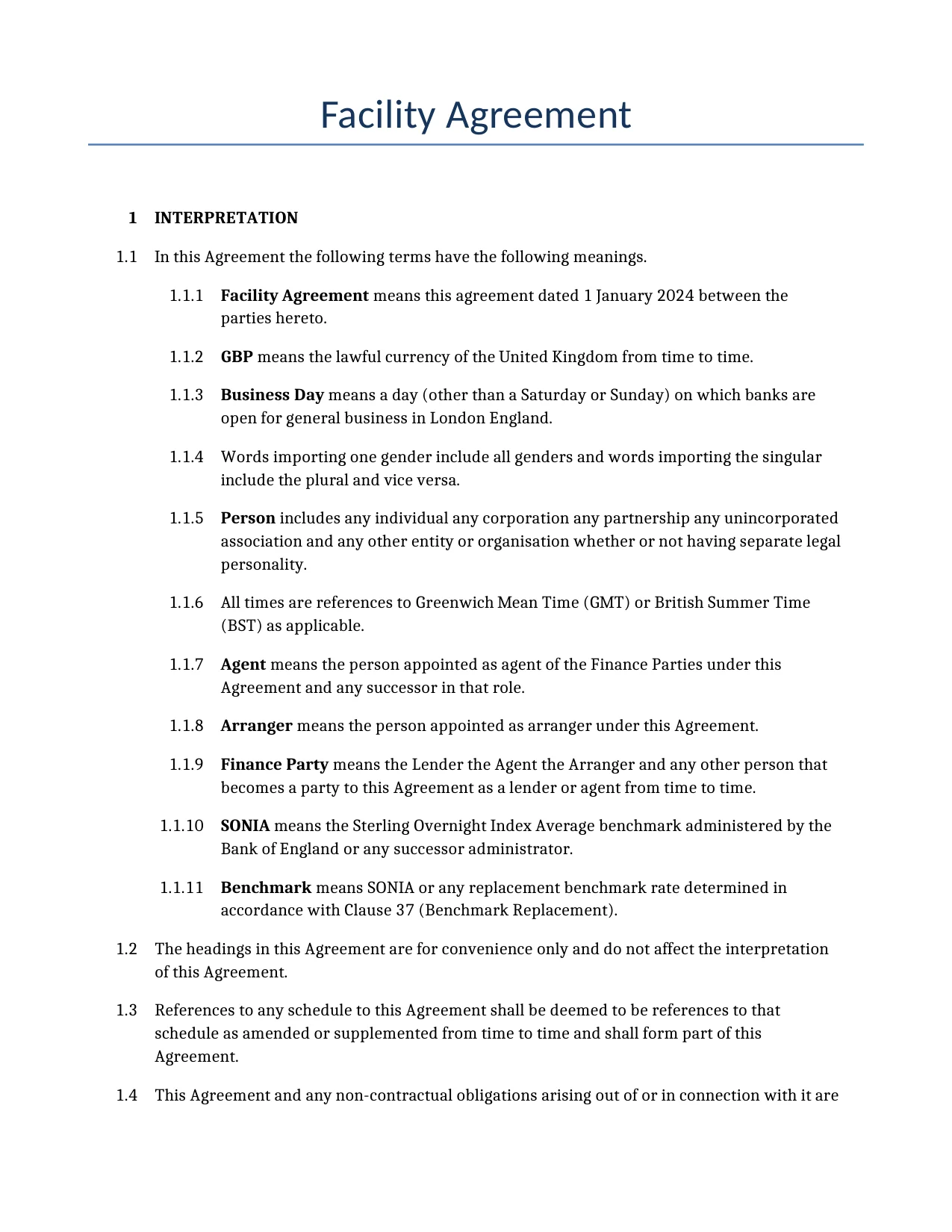

Facility Agreement

1INTERPRETATION

In this Agreement the following terms have the following meanings.

Facility Agreement means this agreement dated 1 January 2024 between the parties hereto.

GBP means the lawful currency of the United Kingdom from time to time.

Business Day means a day (other than a Saturday or Sunday) on which banks are open for general business in London England.

Words importing one gender include all genders and words importing the singular include the plural and vice versa.

Person includes any individual any corporation any partnership any unincorporated association and any other entity or organisation whether or not having separate legal personality.

