AI Generated British Loan Agreement

PDF & Word - 2026 Updated

Docaro Pricing

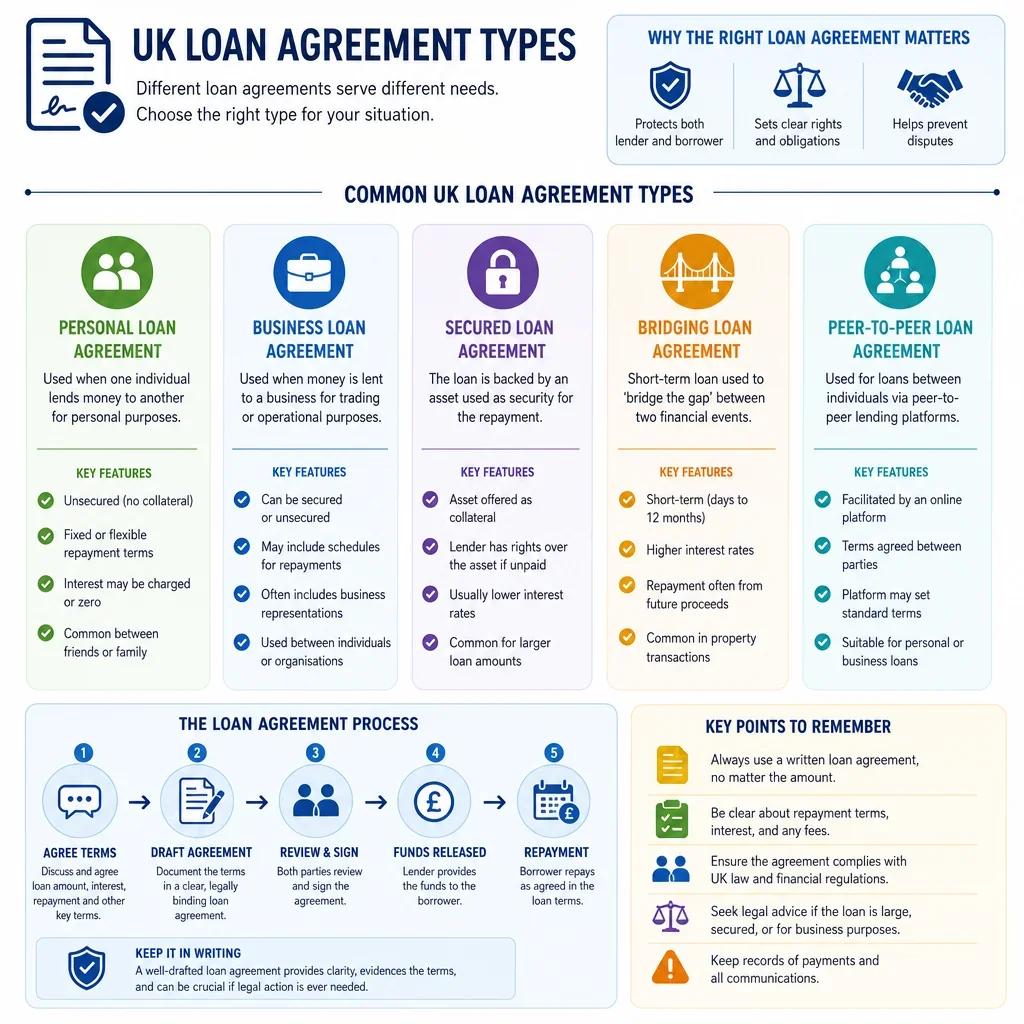

When do you need a Loan Agreement in the United Kingdom?

British Legal Rules for a Loan Agreement

Using the wrong type of loan agreement can result in unenforceable terms or unintended legal liabilities.

What a Proper Loan Agreement Should Include

- Parties InvolvedClearly identify the lender and borrower, including their full names and addresses, to establish who is entering the agreement.

- Loan AmountState the exact amount of money being lent to avoid any confusion about the principal sum.

