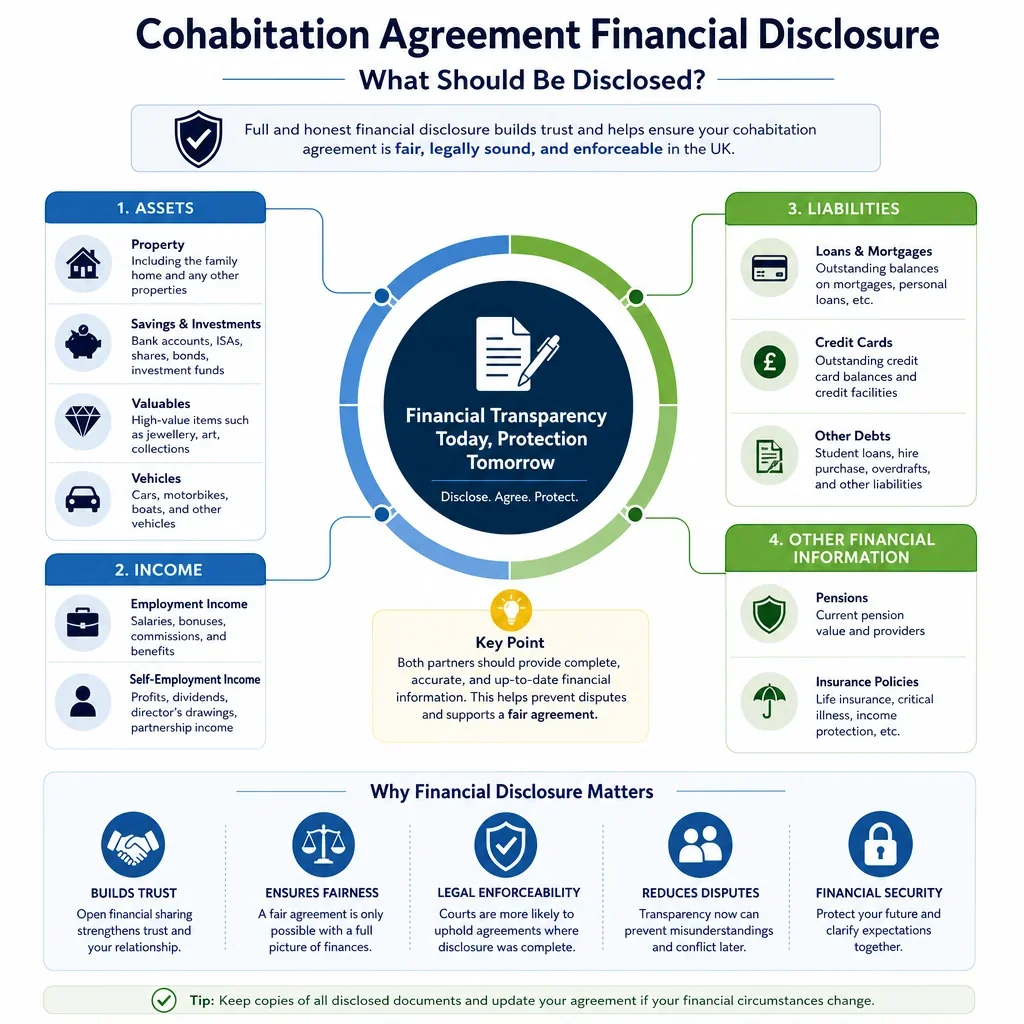

Financial Disclosure Checklist For United Kingdom Cohabitation Agreements

Created:

This checklist helps readers understand the key financial details to gather before preparing a cohabitation agreement in the United Kingdom. It is useful for promoting transparency, reducing disputes, and supporting informed decisions when using an AI Generated British Cohabitation Agreement.

Disclosure Item | Why It Matters | Example Evidence | Relevant Stage | Disclosure Importance |

|---|---|---|---|---|

Income | ||||

Recent payslips | Shows regular employment income and ability to meet shared costs. | Last 3 to 6 monthly payslips. | Before drafting | High |

P60 or annual earnings summary | Confirms annual PAYE income and tax position. | Latest P60 or employer annual pay statement. | Before drafting | Medium |

Self-assessment tax returns | Shows variable income for contribution and affordability planning. | SA302, tax calculation, tax year overview. | Before drafting | High |

Director salary and dividends | Shows income drawn from a company and potential variability. | Dividend vouchers, payslips, company accounts. | Before drafting | High |

Benefits and Universal Credit | Shows benefit income that may affect household budgeting. | Award notices, online journal, bank entries. | Before drafting | Medium |

Child maintenance received | Distinguishes personal income from money intended for children. | CMS calculation, private agreement, bank statements. | Before drafting | Medium |

Rental income | Shows property-derived income and related tax or mortgage issues. | Tenancy agreement, rent statements, tax return. | Before drafting | High |

Savings and investments | ||||

Current and savings account balances | Identifies separate funds and potential deposit contributions. | Recent bank and savings statements. | Before drafting | High |

Joint bank accounts | Clarifies ownership, contributions and use of shared funds. | Joint account statements and account terms. | During drafting | High |

ISAs | Records tax-efficient savings that may remain separate property. | ISA statements and provider valuations. | Before drafting | Medium |

Stocks, shares and funds | Identifies investment assets and whether gains remain separate. | Platform statements, contract notes, valuations. | Before drafting | Medium |

Cryptocurrency holdings | Captures volatile assets and potential tax liabilities. | Exchange statements, wallet records, tax reports. | Before drafting | Medium |

Premium Bonds and NS&I savings | Records savings that may be overlooked in disclosure. | NS&I statement or online account printout. | Before signing | Low |

Inheritance or gifted money | Clarifies whether family money is separate or contributed to the home. | Gift letter, probate papers, bank transfer records. | Before drafting | High |

Trust interests | Identifies contingent or protected family wealth. | Trust deed, trustee letter, distribution statements. | Before drafting | Medium |

Property ownership | ||||

Land Registry title register | Confirms legal owner, title number and registered restrictions. | Official copy register and title plan. | Before drafting | High |

Declaration of trust | Records beneficial shares and should align with the agreement. | Signed declaration or trust deed. | During drafting | High |

