AI Generated British Share Purchase Agreement

PDF & Word - 2026 Updated

Docaro Pricing

When do you need a Business Sale Agreement in the United Kingdom?

British Legal Rules for a Business Sale Agreement

Using the incorrect structure for a business sale agreement may fail to properly allocate risks, liabilities, or tax implications between parties.

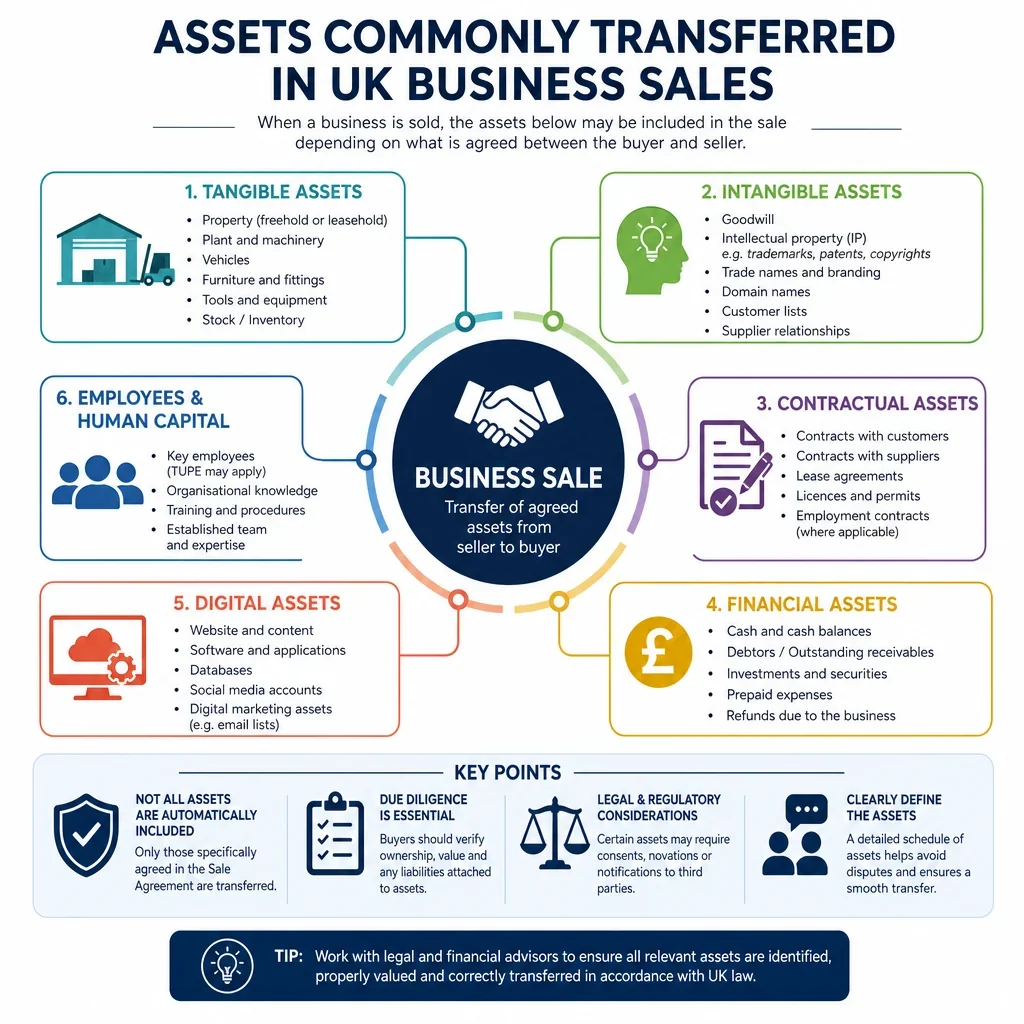

What a Proper Business Sale Agreement Should Include

- Parties InvolvedClearly identifies the buyer and seller, including their full names and contact details.

- Business DescriptionDetails what is being sold, such as assets, stock, or the entire company.

- Purchase PriceSpecifies the total amount to be paid and how it will be structured, like lump sum or installments.

- Payment TermsOutlines when and how payments will be made, including any deposits or conditions.

- Warranties and RepresentationsProvides assurances from the seller about the business's condition, like no hidden debts or legal issues.

