Cohabitation Agreement Review Triggers In Britain

Review Trigger | Reason for Review | Terms Potentially Affected | Suggested Review Timing | Update Priority |

|---|---|---|---|---|

Property change | ||||

Buying a home together | Ownership shares, mortgage liability and sale rights should be clearly recorded. | Ownership shares, deposit contributions, mortgage payments, sale process, buy-out rights. | Immediate review | High |

Partner moves into owned home | Payments and improvements may create disputes over beneficial interest. | Occupation rights, contributions, improvement costs, no-interest wording, exit arrangements. | Immediate review | High |

Adding partner to title | Legal ownership and beneficial ownership may need new written confirmation. | Declaration of trust, ownership percentages, mortgage liability, sale consent. | Immediate review | High |

Removing partner from title | Buy-out, release from mortgage and future occupation rights may change. | Transfer terms, buy-out calculation, release provisions, indemnities, moving-out date. | Immediate review | High |

Changing ownership form | Survivorship and shares differ between joint tenants and tenants in common. | Beneficial shares, death provisions, declaration of trust, will coordination. | Immediate review | High |

Severing joint tenancy | Automatic survivorship may end, changing death and estate outcomes. | Death clause, ownership shares, life insurance, wills, sale-on-death procedure. | Immediate review | High |

New declaration of trust | The agreement should align with express property trust terms. | Priority clause, ownership schedule, deposit record, sale proceeds formula. | Immediate review | High |

Remortgaging the home | Liability, repayments and equity release may alter each partner's position. | Mortgage payment shares, equity release use, indemnities, default consequences. | Review within 1 month | High |

Financial change | ||||

Further advance or secured loan | New secured debt may affect equity, repayments and default risk. | Debt responsibility, repayment shares, use of funds, equity adjustments. | Immediate review | High |

Property change | ||||

Mortgage paid off | Contribution assumptions and equity calculations may now be outdated. | Equity shares, household expense split, title records, sale proceeds schedule. | Review within 3 months | Medium |

Major home improvements | Unequal funding or labour may affect expected equity or reimbursement. | Improvement contributions, reimbursement rights, valuation method, maintenance duties. | Review within 1 month | High |

One partner pays major repairs | Large unequal costs may need reimbursement or contribution records. | Repair cost schedule, reimbursement, household budget, evidence requirements. | Review within 1 month | Medium |

Significant property value change | Fixed sums, percentages and buy-out formulas may no longer be fair. | Valuation method, buy-out price, sale proceeds formula, review thresholds. | Review at next annual review | Medium |

Home is rented out | Rental income, landlord duties and tax responsibilities may change finances. | Rental income split, landlord costs, tax responsibility, management decisions. | Immediate review | High |

Financial change | ||||

Taking in a lodger | Income, privacy and household responsibilities may change. | Income allocation, consent rights, bills, house rules, termination of lodging. | Review within 1 month | Medium |

Property change | ||||

Buying investment property | New asset, debt, income and tax assumptions may need documenting. | Separate property schedule, rental income, mortgage liability, tax costs. | Review within 1 month | Medium |

Selling the shared home | Sale proceeds, moving costs and future living arrangements must be addressed. | Sale proceeds, estate agent choice, costs, repayment of loans, temporary housing. | Immediate review | High |

Buying replacement home | New deposits, mortgage terms and ownership shares may differ. | New property schedule, deposits, mortgage shares, sale proceeds reinvestment. | Immediate review | High |

Relocation | ||||

Moving to rented home | Rent, deposit, notice and joint tenancy liabilities may differ from ownership terms. | Rent split, tenancy deposit, bills, notice procedure, end-of-tenancy costs. | Review within 1 month | High |

Property change | ||||

One partner becomes sole tenant | Non-tenant partner may have limited housing rights and different payment obligations. | Occupation permission, rent contributions, notice rights, deposit ownership. | Immediate review | High |

Tenancy terms change | Rent, break clauses and obligations may affect household cost sharing. | Rent share, deposit, notice, break clause, utilities, damage costs. | Review within 1 month | Medium |

