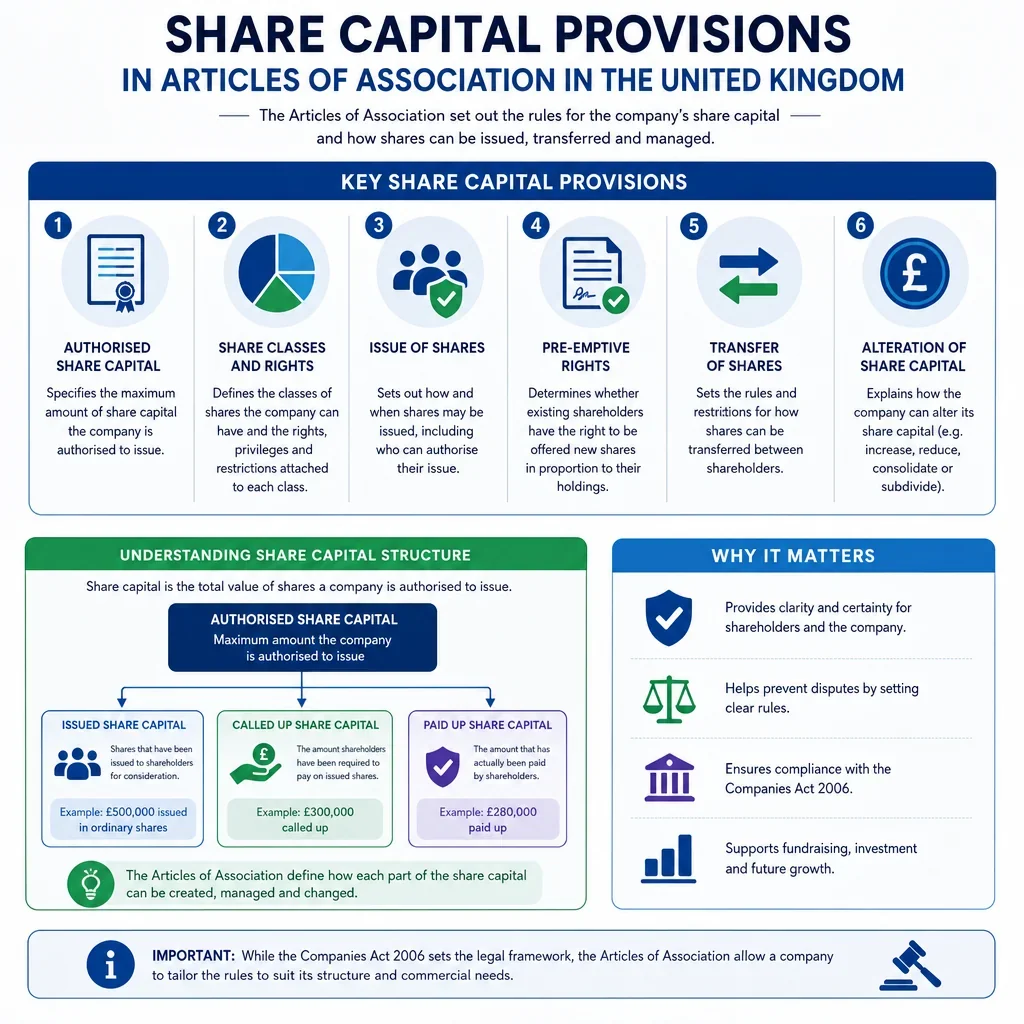

Share Capital Provisions In Articles Of Association In The United Kingdom

Share Capital Provision | Explanation | Common Share Type | Customisation Frequency | Practical Example |

|---|---|---|---|---|

Share classes | ||||

Ordinary share rights | Defines the usual voting, dividend and capital rights attached to ordinary shares. | Ordinary shares | Usually standard | A founder needs one vote per share and equal dividends for all holders. |

Preference share rights | Sets priority rights, usually for dividends or capital repayment, ahead of ordinary shares. | Preference shares | Highly bespoke | An investor receives a fixed dividend before ordinary shareholders are paid. |

Dividends | ||||

Cumulative preference dividend | Provides that unpaid preference dividends accrue and must be paid later before junior dividends. | Preference shares | Often customised | A company skips dividends during a loss-making year and arrears carry forward. |