Joint tenants or tenants in common status | Affects survivorship and each partner's property share. | TR1, title register, Form A restriction. | Before signing | High |

Mortgage balance and terms | Shows secured debt, repayment obligations and exit costs. | Mortgage offer, annual statement, redemption figure. | Before drafting | High |

Home deposit contributions | Protects unequal contributions and repayment expectations. | Completion statement, bank transfers, gift letters. | During drafting | High |

Current property valuation | Helps calculate equity and buyout mechanisms. | Estate agent appraisals, RICS valuation, online estimates. | During drafting | Medium |

Renovation contributions | May affect reimbursement or beneficial interest arguments. | Invoices, receipts, bank transfers, photos. | During drafting | High |

Stamp duty and purchase costs paid | Records unequal acquisition costs and repayment intentions. | Completion statement, SDLT return, solicitor ledger. | During drafting | Medium |

Other owned properties | Identifies separate assets, rental income and secured liabilities. | Title registers, mortgage statements, tenancy records. | Before drafting | High |

Household expenses | ||||

Service charges and ground rent | Allocates recurring leasehold costs and arrears responsibility. | Managing agent demands, lease, payment records. | During drafting | Medium |

Tenancy agreement and rent | Shows who is liable for rent and tenancy obligations. | AST, rent schedule, landlord correspondence. | Before drafting | High |

Debts and liabilities | ||||

Secured loans or second charges | Affects property equity and sale or refinance planning. | Loan agreement, title charge, redemption statement. | Before drafting | High |

Personal loans | Clarifies separate and shared repayment responsibility. | Loan agreement, balance statement, payment history. | Before drafting | High |

Credit card balances | Identifies short-term debts and household spending liabilities. | Latest card statements and transaction history. | Before signing | Medium |

Overdrafts | Shows ongoing cashflow pressure and bank debt. | Bank statements and overdraft limit confirmation. | Before signing | Medium |

Car finance agreements | Separates vehicle ownership from finance liability. | HP, PCP or lease agreement and settlement figure. | Before drafting | Medium |

Student loans | Affects net income and long-term affordability. | Student Loans Company statement, payslip deductions. | Before drafting | Low |

Tax arrears or HMRC liabilities | Identifies priority debts that may affect shared finances. | HMRC statements, payment plans, tax calculations. | Before signing | High |

Personal guarantees | Reveals contingent liabilities that could affect assets. | Guarantee deed, lender correspondence, company loan papers. | Before drafting | High |

CCJs and enforcement action | Shows serious debt risk and credit implications. | Judgment, Registry Trust entry, court correspondence. | Before signing | High |

Bankruptcy or IVA status | May affect property, credit and ability to meet obligations. | Insolvency register entry, IVA proposal, trustee letters. | Before signing | High |

Household expenses | ||||

Council tax liability | Allocates ongoing local tax and arrears responsibility. | Council tax bill, payment schedule, arrears notice. | During drafting | Medium |

Utility bills | Sets how recurring bills are divided and paid. | Gas, electricity, water and broadband bills. | During drafting | Medium |

Groceries and household supplies | Helps define fair routine spending contributions. | Budget spreadsheet, receipts, card statements. | During drafting | Low |

Childcare costs | Allocates child-related costs without confusing property rights. | Nursery invoices, childminder contract, payment records. | During drafting | High |

School fees and education costs | Clarifies responsibility for major child-related expenditure. | Fee invoices, school account statements, payment plan. | During drafting | Medium |

Repairs and maintenance budget | Separates routine maintenance from capital improvements. | Quotes, invoices, annual budget, service contracts. | During drafting | Medium |

Insurance and pensions | ||||

Buildings and contents insurance | Shows cover for the home and who pays premiums. | Policy schedule, renewal notice, premium receipts. | During drafting | Medium |

Life insurance policies | May support mortgage protection or survivor arrangements. | Policy schedule, trust form, beneficiary nomination. | During drafting | High |

Income protection or critical illness cover | Helps plan affordability if illness prevents work. | Policy schedule, exclusions, benefit amount. | During drafting | Medium |

Workplace and private pensions | Records long-term assets and death benefit nominations. | Annual pension statement, provider valuation, nomination form. | Before signing | Medium |

Death-in-service benefits | May affect survivor planning outside marriage or civil partnership. | Employer benefit booklet, nomination form, HR confirmation. | Before signing | Medium |

Major personal assets | ||||

Cars and motor vehicles | Clarifies ownership, finance and use of valuable vehicles. | V5C, purchase invoice, finance settlement, valuation. | Before drafting | Medium |

Jewellery, watches and valuables | Avoids disputes over high-value personal items. | Receipts, insurance schedule, valuation certificates. | Before signing | Low |

Art, antiques and collections | Records ownership of appreciating or sentimental assets. | Valuations, purchase records, insurance schedules. | Before signing | Medium |

Business shares or partnership interests | Identifies valuable business assets and related liabilities. | Companies House filings, shareholders agreement, accounts. | Before drafting | High |

Furniture and appliances | Helps divide jointly bought household items fairly. | Receipts, inventory, photos, bank statements. | During drafting | Low |

Household expenses | ||||

Pets and animal expenses | Clarifies ownership, care costs and insurance responsibility. | Microchip record, vet bills, insurance policy. | During drafting | Low |

Debts and liabilities | ||||

Credit report summary | Reveals undisclosed debts, defaults and linked finances. | Experian, Equifax or TransUnion statutory report. | Before signing | Medium |

Savings and investments | ||||

Emergency fund arrangements | Clarifies whether shared savings can cover unexpected costs. | Savings account statement, agreed budget note. | During drafting | Low |

Property ownership | ||||

Existing will provisions | Checks whether property and survivor intentions are consistent. | Copy will, codicil, solicitor confirmation. | Before signing | Medium |

Savings and investments | ||||

Shared savings goals | Defines ownership of money saved for holidays, repairs or purchases. | Savings statements, budget plan, contribution schedule. | During drafting | Medium |

Debts and liabilities | ||||

Loans between partners | Distinguishes gifts from repayable advances. | Loan note, messages, bank transfers, repayment schedule. | During drafting | High |

Family loans | Clarifies whether family money must be repaid or is a gift. | Loan agreement, gift letter, transfer records. | Before signing | High |

Savings and investments | ||||

Separation and moving costs fund | Plans how immediate exit costs will be funded. | Savings statement, agreed contribution schedule. | During drafting | Low |

Household expenses | ||||

Past household contribution history | Shows existing practice before new written terms are agreed. | Bank transfers, standing orders, shared spreadsheet. | Before drafting | Medium |

Property ownership | ||||

Trusts of Land and Appointment of Trustees Act 1996 context | Property disputes between cohabitants may involve beneficial interests in land. | Title register, declaration of trust, contribution records. | Before drafting | High |

Law of Property Act 1925 section 53 context | Declarations of trust over land generally need signed written evidence. | Signed trust declaration or written property ownership terms. | During drafting | High |

What Financial Disclosure Is Most Important For A UK Cohabitation Agreement?