Financial change | ||||

Rent increase | The agreed household contribution split may become unaffordable or outdated. | Rent contributions, bills split, affordability review, arrears responsibility. | Review within 1 month | Medium |

Council tax liability changes | Household occupancy and discounts may affect shared outgoings. | Bill split, discounts, arrears responsibility, moving-out adjustments. | Review within 1 month | Medium |

Substantial salary increase | Income-based contribution ratios may no longer match current affordability. | Household contributions, savings targets, debt payments, lifestyle expenses. | Review at next annual review | Medium |

Substantial salary reduction | Existing payment obligations may become unrealistic or unfair. | Bills split, mortgage support, shortfall rules, review thresholds. | Review within 1 month | High |

Employment change | ||||

Redundancy | Loss of income and redundancy pay may affect contribution obligations. | Household contributions, emergency fund use, arrears, temporary support. | Immediate review | High |

Long-term unemployment | Ongoing income loss may require a sustainable contribution arrangement. | Bills split, temporary support, debt prevention, review dates, job-search costs. | Review within 1 month | High |

Starting a new job | Income, hours, commuting costs and location may change household arrangements. | Expense split, commuting costs, childcare, relocation, household duties. | Review within 3 months | Medium |

Becoming self-employed | Income volatility, tax reserves and business debts may affect household finances. | Contribution formula, tax reserves, business assets, personal guarantees, debts. | Review within 1 month | High |

Starting a limited company | Shares, dividends, director loans and guarantees may affect assets and liabilities. | Business ownership schedule, dividends, guarantees, director loans, tax reserves. | Review within 1 month | High |

Financial change | ||||

Personal guarantee given | A contingent liability may put shared assets or household finances at risk. | Debt disclosure, indemnity, asset protection, household contribution fallback. | Immediate review | High |

Bankruptcy or insolvency risk | Creditors may affect assets, home equity and payment responsibilities. | Debt schedules, indemnities, beneficial interest, default clauses, evidence records. | Immediate review | High |

IVA or debt arrangement | Formal debt plans may affect disposable income and shared assets. | Debt responsibility, bill payments, asset disclosures, arrears prevention. | Immediate review | High |

Significant personal debt | Debt repayments may reduce contributions and create disputes over liability. | Debt schedule, separate liabilities, bill priority, indemnities, credit use. | Review within 1 month | High |

Opening joint bank account | Joint accounts can create shared access and practical exposure to overdrafts. | Account use, overdraft limits, contributions, closing procedure, records. | Review within 1 month | Medium |

Closing joint bank account | Payment routes and shared savings arrangements may no longer work. | Bill payment method, account balance split, standing orders, savings records. | Review within 1 month | Medium |

Creating joint investments | Ownership, withdrawals and tax treatment should be recorded. | Investment ownership, contributions, withdrawals, gains, losses, tax liability. | Review within 1 month | Medium |

Receiving inheritance | Inherited money used for the home may need protection or repayment terms. | Separate property, ring-fencing, deposit contribution, repayment on sale, wills. | Review within 1 month | High |

Large family gift received | Gift or loan status should be clear if funds support shared property. | Gift evidence, family loan, deposit source, repayment, ownership shares. | Immediate review | High |

Large bonus or windfall | Use of windfall for shared assets may affect ownership expectations. | Separate property, shared purchases, debt repayment, savings allocation. | Review within 3 months | Medium |

Lottery or prize win | Major new wealth may change property, gifts and support arrangements. | Separate assets, shared purchases, gifts, tax planning, estate planning. | Review within 1 month | High |

Buying a car together | Ownership, finance and use costs may need clear allocation. | Vehicle ownership, finance payments, insurance, maintenance, sale or buy-out. | Review within 1 month | Medium |

High-value shared purchase | Expensive items may be disputed if the relationship ends. | Asset inventory, ownership, reimbursement, possession, valuation method. | Review within 3 months | Medium |