- Conditions PrecedentLists requirements that must be met before the sale completes, such as approvals or due diligence.

- Non-Compete ClauseRestricts the seller from starting a similar business nearby for a set period after the sale.

- ConfidentialityRequires both parties to keep sensitive information private during and after the deal.

- IndemnitiesAgrees that the seller will cover the buyer for any losses from pre-sale issues.

- Closing and CompletionDefines the date and steps for finalizing the sale, including document exchanges.

- Governing LawStates that the agreement follows UK laws and which courts handle disputes.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Business Sale Agreement Template

Below is a free template example of a Business Sale Agreement for use in the United Kingdom generated by our AI model.

The clauses in your actual Business Sale Agreement will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Business Sale Agreement

1DEFINITIONS AND INTERPRETATION

In this Agreement the following words and expressions shall have the following meanings unless the context requires otherwise.

Assets means all of the assets of the Business to be transferred to the Buyer as listed in Schedule 1 (Assets).

Assumed Liabilities means the liabilities of the Business to be assumed by the Buyer as listed in Schedule 3 (Assumed Liabilities).

Business means the retail coffee shop operating from the Premises in central London including all equipment, inventory, customer relationships, the Lease, and the Goodwill of the business carried on by the Seller.

Completion means completion of the sale and purchase of the Business in accordance with clause 11.

Completion Date means 1 December 2024 or such other date as the parties may agree in writing.

Consideration means the sum of two hundred and fifty thousand pounds sterling (GBP 250,000) being the total consideration payable by the Buyer to the Seller for the Business.

Disclosure Letter means the letter dated with the same date as this Agreement from the Seller to the Buyer disclosing information in relation to the Warranties.

Excluded Assets means the assets of the Business listed in Schedule 2 (Excluded Assets).

Excluded Liabilities means the liabilities of the Business listed in Schedule 4 (Excluded Liabilities).

Goodwill means the goodwill of the Business together with the exclusive right for the Buyer to represent itself as carrying on the Business in succession to the Seller and to use the name "London Brews".

Intellectual Property means all patents, trade marks, service marks, design rights, copyright, database rights, trade secrets, know-how and other intellectual property rights (whether registered or unregistered) used in or relating to the Business including those listed in Schedule 1.

Lease means the lease of the Premises dated 1 April 2020 between ABC Properties Ltd and the Seller.

Material Contracts means the contracts listed in Schedule 1 together with the Lease and all customer and supplier contracts material to the Business.

Premises means 123 High Street, London EC1A 1BB.

Seller means London Brews Limited a company incorporated in England and Wales with registered number 09456789 whose registered office is at 123 High Street, London EC1A 1BB.

Buyer means Brew Acquisition Limited a company incorporated in England and Wales with registered number 12345678 whose registered office is at 456 Oxford Road, Manchester M1 1AA.

In this Agreement, unless the context otherwise requires: (a) words in the singular include the plural and vice versa and words in one gender include any other gender; (b) a reference to a statute or statutory provision includes a reference to that statute or statutory provision as amended, consolidated and in force from time to time and to all subordinate legislation made under it from time to time; (c) references to clauses, schedules and recitals are to clauses, schedules and recitals of this Agreement; (d) the headings are for convenience only and shall not affect the interpretation of this Agreement; and (e) references to "including" or "include" shall be construed without limitation.

2RECITALS

The Seller is a company incorporated in England and Wales on 15 March 2015 with registered number 09456789 and whose registered office is at 123 High Street, London EC1A 1BB.

The Seller carries on the Business of a single retail coffee shop from the Premises in central London.

The Business involves the sale of coffee and related products to customers through in-store and takeaway services and employs eight (8) members of staff.

The Seller has agreed to sell and the Buyer has agreed to purchase the Business as a going concern on the terms set out in this Agreement.

3SALE AND PURCHASE

Subject to the terms of this Agreement, the Seller shall sell and the Buyer shall purchase the Business as a going concern with effect from the Completion Date free from all Encumbrances (except as disclosed in the Disclosure Letter) together with the Assets and the Assumed Liabilities but excluding the Excluded Assets and the Excluded Liabilities.

The sale of the Business shall constitute a transfer of a business as a going concern for the purposes of Article 5 of the Value Added Tax Act 1994 and in accordance with VAT Notice 700/9. The parties shall use all reasonable endeavours to ensure that the sale qualifies as a transfer of a going concern (TOGC) so that no VAT is chargeable on the sale.

