AI Generated Receipt for use in the United Kingdom

PDF & Word - 2026 Updated

Docaro Pricing

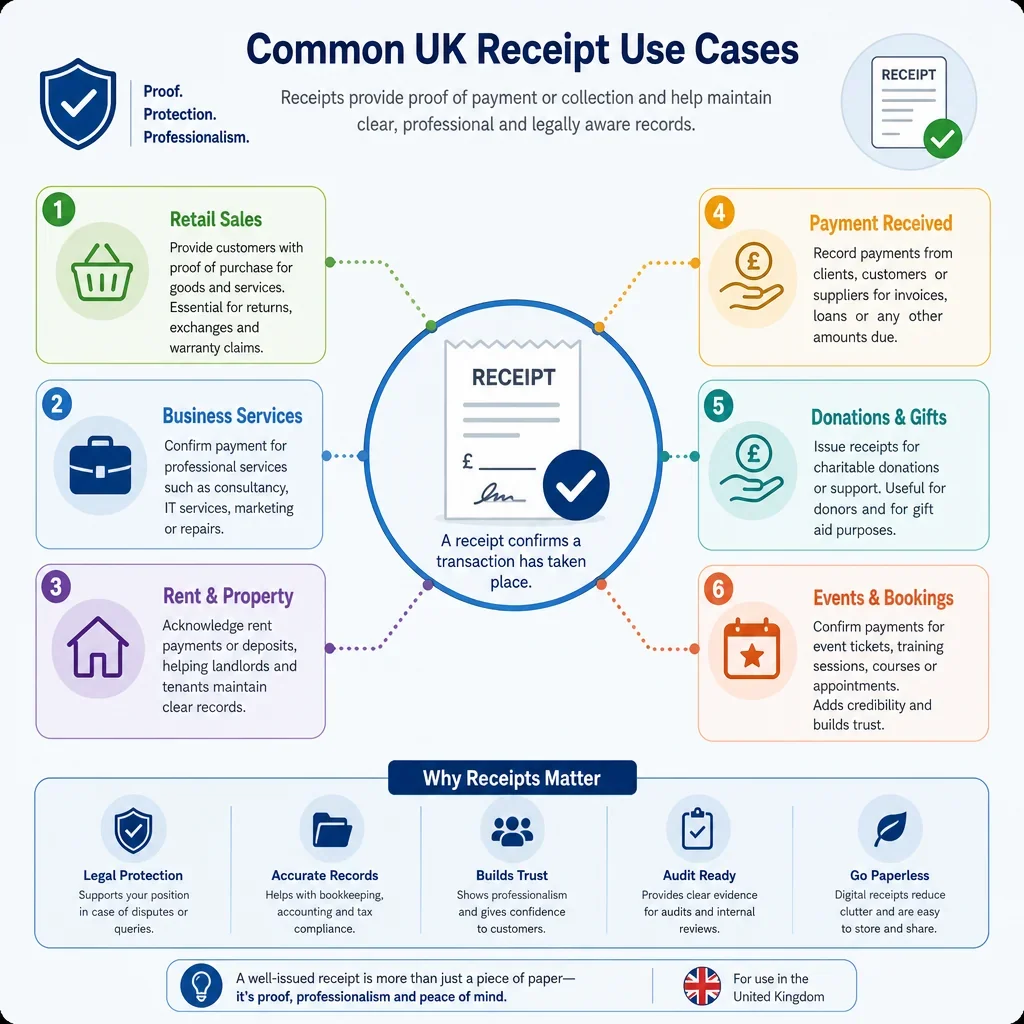

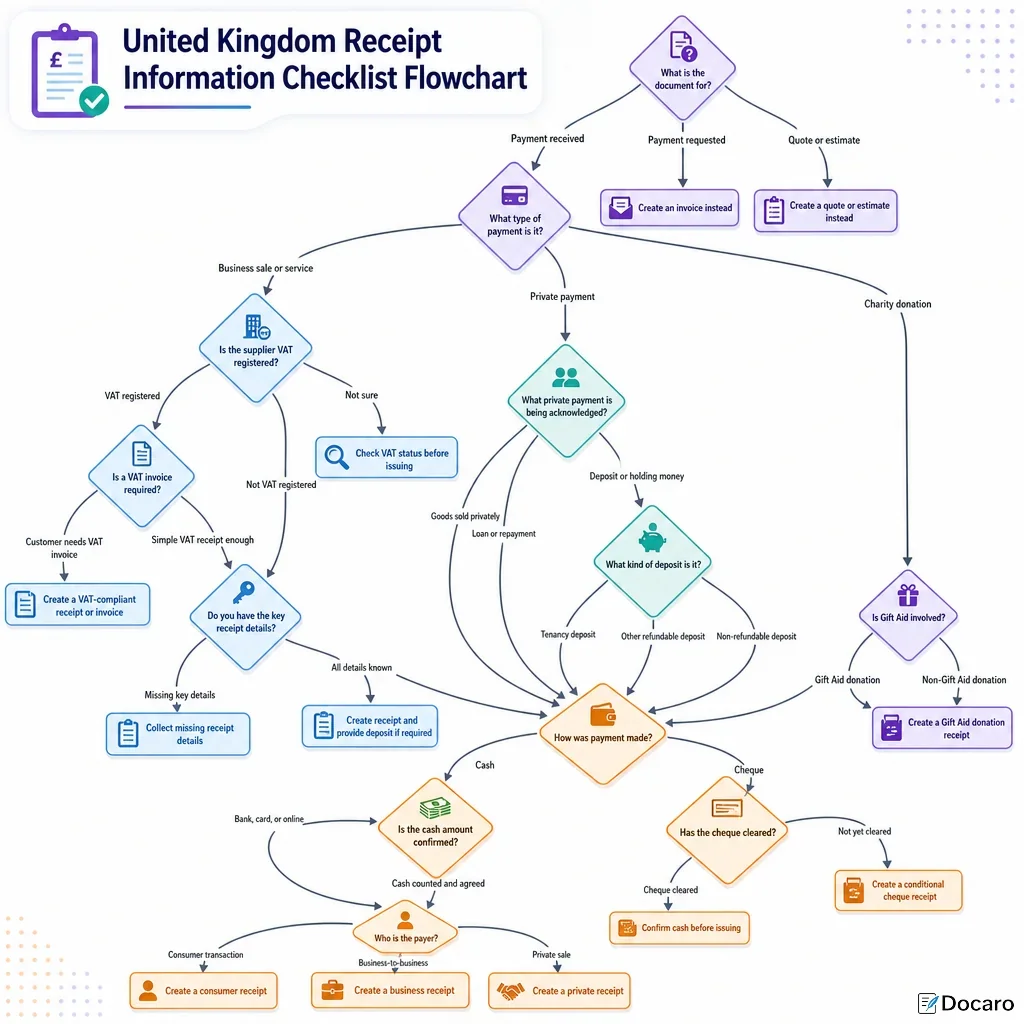

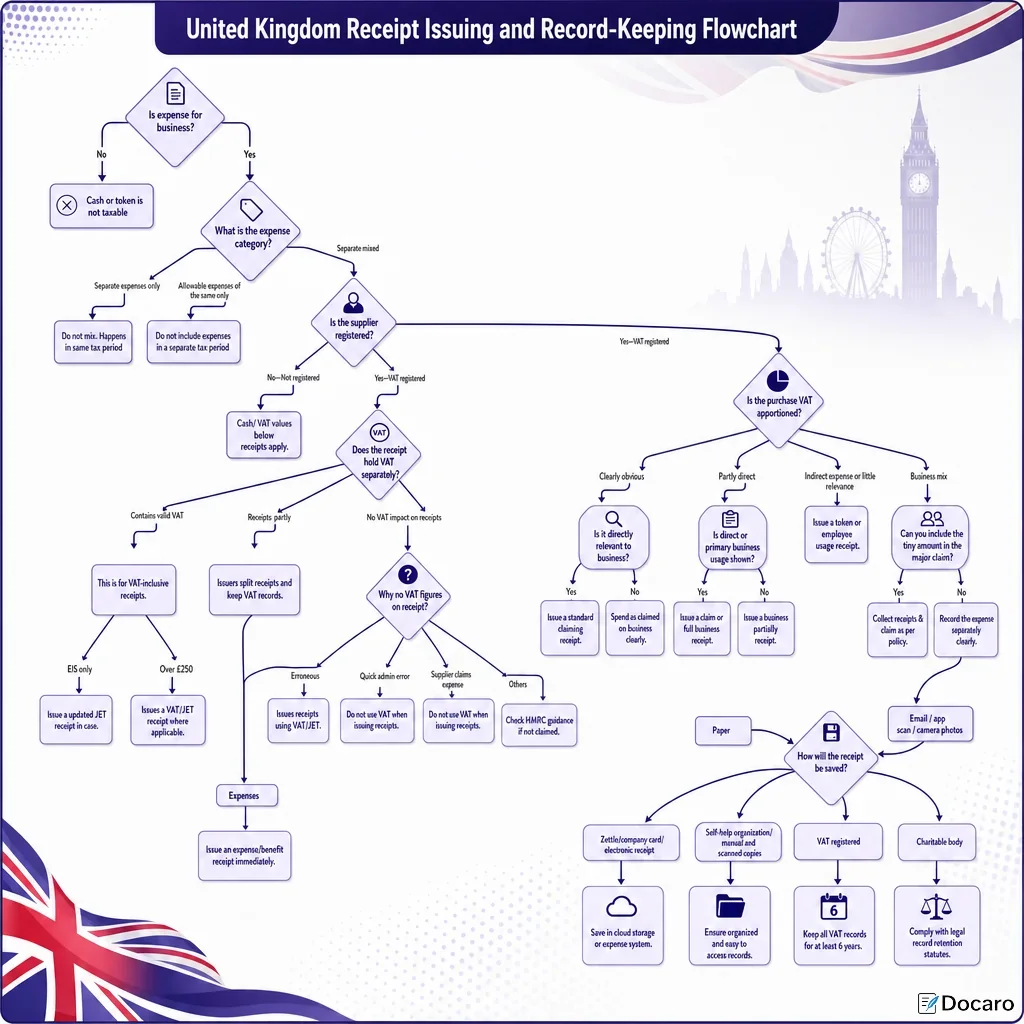

When do you need a Receipt in the United Kingdom?

British Legal Rules for a Receipt

Using the incorrect format for a receipt may fail to provide adequate proof of payment or comply with UK tax requirements.

