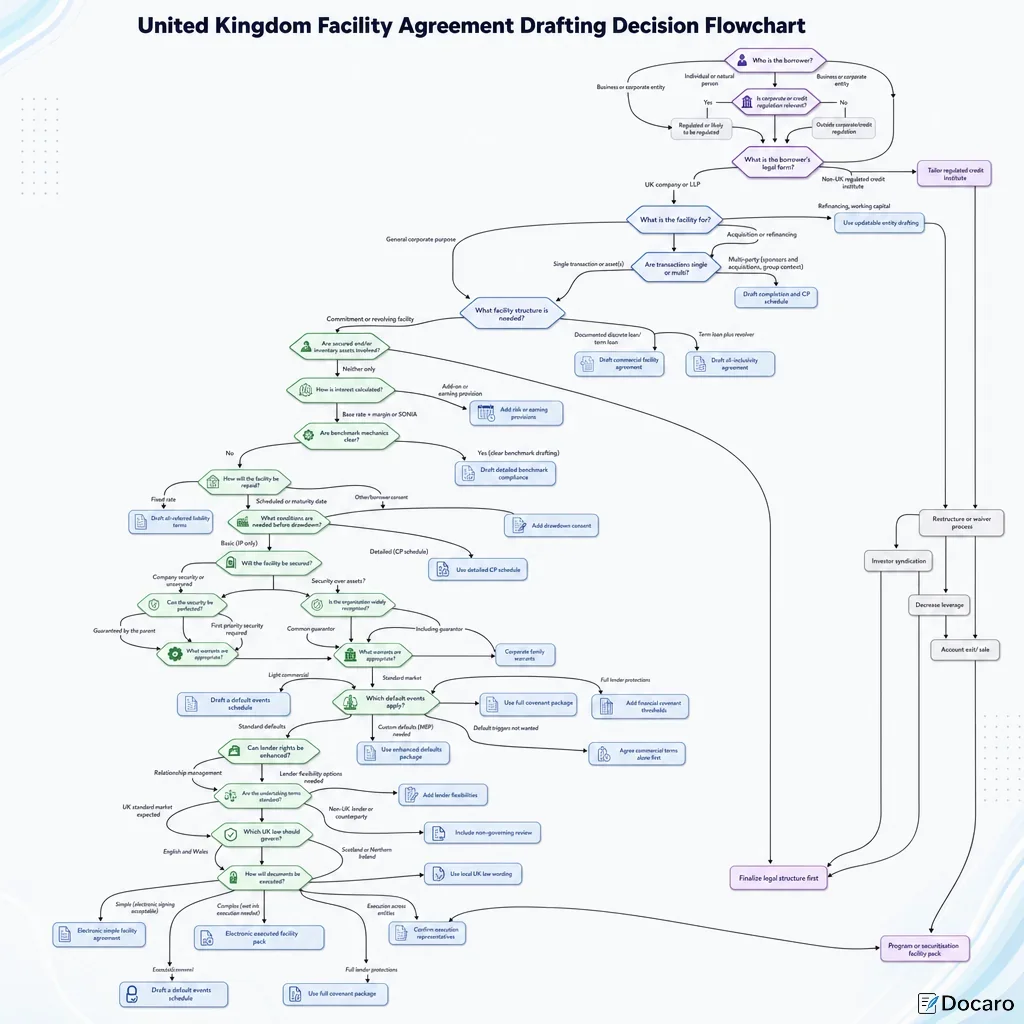

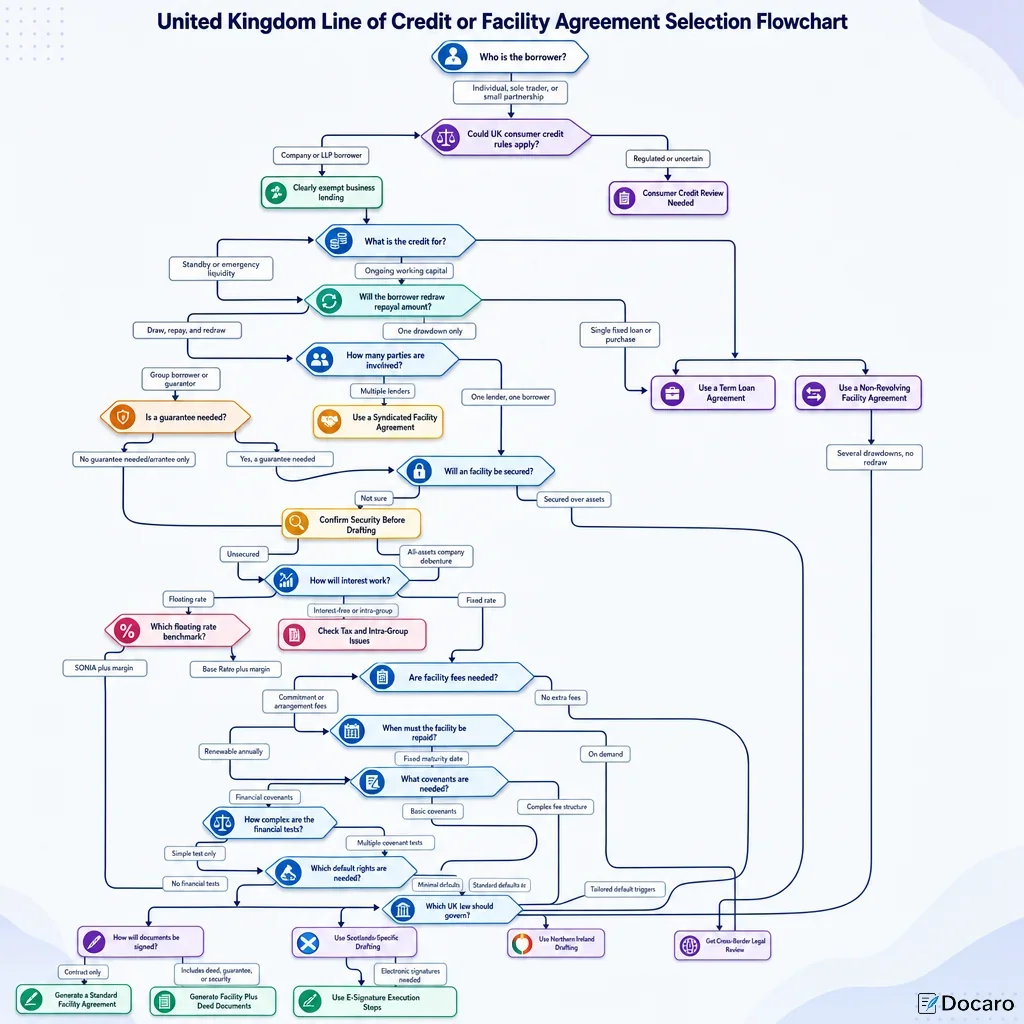

United Kingdom Line Of Credit Or Facility Agreement Selection Flowchart

Who is the borrower?

Why Is Choosing The Right UK Facility Agreement Important?