4ASSETS SOLD

The Assets include all tangible and intangible property used in the operation of the Business as set out in Schedule 1 (Assets).

5SCHEDULE OF ASSETS

The Assets transferred pursuant to this Agreement are as follows with the agreed apportionment of the Consideration for tax purposes:

Goodwill: GBP 150,000;

Equipment and fixtures (including 2 x commercial espresso machines, 4 x grinders, 3 x refrigerators, tables, chairs and point of sale system): GBP 45,000;

Inventory and stock (coffee beans, cups, food items and consumables): GBP 15,000;

Intellectual Property (including trademarks for "London Brews", domain name londonbrews.co.uk, copyright in menus and recipes): GBP 25,000;

Customer lists, relationships and lists of suppliers: GBP 10,000;

Lease and benefit of contracts: GBP 5,000.

Full details of the equipment, inventory, customer lists, Intellectual Property register and the Lease are set out in the annexes to Schedule 1.

6EXCLUDED ASSETS

The following shall be excluded from the sale of the Business and shall remain the property of the Seller:

All cash and cash equivalents held by the Business at the Completion Date;

All book debts and receivables;

The Seller's pension schemes and associated records (subject to TUPE transfer of employees);

Any vehicles owned by the Seller.

7ASSUMED LIABILITIES

The Buyer shall assume only the Assumed Liabilities with effect from the Completion Date. The Buyer shall not assume any other liabilities of the Seller.

The Assumed Liabilities are as follows and total GBP 22,500:

Trade creditors for goods and services supplied after 1 November 2024 (estimated at GBP 7,500);

All liabilities under the Lease from the Completion Date onwards (rent of GBP 5,000 per month);

All liabilities to employees that transfer under TUPE 2006 (including accrued holiday pay post 1 November 2024).

8EXCLUDED LIABILITIES

The Excluded Liabilities shall remain the responsibility of the Seller and shall not pass to the Buyer. The Seller shall indemnify the Buyer against all Excluded Liabilities.

The Excluded Liabilities include (but are not limited to) the following and total approximately GBP 17,500:

All trade creditors for goods and services supplied on or before 31 October 2024 (GBP 8,000);

All pre-Completion employee liabilities including unpaid holiday pay, bonuses and claims arising before Completion;

All corporation tax, VAT, PAYE and National Insurance liabilities arising on or before Completion;

Any pending or threatened litigation or disputes as at the Completion Date;

Any environmental liabilities arising from operations up to Completion.

9PURCHASE PRICE AND APPORTIONMENT

The total Consideration for the sale of the Business shall be GBP 250,000 (exclusive of VAT, if any). The apportionment of the Consideration between the Assets for tax purposes is set out in clause 5.1.

The Consideration shall be adjusted following Completion in accordance with the Completion Accounts prepared pursuant to clause 9.3.

The Seller shall procure that draft Completion Accounts for the Business are prepared as at the Completion Date in accordance with generally accepted accounting principles in the United Kingdom. The Buyer shall have 20 Business Days to review and raise objections. If the parties cannot agree on the Completion Accounts within 10 Business Days of the Buyer raising objections, the matter shall be referred to an independent accountant (acting as expert and not arbitrator) whose decision shall be final. Any adjustment to the Consideration shall be paid within 5 Business Days of agreement or determination of the Completion Accounts.

10PAYMENT TERMS AND ESCROW

On Completion the Buyer shall pay GBP 175,000 by electronic bank transfer to the Seller's solicitors' client account.

The balance of GBP 75,000 shall be paid into an escrow account on Completion to be held and released in accordance with the terms of the escrow agreement in the form set out in Schedule 6. The escrow shall be held for a period of 12 months to cover any warranty or indemnity claims.

Any adjustment to the Consideration pursuant to clause 9 shall be paid by electronic bank transfer to the relevant party's nominated account within 5 Business Days of agreement or determination.

11COMPLETION

Completion shall take place on the Completion Date at the offices of the Seller's solicitors at 10.00 am (or such other time and place as the parties may agree).