All times are references to Greenwich Mean Time (GMT) or British Summer Time (BST) as applicable.

Agent means the person appointed as agent of the Finance Parties under this Agreement and any successor in that role.

Arranger means the person appointed as arranger under this Agreement.

Finance Party means the Lender the Agent the Arranger and any other person that becomes a party to this Agreement as a lender or agent from time to time.

SONIA means the Sterling Overnight Index Average benchmark administered by the Bank of England or any successor administrator.

Benchmark means SONIA or any replacement benchmark rate determined in accordance with Clause 37 (Benchmark Replacement).

The headings in this Agreement are for convenience only and do not affect the interpretation of this Agreement.

References to any schedule to this Agreement shall be deemed to be references to that schedule as amended or supplemented from time to time and shall form part of this Agreement.

This Agreement and any non-contractual obligations arising out of or in connection with it are governed by English law.

2THE FACILITY

Subject to the terms of this Agreement the Lender agrees to make available to the Borrower a revolving credit facility in an aggregate amount not exceeding five hundred thousand pounds sterling (GBP 500000) for the purpose of financing the day to day operational expenses and managing short term cash flow needs of the business of the Borrower.

The Facility shall be available for utilisation during the period from the date of this Agreement until 31 December 2025.

3CONDITIONS PRECEDENT

The obligations of the Lender to make the Facility available are subject to the conditions precedent that the Lender has received in form and substance satisfactory to it: (a) a copy of this Agreement duly executed by the parties; (b) evidence that any security required has been granted and perfected; (c) a legal opinion from counsel to the Borrower dated no later than the date of this Agreement; (d) copies of the constitutional documents of the Borrower; (e) evidence of all necessary authorisations required by the Borrower to enter into this Agreement and perform its obligations hereunder; (f) the audited financial statements of the Borrower for the period ending on 30 June 2023; (g) a certificate from the Borrower confirming that no material adverse change has occurred in the financial condition of the Borrower since the date of the latest financial statements; and (h) evidence that the Lender has completed its Know Your Customer procedures in respect of the Borrower to its satisfaction.

The Lender shall not be obliged to make any utilisation available to the Borrower unless on the date of the utilisation request and on the proposed utilisation date the Repeating Representations are true and no Default is continuing or would result from the proposed utilisation.

4UTILIZATION

The Borrower may utilise the Facility by delivering to the Lender a duly completed utilisation request by electronic mail or through the online portal maintained by the Lender not less than three Business Days before the proposed utilisation date.

Each utilisation request shall be addressed to John Smith Senior Loan Officer at the email address john.smith@bank.com and shall specify the amount of the proposed loan or letter of credit the currency thereof the proposed drawdown date the purpose of the utilisation and shall be accompanied by any supporting documentation required by the Lender.

No utilisation request may be delivered after 31 December 2025.

Utilisations may be made in British Pound Sterling or in United States Dollars.

The Lender may issue letters of credit under the Facility in accordance with the procedures set out in this Clause 4.

5REPAYMENT

The Borrower shall repay the Loans in full on the Termination Date which shall be 31 December 2025.

All repayments shall be made by bank transfer to the account specified by the Lender.

6PREPAYMENT AND CANCELLATION

The Borrower may make voluntary prepayments of any loan in whole or in part on any Business Day provided that the Borrower gives the Lender not less than five Business Days prior written notice of its intention to prepay.

Any voluntary prepayment shall be applied pro rata across all advances outstanding under the Facility.

The Borrower shall make mandatory prepayment of the Facility in full upon the occurrence of a change of control or upon the disposal of any material asset of the Borrower.

The Borrower may cancel any part of the undrawn commitment under the Facility by giving the Lender not less than thirty Business Days prior written notice.

