Purchase Price Mechanisms In United Kingdom Asset Purchase Agreements

Pricing mechanism | How it works | Typical use case | Typical benefit | Drafting points | Common issues |

|---|---|---|---|---|---|

Fixed price | |||||

Fixed Purchase Price | A single agreed price is payable at completion with no post-completion adjustment. | Simple asset sales with stable value and limited balance sheet exposure. | Seller | Define included assets, excluded liabilities, payment method, timing and any VAT gross-up. | Mispriced stock, undisclosed liabilities, asset omissions and disputes over apportionments. |

Fixed Price With Working Capital Assumption | Price is fixed but negotiated by reference to an assumed normal working capital level. | Transactions where parties want simplicity but still price the business on normalised trading levels. | Depends on drafting | Record assumptions, management accounts relied on and any express no-adjustment wording. | Buyer may discover abnormal working capital after completion without a price remedy. |

Completion accounts | |||||

Completion Accounts Net Asset Adjustment | Estimated price is adjusted after completion by comparing actual net assets with a target figure. | Asset deals where value depends on balance sheet items at completion. | Buyer | Define assets, liabilities, accounting policies, hierarchy, timetable and dispute expert. | Accounting policy conflicts, cut-off errors, provisions and classification disputes. |

Completion Accounts Working Capital Adjustment | Price moves pound-for-pound above or below agreed target working capital at completion. | Trading businesses with receivables, payables and stock levels fluctuating before completion. | Balanced | Define working capital, target, normalisation, debt-like items and consistency with accounts. | Seasonality, aged debtors, accrued expenses, deferred income and manipulation before completion. |

Cash-Free Debt-Free Adjustment | Enterprise value is converted to equity value by adding cash and deducting debt at completion. | Business sales priced on EBITDA or enterprise value metrics. | Balanced | Define cash, debt, debt-like items, trapped cash, leases and intra-group balances. | Disputes over overdrafts, customer deposits, finance leases, unpaid bonuses and tax liabilities. |

Estimated Completion Statement True-Up | Buyer pays an estimated amount at completion, then a later statement creates a balancing payment. | Deals needing completion before final accounts figures are available. | Balanced | Set estimate process, supporting evidence, payment deadlines and interest on late adjustment. | Inflated estimates, poor records and disagreement over post-completion adjustments. |

Locked box | |||||

Locked Box Fixed Equity Price | Price is fixed by reference to accounts at a historic locked box date. | Competitive sales where seller wants price certainty and no completion accounts process. | Seller | Define locked box accounts, leakage, permitted leakage, covenants and buyer information rights. | Hidden leakage, unreliable locked box accounts and value movement before completion. |

Locked Box Leakage Indemnity | Seller indemnifies buyer for prohibited value leakage between locked box date and completion. | Locked box asset sales with ongoing seller control before completion. | Buyer | List leakage categories, claim period, pound-for-pound recovery and tax gross-up. | Whether management charges, bonuses, dividends or related-party payments are leakage. |

Permitted Leakage Pricing | Specified value transfers to the seller are allowed and factored into the agreed price. | Locked box deals where known dividends, salaries or group charges must continue. | Seller | State amounts, recipients, timing, supporting documents and whether caps are inclusive of VAT. | Ambiguous categories allow unexpected value extraction before completion. |

Locked Box Interest Ticker | Buyer pays daily interest or an economic accrual from locked box date to completion. | Seller gives buyer economic benefit from the locked box date but retains completion risk. | Seller | Specify rate, day count, start date, end date and whether it compounds. | Rate may overcompensate seller if trading deteriorates before completion. |

Deferred consideration | |||||

Fixed Deferred Instalments | Part of the purchase price is paid in fixed amounts after completion on agreed dates. | Buyer needs staged funding or seller accepts credit exposure for a higher headline price. | Buyer | Set payment dates, interest, acceleration, security, guarantees and set-off rights. | Buyer default, insolvency risk and disputed warranty set-off. |

Promissory Note Consideration | Buyer issues a negotiable or contractual payment instrument for deferred purchase price. | Private asset sales where seller wants documentary evidence of deferred debt. | Seller | Align note terms with APA, include default events and preserve or exclude set-off. | Priority, enforceability, transferability and conflict with limitation or claim procedures. |

Secured Deferred Consideration | Deferred price is backed by security, guarantee or charge over assets or buyer obligations. | Seller accepts payment delay but requires protection against buyer credit risk. | Seller | Draft security documents, registration obligations, priority, release and enforcement triggers. | Unregistered charges, competing lenders, enforcement delay and asset value deterioration. |