On Completion:

the Buyer shall pay the sums due under clause 10;

the Seller shall deliver to the Buyer: (i) executed assignments of the Lease, Material Contracts and Intellectual Property; (ii) a duly executed transfer of the lease and any licences/permits (including food premises registration and any alcohol licence if applicable); (iii) all books, records, customer lists and other documents relating to the Business; (iv) keys, passwords and access codes to the Premises and equipment; and (v) evidence of discharge of all Encumbrances over the Assets;

the Seller shall give vacant possession of the Premises;

the parties shall execute the escrow agreement and any other ancillary documents.

If Completion does not take place on the Completion Date due to the default of one party, the non-defaulting party may elect to rescind this Agreement without prejudice to any claim for damages.

12CONDITIONS PRECEDENT

Completion is conditional upon satisfaction (or waiver) of the following conditions:

the Buyer having completed satisfactory financial, legal, commercial and operational due diligence;

no Material Adverse Change having occurred in the Business between the date of this Agreement and the Completion Date;

all necessary third party consents being obtained including the consent of the landlord to the assignment of the Lease;

transfer of all insurance policies into the name of the Buyer or novation of such policies;

all food safety, health and safety and environmental permits and licences being capable of transfer or the Buyer having obtained equivalent permits;

the Seller's warranties being true and accurate in all material respects as at the Completion Date.

The long stop date for satisfaction of the conditions is 31 December 2024. If the conditions have not been satisfied (or waived) by the long stop date, either party may terminate this Agreement by written notice to the other, in which event this Agreement shall be of no further effect and no party shall have any claim against the other save in respect of any prior breach.

Both parties shall use all reasonable endeavours to procure the satisfaction of the conditions precedent as soon as possible.

13WARRANTIES AND REPRESENTATIONS

The Seller warrants to the Buyer that each of the warranties set out in Schedule 5 (Warranties) is true and accurate in all respects and not misleading as at the date of this Agreement and will be true and accurate as at the Completion Date. The Warranties are given on an absolute basis subject only to matters fairly disclosed in the Disclosure Letter. The Warranties shall be separate and independent and shall not be limited by reference to any other provision of this Agreement.

The Buyer warrants to the Seller that:

it has sufficient funds or binding financing arrangements in place to complete the purchase of the Business;

there are no legal or regulatory impediments that would prevent the Buyer from completing the transaction;

it has full power and authority to enter into and perform its obligations under this Agreement;

it is in compliance with all applicable laws relevant to the transaction including the Bribery Act 2010 and the Companies Act 2006.

The full warranties given by the Seller are set out in Schedule 5 and cover (without limitation) the following matters: accuracy and completeness of accounts; no undisclosed liabilities; ownership of and condition of Assets; validity and performance of Material Contracts; ownership, validity and non-infringement of Intellectual Property; compliance with all laws (including food hygiene under the Food Safety Act 1990, health and safety, employment law, environmental law, data protection under the UK GDPR and the Data Protection Act 2018); employee and TUPE compliance; pensions and auto-enrolment compliance under the Pensions Act 2008; adequacy of insurance; no litigation; tax compliance under the Corporation Tax Act 2010, Value Added Tax Act 1994 and other relevant tax statutes; and environmental matters.

14DISCLOSURE LETTER

The Seller has delivered the Disclosure Letter to the Buyer on the date of this Agreement. The Disclosure Letter qualifies the Warranties and matters disclosed in it shall be deemed to be disclosed against all of the Warranties to which they are relevant. The Buyer acknowledges that it has reviewed the Disclosure Letter and accepts the disclosures contained in it.

The Disclosure Letter includes (without limitation) the following specific disclosures:

Against the accounts warranty: the accounts for the year ended 31 December 2023 are attached;

Against the assets and equipment warranty: one of the commercial espresso machines required a major repair on 15 May 2024 at a cost of GBP 2,500 which has been completed and the machine is now fully operational;

Against the litigation warranty: there are no claims but a former employee raised a grievance in September 2024 which has been resolved;

Such other matters as are set out in the Disclosure Letter in the form attached as Schedule 7.

15INDEMNITIES

The Seller shall indemnify and hold harmless the Buyer against all losses, costs, damages and expenses suffered or incurred by the Buyer as a result of or in connection with:

any pre-Completion tax liabilities of the Business (including corporation tax, VAT, PAYE, National Insurance and stamp duty) under the Corporation Tax Act 2010, Value Added Tax Act 1994, Income Tax (Earnings and Pensions) Act 2003 and other relevant UK tax legislation;

any Excluded Liabilities;

any breach of the Warranties relating to title to Assets, capacity and authority, and environmental matters;

any claims arising from failure to comply with TUPE 2006 including failure to inform and consult.

