AI Generated British Mortgage Deed

PDF & Word - 2026 Updated

Docaro Pricing

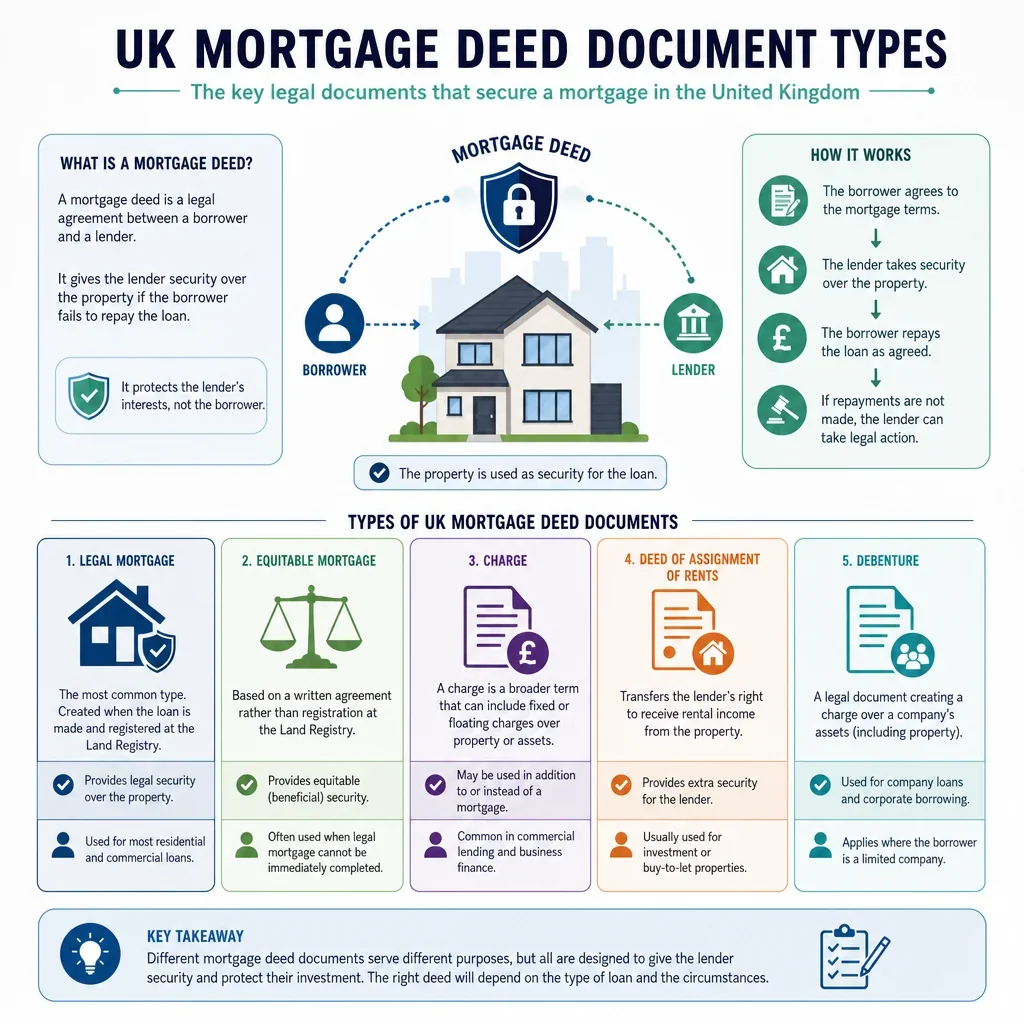

When do you need a Mortgage Deed in the United Kingdom?

British Legal Rules for a Mortgage Deed

Using the wrong type or structure of mortgage deed can invalidate the security interest or lead to unenforceable terms under UK property law.