Vendor Loan Note | Seller receives loan notes instead of immediate cash for part of the purchase price. | Larger private transactions needing staged payment or tax and funding structuring. | Depends on drafting | Define redemption, interest, subordination, transfer restrictions, events of default and withholding tax. | Subordination to bank debt, illiquidity, default and tax treatment uncertainty. |

Deposit or retention | |||||

Warranty Retention Holdback | Buyer withholds part of the price for a defined period to cover potential claims. | Small and mid-market asset sales with limited seller covenant strength after completion. | Buyer | State amount, release date, claim notice mechanics, set-off and disputed claim treatment. | Buyer over-withholding, late claims and unclear release procedures. |

Escrow Account Holdback | Part of the price is paid to an escrow agent and released under agreed conditions. | Deals where neutral custody is needed for claims, consents or completion deliverables. | Balanced | Use escrow agreement covering release triggers, interest, fees, disputes and authorised instructions. | Deadlock, bank compliance delays and inconsistency between escrow agreement and APA. |

Deposit Credited Against Price | Buyer pays a deposit on exchange, credited against the purchase price at completion. | Conditional asset sales with a gap between exchange and completion. | Seller | State stakeholder status, forfeiture, refund events, interest and completion failure consequences. | Whether deposit is forfeitable if conditions fail or seller defaults. |

Non-Refundable Deposit | Seller keeps the deposit if buyer fails to complete in specified circumstances. | Seller takes assets off the market or incurs transaction costs for the buyer. | Seller | Avoid penalty risk by linking forfeiture to genuine commercial protection and clear default events. | Penalty clause arguments, failed conditions and disputed buyer default. |

Inventory adjustment | |||||

Stock Valuation Adjustment | Price is adjusted after a stocktake by reference to agreed stock valuation rules. | Asset purchases involving retail, manufacturing, wholesale or hospitality stock. | Balanced | Define stock, valuation basis, stocktake process, obsolete stock and observer rights. | Obsolescence, damaged goods, consignment stock, cut-off and valuation method disputes. |

Inventory Target Collar | No adjustment applies unless stock value falls outside an agreed upper or lower band. | Businesses where minor stock fluctuations are commercially immaterial. | Balanced | Specify target, collar width, whether adjustment applies to excess only or full shortfall. | Cliff-edge effects and disputes over whether abnormal stock builds count. |

Obsolete Stock Exclusion | Obsolete, damaged or slow-moving stock is excluded or discounted in calculating price. | Asset sales with aged inventory or product lines at risk of write-down. | Buyer | Define obsolescence by age, condition, saleability, write-down policy and inspection rights. | Subjective saleability tests and inconsistent historic provisioning. |

Work In Progress Adjustment | Price includes or adjusts for unfinished work valued under agreed cost or recoverability rules. | Manufacturing, construction, professional services or project-based asset purchases. | Depends on drafting | Define WIP, valuation method, customer billing cut-off, losses and completion responsibility. | Overstated recoverability, incomplete records and customer disputes after handover. |

Completion Stocktake Adjustment | Parties conduct a completion stocktake and adjust price for counted stock value. | Retail or warehouse businesses where stock is a major acquired asset. | Balanced | Set timing, counting rules, independent valuer, access, sampling and disagreement process. | Trading during stocktake, shrinkage, damaged stock and inconsistent SKU records. |

Earn-out | |||||

Revenue Earn-Out | Additional consideration is payable if the acquired business reaches revenue targets after completion. | High-growth businesses where profit is uncertain but sales pipeline is important. | Depends on drafting | Define revenue recognition, excluded revenue, returns, related-party sales and audit rights. | Revenue acceleration, discounts, customer churn and post-completion integration effects. |

EBITDA Earn-Out | Further price is payable if EBITDA exceeds agreed thresholds during an earn-out period. | Profitable businesses where seller and buyer disagree on maintainable earnings. | Depends on drafting | Define EBITDA, add-backs, management charges, accounting policies and buyer conduct obligations. | Cost allocation, exceptional items, group overheads and deliberate profit suppression. |

Gross Profit Earn-Out | Additional consideration depends on gross profit rather than revenue or EBITDA. | Businesses where margins matter but overhead allocation would be contentious. | Balanced | Define cost of goods sold, rebates, discounts, returns, stock write-offs and margin adjustments. | Input cost allocation, product mix changes and inconsistent margin reporting. |