- Repayment TermsSpecify how and when the loan must be repaid, such as the schedule of payments and method of transfer.

- Interest RateDetail any interest charged on the loan, including the rate and how it is calculated.

- Default ConsequencesOutline what happens if payments are missed, like additional fees or actions the lender can take.

- Security or CollateralIf applicable, describe any assets pledged as security for the loan to protect the lender.

- SignaturesInclude spaces for both parties to sign and date the agreement to make it legally binding.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United Kingdom

United KingdomFree Example Loan Agreement Template

Below is a free template example of a Loan Agreement for use in the United Kingdom generated by our AI model.

The clauses in your actual Loan Agreement will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Loan Agreement between ABC Lender and XYZ Borrower

1DEFINITIONS AND INTERPRETATION

In this Agreement the following terms shall have the following meanings unless the context requires otherwise.

Loan Amount means the total sum advanced by the Lender to the Borrower under this Agreement being \£50,000.

Interest Rate means the annual percentage rate applied to the outstanding principal balance of the loan which shall be 5.5 percent per annum.

Repayment Date means the same day of each month as the First Repayment Date or if that day does not exist in a month the last day of that month.

Business Day means a day other than a Saturday Sunday or public holiday in England and Wales on which banks are open for general business in London.

Default Event means any of the events described in clause 11 of this Agreement.

This Agreement is made on 2024-01-15 and shall come into force on that date.

In this Agreement references to clauses and schedules are to clauses and schedules of this Agreement.

The headings in this Agreement are for ease of reference only and shall not affect its construction.

Material Adverse Change means any material adverse change in the business assets condition (financial or otherwise) operations or prospects of the Borrower which in the reasonable opinion of the Lender is likely to have a material adverse effect on the ability of the Borrower to perform or comply with any of its obligations under this Agreement or any Security Document.

EBITDA means earnings before interest taxes depreciation and amortisation calculated in accordance with UK GAAP or IFRS (as applicable).

Guarantor means any person who provides a guarantee in respect of the obligations of the Borrower under this Agreement.

Security Documents means the Debenture the legal charge over the residential property and any other document creating or evidencing security in favour of the Lender from time to time.

Insolvency Event means in relation to the Borrower or any Guarantor any circumstance where it is unable to pay its debts within the meaning of section 123 of the Insolvency Act 1986 or it enters into administration bankruptcy liquidation or any analogous proceedings under the laws of England and Wales or any other jurisdiction.

2LOAN FACILITY

Subject to the terms and conditions of this Agreement the Lender grants to the Borrower a term loan facility of \£50,000 (the Loan).

The Loan shall be available to the Borrower in a single advance on the date of this Agreement subject to the satisfaction of all conditions precedent set out in clause 13.

The Borrower shall deliver a drawdown notice to the Lender not less than 3 Business Days prior to the proposed drawdown date (or such shorter period as the Lender may agree) specifying the amount (which shall not exceed the Loan) and the proposed drawdown date (which must be a Business Day).

The Lender shall have no obligation to advance the Loan if any representation or warranty under this Agreement is untrue or if any Default Event is continuing or would result from the advance.

3INTEREST AND FEES

Interest shall accrue on the outstanding principal balance of the Loan at the Interest Rate and shall be calculated on a daily basis by reference to the actual number of days elapsed and a 365-day year.

Interest shall be calculated from the date of this Agreement and shall be payable monthly in arrears on each Repayment Date.

If the Borrower fails to pay any sum due under this Agreement on the due date the Borrower shall pay default interest on the overdue amount at the rate of 10 percent per annum above the Interest Rate both before and after judgment.

Default interest shall be payable on demand by the Lender and shall accrue from day to day on the basis of the actual number of days elapsed and a year of 365 days and shall be compounded monthly.

The interest rate and default interest rate under this Agreement shall not exceed the maximum rate permitted under applicable UK law including the Consumer Credit Act 1974 (if this Agreement is a regulated agreement) and nothing in this Agreement shall require the payment of interest at a rate which would constitute a criminal rate under the Criminal Code or otherwise contravene applicable usury laws.