Non-cumulative preference dividend | Provides that missed preference dividends do not accrue for later payment. | Preference shares | Often customised | A company cannot pay the fixed dividend in one year and no arrears arise. |

Share classes | ||||

Participating preference shares | Gives preference shareholders their priority return plus a further share in surplus profits or assets. | Preference shares | Highly bespoke | A venture investor receives a liquidation preference and then participates in remaining proceeds. |

Capital distributions | ||||

Redeemable share terms | States when shares may or must be bought back by the company and on what terms. | Redeemable shares | Highly bespoke | Employee shares are redeemed when the employee leaves the business. |

Redemption at company option | Allows the company to choose whether and when to redeem specified shares. | Redeemable shares | Often customised | The company redeems investor shares after a financing milestone. |

Redemption at shareholder option | Allows a shareholder to require the company to redeem shares on stated terms. | Redeemable shares | Highly bespoke | An investor can exit if no sale or listing occurs by a target date. |

Share classes | ||||

Alphabet share classes | Creates separate classes, such as A, B and C shares, often with different dividend rights. | Alphabet shares | Often customised | Family shareholders receive different dividend amounts through A and B shares. |

Dividends | ||||

Differential dividend rights | Allows different share classes to receive different dividend amounts or rates. | Alphabet shares | Highly bespoke | Directors declare a dividend only on B shares held by one spouse. |

Share classes | ||||

Pari passu ranking | States that shares rank equally with each other for dividends, voting or capital. | All share types | Usually standard | New ordinary shares rank equally with existing ordinary shares after issue. |

Voting rights by class | Specifies whether each share class carries votes and how many votes apply per share. | All share types | Often customised | A founder keeps enhanced voting shares after outside investment. |

Non-voting shares | Gives shares economic rights but no vote, except where the articles provide otherwise. | Alphabet shares | Often customised | Employee shareholders receive profit participation without control rights. |

Weighted voting rights | Gives particular shares more than one vote per share on some or all decisions. | Ordinary shares | Highly bespoke | A founder retains control while issuing ordinary economic shares to investors. |

Deferred shares | Creates shares with rights postponed behind other classes, often with minimal practical value. | All share types | Often customised | Old shares are converted into deferred shares during a capital reorganisation. |

Partly paid shares | Allows shares to be issued with some nominal value unpaid and callable later. | All share types | Often customised | Investors agree to pay remaining share capital when a future funding call is made. |

Calls on unpaid share capital | Sets how directors can require payment of unpaid amounts on partly paid shares. | All share types | Often customised | The board calls unpaid capital to meet project funding needs. |

Share transfer | ||||

Company lien on shares | Allows the company to retain rights over shares where amounts owed on them are unpaid. | All share types | Usually standard | A shareholder has unpaid calls and the company blocks transfer until payment. |

Forfeiture for non-payment | Permits shares to be forfeited if a shareholder fails to pay a valid call. | All share types | Usually standard | A shareholder ignores a call notice and the board forfeits the shares. |

Share allotment | ||||

Directors' authority to allot shares | Gives directors power to issue shares, subject to statutory limits and articles. | All share types | Often customised | The board issues new shares to an angel investor after shareholder approval. |

Single-class private company allotment power | A private company with one share class may allot shares unless the articles prohibit it. | Ordinary shares | Usually standard | A simple private company issues more ordinary shares without separate allotment authority. |

Allotment authority expiry | Sets a time limit and maximum amount for directors' authority to allot shares. | All share types | Often customised | Shareholders renew allotment authority before a planned investment round. |

Pre-emption | ||||

Statutory pre-emption on allotment | Requires new equity securities to be offered first to existing shareholders pro rata. | All share types | Often customised | Existing shareholders must be offered shares before a new investor subscribes. |

Exclusion of statutory pre-emption | Articles may exclude statutory pre-emption rights for private companies. | All share types | Often customised | A startup removes statutory pre-emption to simplify small option-style issues. |

Disapplication of pre-emption rights | Allows shareholders to disapply statutory pre-emption rights for a specific authority or issue. | All share types | Often customised | Shareholders approve issuing shares directly to a strategic investor. |

Pre-emption on share transfers | Requires selling shareholders to offer shares to existing members before outsiders. | All share types | Highly bespoke | A co-founder must offer shares to the other founder before selling to a third party. |