Milestone Earn-Out | Extra price is paid when specified operational, regulatory or commercial milestones are achieved. | Technology, life sciences, licensing or project businesses with identifiable future events. | Depends on drafting | Define objective milestone evidence, deadlines, partial achievement and buyer effort obligations. | Whether buyer must pursue milestones and whether achievement was prevented. |

Customer Retention Earn-Out | Further price is payable if specified customers remain or renew after completion. | Service businesses where goodwill depends on recurring customer relationships. | Buyer | Define retained customer, renewal value, churn, replacement contracts and attribution rules. | Customer migration, buyer service standards and disputes over equivalent replacement revenue. |

Seller-Managed Earn-Out | Seller remains involved and can influence post-completion performance during the earn-out period. | Owner-managed businesses where goodwill and know-how remain tied to the seller. | Seller | Align service terms, restrictive covenants, authority limits, dismissal consequences and tax status. | Employment disputes, loss of control, conflicts with buyer integration and bad leaver provisions. |

Capped Earn-Out | Earn-out is payable by formula but cannot exceed an agreed maximum amount. | Buyer will share upside but needs certainty on maximum acquisition cost. | Buyer | State cap, currency, aggregation across periods and whether overperformance carries forward. | Seller incentives reduce once cap is reached. |

Tiered Earn-Out | Different payment levels apply as performance passes agreed thresholds. | Transactions where parties want graduated upside sharing rather than an all-or-nothing trigger. | Balanced | Define tiers, cliff effects, interpolation, carry-forward and worked examples. | Threshold manipulation and ambiguity around partial period performance. |

Deferred consideration | |||||

Royalty-Based Deferred Consideration | Seller receives a percentage of future sales from specified acquired assets or products. | Intellectual property, product line or licensing asset purchases. | Depends on drafting | Define royalty base, deductions, audit rights, reporting, term and anti-avoidance protections. | Bundled sales, transfer pricing, discontinued products and under-reporting. |

Completion accounts | |||||

Trade Receivables Collection Adjustment | Price is adjusted if acquired receivables are not collected within an agreed period. | Asset sales where debtors transfer and collectability is uncertain. | Buyer | Define receivables, collection efforts, bad debt threshold, reassignment and set-off. | Customer disputes, pre-completion credits, allocation of part-payments and bad debt timing. |

Assumed Liabilities Adjustment | Purchase price is reduced by liabilities the buyer agrees to assume at completion. | Asset purchases where selected contracts, employee liabilities or trade creditors are assumed. | Buyer | List assumed and excluded liabilities, valuation basis, cut-off and indemnities. | Unclear liability allocation, contingent liabilities and liabilities embedded in assigned contracts. |

Tax Liability Adjustment | Price is adjusted or indemnified for specified tax liabilities connected with pre-completion periods. | Asset sales involving payroll taxes, VAT, capital allowances or historic tax risks. | Buyer | Define tax, periods, conduct of claims, gross-up, VAT treatment and exclusions. | TOGC failure, unpaid PAYE, VAT assessments and overlap with warranties. |

Fixed price | |||||

VAT TOGC Price Protection | Price assumes no VAT if the asset sale qualifies as a transfer of a going concern. | UK business asset sales intended to be outside the scope of VAT as a TOGC. | Buyer | Include VAT gross-up, TOGC conditions, option to tax confirmations and HMRC challenge allocation. | Unexpected VAT funding, SDLT interaction for property and failed TOGC conditions. |

Asset Class Price Allocation | Overall price is allocated among goodwill, stock, plant, IP, property and other assets. | Asset purchases needing tax, accounting, capital allowance or stamp duty allocation. | Depends on drafting | Include allocation schedule, tax consistency covenant and adjustment if HMRC challenges values. | Buyer and seller may prefer different allocations for tax and accounting reasons. |

Completion accounts | |||||

Property Outgoings Apportionment | Rent, service charge, rates and utilities are apportioned between seller and buyer at completion. | Asset purchases including leasehold or freehold business premises. | Balanced | Set apportionment date, estimates, balancing payments and responsibility for arrears. | Late service charge reconciliations, dilapidations and business rates cut-off. |

Employee Liability Adjustment | Price is adjusted for accrued holiday, bonuses, wages or employee liabilities transferring with the business. | Business asset sales where employees transfer under TUPE. | Buyer | Define transferring employees, accrued liabilities, payroll cut-off, indemnities and employee information. | Unknown claims, holiday accruals, enhanced terms and failure to consult. |