4REPAYMENT TERMS

The Borrower shall repay the Loan together with all accrued interest by way of monthly instalments in accordance with the repayment schedule set out in Schedule 1 (Repayment Schedule).

The first repayment (the First Repayment Date) shall be made on 2024-03-01 and there shall be 24 monthly instalments in total.

If any Repayment Date falls on a day that is not a Business Day the payment shall be made on the next succeeding Business Day (unless that Business Day falls in the next calendar month in which event the payment shall be made on the immediately preceding Business Day).

All payments made by the Borrower under this Agreement shall be applied first in payment of any default interest then in payment of any fees or expenses then in payment of accrued interest and finally in reduction of the outstanding principal.

If the calculations in the repayment schedule do not result in the Loan being fully amortised by the final Repayment Date the Borrower shall pay a final balloon payment of all remaining principal interest and other sums due on the final Repayment Date.

The Borrower may terminate this Agreement early by giving not less than 14 days prior written notice to the Lender and paying all outstanding principal accrued interest default interest (if any) and all other sums due under this Agreement on the date of early termination.

5PREPAYMENT

The Borrower may make prepayments of the whole or any part of the Loan provided that the Borrower gives the Lender not less than 14 days prior written notice of its intention to make such prepayment.

There shall be no restrictions on the frequency with which the Borrower may make prepayments and no penalty shall be payable in respect of any prepayment.

Any prepayment shall be applied first to accrued interest and then to the outstanding principal and shall be made together with all interest accrued on the amount prepaid up to the date of prepayment.

6REPRESENTATIONS AND WARRANTIES - BORROWER

The Borrower represents and warrants to the Lender that the Borrower is duly incorporated and validly existing under the laws of England and Wales.

The Borrower is in good standing with all relevant regulatory authorities in the United Kingdom.

The Borrower has the full corporate power and authority to enter into and perform its obligations under this Agreement.

The entering into of this Agreement will not conflict with any applicable laws or regulations in the United Kingdom.

The entering into of this Agreement will not breach any existing contracts or agreements to which the Borrower is a party.

The Borrower has obtained all necessary approvals licenses and consents required under UK law to enter into this Agreement.

The most recent financial statements of the Borrower dated 2023-12-31 are true complete and fairly representative of its financial condition in accordance with UK GAAP or IFRS.

There has been no Material Adverse Change in the financial condition of the Borrower since the date of the latest financial statements.

The Borrower has no material contingent liabilities not disclosed in the latest financial statements.

The Borrower is not involved in any pending or threatened litigation arbitration or administrative proceedings in the United Kingdom which could reasonably be expected to have a Material Adverse Change.

The Borrower has full legal and beneficial title to all its assets free from any undisclosed security interests.

The Borrower is not in default under any other loan or financing agreements.

The total amount of indebtedness of the Borrower to third parties does not exceed \£150,000.

There are no security interests or encumbrances over the Borrower's assets other than those disclosed to the Lender prior to the date of this Agreement.

The Borrower is fully compliant with all UK tax obligations including corporation tax and VAT.

The Borrower is in compliance with all applicable UK environmental laws and regulations.

The Borrower complies with all UK employment laws regarding its workforce.

The Borrower has met all obligations under UK pension schemes.

The Borrower has never been subject to insolvency proceedings or administration in the United Kingdom.

Each of the representations and warranties set out in this clause 6 is repeated on each day during the term of this Agreement with reference to the facts and circumstances then subsisting as if made on each such day.

7REPRESENTATIONS AND WARRANTIES - LENDER

The Lender represents and warrants to the Borrower that it has the full power and authority to enter into lend under and perform its obligations under this Agreement in accordance with English law.

The Lender has taken all necessary corporate or other action to authorise the execution delivery and performance of this Agreement.