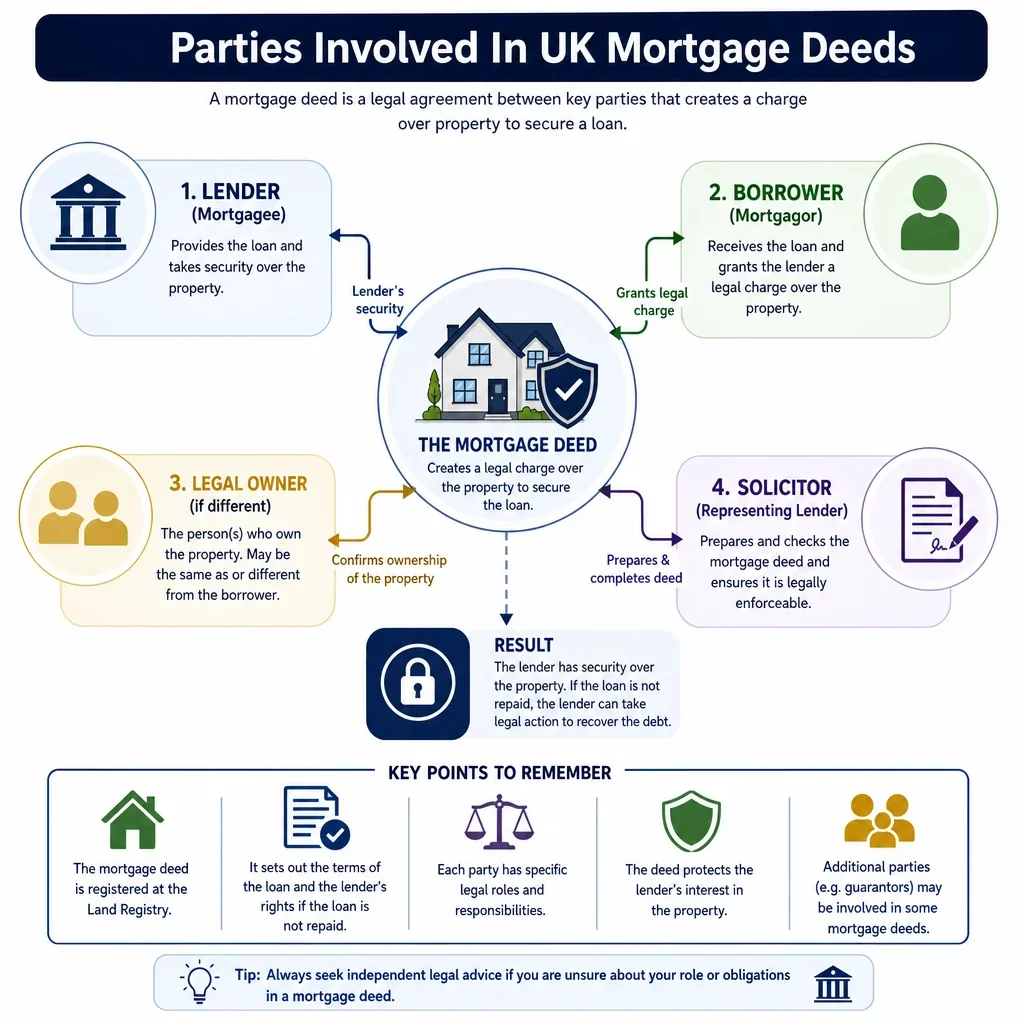

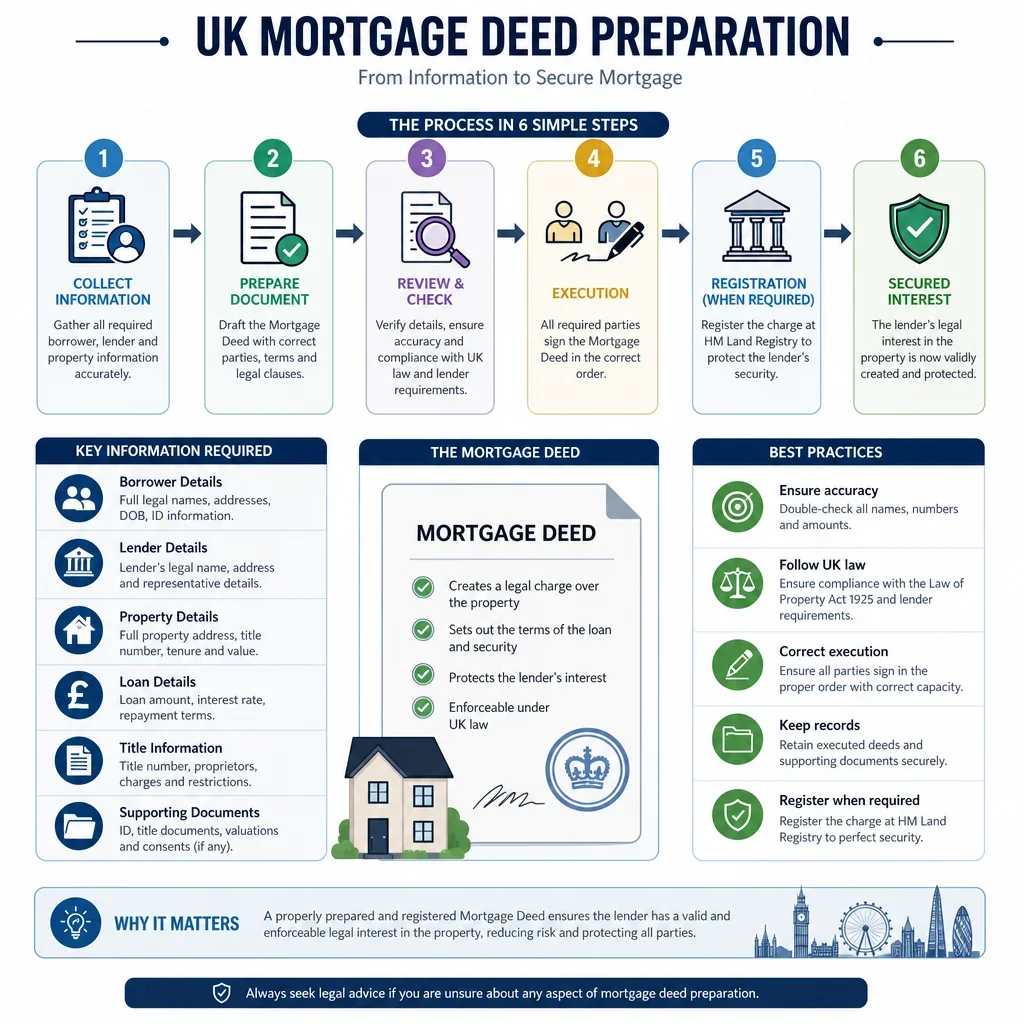

What a Proper Mortgage Deed Should Include

- Parties InvolvedIt identifies the borrower and lender clearly, including their full names and addresses.

- Property DetailsIt describes the property being mortgaged, such as its address and any unique identifiers.

- Loan AmountIt states the exact amount of money borrowed and any interest rates or repayment terms.

- Security ChargeIt explains how the property serves as security for the loan, allowing the lender to claim it if the borrower defaults.

- Borrower's PromisesIt lists the borrower's commitments, like making timely payments and maintaining the property.

- What Happens on DefaultIt outlines steps if payments are missed, including the lender's right to take back the property.

- Signatures and DatesIt includes spaces for the borrower and lender to sign and date the document to make it legally binding.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Mortgage Deed Template

Below is a free template example of a Mortgage Deed for use in the United Kingdom generated by our AI model.

The clauses in your actual Mortgage Deed will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