Property, mortgage liability, deposits, debts and household contributions are usually the highest-impact disclosures because they affect who owns what, who pays what, and what should happen if the relationship ends. In England and Wales, cohabitants do not acquire automatic financial rights simply by living together, so clear evidence of ownership and contributions is especially important.

What Documents Should Cohabiting Partners Gather Before Drafting?

- Land Registry title documents, mortgage statements and deposit evidence help show legal ownership, beneficial interests and repayment responsibility.

- Bank statements, payslips, tax returns and benefit evidence help assess affordability and agree fair household contributions.

- Loan, credit card and overdraft statements help identify debts that should remain separate or be shared.

- Pension, life insurance and protection policy details help align the agreement with nominations, wills and estate planning.

Why Should Disclosure Be Updated Before Signing?

A cohabitation agreement is stronger in practice when both partners understand the other\'s financial position before signing. Material changes, such as a new mortgage, redundancy, large inheritance, pregnancy, or a major renovation contribution, should be checked before signature and kept with the signed agreement for record keeping.

Want to Generate Your own Cohabitation Agreement?

Docaro AI can help you write your own Cohabitation Agreement for use in the United Kingdom in minutes.

FAQs

It is a list of financial information and documents each partner should consider sharing before signing a cohabitation agreement in the United Kingdom.

Show All FAQs

You Might Also Be Interested In

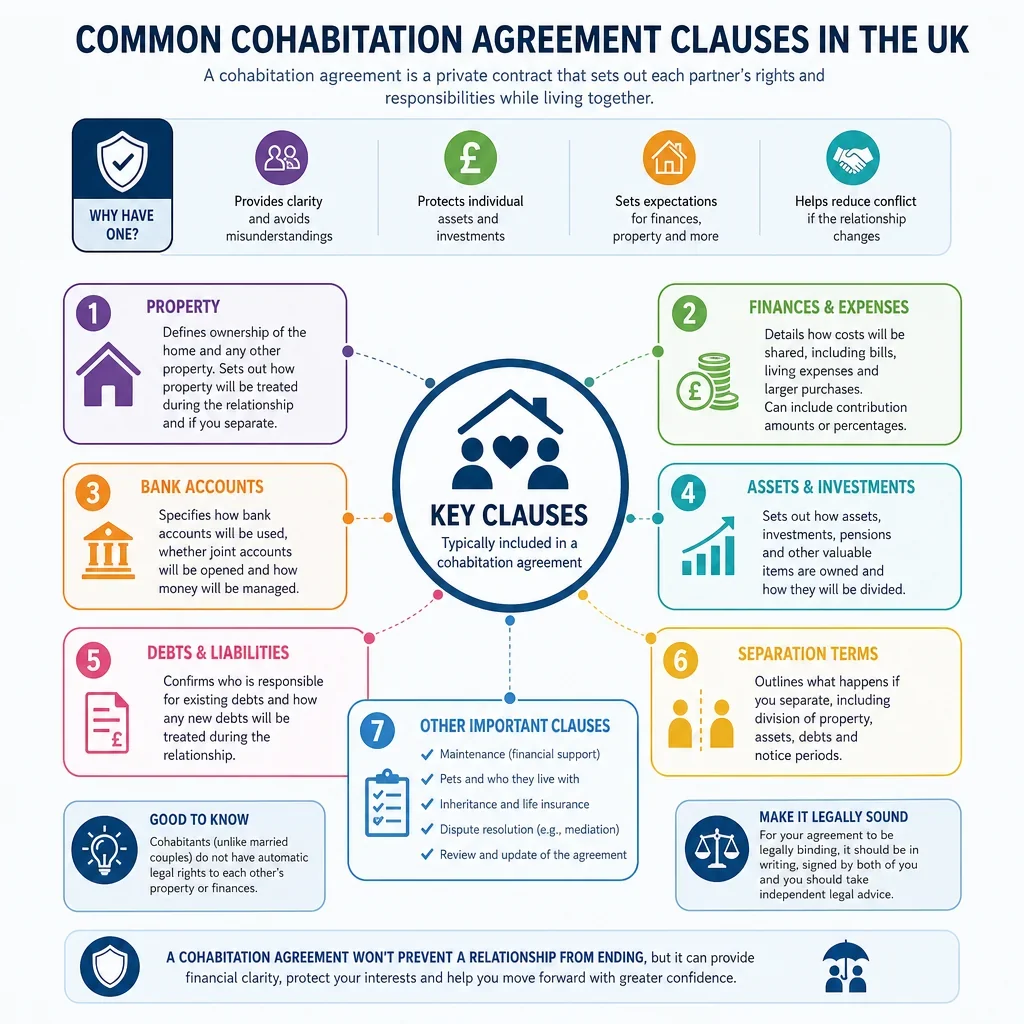

Explore common cohabitation agreement clauses in the UK, including property, finances, debts, and separation terms for unmarried couples.

UK guide to cohabitation living arrangements, agreement considerations, shared responsibilities, and legal planning for unmarried couples.

