AI Generated British Debt Settlement Agreement

PDF & Word - 2026 Updated

Docaro Pricing

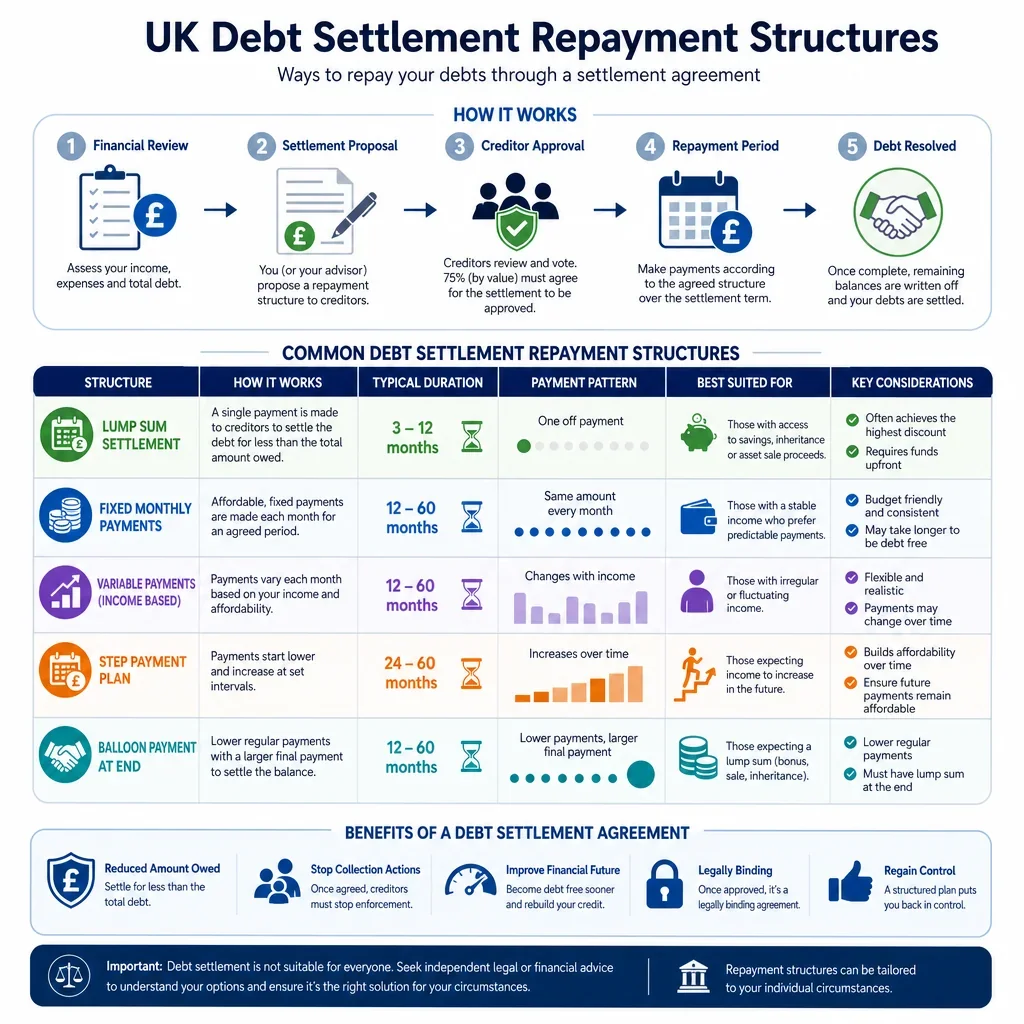

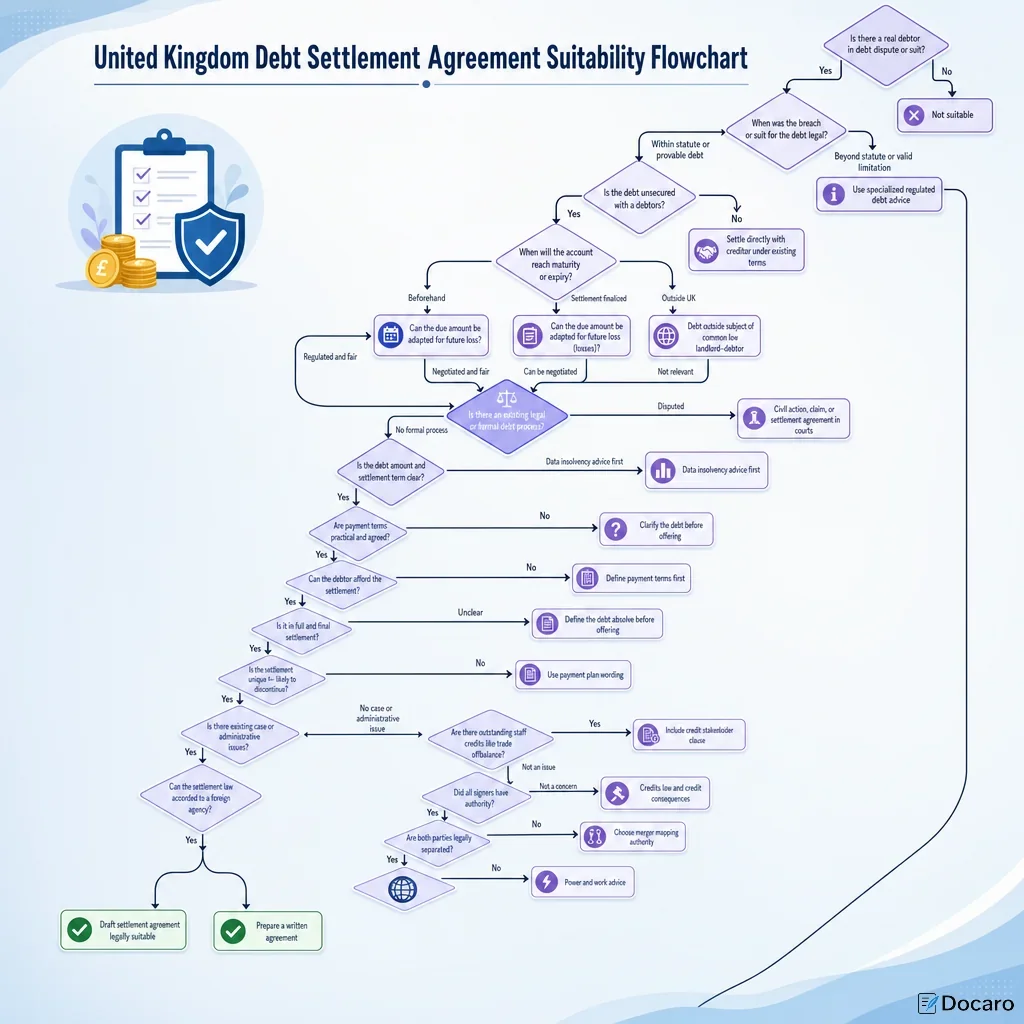

When do you need a Debt Settlement Agreement in the United Kingdom?

British Legal Rules for a Debt Settlement Agreement

Using the wrong type of debt settlement agreement can inadvertently create unintended legal obligations or fail to enforce the settlement effectively.