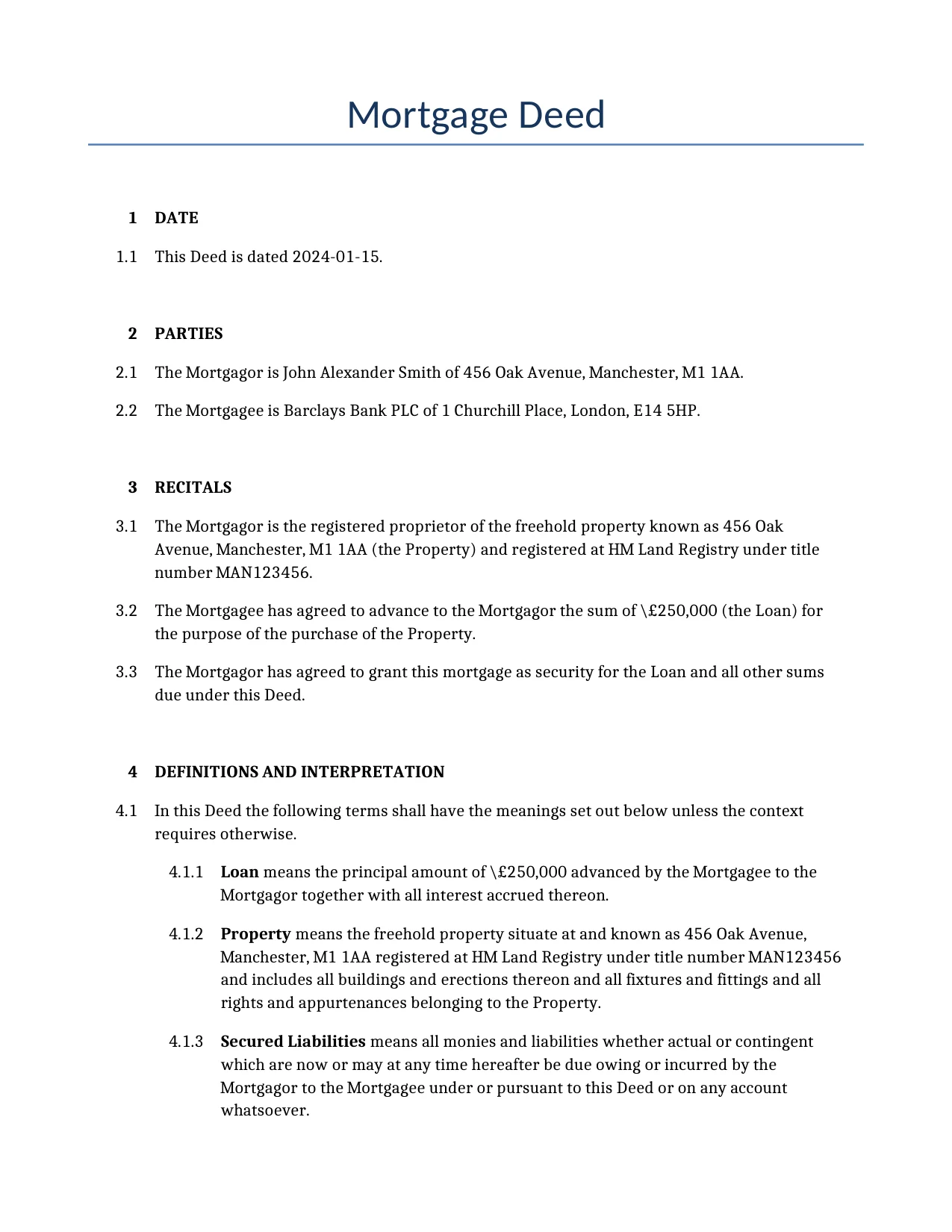

Mortgage Deed

1DATE

This Deed is dated 2024-01-15.

2PARTIES

The Mortgagor is John Alexander Smith of 456 Oak Avenue, Manchester, M1 1AA.

The Mortgagee is Barclays Bank PLC of 1 Churchill Place, London, E14 5HP.

3RECITALS

The Mortgagor is the registered proprietor of the freehold property known as 456 Oak Avenue, Manchester, M1 1AA (the Property) and registered at HM Land Registry under title number MAN123456.

The Mortgagee has agreed to advance to the Mortgagor the sum of \£250,000 (the Loan) for the purpose of the purchase of the Property.

The Mortgagor has agreed to grant this mortgage as security for the Loan and all other sums due under this Deed.

4DEFINITIONS AND INTERPRETATION

In this Deed the following terms shall have the meanings set out below unless the context requires otherwise.

Loan means the principal amount of \£250,000 advanced by the Mortgagee to the Mortgagor together with all interest accrued thereon.