Deferred consideration | |||||

Contract Assignment Contingent Price | Part of the price becomes payable only when key contracts are assigned or novated. | Asset sales where customer, supplier or landlord consent is needed after completion. | Buyer | Define required consents, longstop, substitute benefit, cooperation duties and payment trigger. | Third-party refusal, interim trading arrangements and disagreement over equivalent value. |

Regulatory Approval Contingent Price | A deferred amount is payable only if required regulatory approvals or licences are obtained. | Regulated asset sales involving licences, permits or change of control approvals. | Buyer | Identify approvals, responsible party, effort standard, longstop and consequences of refusal. | Delay, conditional approvals and disputes over reasonable endeavours. |

Post-Completion Clawback | Seller must repay part of the price if specified adverse events occur after completion. | Deals with uncertain customer retention, licence transfer or asset condition risks. | Buyer | Define trigger events, repayment formula, time limits, caps and enforcement security. | Characterisation as penalty, causation and seller ability to repay. |

Completion accounts | |||||

Expert Determined Adjustment | An independent accountant or valuer resolves disputed price adjustment items. | Any completion accounts, stock valuation or earn-out calculation with technical disputes. | Balanced | Define expert role, appointment, submissions, jurisdiction, costs and finality of decision. | Expert exceeds mandate, procedural unfairness and unclear distinction from arbitration. |

Adjustment Cap And Basket | Adjustments apply only above thresholds and may be capped at a maximum amount. | Deals where parties want to avoid immaterial true-up disputes. | Depends on drafting | State deductible or tipping basket, cap, aggregation and excluded fraud or leakage claims. | Confusion between warranty limitations and price adjustment limitations. |

Minimum Cash Adjustment | Price is reduced if the business has less than agreed minimum cash at completion. | Asset deals where buyer needs immediate liquidity to operate acquired business. | Buyer | Define cash, restricted cash, bank cut-off, uncleared payments and intra-group sweep restrictions. | Cash sweeps, uncleared cheques, customer deposits and bank reconciliation timing. |

Debt-Like Item Adjustment | Price is reduced for obligations treated commercially as debt despite accounting classification. | Enterprise value deals with liabilities not shown as conventional borrowings. | Buyer | List items such as finance leases, unpaid bonuses, tax, pensions and customer deposits. | Double counting with working capital and disagreement over normal trading liabilities. |

Locked box | |||||

Pound-For-Pound Leakage Reduction | Purchase price is reduced or reimbursed exactly by the amount of prohibited leakage. | Locked box deals where parties want simple compensation for value extraction. | Buyer | Include direct and indirect leakage, tax, connected persons and no de minimis unless intended. | Proving indirect leakage and quantifying tax effects. |

Deferred consideration | |||||

Split Completion And Deferred Payment | Buyer pays part at completion and the balance later, often without performance conditions. | Cash-constrained buyers or seller-financed management buyouts of business assets. | Buyer | Document schedule, security, default interest, acceleration and whether title passes immediately. | Seller credit risk, title retention conflict and buyer insolvency. |

Title Retention Price Protection | Seller seeks to retain title to specified assets until deferred price is paid. | Asset sales involving identifiable goods or equipment with staged payments. | Seller | Identify assets, possession rights, insurance, risk, insolvency effects and registration if security. | May operate as registrable security and conflict with buyer financing or onward sales. |

Deposit or retention | |||||

Contingent Liability Escrow | Specific amount is held back until identified contingent liabilities are resolved. | Known disputes, tax audits, environmental issues or customer claims in an asset sale. | Buyer | Describe liability, reserve amount, release evidence, defence control and excess liability allocation. | Reserve adequacy, prolonged disputes and overlapping indemnity caps. |

Environmental Remediation Holdback | Part of the price is retained pending investigation or remediation of environmental liabilities. | Asset purchases involving land, industrial sites, waste permits or contamination risk. | Buyer | Define remediation standard, regulator involvement, access rights, expert reports and release mechanics. | Unknown contamination, regulator requirements and remediation cost overruns. |

Completion accounts | |||||

Pension Liability Adjustment | Price is reduced or indemnified for pension liabilities connected with transferring employees or schemes. | Asset sales involving defined benefit exposure or significant employee transfers. | Buyer | Identify schemes, liabilities, actuarial basis, auto-enrolment duties and indemnity scope. | Hidden deficits, contribution notices and mismatch between employment and pensions obligations. |