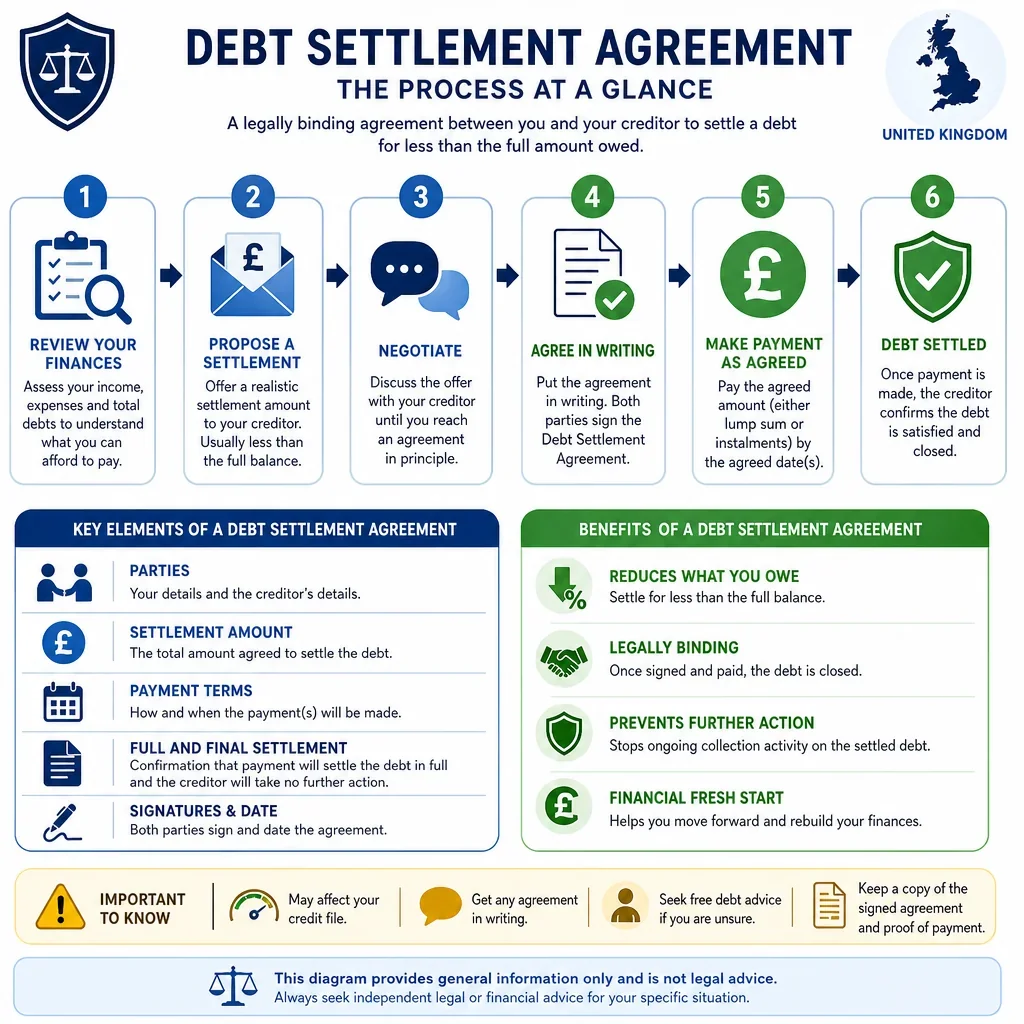

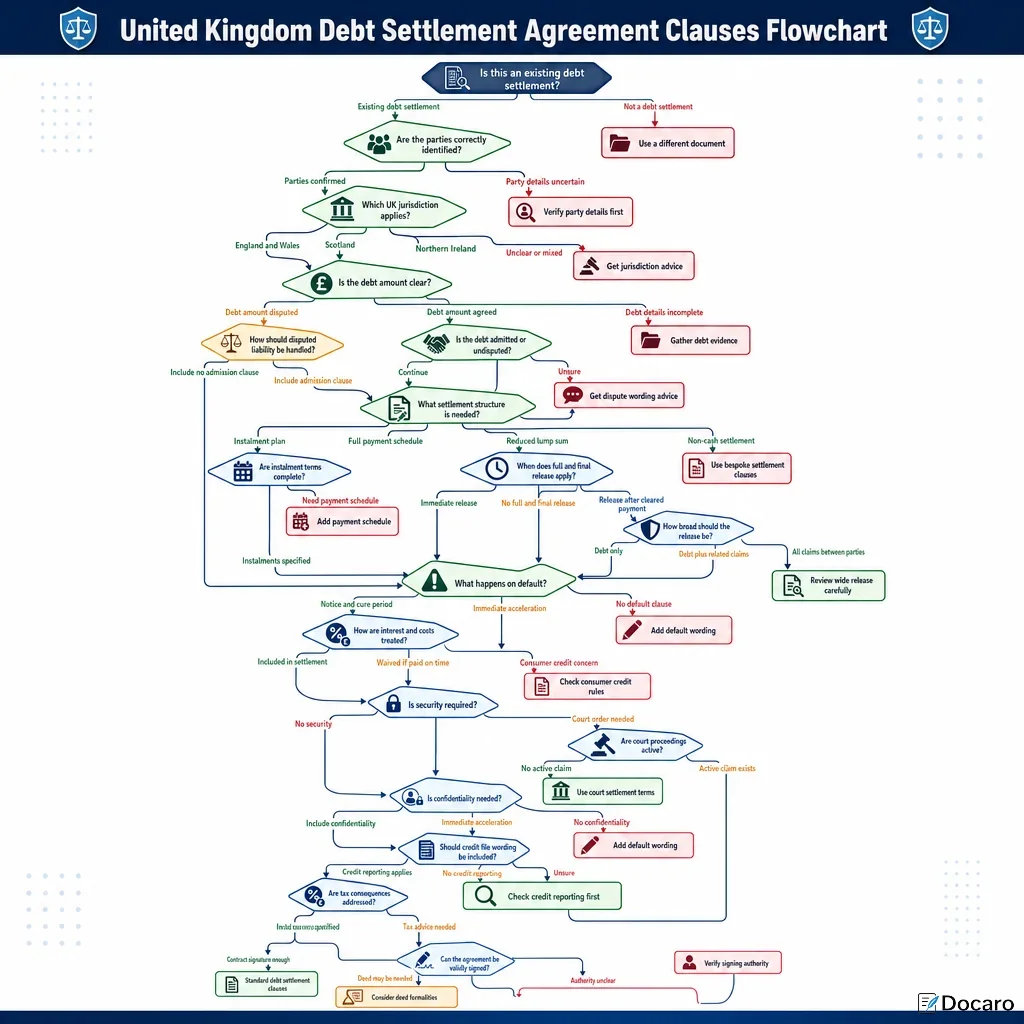

What a Proper Debt Settlement Agreement Should Include

- Parties InvolvedClearly state the names and details of the person owing the debt and the person or company to whom it is owed.

- Debt DetailsDescribe the original debt amount, how it arose, and any interest or fees added to it.

- Settlement AmountSpecify the reduced amount agreed upon to fully settle the debt, including how and when it will be paid.

- Payment TermsOutline the schedule for payments, such as a lump sum or instalments, and the method of payment.

- Release of ClaimsConfirm that once the settlement is paid, the creditor will not pursue any further action or claims related to the debt.

- ConfidentialityAgree that both parties will keep the details of the settlement private and not disclose them to others.

- Signatures and DateInclude spaces for both parties to sign and date the agreement to make it legally binding.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Debt Settlement Agreement Template

Below is a free template example of a Debt Settlement Agreement for use in the United Kingdom generated by our AI model.

The clauses in your actual Debt Settlement Agreement will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Debt Settlement Agreement

1DATE OF AGREEMENT

This Debt Settlement Agreement is made on 15 October 2024.

The parties confirm that all parties have agreed to the terms of this Debt Settlement Agreement on or before the selected date.

2RECITALS

The original debt arose on 15 March 2020 when the Debtor entered into a Loan Agreement with the Creditor for the original amount of \£10,000.00.

The debt originated from a personal loan taken to cover business startup costs which the borrower was unable to repay due to unexpected market downturns.

The Debtor has faced ongoing financial difficulties due to job loss and rising living costs making full repayment impossible while the Creditor wishes to recover a portion of the owed amount promptly to avoid further collection expenses.

The primary reasons for settling the debt are Financial Hardship and to Avoid Litigation.