Right of first refusal | Gives existing shareholders first chance to match or accept a proposed transfer offer. | All share types | Highly bespoke | A shareholder receives a buyer offer and the others can match it. |

Pro rata allotment offer procedure | Sets how new shares are offered to existing holders in proportion to their holdings. | All share types | Usually standard | A rights-style offer lets each shareholder maintain their percentage ownership. |

Excess application rights | Lets shareholders apply for shares not taken up by others in a pre-emption offer. | All share types | Often customised | One shareholder takes extra shares after another declines their allocation. |

Share allotment | ||||

Minimum issue price | Shares must not be allotted at a discount to nominal value. | All share types | Usually standard | A £1 nominal share cannot be issued for 50p. |

Share premium treatment | Records amounts paid above nominal value in the share premium account. | All share types | Usually standard | An investor pays £10 for a £0.01 share, creating share premium. |

Payment for shares in cash | Covers allotments paid by cash, cheque, bank transfer or equivalent consideration. | All share types | Usually standard | A new shareholder subscribes for shares by bank transfer. |

Non-cash consideration for shares | Allows shares to be issued for assets, services or other non-cash consideration, subject to rules. | All share types | Often customised | A seller receives shares as consideration for transferring intellectual property. |

Share transfer | ||||

Directors' discretion to refuse transfer | Allows directors to refuse to register a share transfer in specified circumstances. | All share types | Often customised | The board refuses registration because transfer pre-emption was not followed. |

Instrument of transfer requirement | Requires a proper transfer document before shares are registered in another name. | All share types | Usually standard | A stock transfer form is delivered before the register is updated. |

Transfer notice procedure | Requires a selling shareholder to notify the company before a transfer can proceed. | All share types | Highly bespoke | A founder serves a transfer notice before offering shares to other members. |

Permitted transfers | Allows transfers to specified people without normal restrictions or pre-emption rights. | All share types | Highly bespoke | A family company allows transfers to spouses, children or family trusts. |

Compulsory transfer on trigger event | Requires a shareholder to sell shares when specified events occur. | All share types | Highly bespoke | A shareholder must sell after bankruptcy, death or serious breach. |

Good leaver and bad leaver provisions | Sets different transfer obligations and prices depending on why a shareholder leaves. | Ordinary shares | Highly bespoke | A dismissed employee must sell shares at a discount under bad leaver terms. |

Transmission on death | Deals with rights of personal representatives or beneficiaries after a shareholder dies. | All share types | Often customised | Executors seek registration or sale of a deceased shareholder's shares. |

Transmission on bankruptcy | Deals with rights of a trustee in bankruptcy or similar office-holder over shares. | All share types | Often customised | A trustee in bankruptcy asks to be recognised as entitled to shares. |

Share valuation on forced transfer | Sets how shares are valued when a shareholder must sell under the articles. | All share types | Highly bespoke | An independent accountant values shares after a founder leaves. |

Fair value transfer price | Requires shares to be sold at a fair value determined by an agreed method. | All share types | Highly bespoke | A departing shareholder receives market value for a minority holding. |

Discounted bad leaver price | Applies a lower price to shares sold after misconduct or prohibited departure. | Ordinary shares | Highly bespoke | A founder dismissed for fraud sells at nominal value rather than market value. |

Drag-along rights | Allows a required majority to force minority shareholders to sell on the same terms. | All share types | Highly bespoke | A buyer wants 100% ownership and majority shareholders trigger drag rights. |

Tag-along rights | Allows minority shareholders to join a majority sale on the same terms. | All share types | Highly bespoke | A majority shareholder sells control and minority holders can sell alongside. |

Share transfer lock-in period | Prevents shareholders from transferring shares for a stated period or before milestones. | All share types | Highly bespoke | Founders cannot sell shares for three years after incorporation. |

Board-approved transfers | Requires directors' consent before shares may be transferred. | All share types | Often customised | Directors block a transfer to a competitor. |

Dividends | ||||

Dividend declaration procedure | Sets how final and interim dividends are recommended, declared and paid. | All share types | Usually standard | Directors recommend a final dividend for shareholder approval. |

Distributable profits requirement | A company may make distributions only from profits available for that purpose. | All share types | Usually standard | Directors cannot pay dividends if accounts show no distributable profits. |