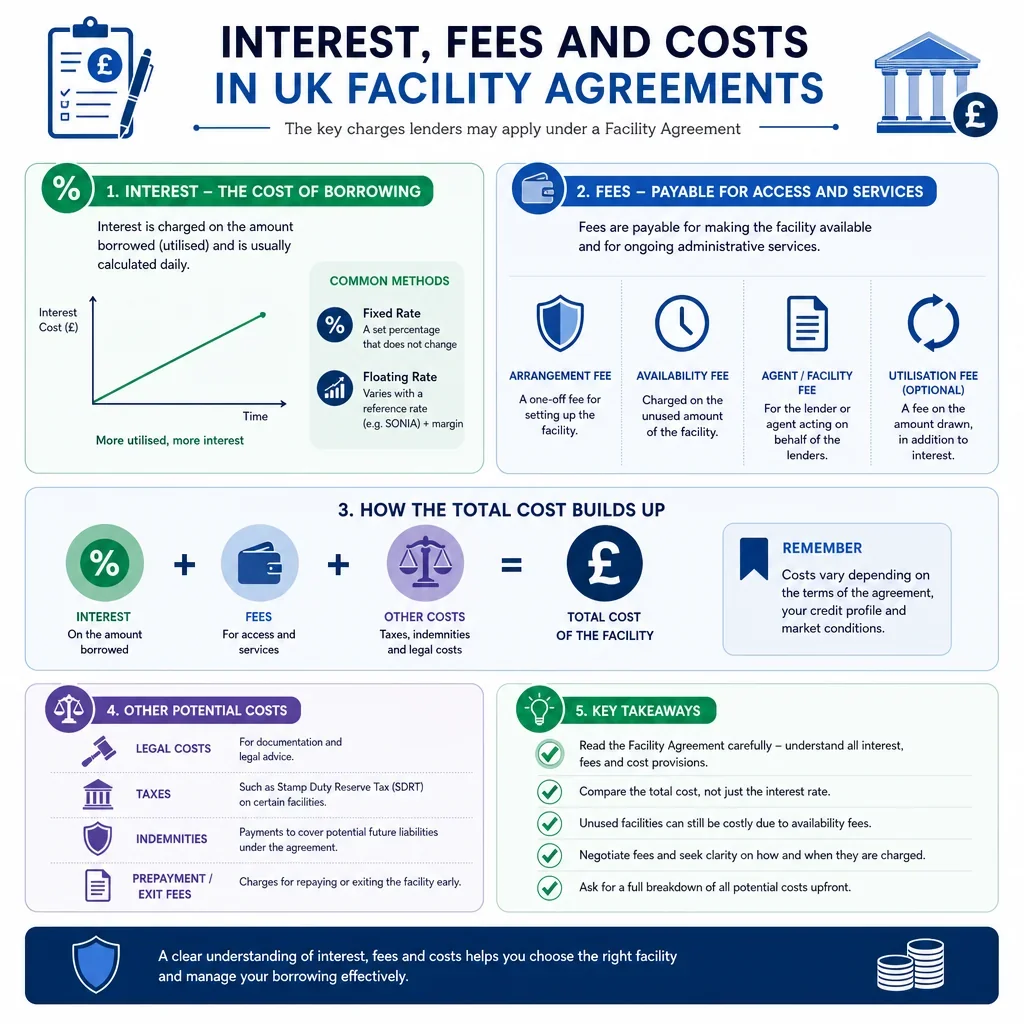

7INTEREST

Interest shall accrue on the outstanding principal amount of each loan at a fixed rate of 4.5 per cent per annum (subject to any Margin review pursuant to Clause 7.5).

Interest shall be calculated on the basis of actual days elapsed and a 365 day year.

The Borrower shall pay accrued interest quarterly in arrear on the fifteenth day of each calendar quarter with the first such payment being due on 31 March 2024.

If any amount due under this Agreement is not paid on its due date default interest shall accrue on such amount at a rate of two per cent per annum above the rate specified in Clause 7.1 from the due date until the date of actual payment. Such default interest shall be compounded monthly. For the avoidance of doubt the default interest rate is not a penalty and is a genuine pre-estimate of loss.

The Lender may review the Margin annually on each anniversary of the date of this Agreement and propose any adjustment in writing. Any such adjustment shall take effect 30 days after notice unless the Borrower notifies the Lender of its objection in which case the parties shall negotiate in good faith.

8INTEREST PERIODS

For the purposes of calculating interest by reference to the Benchmark the Borrower may select interest periods of one month three months or six months.

If no interest period is selected by the Borrower the default interest period shall be three months.

The Borrower shall give the Lender not less than three Business Days prior written notice of the selection or rollover of any interest period.