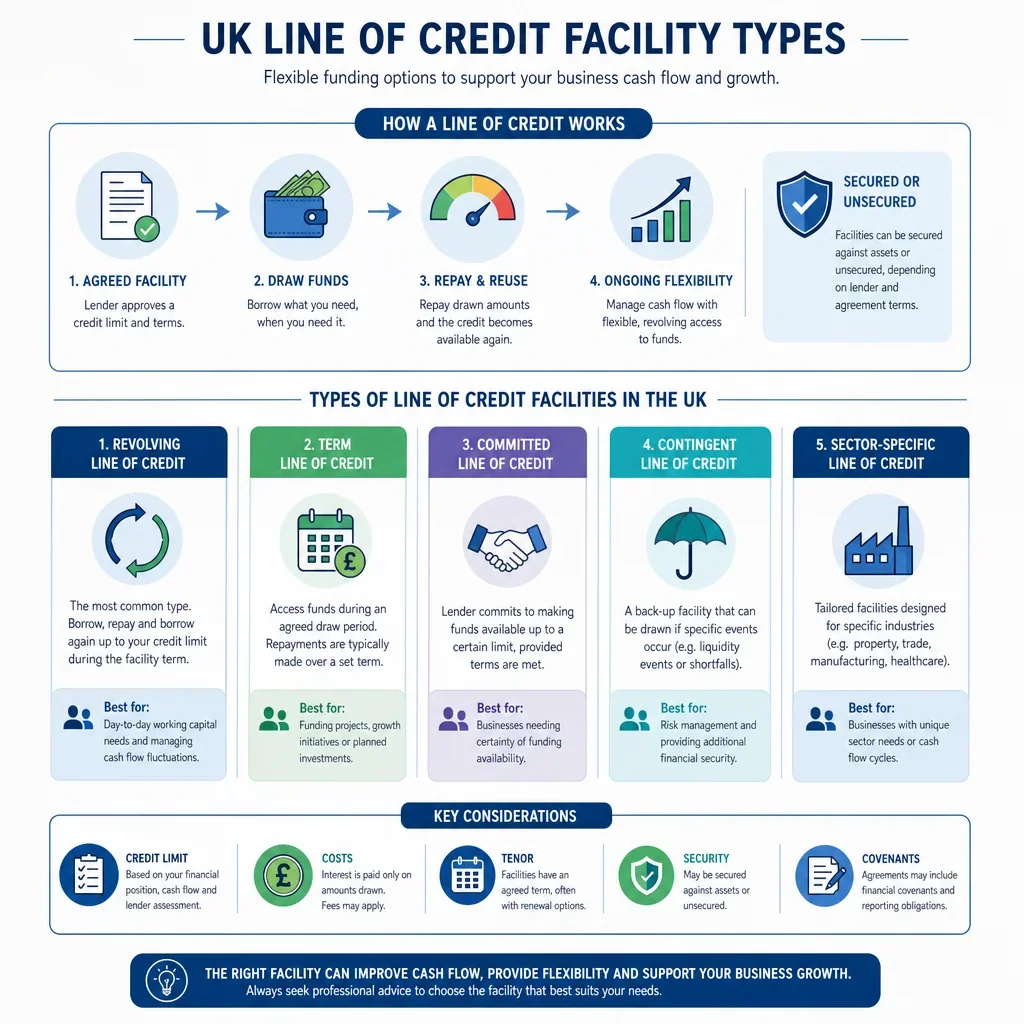

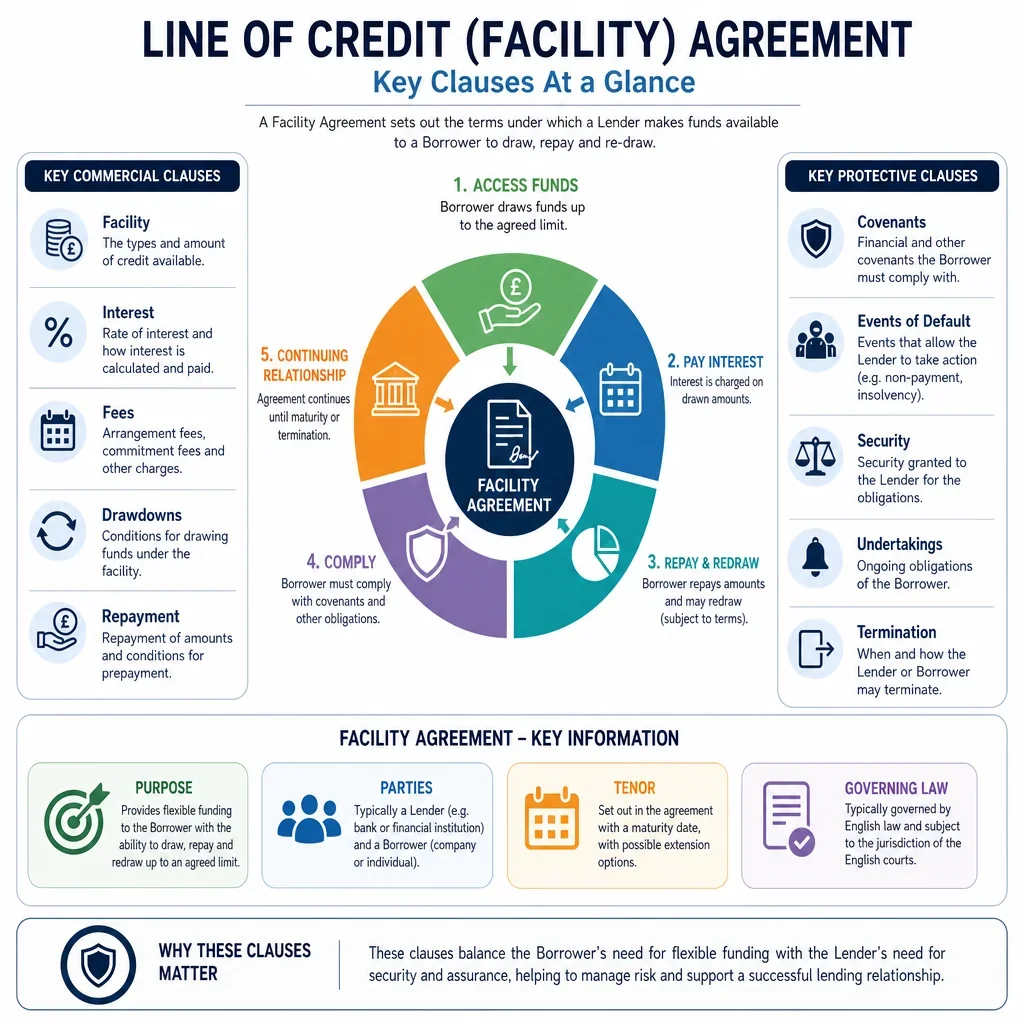

A UK line of credit or facility agreement controls how money is made available, repaid, priced, and enforced. Choosing the wrong document can create uncertainty about drawdowns, interest, default rights, guarantees, security, and repayment obligations.