Insurance cover changes | Protection for mortgage, contents, illness or death may no longer match risks. | Life insurance, income protection, contents cover, beneficiary nominations, premiums. | Review within 3 months | Medium |

Pension nomination changes | Death benefits may not align with property or support intentions. | Death benefits, beneficiary nominations, wills, mortgage protection, dependants. | Review within 3 months | Medium |

Family change | ||||

Making or updating a will | Will provisions should align with home ownership and death clauses. | Death clause, survivorship, occupation after death, beneficiary records, insurance. | Review within 1 month | High |

No will despite inheritance expectations | Unmarried partners do not inherit under intestacy rules in England and Wales. | Will coordination, death clause, life insurance, occupation rights, emergency contacts. | Immediate review | High |

Making an LPA | Attorney choices may affect property decisions if a partner loses capacity. | Emergency decision-making, mortgage payments, sale authority, care costs. | Review within 3 months | Medium |

Serious illness or incapacity | Care needs, income loss and decision-making arrangements may change. | Household contributions, care costs, occupation, LPA, insurance, emergency funds. | Immediate review | High |

Long-term care needs arise | Care costs, adaptations and living arrangements may materially change finances. | Care costs, home adaptations, contribution split, occupation rights, emergency support. | Review within 1 month | High |

Pregnancy | Leave, income, childcare and housing needs may change before birth. | Household contributions, parental leave, childcare costs, room use, savings. | Review within 3 months | High |

Birth of a child | Childcare costs, leave, housing and support obligations may change significantly. | Child-related costs, leave income, housing use, savings, insurance, wills. | Review within 1 month | High |

Adoption of a child | Parental responsibilities, leave and family costs may change. | Childcare costs, parental leave, room allocation, insurance, wills, savings. | Review within 1 month | High |

Partner supports existing child | Voluntary support and household cost-sharing should be distinguished from legal duties. | Child costs, school expenses, bedroom use, caregiving, separation arrangements. | Review within 3 months | Medium |

Childcare arrangements change | Childcare costs can materially affect disposable income and contributions. | Childcare payments, work hours, school costs, household budget, tax-free childcare. | Review within 1 month | Medium |

Child maintenance changes | Maintenance paid or received affects household income and affordability. | Income schedule, child costs, contribution formula, savings targets, debts. | Review within 1 month | Medium |

Adult dependent moves in | Care duties, bills and occupation arrangements may change. | Occupancy, bills, care costs, privacy, house rules, moving-out process. | Review within 1 month | Medium |

Relationship status change | ||||

Death of a partner | Estate, mortgage, occupation and survivorship provisions may need to be applied. | Death clause, ownership transfer, mortgage, insurance, personal belongings, notices. | Immediate review | High |

Relationship separation | Exit, sale, occupation and asset division clauses may need activating. | Move-out date, sale process, buy-out, bills, belongings, pets, dispute resolution. | Immediate review | High |

Trial separation | Temporary occupation and payment responsibilities may need clear interim rules. | Interim bills, mortgage payments, exclusive occupation, belongings, reconciliation date. | Immediate review | High |

Reconciliation after separation | Previous exit arrangements may be unsuitable once cohabitation resumes. | Suspended sale, payment arrears, renewed contributions, belongings, review date. | Review within 1 month | High |

Engagement | Future marriage may require different planning documents and asset protection. | Marriage plans, ring ownership, wedding costs, pre-nuptial agreement, property. | Review within 3 months | Medium |

Marriage | Marriage creates a different legal framework for finances and inheritance. | Pre-nuptial agreement, wills, property ownership, death benefits, household finances. | Immediate review | High |

Civil partnership | Civil partnership creates a different legal framework for finances and inheritance. | Pre-registration agreement, wills, property ownership, death benefits, finances. | Immediate review | High |

Financial change | ||||

Wedding costs incurred | Shared deposits, loans and cancellations may create financial disputes. | Wedding savings, supplier deposits, loans, cancellation costs, gift ownership. | Review within 3 months | Medium |