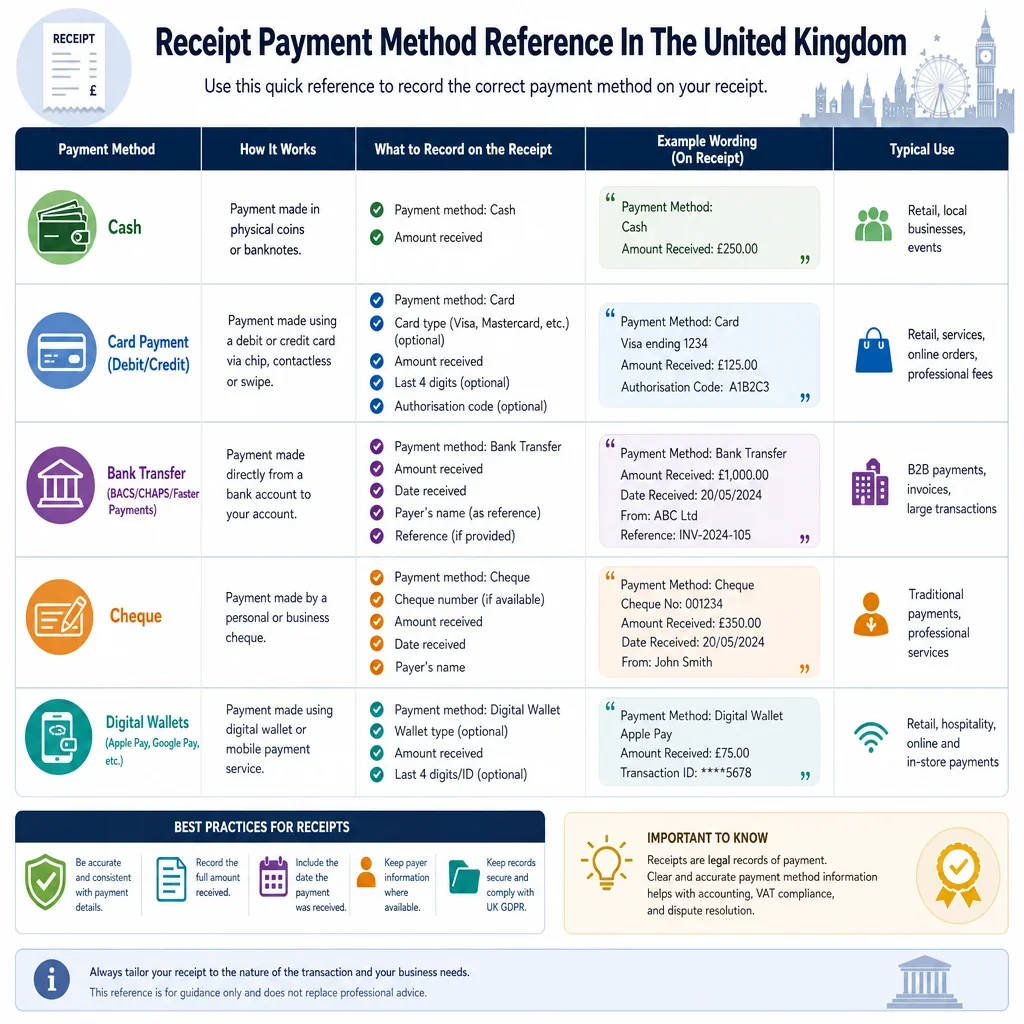

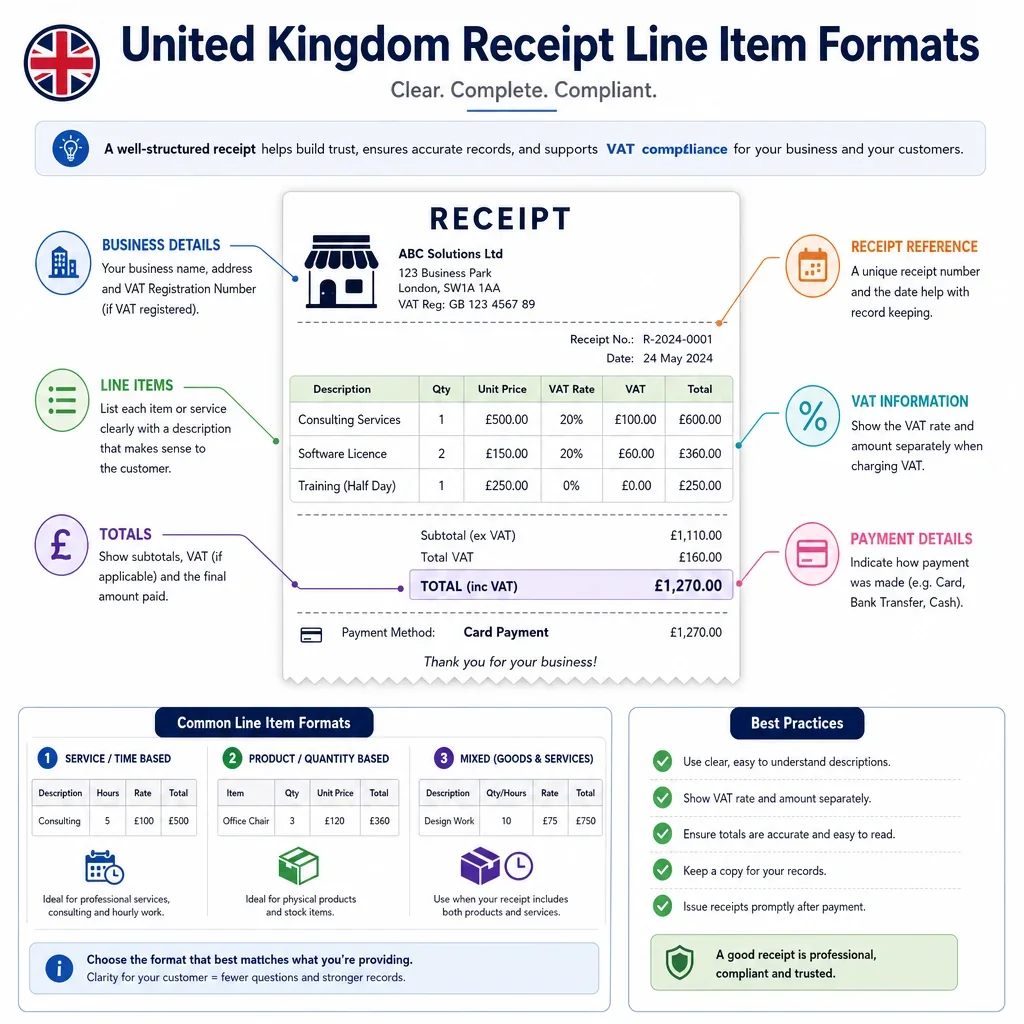

What a Proper Receipt Should Include

- Date of TransactionInclude the exact date when the payment or exchange took place to record when the transaction occurred.

- Details of Buyer and SellerList the full names and contact information of both the person paying and the person or business receiving the payment.

- Description of Goods or ServicesClearly describe what was bought or the service provided, including any relevant quantities or specifics.

- Amount PaidState the total amount paid, specifying the currency (e.g., GBP) and breaking it down if there are multiple items.

- Payment MethodNote how the payment was made, such as cash, card, bank transfer, or cheque.

- Unique Receipt NumberAssign a unique reference number to the receipt for easy tracking and record-keeping.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Receipt Template

Below is a free template example of a Receipt for use in the United Kingdom generated by our AI model.

The clauses in your actual Receipt will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