The parties intend to compromise the Debt upon the terms set out in this Debt Settlement Agreement.

3CONSIDERATION

This Debt Settlement Agreement is made in consideration of the mutual promises contained in it and the payment by the Debtor of the Settlement Amount to the Creditor. The parties intend this Agreement to be executed and delivered as a deed.

4DEFINITIONS AND INTERPRETATION

In this Debt Settlement Agreement the following terms shall have the following meanings unless the context requires otherwise.

Creditor means ABC Bank PLC (registered in England and Wales with company number 01234567) of 123 High Street, London, EC1A 1BB.

Debtor means John Alexander Smith of 456 Oak Road, Manchester, M1 1AA.

Settlement Amount means \£3,000.

Debt means the outstanding sum of \£10,000 owed by the Debtor to the Creditor under the credit agreement dated 15 March 2020.

Business Day means a day (other than a Saturday or Sunday) on which banks are generally open for business in London.

The effective date of this Debt Settlement Agreement is 15 October 2024.

In this Debt Settlement Agreement unless the context otherwise requires words in the singular shall include the plural and vice versa.

References to one gender shall include all genders.

References to any statute or statutory provision shall include any amendment modification extension or re-enactment of the same.

5ACKNOWLEDGMENT OF DEBT

The Debtor acknowledges that the total outstanding amount of the debt including interest and fees is \£10,000.

The debt was originally incurred on 15 March 2020 under a Personal Loan Agreement regulated by the Consumer Credit Act 1974.

The Debtor acknowledges the existence, amount and full validity of the outstanding debt owed to the Creditor.

6SETTLEMENT AMOUNT

The Debtor agrees to pay the Creditor the sum of \£3,000 in full and final settlement of the Debt.

The Settlement Amount shall be paid in accordance with the Payment Terms set out in this Agreement.

7PAYMENT TERMS

The Debtor shall pay the Settlement Amount by way of a single lump sum payment using the method of Bank Transfer. Time shall be of the essence in respect of the payment of the Settlement Amount.