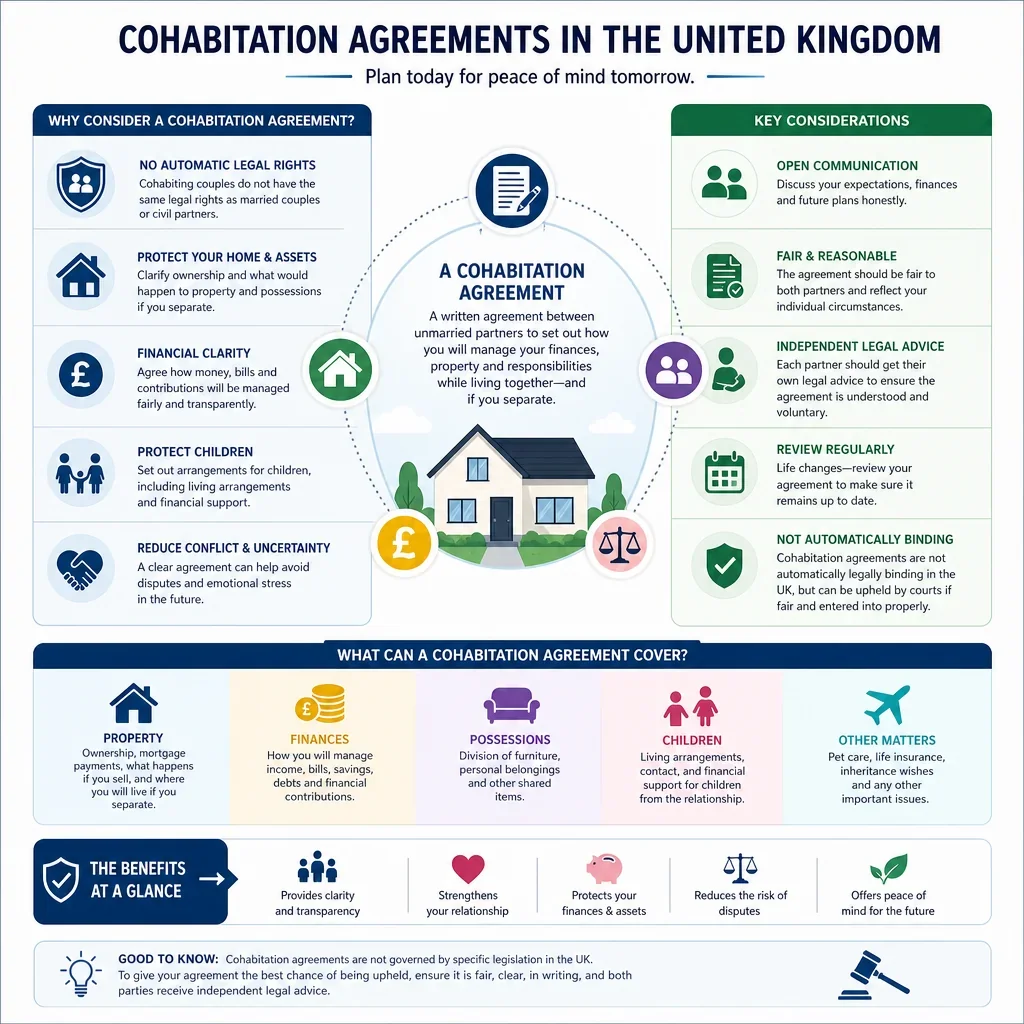

Need a cohabitation agreement in the United Kingdom? Learn when it helps protect property, finances, and rights for unmarried couples.

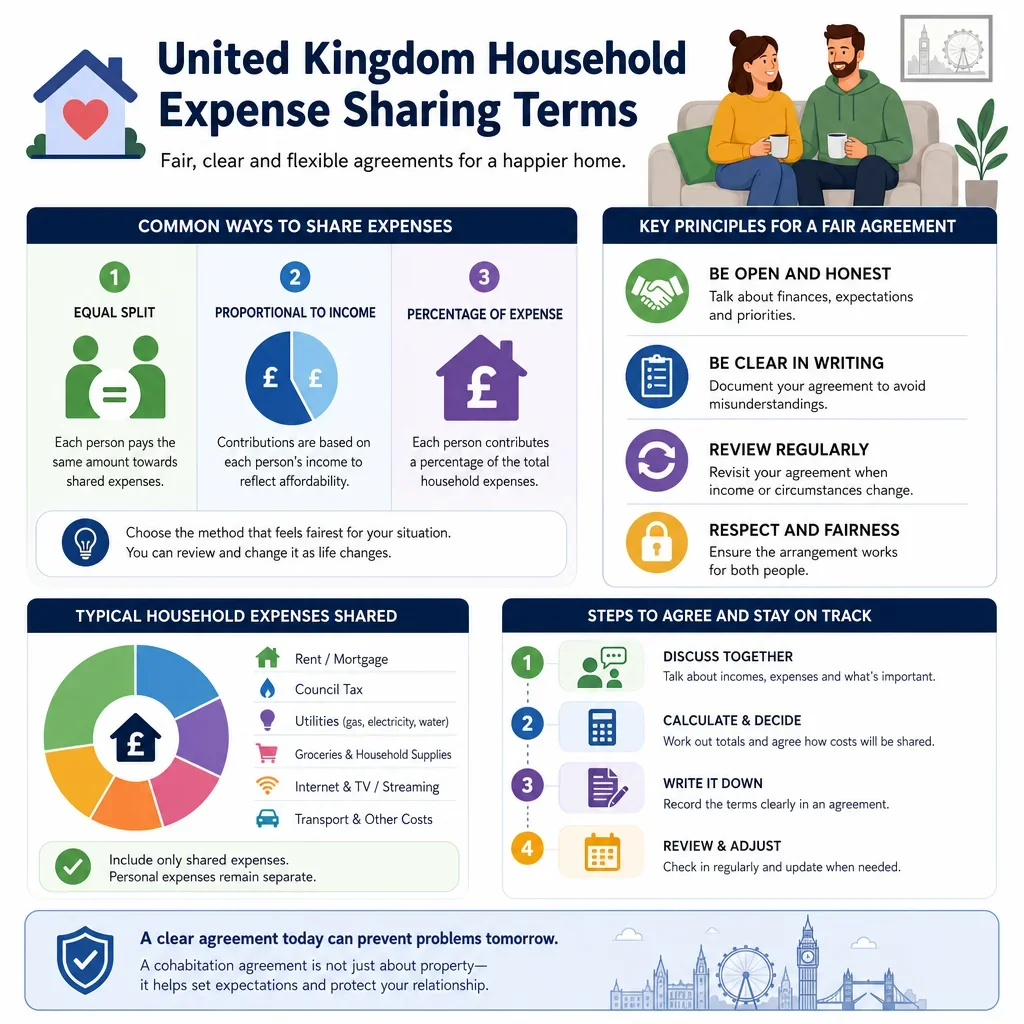

United Kingdom household expense sharing terms for cohabiting partners, covering bills, rent, utilities, and fair cost contributions.