Relationship status change | ||||

Separated but still co-owning | Ongoing mortgage, repairs and sale decisions need post-separation rules. | Mortgage payments, occupation rent, sale timetable, repairs, insurance, buy-out. | Immediate review | High |

New partner moves in | Existing ownership and household arrangements may be affected by a third adult. | Occupancy, bills, no-interest wording, privacy, lodger or licence terms. | Immediate review | High |

Relocation | ||||

Moving within the UK | Property, family and procedure rules may differ between UK jurisdictions. | Governing law, property rules, dispute forum, tax, registration documents. | Review within 1 month | High |

Moving abroad | Jurisdiction, tax residence and enforceability may need specialist review. | Governing law, dispute forum, tax, property management, banking, service notices. | Immediate review | High |

Temporary work relocation | Two households may alter costs, occupation and contribution expectations. | Travel costs, rent, mortgage payments, utilities, absence from home. | Review within 1 month | Medium |

Relocating for family care | Care duties may affect work, housing costs and household contributions. | Relocation costs, care costs, work changes, property sale, rent or mortgage. | Review within 3 months | Medium |

Partner moves out temporarily | Contribution, occupation and return rights may need interim rules. | Bills, mortgage, rent, room use, belongings, return date, notice. | Immediate review | High |

Returning to shared home | Temporary cost-sharing terms may need ending or updating. | Contribution split, occupation, arrears, storage, travel costs, review date. | Review within 1 month | Medium |

Employment change | ||||

Permanent home working | Use of space, utilities and business equipment may affect household costs. | Utility split, workspace, equipment ownership, insurance, business visitors. | Review within 3 months | Medium |

Starting home business | Home business use may affect insurance, costs, consent and property risk. | Business use, insurance, utilities, storage, client visits, landlord or lender consent. | Immediate review | High |

Retirement | Income source, pension access and estate planning priorities may change. | Contribution split, pension income, savings use, wills, care planning. | Review within 3 months | Medium |

Career break | Reduced income and non-financial contributions may need recognition. | Bills, savings use, childcare or care work, pension contributions, review date. | Review within 1 month | Medium |

Parental leave starts | Temporary income reduction and care duties may affect contributions. | Income schedule, bills, childcare, savings use, return-to-work review. | Review within 1 month | High |

Financial change | ||||

Benefits entitlement changes | Means-tested benefits and household status may affect available income. | Income schedule, rent support, childcare support, bill split, disclosure duties. | Review within 1 month | Medium |

Relationship status change | ||||

Universal Credit couple status changes | Living with a partner can affect Universal Credit assessment as a couple. | Income disclosure, rent support, bill contributions, shortfall arrangements. | Review within 1 month | Medium |

Relocation | ||||

Tax residence changes | UK tax residence affects income, gains and overseas asset planning. | Tax liability, foreign income, property income, investment gains, notices. | Immediate review | High |

Financial change | ||||

Tax rules materially change | Changes may affect property income, gains, gifts or household budgeting. | Tax responsibility, rental income, capital gains, gift records, review thresholds. | Review at next annual review | Low |

Time-based review | ||||

Cohabitation law reforms | Legal reform could affect enforceability, remedies or recommended drafting. | Governing law, dispute resolution, property rights, financial remedies, review clause. | Review within 3 months | Medium |

Property change | ||||

Property ownership dispute arises | A co-owner or alleged beneficiary may seek court orders about land. | Beneficial shares, evidence schedule, dispute resolution, sale orders, occupation. | Immediate review | High |

Relationship status change | ||||

Domestic abuse concerns | Safety, consent and independent advice issues may affect any agreement or variation. | Occupation, contact, payment access, possessions, pets, dispute resolution, advice evidence. | Immediate review | High |

Consent concerns identified | Pressure, non-disclosure or no advice may undermine reliability of the agreement. | Execution process, disclosure schedule, independent advice, fairness, variation deed. | Immediate review | High |