The conduct of claims shall be in accordance with clause 16.5.

16LIMITATIONS ON LIABILITY

The limitations on liability set out in this clause 16 shall not apply to claims for breach of the fundamental warranties (title, capacity, authority and tax), indemnities in clause 15, fraud or fraudulent misrepresentation.

The maximum aggregate liability of the Seller for all claims under the Warranties and indemnities (other than fundamental warranties and tax claims) shall not exceed GBP 250,000.

No claim shall be brought by the Buyer under the Warranties unless the amount of the claim (or a series of related claims) exceeds a de minimis threshold of GBP 2,500. Claims below this threshold shall be disregarded.

A tipping basket of GBP 10,000 shall apply to warranty claims (other than fundamental warranties). Once the basket is exceeded, the Seller shall be liable for the whole amount of all claims including those below the basket.

The limitation period for claims under the Warranties (other than tax and fundamental warranties) shall be 24 months from the Completion Date. Tax claims and claims under the tax indemnity shall be limited to 7 years from the Completion Date. Claims must be notified to the Seller in writing as soon as reasonably practicable and in any event within the relevant limitation period, giving reasonable details of the claim.

The Seller shall have conduct of any third party claims notified under this clause. The Buyer shall provide reasonable assistance and shall not admit liability or settle any claim without the Seller's prior written consent (not to be unreasonably withheld).

17NON-COMPETE AND RESTRICTIVE COVENANTS

In order to assure the value of the Goodwill to the Buyer, the Seller covenants with the Buyer that it shall not, and shall procure that its group companies shall not, for a period of 12 months from the Completion Date directly or indirectly:

carry on or be engaged in any competing business involving the operation of a coffee shop or cafe selling similar products within a radius of 3 miles of the Premises;

solicit or canvass the custom of any person who was a customer of the Business in the 12 months prior to Completion;

offer to employ or engage or solicit any person who was an employee of the Business at Completion.

The Seller shall keep all information relating to the Business confidential and shall not use it for any purpose after Completion.

The covenants in this clause 17 are considered reasonable by the parties in terms of duration, scope and geography for the protection of the Goodwill. If any covenant is found to be unenforceable under the restraint of trade doctrine at common law or the Competition Act 1998, the parties agree that the court may modify the covenant to the minimum extent necessary to make it enforceable or the invalid provision shall be severed and the remainder shall continue in full force.

18EMPLOYEES AND TUPE

The sale of the Business shall constitute a relevant transfer for the purposes of the Transfer of Undertakings (Protection of Employment) Regulations 2006 (TUPE).

The Seller shall provide to the Buyer not less than 14 days before the Completion Date a list of all employees engaged in the Business (the Employee List) containing each employee's name, job title, date of commencement of employment, salary, benefits, notice period, holiday entitlement and any other material terms. The current Employee List is set out in Schedule 8.

The Seller warrants that it has complied with its obligations to inform and consult the employees and their representatives under Regulation 13 of TUPE. The Seller shall indemnify the Buyer against any claims arising from failure to inform and consult.

The Buyer shall comply with its obligations under TUPE to take over the contracts of employment of the transferring employees. The Seller shall indemnify the Buyer against all employment liabilities arising prior to Completion (including unfair dismissal, discrimination or breach of contract claims).

The Business operates a compliant auto-enrolment pension scheme under the Pensions Act 2008. All pension contributions have been paid up to date. The Seller shall have no liability for pension liabilities after Completion.

19INTELLECTUAL PROPERTY RIGHTS

The Seller warrants that it is the sole legal and beneficial owner of all the Intellectual Property used in the Business free from all Encumbrances. Full details of the Intellectual Property are set out in Schedule 1 including the trademark "London Brews", the domain name londonbrews.co.uk and copyright in menus, recipes and branding materials.

On Completion the Seller shall execute an assignment of all Intellectual Property to the Buyer in a form reasonably required by the Buyer. The Seller waives all moral rights in any copyright works assigned.