Property means the freehold property situate at and known as 456 Oak Avenue, Manchester, M1 1AA registered at HM Land Registry under title number MAN123456 and includes all buildings and erections thereon and all fixtures and fittings and all rights and appurtenances belonging to the Property.

Secured Liabilities means all monies and liabilities whether actual or contingent which are now or may at any time hereafter be due owing or incurred by the Mortgagor to the Mortgagee under or pursuant to this Deed or on any account whatsoever.

Events of Default means any of the events set out in clause 10 of this Deed.

Interest Rate means 4.5 percent per annum or such other rate as may be notified by the Mortgagee from time to time in accordance with the terms of the Loan.

Business Day means a day (other than a Saturday or Sunday) on which banks are open for business in London.

References to clauses and schedules are to clauses and schedules of this Deed.

Headings are for convenience only and shall not affect the interpretation of this Deed.

This Deed is executed and delivered as a deed and shall take effect accordingly.

5CHARGING CLAUSE

The Mortgagor as beneficial owner hereby charges the Property by way of legal mortgage to the Mortgagee as security for the payment and discharge of the Secured Liabilities.

This Deed is made by way of a legal mortgage and the Mortgagor charges the Property with the payment of the Secured Liabilities.

6THE LOAN

The Mortgagee agrees to advance the Loan to the Mortgagor subject to the terms of the Mortgage Offer Letter (which terms are incorporated herein by reference).

Interest shall accrue on the outstanding principal balance of the Loan at the Interest Rate.

The Mortgagor shall repay the Loan together with interest thereon in accordance with the repayment schedule set out in the Mortgage Offer Letter.

The term of the Loan shall be as set out in the Mortgage Offer Letter.

The Mortgagor shall pay all fees and other charges in respect of the Loan as notified by the Mortgagee from time to time.

7COVENANTS BY THE MORTGAGOR

The Mortgagor covenants with the Mortgagee that the Mortgagor will repay the Loan and all other Secured Liabilities on demand or in accordance with the repayment schedule set out in the Mortgage Offer Letter.

The Mortgagor covenants with the Mortgagee to pay interest on the Loan at the Interest Rate or such other rate as may apply from time to time in accordance with the terms of the Loan.

The Mortgagor covenants with the Mortgagee that the Mortgagor will at all times comply with all applicable laws and regulations in relation to the Property and the Loan.

The Mortgagor covenants with the Mortgagee that the Mortgagor will not make any alterations to the Property without the prior written consent of the Mortgagee.

The Mortgagor covenants with the Mortgagee to insure the Property in accordance with clause 11 of this Deed.

The Mortgagor covenants with the Mortgagee to pay and discharge all Outgoings in accordance with clause 12 of this Deed.

The Mortgagor covenants with the Mortgagee to repair and maintain the Property in accordance with clause 13 of this Deed.

The Mortgagor covenants with the Mortgagee to comply with all tenancy and lease obligations in accordance with clause 14 of this Deed.

8THE PROPERTY

The Property is more particularly described in the Mortgage Offer Letter and/or the Land Registry title.

The Property is held on a freehold tenure and includes all fixtures and fittings and all appurtenances such as rights of way or easements belonging to or benefiting the Property.

The Property is subject to this mortgage and the charge created by this Deed.

9RIGHTS OF THE MORTGAGEE

The Mortgagee shall have all the powers of a mortgagee under the Law of Property Act 1925 (including the power of sale under section 101 thereof) and all other powers conferred by this Deed or by statute.

Upon the occurrence of an Event of Default the Mortgagee shall have the right to enter the Property.

Upon the occurrence of an Event of Default the Mortgagee shall have the right to appoint a receiver over the Property.

Upon the occurrence of an Event of Default the Mortgagee shall have the right to take possession of the Property.

The Mortgagee may exercise its power of sale without the restrictions contained in section 103 of the Law of Property Act 1925.

10DEFAULT AND ENFORCEMENT

Each of the following shall constitute an Event of Default: (a) failure to pay any principal or interest when due; (b) breach of any other covenant or obligation under this Deed; (c) the insolvency of the Mortgagor; (d) the sale or transfer of the Property without the prior written consent of the Mortgagee; and (e) any other event specified in the Mortgage Offer Letter.