Financial change | ||||

Undisclosed asset or debt found | Schedules and assumptions may be inaccurate or misleading. | Asset schedule, debt schedule, warranties, contribution formula, validity evidence. | Immediate review | High |

Family change | ||||

Getting a pet together | Care costs and ownership can become contentious on separation. | Pet ownership, vet bills, insurance, care schedule, separation arrangements. | Review within 3 months | Medium |

Financial change | ||||

High pet care costs | Ongoing costs may affect shared budgets and separation planning. | Vet bills, insurance excess, pet ownership, reimbursement, emergency decisions. | Review within 3 months | Low |

Time-based review | ||||

Annual review date | Regular checks keep contributions, assets and contact details current. | Asset schedules, income, bills, mortgage balance, insurance, emergency contacts. | Review at next annual review | Medium |

3 to 5 year full review | Longer-term changes may accumulate even without a single major trigger. | All schedules, ownership assumptions, review clause, dispute process, execution. | Review at next annual review | Medium |

Scheduled review missed | Outdated schedules weaken the agreement's usefulness in a dispute. | Asset schedule, debt schedule, income, property value, signature of variation. | Review within 1 month | Medium |

Financial change | ||||

Cost-of-living shock | Bills and fixed contribution sums may become unaffordable or outdated. | Fixed payments, utilities, food costs, emergency fund, review thresholds. | Review at next annual review | Low |

Mortgage interest rate rises | Mortgage repayments may increase and alter affordability or contribution shares. | Mortgage payment split, shortfall rules, arrears, fixed-rate expiry review. | Review within 1 month | High |

Fixed-rate mortgage ends | Payment changes can alter affordability and contribution arrangements. | Payment split, remortgage consent, arrears, equity release, budget review. | Review within 3 months | Medium |

Mortgage arrears arise | Arrears threaten the home and may create unequal liabilities. | Arrears responsibility, payment priority, default clause, sale trigger, indemnities. | Immediate review | High |

Rent arrears arise | Arrears may affect both tenants and require urgent payment rules. | Rent payments, arrears responsibility, notice, deposit deductions, guarantor issues. | Immediate review | High |

Utility arrears arise | Unpaid bills may affect credit, household services and contribution fairness. | Bill split, arrears repayment, account holder responsibility, emergency fund. | Review within 1 month | Medium |

Acting as guarantor | Guarantee liability may reduce ability to meet shared costs. | Debt disclosure, indemnities, affordability, household contribution fallback. | Review within 1 month | Medium |

Compensation payment received | Personal injury or other compensation may be intended for one partner only. | Separate property, care costs, adaptations, lost earnings, trust arrangements. | Review within 1 month | High |

Relationship status change | ||||

Imprisonment or conviction | Income, occupation, mortgage and care arrangements may be disrupted. | Bills, mortgage, childcare, sale rights, belongings, communication, default. | Immediate review | High |

Relocation | ||||

Immigration status changes | Right to live, work or remain in the UK may affect housing and income. | Occupation, rent or mortgage, income, relocation, notices, support arrangements. | Immediate review | High |

Property change | ||||

Lender consent issue arises | Occupiers, letting or business use may breach mortgage conditions. | Consent obligations, letting, lodgers, business use, default responsibility. | Immediate review | High |

Landlord consent issue arises | Extra occupiers, pets or business use may breach tenancy terms. | Consent obligations, pets, lodgers, business use, breach costs, notice. | Immediate review | High |

Time-based review | ||||

Legal advice flags issue | Drafting, execution or disclosure problems may reduce practical protection. | Execution, disclosure, independent advice, fairness, property schedules, variation. | Immediate review | High |