When Can A Facility Agreement Become A Regulated Credit Issue?

If the borrower is an individual, sole trader, or small partnership, UK consumer credit law may apply unless an exemption is available. This can affect FCA authorisation, required wording, borrower protections, and enforceability. A standard commercial facility agreement should not be used without checking the regulatory position.

Why Does Security Change The Document Package?

Secured lending often needs more than the facility agreement itself. A lender may need a debenture, legal charge, guarantee, or asset-specific security. UK company charges may need registration at Companies House, and land security may also need Land Registry steps.

What Terms Should Be Clear Before Drafting?

- Borrower and lender details, including company names and authority to sign.

- Facility type, such as revolving, non-revolving, demand, or fixed maturity.

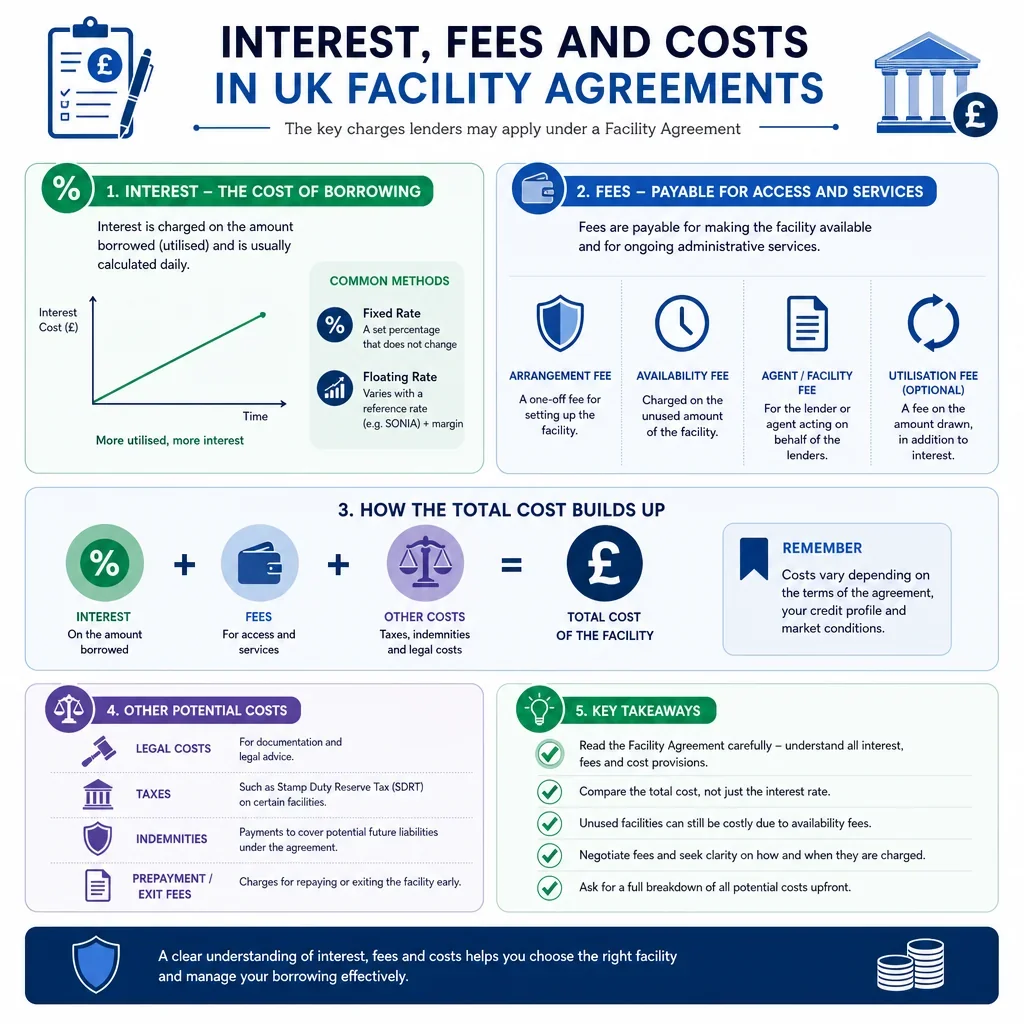

- Interest and fees, including fixed rates, Bank Rate, SONIA, margins, and default interest.

- Covenants and defaults, including reporting duties, financial tests, and insolvency events.

- Governing law, especially where Scotland, Northern Ireland, or cross-border parties are involved.

How Does The Right Agreement Reduce Risk?

The right facility agreement helps both parties understand the commercial bargain and reduces disputes. It also supports enforcement if payments are missed, covenants are breached, or security must be relied on. For UK businesses, careful selection is especially important where FCA rules, Companies House filings, tax issues, or property security are involved.

FAQs

You Might Also Be Interested In