The Lender is not subject to any legal or regulatory restriction under UK law which would prevent it from entering into this Agreement or advancing the Loan.

The Lender is a UK resident for tax purposes.

8COVENANTS

Positive Covenants: The Borrower shall (a) maintain its corporate existence and good standing under the laws of England and Wales; (b) comply with all applicable laws and regulations including without limitation the Consumer Credit Act 1974 (if applicable) the Financial Services and Markets Act 2000 and all tax environmental employment and pension laws; (c) maintain adequate insurance over its assets and business with reputable insurers and on terms satisfactory to the Lender; (d) promptly notify the Lender of any Default Event or any event or circumstance which may reasonably be expected to give rise to a Default Event; and (e) provide such financial and other information as the Lender may reasonably require from time to time.

Negative Covenants: The Borrower shall not without the prior written consent of the Lender (a) incur any additional borrowings or indebtedness; (b) dispose of any material assets; (c) pay any dividends or make any distributions to its shareholders; or (d) create or permit to subsist any security over its assets other than in favour of the Lender (negative pledge).

Financial Covenants: The Borrower shall maintain at all times (a) a maximum debt to EBITDA ratio of 3.5:1 and (b) a minimum interest coverage ratio of 2.0:1. Compliance with the financial covenants shall be tested quarterly and certified by the Borrower in the compliance certificates delivered with its financial statements.

The covenants set out in this clause 8 shall commence on the date of this Agreement and shall continue for the duration of this Agreement until all amounts due under this Agreement have been irrevocably paid in full.

9EVENTS OF DEFAULT

Each of the following shall constitute a Default Event: (a) the Borrower fails to pay any principal interest or other sum due under this Agreement within 7 Business Days after the due date; (b) any representation or warranty made by the Borrower (or any Guarantor) is or becomes incorrect or misleading in any material respect when made or repeated; (c) the Borrower fails to comply with any of its obligations under this Agreement or any Security Document and (if capable of remedy) such breach is not remedied within 14 days of the Lender giving notice of such breach; (d) an Insolvency Event occurs in respect of the Borrower or any Guarantor; (e) cross-default: any indebtedness of the Borrower or any Guarantor in excess of \£10,000 is not paid when due or is accelerated prior to its stated maturity; (f) a Material Adverse Change occurs; or (g) any judgment or order is made against the Borrower or any Guarantor in excess of \£10,000 which remains undischarged for 14 days.

The Lender shall not be entitled to declare a Default Event in respect of clauses (b) (c) or (g) above until the expiry of any applicable grace period.

10CONSEQUENCES OF DEFAULT

Upon the occurrence of any Default Event the Lender may by notice in writing to the Borrower declare that the Loan together with all accrued interest and any other sums due under this Agreement shall become immediately due and payable.

Default interest shall be payable on all overdue amounts from the date of the Default Event until the date of actual payment.

The Borrower shall indemnify the Lender against all costs and expenses incurred by the Lender in enforcing its rights and remedies under this Agreement.

11ACCELERATION AND REMEDIES

On and at any time after the occurrence of a Default Event which is continuing the Lender may by notice to the Borrower: (a) cancel the Loan Facility (if not already drawn); (b) declare that all or any part of the Loan together with all accrued interest and all other amounts outstanding under this Agreement be immediately due and payable; and (c) exercise all its rights and remedies under the Security Documents including enforcement of the security and the appointment of a receiver or administrator under the Law of Property Act 1925 or the Insolvency Act 1986 (as applicable).

The Borrower shall pay on demand all costs and expenses (including legal fees) incurred by the Lender in connection with the enforcement of this Agreement or any Security Document following a Default Event.

12SECURITY AND GUARANTEES

The Borrower shall as a condition of the Loan provide security in favour of the Lender pursuant to the Security Documents which shall include a first legal charge over the residential property located at 123 High Street London UK and a debenture creating fixed and floating charges over all of the Borrower's assets and undertaking.