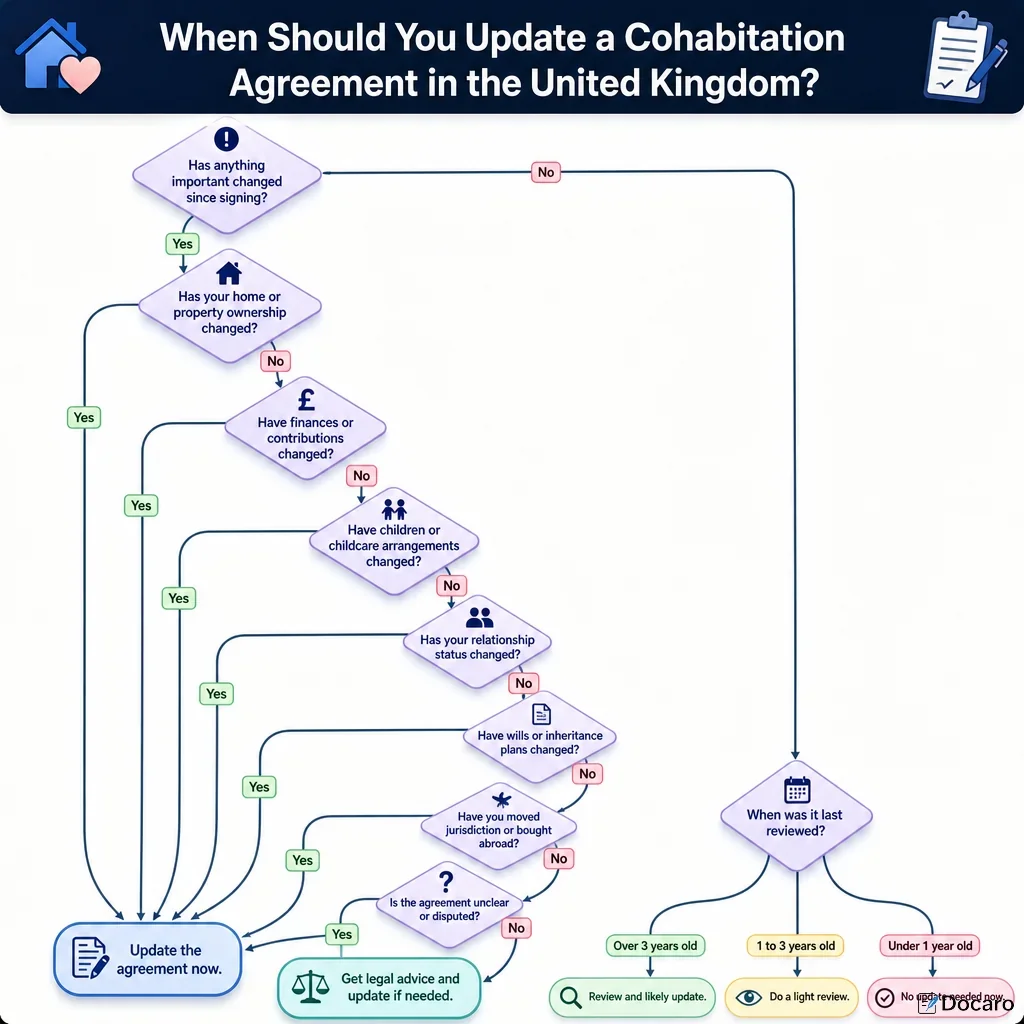

When Should A UK Cohabitation Agreement Be Reviewed?