Net Debt Peg Adjustment | Price adjusts by comparing actual net debt at completion against an agreed peg. | Acquisitions priced with assumed normalised borrowing or debt-like obligations. | Balanced | Define net debt, peg, debt-like items, cash equivalents and double-count protections. | Overlap with working capital, treatment of leases and intra-group balances. |

Surplus Cash Sweep | Seller extracts surplus cash before completion or receives value for cash left in the business. | Asset sales where cash is excluded unless expressly transferred. | Seller | Clarify whether cash is an asset, excluded asset, leakage or completion adjustment item. | Operational cash needs, trapped cash and double counting in working capital. |

Fixed price | |||||

Nominal Or Negative Price With Liabilities Assumed | Buyer pays nominal price or receives value because assumed liabilities exceed asset value. | Distressed asset sales, restructurings or transfers of loss-making business units. | Depends on drafting | Precisely define assumed liabilities, excluded liabilities, creditor consents and insolvency risk. | Creditor challenge, undervalue issues, hidden liabilities and consent failures. |

Deferred consideration | |||||

Deferred Price With Solvency Covenant | Buyer pays later but gives financial covenants to protect seller against deterioration. | Seller-financed acquisitions where buyer credit risk is material. | Seller | Include covenants, reporting, default triggers, acceleration and restrictions on distributions or new debt. | Monitoring burden and difficulty enforcing before actual payment default. |

Earn-out | |||||

Earn-Out Set-Off Mechanism | Buyer may set warranty or indemnity claims against earn-out payments otherwise due. | Deals where earn-out is the main seller recourse fund after completion. | Buyer | State whether set-off requires admitted, determined or merely notified claims. | Buyer may delay earn-out by asserting unproven claims. |

Deferred consideration | |||||

Acceleration On Buyer Default | All deferred amounts become immediately due if buyer defaults or insolvency occurs. | Seller accepts deferred payment but wants leverage if buyer credit worsens. | Seller | Define default, cure periods, insolvency events, notice and interaction with security enforcement. | Disputes over material default and enforceability of default interest or charges. |

Completion accounts | |||||

Missing Asset Price Reduction | Price is reduced if specified assets are not transferred or delivered at completion. | Asset sales with long asset schedules, equipment lists or IP transfer deliverables. | Buyer | Attach asset schedules, condition standards, replacement value rules and delivery evidence. | Unclear asset identification, leased assets and assets already disposed of. |

Inventory adjustment | |||||

Condition-Based Asset Valuation | Price for plant, equipment or stock changes based on agreed condition or usability criteria. | Sales of machinery, vehicles, fixtures, plant or operational equipment. | Buyer | Define condition standards, inspection timing, valuation expert and repair cost deductions. | Wear and tear, undocumented defects and disagreement over fair repair costs. |

Completion accounts | |||||

Accounting Hierarchy Adjustment | Calculation follows a ranked hierarchy of specific policies, past practice and accounting standards. | Any completion accounts deal where accounting judgement could affect price. | Balanced | Rank transaction-specific rules above consistency and UK GAAP or IFRS as intended. | Conflict between consistency with past accounts and compliance with accounting standards. |

Earn-out | |||||

Earn-Out Anti-Manipulation Covenant | Buyer must not run the acquired business mainly to avoid or reduce earn-out payments. | Earn-outs where buyer controls pricing, costs, customers or integration after completion. | Seller | Define conduct standard, reserved matters, information rights and remedies for breach. | Distinguishing legitimate business decisions from earn-out avoidance. |

Earn-Out Accounting Policy Lock | Earn-out calculations use agreed accounting policies regardless of buyer post-completion changes. | Performance earn-outs where accounting treatment can move targets materially. | Seller | Specify locked policies, management accounts format, adjustments and expert review rights. | Buyer systems integration makes historic reporting hard to reproduce. |

Deferred consideration | |||||

Key Employee Retention Price Adjustment | Part of the price depends on specified employees remaining for a set period after completion. | People-dependent asset purchases where value depends on transferring staff continuity. | Buyer | Avoid employment penalty issues define voluntary resignation, dismissal, death and redundancy effects. | Tax, employment law, enforceability and whether seller can control employee retention. |

Deposit or retention | |||||

Landlord Consent Holdback | Part of the price is retained until lease assignment or licence to assign is completed. | Asset purchases where premises are essential to the acquired business. | Buyer | Define consent condition, interim occupation, rent liability, longstop and refund or release rules. | Landlord delay, consent conditions, authorised guarantee agreements and business interruption. |