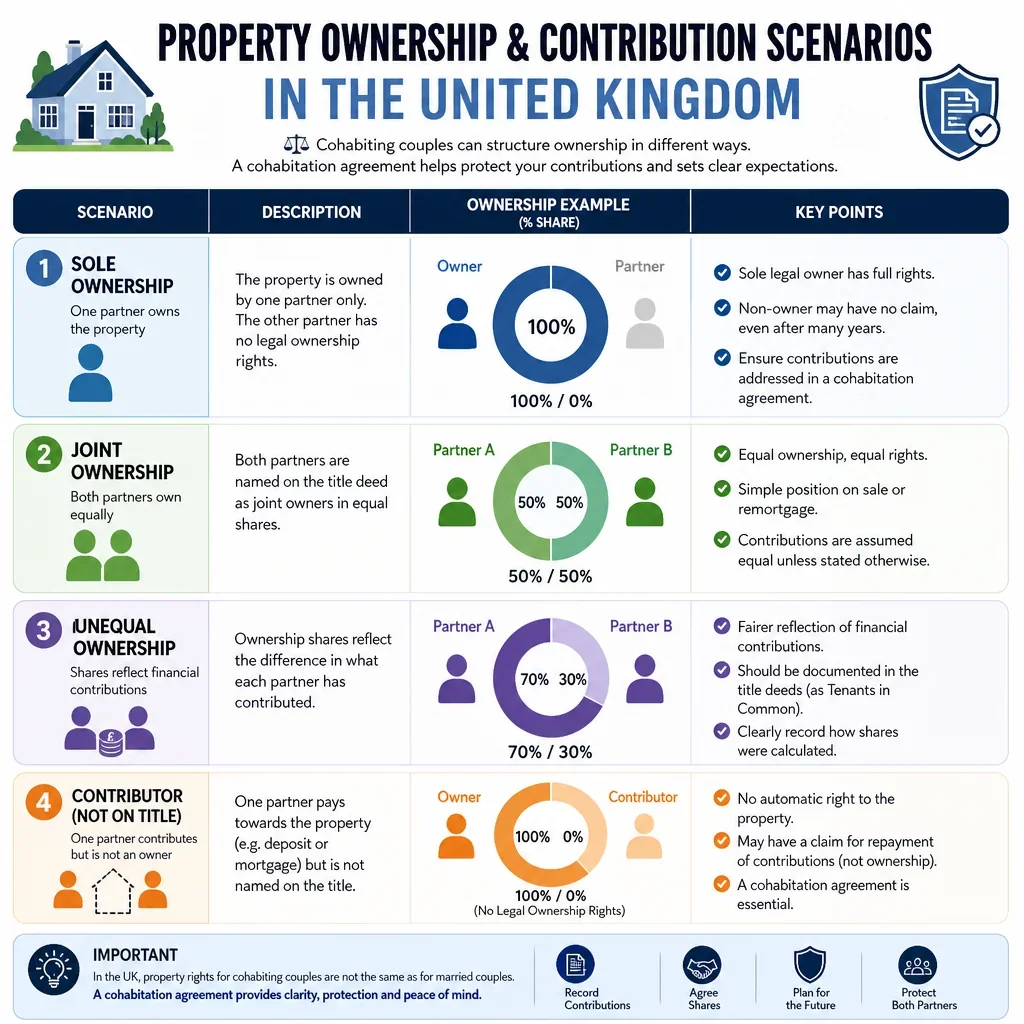

Explore UK property ownership and contribution scenarios for cohabiting partners, with clear insights for agreement planning.