The security shall be created by the Security Documents in a form satisfactory to the Lender and shall be perfected in accordance with the Companies Act 2006 including registration of all charges at Companies House within 21 days of creation.

The Borrower shall not create or permit to subsist any security over any of its assets other than in favour of the Lender (negative pledge).

The Borrower shall procure the provision of a guarantee from each Guarantor in respect of the obligations of the Borrower under this Agreement and the Security Documents. Each guarantee shall be in a form satisfactory to the Lender and if required executed as a deed.

The security and guarantees provided under this clause 12 shall continue in full force and effect until all obligations of the Borrower under this Agreement and the Security Documents have been discharged in full. The charge over residential property shall comply with all applicable UK mortgage regulations including the Mortgages and Home Finance: Conduct of Business sourcebook (MCOB) to the extent applicable.

13CONDITIONS PRECEDENT

The obligation of the Lender to advance the Loan is subject to the satisfaction of the following conditions precedent: (a) delivery to the Lender of this Agreement duly executed by the Borrower; (b) delivery of all Security Documents duly executed (and if required as a deed) together with evidence of their due stamping and registration at Companies House within 21 days; (c) all representations and warranties set out in clause 6 being true and accurate in all material respects; (d) no Default Event having occurred or being continuing or which would result from the advance of the Loan; (e) delivery of a legal opinion from the Borrower's solicitors confirming the validity and enforceability of this Agreement and the Security Documents; (f) the Borrower having delivered its latest audited and interim accounts; (g) completion of all due diligence and Know Your Customer requirements to the Lender's satisfaction; and (h) there having been no Material Adverse Change since 2024-01-15.

14INDEMNITIES

The Borrower shall indemnify the Lender against all losses damages costs and expenses arising from or in connection with this Agreement or the Security Documents except to the extent that such losses result from the Lender's gross negligence or wilful misconduct.

The Borrower shall indemnify the Lender against any tax liabilities including stamp duty or VAT related to the Loan this Agreement or the Security Documents.

The Borrower shall indemnify the Lender for all reasonable legal and enforcement costs incurred by the Lender in connection with this Agreement or the Security Documents.

15EXPENSES AND COSTS

The Borrower shall pay all legal fees and expenses incurred by the Lender in connection with the preparation negotiation and execution of this Agreement and the Security Documents.

The Borrower shall pay all such expenses and costs on demand by the Lender.

16TAXES AND WITHHOLDING

All payments to be made by the Borrower under this Agreement shall be made free and clear of and without any deduction for or on account of withholding tax or any other taxes unless required by law.

If the Borrower is required by law to make any deduction or withholding from any payment the Borrower shall pay to the Lender such additional amounts (gross-up) as will result in the Lender receiving the full amount which it would have received had no such deduction or withholding been made. The Borrower shall provide the Lender with tax receipts or other evidence of payment of any withheld tax within 30 days of making such payment.

The Lender shall provide the Borrower with such forms and information as may be reasonably required to enable the Borrower to make payments without withholding or at a reduced rate under applicable UK tax rules (including FATCA if applicable). If the Lender receives a tax credit in respect of any additional amount paid by the Borrower it shall reimburse the Borrower such amount as the Lender determines (acting reasonably) will leave it in the same after-tax position as it would have been in had the additional amount not been required.

The provisions of this clause 16 shall apply to all payments under this Agreement.

17CONFIDENTIALITY

Each party shall keep confidential the terms of this Agreement and any information disclosed to it by the other party in connection with this Agreement and shall not disclose such information to any third party without the prior written consent of the disclosing party.

The confidentiality obligations in this clause 17 shall not apply to information which (a) is or becomes public knowledge other than as a result of a breach of this clause; (b) is required to be disclosed by law court order or any governmental or regulatory authority (including HMRC or the Financial Conduct Authority); or (c) was already known to the receiving party prior to disclosure.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.

Useful Resources When Considering a Loan Agreement in the United Kingdom

United Kingdom Reference Legislation

Loan Agreement FAQs

Document Generation FAQs

Related Articles