Licence Transfer Holdback | Price is held back until operating licences, permits or franchise rights are transferred or reissued. | Hospitality, care, transport, financial services or franchised business asset sales. | Buyer | Identify licences, transferability, interim operation, cooperation duties and failure consequences. | Non-transferable licences, regulator delay and loss of trading ability. |

Fixed price | |||||

Normalised EBITDA Price Bridge | Price is fixed using agreed normalised EBITDA and multiple rather than adjusted later. | Business asset sales valued on earnings but closed without completion accounts. | Depends on drafting | Document normalisation adjustments, add-backs, excluded one-offs and reliance limitations. | Overstated add-backs, owner salary adjustments and reliance on unaudited figures. |

Deferred consideration | |||||

Deferred Consideration With Interest | Deferred price accrues agreed interest until paid. | Longer payment deferrals where seller requires compensation for funding the buyer. | Seller | State rate, compounding, withholding, default rate and whether interest is price or debt return. | Tax treatment, usury not typical in UK, and excessive default interest penalty arguments. |

Completion accounts | |||||

De Minimis Completion Adjustment | No balancing payment is made unless the adjustment exceeds an agreed minimum amount. | Smaller asset deals where adjustment costs could exceed the amount at stake. | Balanced | Clarify whether threshold is deductible, tipping or item-by-item. | Parties dispute aggregation and whether several small items count together. |

Deposit or retention | |||||

Tax Clearance Retention | Part of the price is retained until specified tax clearances, filings or confirmations are obtained. | Asset deals with historic VAT, PAYE, capital allowance or transaction tax concerns. | Buyer | Specify clearance required, cooperation, release deadline and fallback if HMRC does not respond. | HMRC timing, unclear clearance scope and unnecessary withholding of seller funds. |

Fixed price | |||||

Capital Allowances Allocation Mechanism | Parties allocate price to plant and machinery or fixtures for capital allowances purposes. | UK asset sales including plant, machinery, fixtures or commercial property interests. | Depends on drafting | Include tax allocation, section 198 election where relevant and cooperation covenants. | Seller and buyer have conflicting tax incentives and missed election deadlines. |

SDLT Allocation Adjustment | Price allocation to land is separately stated because SDLT may apply to land transactions. | Asset purchases including freehold or leasehold property in England or Northern Ireland. | Depends on drafting | Allocate consideration to land, chattels and goodwill on supportable market values. | HMRC challenge to allocation, chattel overvaluation and VAT-inclusive consideration effects. |

LBTT Property Allocation Adjustment | Price allocation identifies consideration for Scottish land transactions subject to LBTT. | Asset purchases including Scottish freehold, leasehold or other land interests. | Depends on drafting | Separate Scottish land value from goodwill, moveables and other business assets. | Incorrect jurisdictional tax treatment and unsupported allocation between land and business assets. |

LTT Property Allocation Adjustment | Price allocation identifies consideration for Welsh land transactions subject to LTT. | Asset purchases including land or leases in Wales. | Depends on drafting | Separate Welsh land value from goodwill, chattels, stock and other assets. | Wrong UK land tax regime and HMRC or WRA valuation challenge. |

Completion accounts | |||||

Grant Repayment Adjustment | Price is reduced for public grants or subsidies repayable due to asset transfer or change of use. | Asset sales involving grant-funded equipment, premises or regional support schemes. | Buyer | Identify grants, clawback triggers, consent requirements and indemnity responsibility. | Undisclosed grant conditions and post-completion repayment demands. |

Deposit or retention | |||||

Handover Deliverables Retention | Part of the price is retained until records, data, keys, passwords or operational materials are delivered. | Asset sales where operational continuity depends on seller handover after completion. | Buyer | List deliverables, objective acceptance tests, release timing and cure procedure. | Subjective satisfaction tests and disputes over incomplete or unusable records. |

Earn-out | |||||

Customer Book Valuation Adjustment | Price depends on value, number or recurring revenue of customers transferred to the buyer. | Insurance, financial advice, subscription, agency or service business asset purchases. | Depends on drafting | Define customer, consent, recurring revenue, clawback, non-solicitation and data transfer conditions. | Customer consent, data protection, churn and double counting new customers. |

Deferred consideration | |||||

Licence Revenue Share | Seller receives a share of future licence income from acquired intellectual property. | IP asset sales where future exploitation value is uncertain. | Seller | Define net receipts, sublicensing, audit, minimum exploitation duties and anti-diversion rules. | Buyer parks IP, routes income through affiliates or bundles licences with services. |