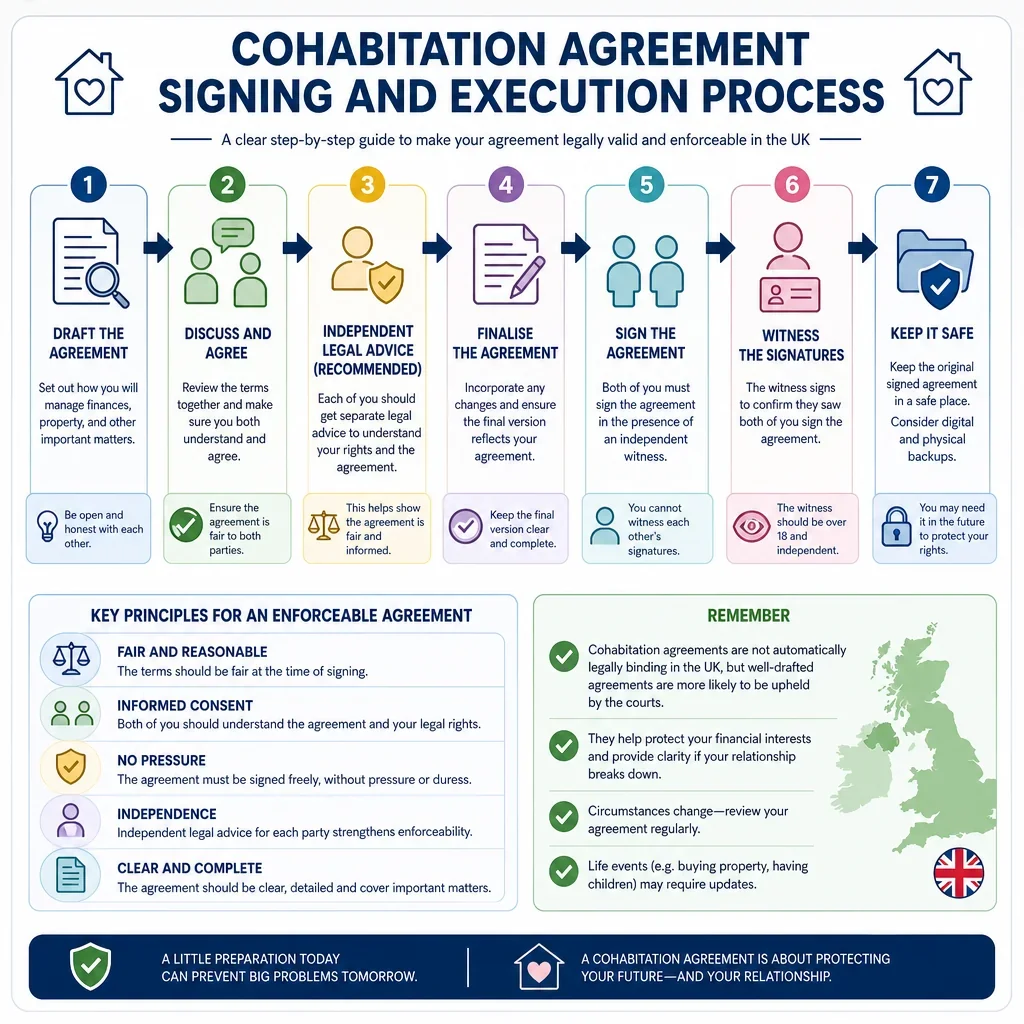

United Kingdom checklist for signing and executing a cohabitation agreement correctly, clearly, and confidently.

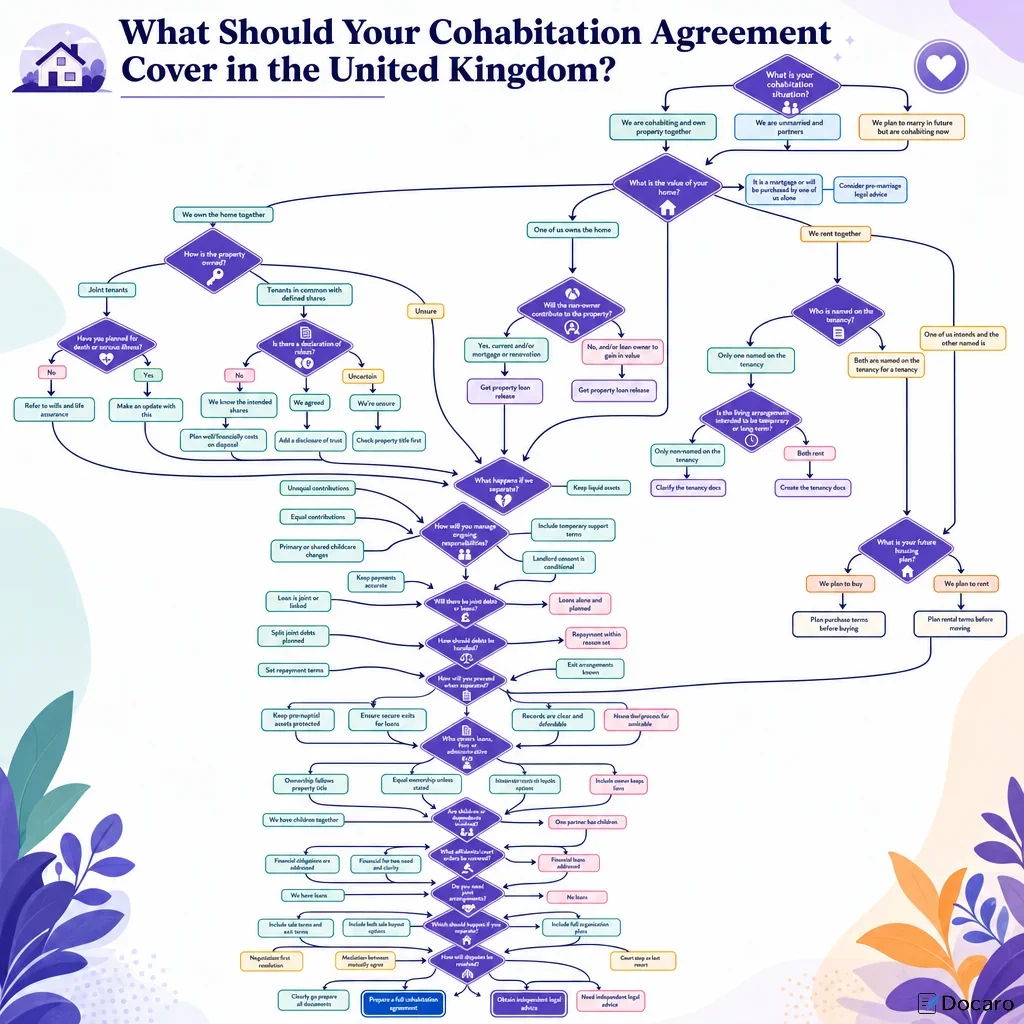

Learn what a cohabitation agreement should cover in the United Kingdom, from property and finances to separation planning.