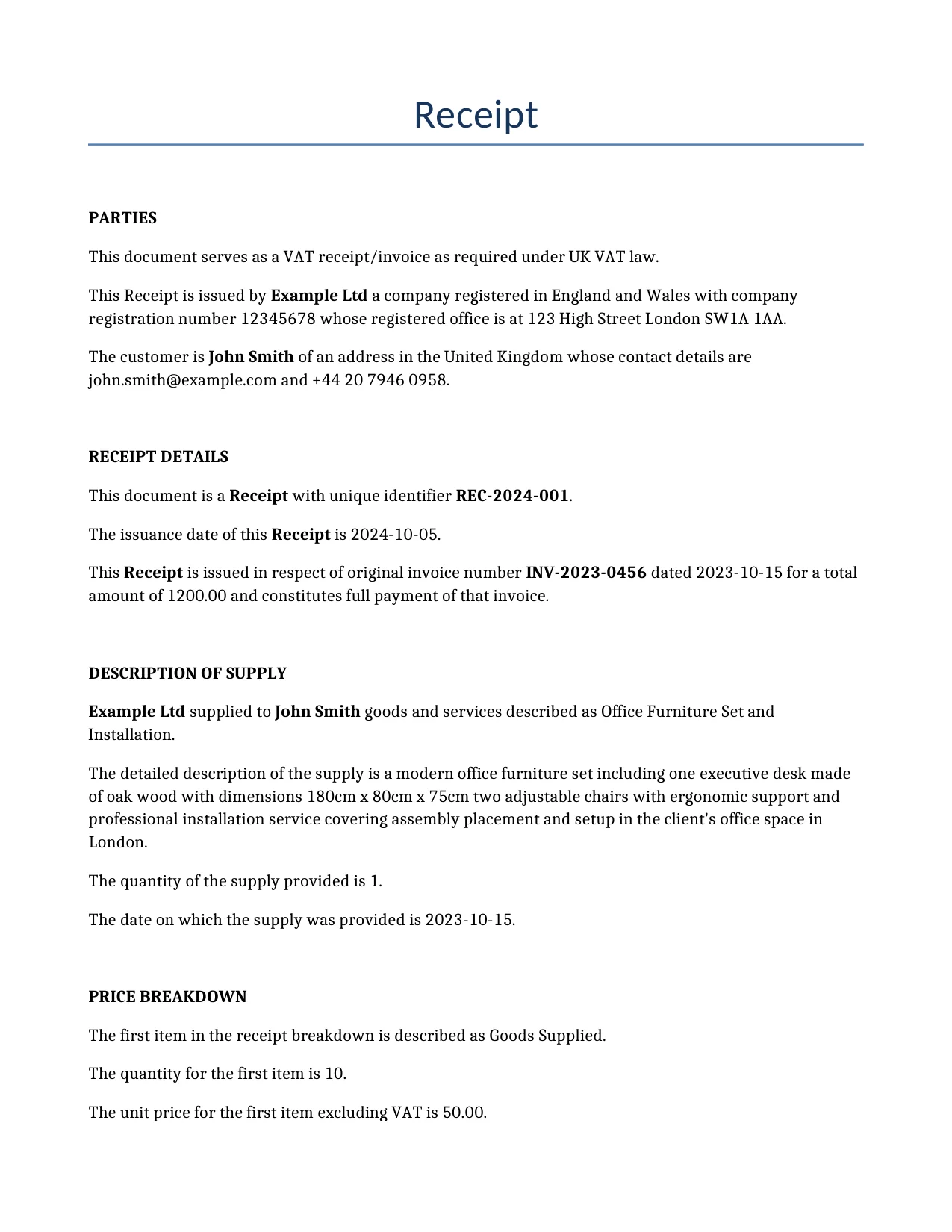

Receipt

PARTIES

This document serves as a VAT receipt/invoice as required under UK VAT law.

This Receipt is issued by Example Ltd a company registered in England and Wales with company registration number 12345678 whose registered office is at 123 High Street London SW1A 1AA.

The customer is John Smith of an address in the United Kingdom whose contact details are john.smith@example.com and +44 20 7946 0958.

RECEIPT DETAILS

This document is a Receipt with unique identifier REC-2024-001.

The issuance date of this Receipt is 2024-10-05.

This Receipt is issued in respect of original invoice number INV-2023-0456 dated 2023-10-15 for a total amount of 1200.00 and constitutes full payment of that invoice.

DESCRIPTION OF SUPPLY

Example Ltd supplied to John Smith goods and services described as Office Furniture Set and Installation.

The detailed description of the supply is a modern office furniture set including one executive desk made of oak wood with dimensions 180cm x 80cm x 75cm two adjustable chairs with ergonomic support and professional installation service covering assembly placement and setup in the client's office space in London.

The quantity of the supply provided is 1.

The date on which the supply was provided is 2023-10-15.

PRICE BREAKDOWN

The first item in the receipt breakdown is described as Goods Supplied.

The quantity for the first item is 10.

The unit price for the first item excluding VAT is 50.00.

The subtotal for the first item including VAT is 600.00.

The second item in the receipt breakdown is described as Installation Service.

The quantity for the second item is 1.

The unit price for the second item excluding VAT is 500.00.

The subtotal for the second item including VAT is 600.00.