Interim dividends | Allows directors to pay dividends during the financial year if profits justify payment. | All share types | Usually standard | The board pays a mid-year dividend after strong quarterly results. |

Final dividends | Provides for shareholders to approve a dividend recommended by directors. | All share types | Usually standard | Members approve a year-end dividend at a general meeting or by written resolution. |

Dividends in specie | Allows distributions by transferring non-cash assets rather than paying cash. | All share types | Often customised | A holding company distributes shares in a subsidiary to its shareholders. |

Scrip dividends | Allows shareholders to receive new shares instead of a cash dividend. | Ordinary shares | Often customised | A shareholder elects to take shares rather than cash to preserve company cash. |

Dividend waiver recognition | Recognises that a shareholder may waive a dividend entitlement if validly documented. | All share types | Often customised | A founder waives a dividend so cash can be paid to external investors. |

Dividend record date | Identifies which shareholders are entitled to a dividend on a specified date. | All share types | Usually standard | A buyer of shares after the record date does not receive the declared dividend. |

Capital distributions | ||||

Capitalisation of profits | Allows reserves or profits to be capitalised and applied in paying up bonus shares. | All share types | Usually standard | The company issues bonus shares without shareholders paying cash. |

Share allotment | ||||

Bonus share issue | Issues additional shares to existing shareholders, usually funded from reserves. | Ordinary shares | Usually standard | Each shareholder receives one extra share for every ten held. |

Capital distributions | ||||

Reduction of share capital | Allows share capital to be reduced using statutory procedures, often with solvency statement approval. | All share types | Often customised | A company creates distributable reserves by reducing share capital. |

Purchase of own shares | Permits the company to buy back its own shares if statutory requirements are met. | All share types | Often customised | A company buys back a retiring shareholder's shares. |

Off-market buyback approval | Requires approval of an off-market contract before a company buys back shares privately. | All share types | Usually standard | Members approve a buyback agreement with a departing founder. |

Buyback out of distributable profits | Uses available distributable profits to fund the company's purchase of its own shares. | All share types | Usually standard | A profitable private company funds a founder exit from retained earnings. |

Buyback out of capital | Allows private companies to fund buybacks from capital using stricter statutory steps. | All share types | Often customised | A company lacks distributable profits but needs to buy back a leaver's shares. |

Treasury shares | Allows bought-back shares to be held by the company rather than cancelled, where permitted. | All share types | Often customised | A company holds repurchased shares for later employee share awards. |

Cancellation of bought-back shares | Cancels shares following buyback, reducing issued share capital. | All share types | Usually standard | A founder exit reduces the total number of shares in issue. |

Priority on return of capital | States the order in which share classes receive assets on winding up or capital return. | Preference shares | Highly bespoke | Preference shareholders recover invested capital before ordinary shareholders receive proceeds. |

Liquidation preference | Gives investors a preferred return on sale, liquidation or deemed liquidation events. | Preference shares | Highly bespoke | An investor receives 1x subscription money before proceeds are shared with founders. |

Distribution of surplus assets | Sets how remaining assets are divided after debts and priority rights are satisfied. | All share types | Often customised | On winding up, remaining cash is distributed pro rata to ordinary shareholders. |

Variation of rights | ||||

Definition of class rights | Identifies the rights attached to a class, such as voting, dividends and capital priority. | All share types | Often customised | A new investor checks whether preference rights are protected class rights. |

Variation of class rights procedure | Sets the consent needed to change rights attached to a particular share class. | All share types | Often customised | Preference shareholders must approve removal of their priority dividend rights. |

Class consent threshold | Typically requires written consent or a special resolution of the affected class. | All share types | Often customised | A 75% class vote is needed before A share rights can be amended. |

Minority objection to class variation | Allows qualifying dissenting class members to apply to court to cancel a variation. | All share types | Usually standard | Minority preference shareholders challenge a variation that removes their priority rights. |

Deemed variation of rights | States whether issuing further shares or changing capital counts as varying class rights. | All share types | Highly bespoke | Preference holders require consent before more senior shares are issued. |

Restriction on senior share classes | Prevents creation of shares ranking ahead of an existing class without class consent. | Preference shares | Highly bespoke | Series A investors block a later class with better liquidation priority. |