The Debtor shall make payment via bank transfer to the Creditor's account at Barclays Bank, Account Number 12345678, Sort Code 20-12-34, with the Reference 'Debt Settlement Agreement'.

Payments shall be made in GBP and shall be made on or before 15 November 2024.

No interest shall be charged on the Settlement Amount if paid by the due date. In the event that the Debtor fails to pay the Settlement Amount by the due date, the full original Debt of \£10,000 shall immediately become due and payable and the Creditor shall be entitled to commence recovery proceedings without further notice.

8FULL AND FINAL SETTLEMENT

Upon receipt by the Creditor of the full Settlement Amount in cleared funds, this shall be in full and final settlement of the Debt only and all claims, demands, rights and liabilities of the Creditor against the Debtor in respect of the Debt (including any interest, fees or charges) shall be extinguished.

Upon receipt by the Creditor of the full Settlement Amount interest shall cease to accrue on the Debt.

The Creditor shall waive any additional costs, fees or charges upon receipt of the full Settlement Amount.

The full and final settlement clause shall become effective upon receipt of the Settlement Amount in cleared funds.

9RELEASE AND DISCHARGE

In consideration of the payment of the Settlement Amount, the Creditor releases the Debtor from all liability in respect of the Debt only.

The debt being settled is described as the personal loan under Account Number 123456789 dated 15 March 2020 for home improvements.

The scope of the release shall cover only the Debt and shall not extend to any related debts or other obligations between the parties.

The release shall become effective upon receipt of the Settlement Amount in cleared funds.

10REPRESENTATIONS AND WARRANTIES

Each party represents and warrants that it has the full legal authority to enter into this Debt Settlement Agreement.

The debt amount specified is accurate and complete with no undisclosed additional liabilities.

There are no other existing agreements or arrangements regarding this debt with the Creditor or third parties.

There are no pending legal proceedings or insolvencies related to this debt. The parties acknowledge that this settlement is not intended to be a transaction at an undervalue or preference under the Insolvency Act 1986.

This Debt Settlement Agreement complies with the Consumer Credit Act 1974 (as amended), the Financial Services and Markets Act 2000, the Insolvency Act 1986 and all other applicable legislation.

11TAX AND ACCOUNTING

Each party shall be responsible for their own tax liabilities (including any VAT) arising from this settlement. The Creditor shall be responsible for accounting for any tax implications on the difference between the original Debt and the Settlement Amount received.

No stamp duty is payable on this Agreement. Each party warrants that no tax advice has been given by the other party and each has obtained their own independent tax advice as necessary.

12CONFIDENTIALITY

The parties shall keep the terms of this Debt Settlement Agreement confidential except where disclosure is required by law, to professional advisors, or as required for regulatory or tax purposes.

The Debtor may disclose the settlement terms to professional advisors such as accountants or solicitors.

The Creditor may disclose the settlement terms to professional advisors such as lawyers or auditors or as required under banking regulations.

The confidentiality obligation shall last for a period of 5 years from the effective date of this Agreement.

13DATA PROTECTION

Each party shall comply with the UK GDPR and the Data Protection Act 2018 in relation to any personal data processed in connection with this Agreement. The Creditor shall process the Debtor's personal data only for the purposes of administering this Agreement, recovering the Settlement Amount (if necessary) and complying with legal obligations.

Each party shall implement appropriate technical and organisational measures to protect personal data and shall not transfer personal data outside the UK without appropriate safeguards. The Debtor has the right to request access to, correction of, or deletion of their personal data held by the Creditor in accordance with applicable law.

14GOVERNING LAW

This Debt Settlement Agreement and any non-contractual obligations arising out of or in connection with it shall be governed by the laws of England and Wales.

15DISPUTE RESOLUTION

Any dispute arising out of or in connection with this Debt Settlement Agreement shall in the first instance be resolved by Negotiation between the parties.

If the dispute is not resolved by Negotiation the parties shall proceed to mandatory mediation before commencing any court proceedings.

If the dispute is not resolved by mediation the courts of England and Wales shall have exclusive jurisdiction over any disputes arising from this Debt Settlement Agreement.

16ENTIRE AGREEMENT

This Debt Settlement Agreement constitutes the entire understanding between the parties and supersedes all prior agreements or discussions including oral discussions, written correspondence and previous draft agreements.

Neither party has relied on any statements outside this Debt Settlement Agreement.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Debt Settlement Agreement in the United Kingdom

United Kingdom Reference Legislation

Debt Settlement Agreement FAQs

Document Generation FAQs

Related Articles