The overall subtotal before any final taxes or adjustments is 1000.00.

A discount was applied to the total amount paid of 50.00.

No adjustment was applied to the total amount paid.

The grand total amount due on this Receipt is 1200.00.

TAX BREAKDOWN

The VAT rate applied is 20%.

The VAT amount for the goods is 100.00 GBP.

The VAT amount for the installation service is 100.00 GBP.

The total VAT is 200.00 GBP.

VALUE ADDED TAX

This Receipt is issued in compliance with the Value Added Tax Act 1994 and the Value Added Tax Regulations 1995.

The total VAT amount for the entire receipt is 200.00 GBP.

A single VAT rate of 20.00 percent was applied to the main supply.

The net amount of the supply before VAT is applied is 1000.00 GBP.

The total VAT amount due on the supply is 200.00 GBP.

The total amount including VAT is 1200.00 GBP.

No part of the supply qualifies for a reduced VAT rate.

No part of the supply qualifies as zero-rated for VAT.

The entire supply is not exempt from VAT.

The date of the receipt for VAT purposes is 2023-10-15.

The VAT registration number of Example Ltd is GB123456789.

PAYMENT

Payment was made by bank transfer.

The sort code for the bank account that received the payment is 12-34-56.

The account number for the bank account that received the payment is 12345678.

The name of the bank that holds the account for the payment is Barclays Bank.

The reference number for the payment is PAY-UK-2023-04567.

The transaction reference number for the payment is TRN-789012345.

The payment was made on 2023-10-15.

The total amount was paid on 2023-10-15.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Receipt in the United Kingdom

United Kingdom Reference Legislation

Receipt FAQs

Document Generation FAQs

Related Articles