If an interest period would otherwise end on a day that is not a Business Day it shall be extended to the next Business Day unless that day falls in the next calendar month in which case it shall be shortened to the preceding Business Day in accordance with the modified following business day convention.

The first interest period shall commence on the first utilisation date.

9BENCHMARK REPLACEMENT

If the Lender determines (acting reasonably) that the Benchmark is no longer appropriate due to a Benchmark Event (including discontinuation of SONIA) the Lender shall notify the Borrower and the parties shall negotiate in good faith to agree a replacement benchmark rate and any necessary adjustments (including the Benchmark Replacement Adjustment).

If agreement is not reached within 30 days the Lender may (subject to compliance with the UK Benchmarks Regulation) designate a replacement benchmark rate (which may include a successor rate or an alternative rate) and any Benchmark Replacement Adjustment. Such replacement shall be notified to the Borrower and shall take effect from the date specified in the notice.

The Lender shall act in good faith and in a commercially reasonable manner when determining or designating any replacement benchmark. No amendment fee shall be payable by the Borrower in respect of any such change.

10FEES

The Borrower shall pay to the Lender an arrangement fee of 25000 GBP and a commitment fee at the rate of 0.5 per cent per annum on the undrawn portion of the Facility.

All fees payable under this Agreement shall be paid by electronic transfer and shall be exclusive of any value added tax which if properly chargeable shall be paid by the Borrower in addition.

11TAX GROSS UP AND INDEMNITIES

All payments to be made by the Borrower under this Agreement shall be made free and clear of and without deduction for or on account of any withholding tax or value added tax.

If the Borrower is required by law to make any deduction or withholding for or on account of tax the sum payable shall be increased so that after such deduction or withholding the Lender receives a net amount equal to the amount it would have received had no such deduction or withholding been required.

The Borrower shall indemnify the Lender against any loss or liability suffered by the Lender as a result of any tax liability arising in connection with this Agreement (including FATCA-related liabilities).

The Borrower shall promptly notify the Lender of any tax event that may give rise to an obligation under this Clause 11.

If the Lender is entitled to claim relief under a double taxation treaty it shall use reasonable endeavours to do so and the gross-up obligation shall be reduced accordingly.

The provisions of this Clause 11 shall survive the termination of this Agreement.

12ILLEGALITY

If it becomes unlawful for any Finance Party to perform any of its obligations under this Agreement or to fund or maintain its participation in any Loan then that Finance Party may by notice to the Borrower require the Borrower to prepay the Loans made to it or (if the Loans have not yet been drawn) cancel the undrawn commitment of that Finance Party on the last day of the current Interest Period or (if earlier) on the date specified by that Finance Party (being no earlier than the last day of any applicable grace period permitted by law).

13INCREASED COSTS

If as a result of any change in law or change in capital requirements occurring after the date of this Agreement the Lender incurs increased costs in connection with this Agreement the Borrower shall on demand pay to the Lender the amount of such increased costs.

The Lender shall notify the Borrower of any claim for increased costs not less than thirty days before such amount becomes due and payable.

The amount of any increased costs shall be calculated on a pro rata allocation basis.

The Borrower shall pay any increased costs claimed by the Lender in accordance with this Clause 13.

14OTHER INDEMNITIES

The Borrower shall indemnify the Lender against any breakage costs incurred by the Lender as a result of any prepayment or default calculated on the basis of market quotation.

The Borrower shall indemnify the Lender against any funding losses incurred by the Lender as a result of any prepayment or default.

The provisions of this Clause 14 shall survive the termination of this Agreement.

15MITIGATION BY THE LENDERS

The Lender shall take all reasonable steps to mitigate any increased costs or tax liabilities arising under this Agreement.

The Lender may take such mitigation steps without the prior consent of the Borrower provided that it acts reasonably in doing so.

16COSTS AND EXPENSES

The Borrower shall pay on demand all costs and expenses incurred by the Finance Parties in connection with the negotiation preparation execution and enforcement of this Agreement including but not limited to legal fees and expenses due diligence costs and enforcement expenses.

All amounts payable under this Clause 16 shall be payable upon execution of this Agreement in the case of any default by the Borrower or on demand by the Finance Parties and shall be inclusive of any value added tax properly chargeable.