Share classes | ||||

Share consolidation | Combines shares into fewer shares with a higher nominal value. | All share types | Usually standard | Ten £0.10 shares are consolidated into one £1 share. |

Share subdivision | Splits shares into more shares with a lower nominal value. | All share types | Usually standard | One £1 share is subdivided into 100 £0.01 shares before investment. |

Conversion of shares into another class | Allows shares of one class to be converted into shares of another class. | All share types | Often customised | Preference shares convert into ordinary shares before a sale or listing. |

Automatic conversion trigger | Converts shares automatically when a specified event occurs. | Preference shares | Highly bespoke | Investor preference shares convert on an IPO or qualified financing. |

Anti-dilution adjustment | Adjusts conversion price or share rights if later shares are issued at a lower price. | Preference shares | Highly bespoke | Series A investors receive extra conversion protection after a down round. |

Share transfer | ||||

Employee shareholder restrictions | Limits employee-held shares through vesting, leaver rules or compulsory transfer terms. | Ordinary shares | Highly bespoke | Unvested shares must be transferred back when employment ends. |

Share classes | ||||

Nil-paid share obligations | Covers shares issued with no amount paid up and the holder's liability to pay later. | All share types | Often customised | A founder receives nil-paid shares and remains liable for unpaid nominal value. |

Share certificates | ||||

Issue of share certificates | Requires certificates to be issued within the statutory period after allotment or transfer. | All share types | Usually standard | A new shareholder receives a certificate after registration in the register of members. |

Share certificate contents | States the holder, number and class of shares, and certificate authentication requirements. | All share types | Usually standard | A certificate confirms ownership of 1,000 A ordinary shares. |

Replacement share certificates | Allows replacement certificates for lost, damaged or destroyed originals, often with indemnity. | All share types | Usually standard | A shareholder signs an indemnity before receiving a replacement certificate. |

Uncertificated shares | Allows shares to be held and transferred without paper certificates under relevant regulations. | All share types | Often customised | A company joining an electronic settlement system permits uncertificated holdings. |

Register of members priority | Recognises that legal title to shares depends on entry in the register of members. | All share types | Usually standard | A buyer is not treated as a member until the register is updated. |

Joint holders of shares | Sets how rights, notices, certificates and voting work where shares have multiple holders. | All share types | Usually standard | Two trustees hold one shareholding and one certificate is issued for it. |

Share classes | ||||

Fractional entitlements on reorganisation | Deals with fractions arising on consolidation, subdivision, bonus issues or conversions. | All share types | Often customised | Fractional shares are rounded or sold after a share consolidation. |

Share allotment | ||||

Authorised share capital limit | A legacy or optional articles limit on the maximum share capital directors may issue. | All share types | Often customised | Older articles require amendment before more shares can be issued. |

Statement of capital consistency | Requires filed share capital details to match issued shares and class rights. | All share types | Usually standard | Companies House filings are updated after issuing a new class of shares. |

What Share Capital Provisions Should UK Articles Of Association Cover?

UK articles should be checked carefully where the company will have more than one shareholder, more than one share class, investor funding, employee shareholders or family ownership. The key drafting choices usually concern who may receive new shares, who may buy existing shares, how dividends are allocated, and how class rights can be changed.

When Are Bespoke Share Capital Articles Most Important?

- Alphabet shares normally need tailored dividend and class rights provisions so directors can lawfully recommend different dividends for different share classes.

- Preference shares should state the dividend rate, priority on capital return, voting rights and whether unpaid dividends accumulate.

- Redeemable shares need clear redemption mechanics, including timing, price and whether redemption is at the company\'s or shareholder\'s option.

- Pre-emption rights on allotment and transfer can protect existing shareholders from dilution or unwanted third-party owners.

- Drag-along and tag-along rights are not in the Companies Act 2006 model articles and are often added for investor-backed or joint venture companies.

Which UK Legal Rules Commonly Affect Share Capital Drafting?

The Companies Act 2006 contains important default rules on allotment authority, statutory pre-emption rights, class rights variation, share certificates, distributions and purchase or redemption of shares. Articles can sometimes modify or exclude statutory defaults, but not every statutory rule can be overridden. Companies using AI-generated articles should therefore ensure the share capital provisions match the intended share structure and comply with the Companies Act 2006.

FAQs

You Might Also Be Interested In