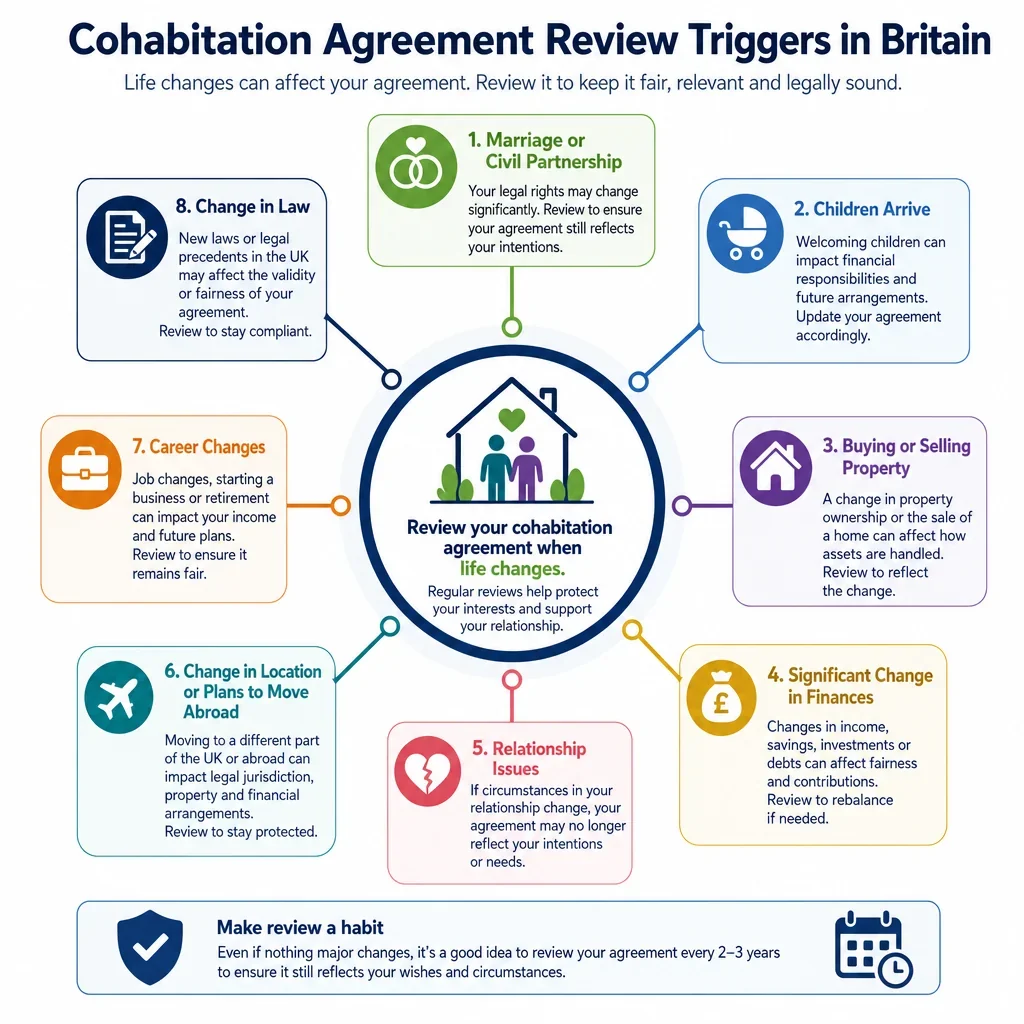

Key Britain cohabitation agreement review triggers to help couples know when legal updates may be needed.

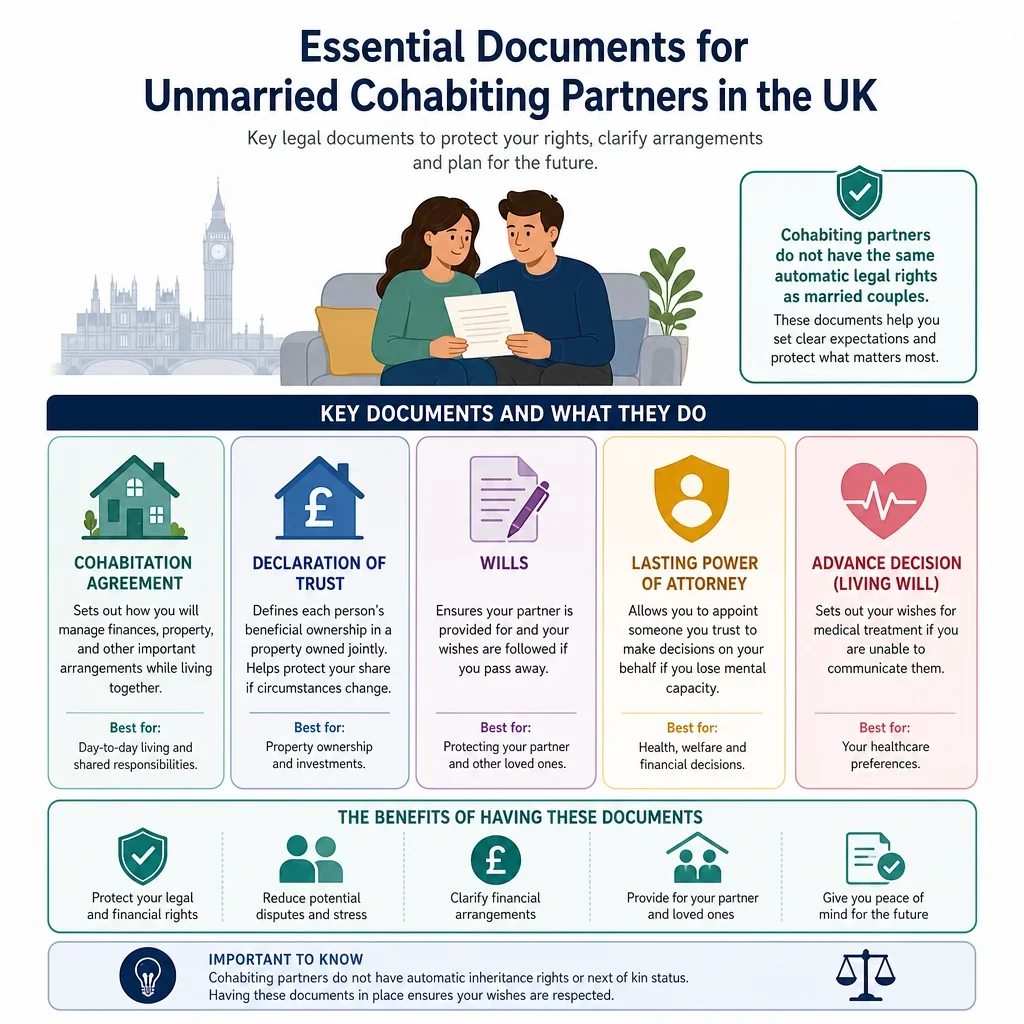

UK guide to related documents for unmarried cohabiting partners, including practical records that support living arrangements.

Key pre-drafting questions for cohabitation agreements in Britain, covering property, finances, and shared responsibilities.