The Borrower shall pay any stamp duty or similar taxes arising in respect of this Agreement or any document executed pursuant hereto.

The Borrower shall indemnify the Finance Parties against any increased costs arising as a result of regulatory changes affecting the Finance Parties.

17REPRESENTATIONS

The Borrower represents and warrants to each Finance Party that it is duly incorporated and validly existing under the laws of England and Wales and is in good standing with no unresolved compliance issues under applicable law.

The Borrower represents and warrants to each Finance Party that it has the full corporate power and authority to enter into this Agreement and to perform its obligations hereunder and that this Agreement does not and will not conflict with any law regulation or agreement binding upon it.

The Borrower represents and warrants to each Finance Party that it has obtained all necessary authorisations approvals and licences required to enter into and perform this Agreement.

The Borrower represents and warrants to each Finance Party that it is not involved in any litigation arbitration or administrative proceedings that could have a material adverse effect on its ability to perform its obligations under this Agreement.

The Borrower represents and warrants to each Finance Party that its existing borrowings do not exceed five hundred thousand pounds sterling (GBP 500000) and that its contingent liabilities do not exceed one hundred and fifty thousand pounds sterling and fifty pence (GBP 150000.50).

The Borrower represents and warrants to each Finance Party that its audited financial statements for the period ended 31 December 2023 are true complete and fairly represent its financial condition in accordance with generally accepted accounting principles.

The Borrower represents and warrants to each Finance Party that there has been no material adverse change in its financial condition since 31 December 2023.

The Borrower represents and warrants to each Finance Party that it is compliant with all tax obligations under United Kingdom law that it complies with all applicable environmental laws and that it maintains comprehensive policies and training in relation to anti bribery and corruption.

The Borrower represents and warrants to each Finance Party that after entering into this Agreement it will remain solvent and able to pay its debts as they fall due and that except as disclosed it has no security interests liens or encumbrances over its assets.

The Borrower was incorporated on 15 March 2015.

The Borrower represents and warrants to each Finance Party that it is in compliance with all applicable Sanctions (including those administered by OFSI) and that neither it nor any of its directors officers agents or employees is a Sanctioned Person.

The Borrower represents and warrants to each Finance Party that it is in compliance with the Bribery Act 2010 the Proceeds of Crime Act 2002 and all applicable anti-money laundering laws and regulations.

Each representation and warranty set out in this Clause 17 is repeated on each utilisation date with reference to the facts and circumstances then subsisting.

18INFORMATION UNDERTAKINGS

The Borrower shall deliver to the Agent its audited financial statements for each financial year ending in December within 180 days of the end of that financial year.

The Borrower shall deliver to the Agent quarterly financial information on or before the fifteenth day of the month following the end of each calendar quarter.

The Borrower shall deliver to the Agent monthly management accounts within 30 days of the end of each calendar month.

The Borrower shall deliver to the Agent its annual budget not later than 30 days before the start of each financial year.

The Borrower shall deliver to the Agent a compliance certificate signed by the Borrower Finance Director on a quarterly basis and in any event not later than 15 April 2024 in respect of the first test date and thereafter within 15 days after each subsequent test date.

All information shall be delivered to John Smith at the email address john.smith@company.com.

The Borrower shall promptly notify the Agent of any material adverse change in its financial condition or operations.

19FINANCIAL COVENANTS

The Borrower shall maintain a leverage ratio and an interest cover ratio in accordance with the levels and on the basis set out in Schedule 1 (Financial Covenants) to this Agreement.

The financial covenants shall be tested quarterly with the first test date being 31 March 2024 and shall be measured on a last twelve months basis.

The Borrower shall have the right to cure any breach of a financial covenant by injecting additional equity within 30 days of the date of the relevant compliance certificate.

20GENERAL UNDERTAKINGS

The Borrower undertakes to comply with all applicable laws and regulations of the United Kingdom (including the Financial Services and Markets Act 2000 to the extent applicable).

The Borrower undertakes to maintain its legal existence and good standing under the laws of England and Wales.

The Borrower undertakes to obtain and maintain all necessary authorisations approvals and licences required for the conduct of its business.

The Borrower undertakes to maintain adequate insurance over its assets and business in accordance with good industry practice.