Fixed price | |||||

Receivables Excluded From Price | Seller keeps pre-completion receivables and they are excluded from the asset price. | Simple asset deals where buyer acquires business assets but not historic debtors. | Seller | Define collection rights, customer notices, misdirected payments and buyer cooperation. | Customer confusion, set-off against buyer invoices and misallocated payments. |

Completion accounts | |||||

Deferred Income Adjustment | Price is reduced for customer payments received by seller for services buyer must perform. | Subscription, maintenance, events, training or support businesses sold as assets. | Buyer | Identify unearned revenue, service obligations, VAT, refunds and contract assignment status. | Understated performance obligations and customer refund claims. |

Prepayments Adjustment | Price increases for prepaid expenses from which buyer benefits after completion. | Asset sales including insurance, software, rent, licences or service contracts paid in advance. | Seller | Define qualifying prepayments, transferability, benefit period and evidence required. | Non-transferable contracts and disputed post-completion benefit. |

Deposit or retention | |||||

Completion Payment Via Solicitor Undertaking | Funds are released at completion against solicitors' undertakings or agreed completion steps. | UK completions requiring controlled exchange of money, transfers and releases. | Balanced | Specify client account details, undertakings, completion sequence and authority to release funds. | Failed completion steps, bank delays and mismatch between undertakings and APA obligations. |

Deferred consideration | |||||

Restrictive Covenant Clawback | Deferred payments reduce or stop if seller breaches non-compete or non-solicitation covenants. | Goodwill-heavy asset sales where seller could damage acquired customer relationships. | Buyer | Ensure covenants are reasonable in scope, territory, duration and protected interest. | Restraint of trade enforceability and disproportionate forfeiture arguments. |

Completion accounts | |||||

Insurance Proceeds Adjustment | Price or proceeds allocation changes if assets suffer insured loss before completion. | Conditional completions involving physical assets or premises at risk of damage. | Depends on drafting | State risk transfer, insurance maintenance, termination rights and proceeds assignment. | Underinsurance, insurer consent, disputed repair value and completion despite damage. |

Unassigned IP Price Reduction | Price reduces if specified intellectual property is not validly assigned to buyer. | Technology, brand, software or content asset purchases. | Buyer | List IP, assignment documents, moral rights waivers, employee-created IP and registration filings. | Third-party ownership, contractor IP, open-source software and incomplete registers. |

Deferred consideration | |||||

Share Consideration Deferred Issue | Buyer issues shares to seller at completion or later instead of cash price. | Strategic acquisitions where seller accepts buyer equity for upside participation. | Depends on drafting | Define valuation, issue timing, class rights, dilution, lock-up and securities law compliance. | Buyer valuation changes, minority protections, dilution and illiquidity. |

Earn-out | |||||

Share-Based Earn-Out | Earn-out is satisfied by issuing shares if performance targets are met. | Growth acquisitions where buyer preserves cash and seller wants equity upside. | Depends on drafting | Set share valuation date, number formula, anti-dilution, tax, leaver and listing restrictions. | Share price volatility, dilution and disagreement over valuation at issue date. |

Completion accounts | |||||

Currency Exchange Rate Adjustment | Price or adjustment items are converted using agreed exchange rates or rate sources. | UK asset sales with foreign receivables, stock, debt or overseas assets. | Depends on drafting | Specify currency, rate source, date, hedging treatment and FX gains or losses. | Volatility between signing and completion and inconsistent rate sources. |

Deferred consideration | |||||

Inflation-Indexed Deferred Consideration | Deferred price increases by reference to CPI, RPI or another agreed index. | Long deferrals where inflation could materially erode seller value. | Seller | Define index, base month, substitute index, cap, floor and calculation examples. | Index discontinuance, negative inflation and disputes over compounding. |

Completion accounts | |||||

Completion Accounts Objection Procedure | Draft accounts become final unless disputed within an agreed review period. | Any asset purchase using a post-completion price true-up. | Balanced | Set preparation deadline, review period, access to papers, objection notice and expert referral. | Late objections, insufficient detail and restricted access to accounting records. |

How Should A UK Asset Purchase Agreement Set The Purchase Price?