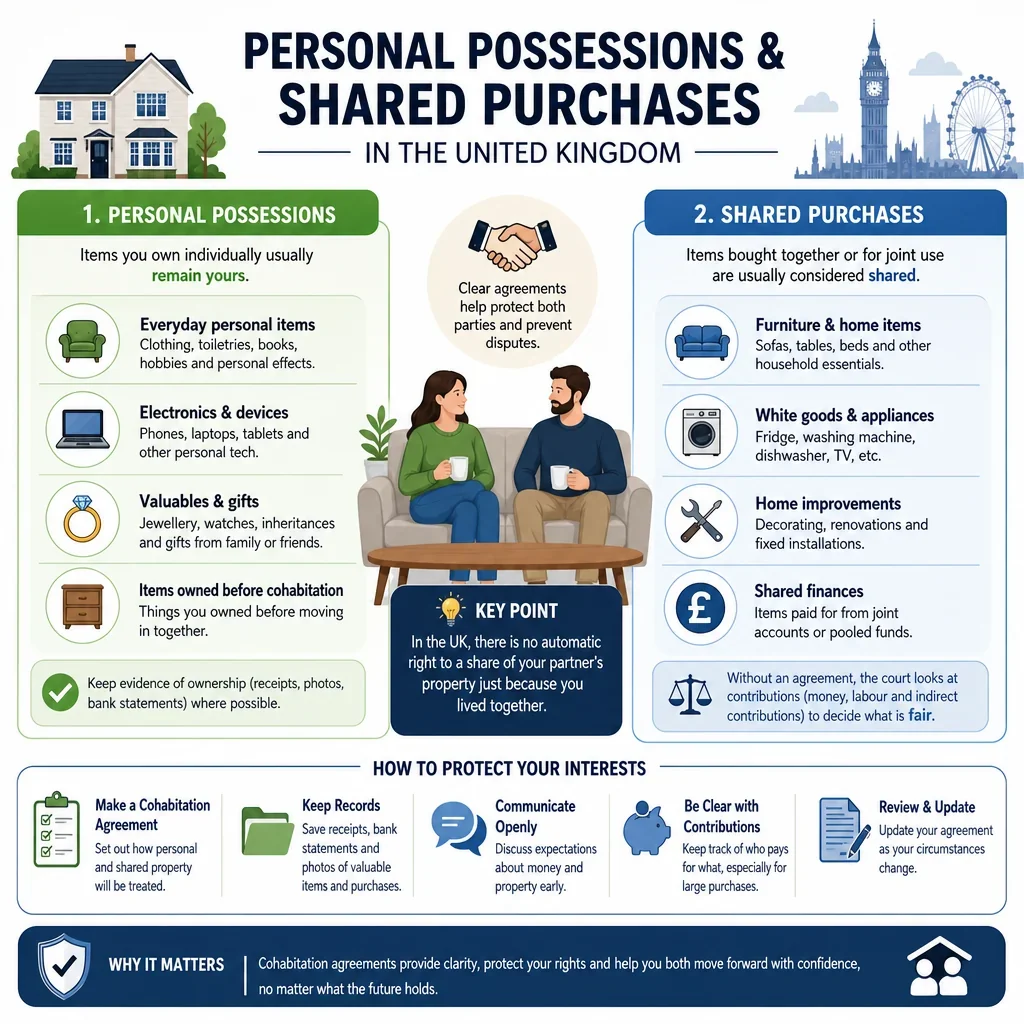

Understand personal possessions and shared purchases in the United Kingdom for clearer cohabitation planning and ownership records.

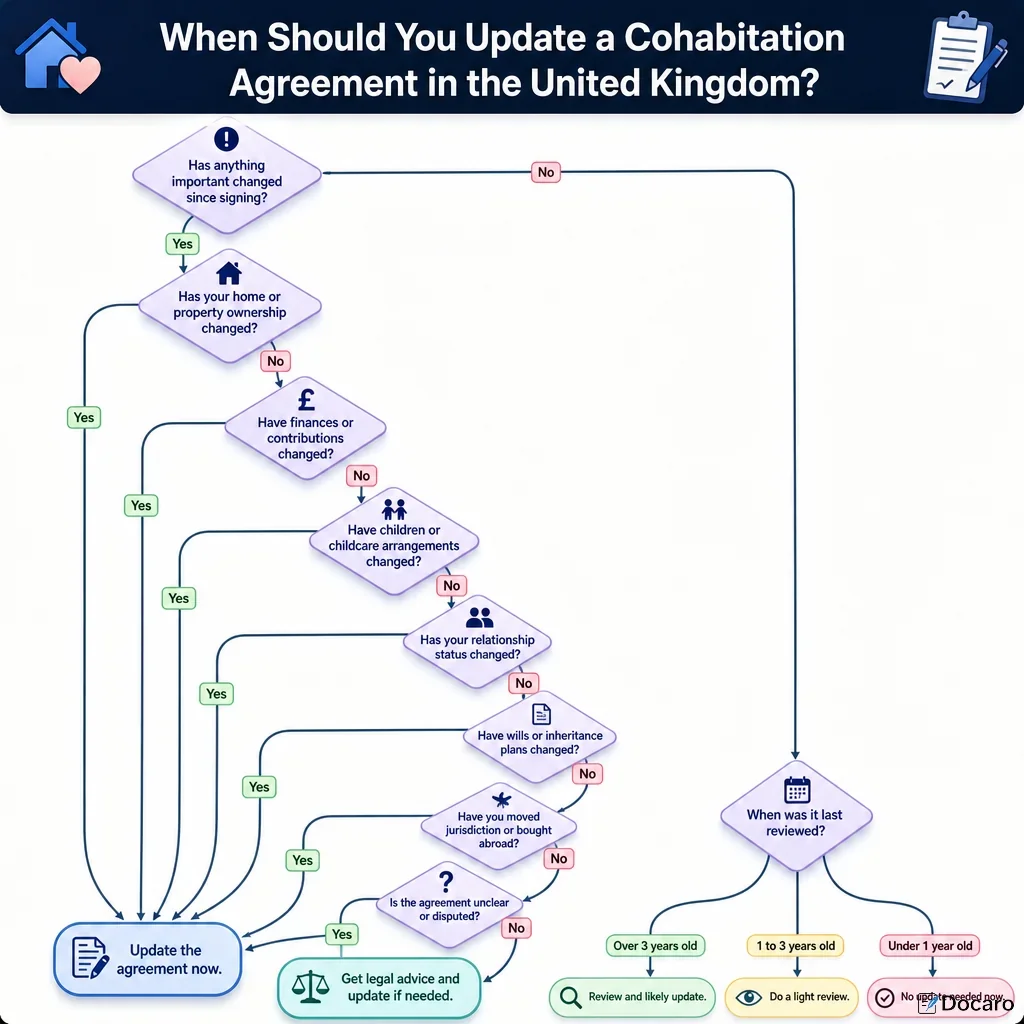

Learn when to update a cohabitation agreement in the United Kingdom after life, property, or financial changes.