The Seller warrants that the use of the Intellectual Property by the Business does not infringe the rights of any third party and that there are no claims or threatened claims in relation to the Intellectual Property.

20DATA PROTECTION

The Seller warrants that it has at all times complied with the UK GDPR, the Data Protection Act 2018 and all applicable data protection laws in respect of the Business. The Seller has in place appropriate technical and organisational measures and has not suffered any personal data breach.

The transfer of personal data relating to customers, employees and suppliers shall be carried out in compliance with the UK GDPR. The parties shall enter into a data processing addendum if required. The Seller shall indemnify the Buyer against any losses arising from breach of data protection law prior to Completion.

21PENSIONS

The Business has complied with its auto-enrolment obligations under the Pensions Act 2008. All employees have been auto-enrolled in a qualifying pension scheme and all contributions due have been paid.

There are no defined benefit pension schemes. The only pension arrangement is a defined contribution group personal pension scheme. The Seller shall have no liability for pensions after Completion.

22ENVIRONMENTAL MATTERS

The Seller warrants that the Business has at all times complied with all applicable environmental laws (including the Environmental Protection Act 1990) and holds all necessary environmental permits (none of which will be revoked by the sale). There has been no contamination of the Premises.

The Seller shall indemnify the Buyer against any environmental liabilities arising prior to Completion.

23INSURANCE

The Business maintains adequate insurance including public liability (GBP 5 million), employers' liability (GBP 10 million) and property damage. The current policies are listed in Schedule 9. The Seller warrants that all premiums have been paid and there are no outstanding claims.

The Seller shall use reasonable endeavours to procure the novation or assignment of the insurance policies to the Buyer with effect from Completion. Pending novation, the Seller shall hold the benefit of the policies on trust for the Buyer.

24VAT AND TOGC

The parties intend that the sale of the Business shall be treated as a TOGC in accordance with Article 5 of the Value Added Tax Act 1994 and VAT Notice 700/9. The Buyer is registered for VAT and will use the Assets in carrying on the same kind of business as the Seller. No election to waive exemption has been made in respect of the Premises.

If for any reason the sale does not qualify as a TOGC, the Consideration shall be deemed to be inclusive of VAT and the Buyer shall pay to the Seller any VAT due within 5 Business Days of a valid VAT invoice being issued.

25BOILERPLATE

This Agreement constitutes the entire agreement between the parties relating to the subject matter and supersedes all prior agreements, understandings or arrangements (whether oral or in writing). The Buyer acknowledges that it has not entered into this Agreement in reliance on any representation, warranty or undertaking not expressly set out in this Agreement.

No variation of this Agreement shall be effective unless in writing and signed by or on behalf of each party.

A person who is not a party to this Agreement shall have no rights under the Contracts (Rights of Third Parties) Act 1999 to enforce any term of this Agreement.

Neither party shall be liable for any failure or delay in performing its obligations under this Agreement to the extent that such failure or delay is caused by a Force Majeure Event (meaning any circumstance beyond a party's reasonable control including acts of God, war, riot, strikes, governmental action or terrorism).

Each party shall comply with the Bribery Act 2010 and shall not engage in any form of bribery or corruption in connection with this Agreement.

This Agreement may be executed in any number of counterparts, each of which when executed and delivered shall constitute a duplicate original, but all counterparts together shall constitute one agreement.

This Agreement and any dispute or claim arising out of or in connection with it or its subject matter or formation (including non-contractual disputes or claims) shall be governed by and construed in accordance with the laws of England and Wales.

Each party irrevocably agrees that the courts of England and Wales shall have exclusive jurisdiction over any dispute or claim that arises out of or in connection with this Agreement or its subject matter or formation.

26EXECUTION

Executed and delivered as a deed by the parties on the date first written above.

SIGNED as a DEED by LONDON BREWS LIMITED acting by a director in the presence of a witness:

_________________________ Director

Witness signature: _________________________

Witness name: _________________________

Witness address: _________________________

SIGNED as a DEED by BREW ACQUISITION LIMITED acting by a director in the presence of a witness:

_________________________ Director

Witness signature: _________________________

Witness name: _________________________

Witness address: _________________________

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Business Sale Agreement in the United Kingdom

United Kingdom Reference Legislation

Business Sale Agreement FAQs

Document Generation FAQs

Related Articles