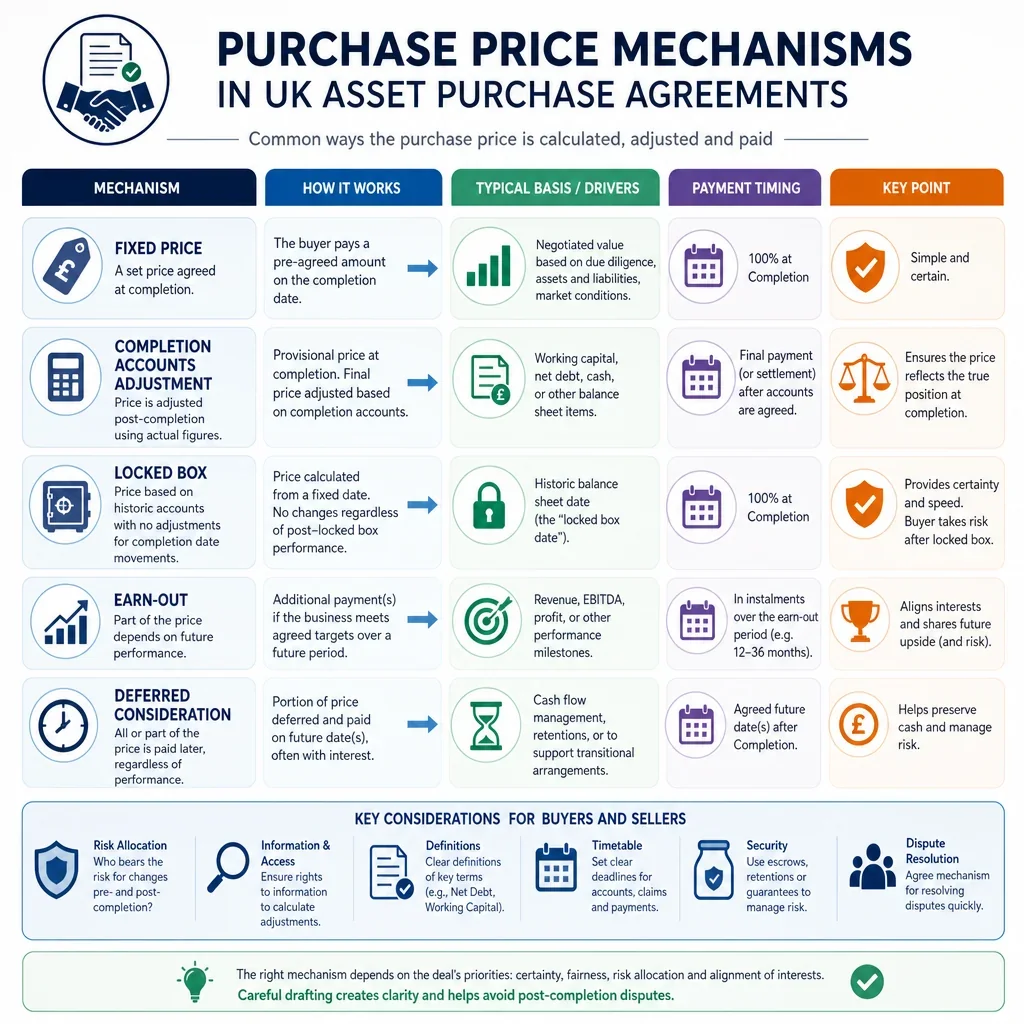

Completion accounts are usually the most precise option where working capital, stock, debt or cash can move materially before completion, but they require detailed accounting definitions, timetable mechanics and expert determination provisions.

Locked box pricing can give the seller earlier price certainty and a cleaner completion, but the buyer should negotiate robust leakage restrictions, permitted leakage schedules and indemnity protection for value extracted after the locked box date.

Earn-outs and deferred consideration can bridge valuation gaps in UK asset sales, especially where future performance is uncertain, but they commonly create disputes over control, accounting policies, targets, mitigation duties and information rights.

Deposits, retentions and escrows are practical tools for warranty claims, stock adjustments, tax liabilities or handover risk, but the agreement should state release conditions, interest treatment, set-off rights and the consequences of completion not occurring.

VAT and TOGC treatment can materially affect cash flow in asset purchases. If the sale is intended to be a transfer of a going concern, the pricing and payment mechanics should align with UK VAT rules and include protections if HMRC later challenges the treatment.

Inventory mechanisms need special care in asset purchases because title, risk, slow-moving stock, consignment stock, work in progress and stock valuation methods directly affect what the buyer is actually acquiring.

FAQs

You Might Also Be Interested In