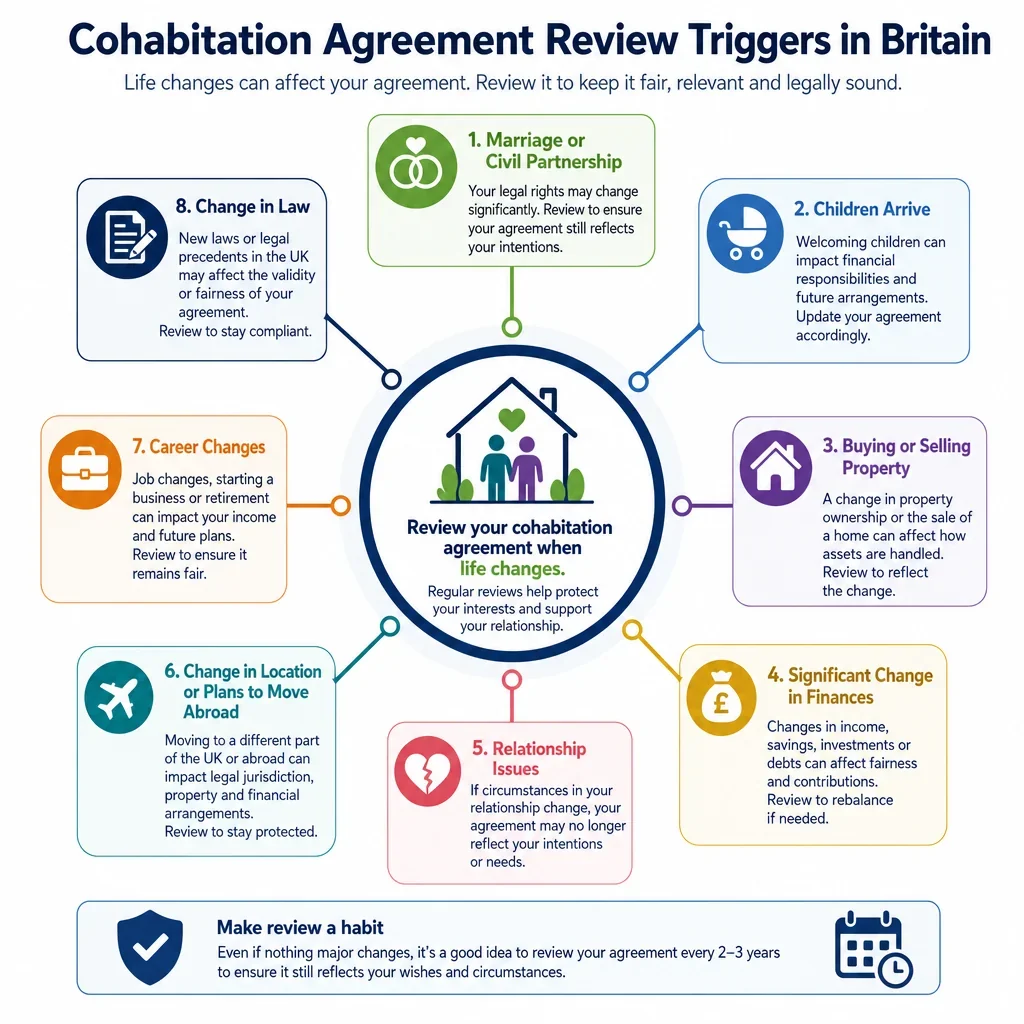

A cohabitation agreement should be reviewed whenever the facts it relies on have materially changed. The highest-priority triggers are usually property purchases, mortgage changes, unequal contributions, the birth or adoption of a child, separation, marriage or civil partnership plans, major inheritance or gift funding, and serious illness or death-planning changes.

Which Changes Most Often Affect Ownership And Money Clauses?

- Property and mortgage changes can affect beneficial shares, occupation rights, sale procedures, buy-out rights, and responsibility for mortgage payments, repairs and insurance.

- Large financial changes, such as redundancy, inheritance, new debt or business ownership, can make existing payment and asset schedules inaccurate or unfair.

- Family changes, especially having children, can affect household contributions, childcare costs, occupation arrangements and practical support obligations.

Why Are Relationship Status Changes Especially Important?

Marriage or civil partnership can significantly change legal rights and may make a cohabitation agreement unsuitable as the main planning document. Separation is also a high-priority trigger because exit clauses, sale arrangements, division of belongings and payment responsibilities often need to be applied or renegotiated quickly.

How Often Should The Agreement Be Checked If Nothing Major Happens?

Even without a major life event, an annual review is sensible. A fuller review every 3 to 5 years can help ensure the agreement still reflects property values, mortgage balances, income, children, debts and intentions.

FAQs

You Might Also Be Interested In