The Borrower undertakes to keep its assets in good repair and condition.

The Borrower undertakes to pay all taxes when due and payable.

The Borrower undertakes to comply with all applicable environmental laws and to hold all necessary environmental permits.

The Borrower undertakes to notify the Lender within ten Business Days of any event that could reasonably be expected to have a material adverse effect on its ability to perform its obligations under this Agreement.

The Borrower undertakes not to merge demerge or consolidate with any other entity and not to make any material change to the nature of its business without the prior written consent of the Lender.

The Borrower undertakes to keep its properties and assets free from any security interests or encumbrances except as expressly permitted under this Agreement.

The Borrower shall (at its own expense) promptly take any action (including execution of any documents) that any Finance Party may reasonably require to perfect or protect any security or to enable any Finance Party to enforce its rights under this Agreement (Further Assurance).

The Borrower shall comply and shall procure that each of its subsidiaries complies with all applicable Sanctions laws and shall not engage in any activity that would breach such laws. The Borrower shall not use the proceeds of the Facility in any manner that would result in a breach of Sanctions.

The Borrower shall comply with the Bribery Act 2010 the Proceeds of Crime Act 2002 and all applicable anti-money laundering and counter-terrorist financing laws. The Borrower shall maintain policies and procedures designed to ensure compliance with such laws.

21EVENTS OF DEFAULT

It shall be an event of default if the Borrower fails to pay any amount due under this Agreement on its due date.

It shall be an event of default if any insolvency proceedings are commenced against the Borrower.

It shall be an event of default if any representation or warranty made by the Borrower proves to have been incorrect or misleading in any material respect.

It shall be an event of default if the Borrower breaches any covenant contained in this Agreement.

It shall be an event of default if any cross default occurs in respect of any other indebtedness of the Borrower.

It shall be an event of default if the Borrower or any of its directors officers agents or employees becomes a Sanctioned Person or if the Borrower breaches any Sanctions undertaking.

Upon the occurrence of an event of default the Lender may by notice to the Borrower declare all amounts outstanding under this Agreement to be immediately due and payable.

22CHANGES TO THE LENDERS

The Lender may assign or transfer all or any of its rights and obligations under this Agreement to any person (subject to any restrictions on assignment by the Borrower set out in Clause 22.8).

Any assignment shall require the prior written consent of the Borrower not to be unreasonably withheld or delayed.

Any transfer may be made without the consent of the Borrower if to another bank or financial institution.

Any transfer shall be effected by means of a novation certificate in the form set out in Schedule 3 (Form of Novation Certificate) to this Agreement.

The Lender shall give not less than thirty days prior notice to the Borrower and the Agent of any proposed assignment or transfer.

The Lender shall bear all costs associated with any assignment or transfer.

The Agent shall be notified of and shall record any change in the Lenders.

The Borrower may not assign transfer or novate any of its rights or obligations under this Agreement without the prior written consent of the Lender.

23THE ADMINISTRATIVE PARTIES

ABC Bank PLC is appointed as the Agent upon execution of this Agreement and shall act in such capacity in accordance with the terms of this Agreement.

The duties of the Agent shall include payment distribution notice coordination and record maintenance.

The Agent may resign upon giving not less than sixty days prior written notice to the parties hereto.

The Borrower shall indemnify the Agent against any liability incurred by the Agent in connection with the performance of its duties under this Agreement (except to the extent caused by the Agent's gross negligence or wilful misconduct).

24ROLE OF THE ARRANGER

ABC Investment Bank PLC is appointed as the Arranger with effect from the date of this Agreement.

The Arranger shall be responsible for structuring the facility syndicating the loan to potential lenders coordinating due diligence and providing ongoing advisory services to the Borrower regarding the terms of this Agreement and compliance therewith.

The Borrower shall pay to the Arranger the fees agreed in writing between them.

The Borrower shall indemnify the Arranger against syndication costs and against any losses arising from inaccuracies in information supplied by the Borrower (except to the extent caused by the Arranger's gross negligence or wilful misconduct).

The Arranger shall be bound by confidentiality obligations in respect of all information received in connection with this Agreement.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Facility Agreement in the United Kingdom

United Kingdom Reference Legislation

Facility Agreement FAQs

Document Generation FAQs

Related Articles