The provisions of this clause shall apply from the date of this Deed.

The Mortgagee shall give the Mortgagor such notice as may be required by law before exercising any rights upon the occurrence of an Event of Default.

Upon the occurrence of an Event of Default the Mortgagee may accelerate the entire Loan so that all Secured Liabilities become immediately due and payable.

Upon the occurrence of an Event of Default the Mortgagee may exercise the following enforcement remedies: the appointment of a receiver; the taking of possession of the Property; and the power of sale of the Property.

Interest shall accrue at the default rate notified by the Mortgagee upon any amount in default.

The Mortgagor shall have such cure period as may be required by law to remedy any non-monetary default before the Mortgagee may exercise its enforcement rights.

11INSURANCE

The Mortgagor covenants with the Mortgagee that the Mortgagor will maintain comprehensive buildings insurance on the Property with an insurer and on terms approved by the Mortgagee against all usual risks (including fire, flood, storm, subsidence, explosion, earthquake, riot, malicious damage, bursting and overflowing of water tanks, apparatus or pipes, impact, aircraft and other aerial devices, and such other risks as the Mortgagee may from time to time require) from the date of this Deed in an amount not less than the full reinstatement value of the Property (including VAT, demolition costs, site clearance and professional fees).

The Mortgagor shall ensure that the interest of the Mortgagee is noted on the insurance policy as loss payee.

The Mortgagor shall notify the Mortgagee immediately of any cancellation of the policy or the filing of any claim and shall hold all monies received from any insurance claim on trust for the Mortgagee until applied in making good the damage or in such other manner as the Mortgagee may direct.

The Mortgagor shall also maintain such other insurances (including public liability insurance and, if the Property is let, landlord's insurance and rent loss insurance) as the Mortgagee may from time to time require.

12OUTGOINGS AND TAXES

The Mortgagor covenants with the Mortgagee that the Mortgagor will pay all council tax, water and sewerage charges, ground rents (if any), service charges (if any) and all other outgoings and taxes relating to the Property as and when they fall due and will produce to the Mortgagee on demand all receipts relating to such payments.

The Mortgagor shall be responsible for any capital gains tax, stamp duty land tax or similar charges relating to the Property or its purchase, sale or disposal.

13REPAIRS AND MAINTENANCE

The Mortgagor covenants with the Mortgagee that the Mortgagor will at all times keep the Property in good and substantial repair and condition and will replace and renew all fixtures and fittings and appurtenances as necessary.

The Mortgagee shall be permitted to inspect the Property at reasonable intervals upon giving reasonable notice to the Mortgagor to verify compliance with the obligations under this clause.

If the Mortgagor fails to comply with this clause the Mortgagee may (but shall not be obliged to) carry out repairs and the cost thereof shall be added to the Secured Liabilities.

14LEASE AND TENANCY PROVISIONS

The Mortgagor shall not let or licence the Property without the prior written consent of the Mortgagee and then only in accordance with the terms of the Mortgage Offer Letter and all applicable law (including without limitation the Housing Act 1988, the Housing Act 2004 and all requirements relating to assured shorthold tenancies, licensing of houses in multiple occupation and selective licensing).

The Mortgagor shall at all times comply with all obligations of a landlord under any tenancy agreement and under all applicable legislation (including without limitation the Landlord and Tenant Act 1985, the Housing Act 1988 as amended and all regulations relating to deposit protection, gas and electrical safety, energy performance certificates and smoke and carbon monoxide alarms).

The Mortgagor shall ensure that any tenancy agreement contains provisions approved by the Mortgagee and shall not permit any tenant to sublet the Property.

The Mortgagor shall maintain landlord's insurance and loss of rent insurance if the Property is let.

All rent and other income from the Property shall be applied first in payment of the Secured Liabilities.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Mortgage Deed in the United Kingdom

United Kingdom Reference Legislation

Mortgage Deed FAQs

Document Generation FAQs

Related Articles