Facility Agreement Clause Guide In The United Kingdom

Created:

This guide helps readers understand key clauses in facility agreements and how they apply in the United Kingdom. It is useful for comparing terms, identifying negotiation points, and drafting with greater confidence. For related resources, see our AI Generated British Facility Agreement page.

Clause Category | Purpose | Importance Level | Drafting Note | Mainly Affects |

|---|---|---|---|---|

Parties | ||||

Core commercial term | Identifies the lender, borrower, guarantors, agents and other parties. | Usually essential | Use exact legal names, registration numbers and addresses check capacity and authority. | All parties |

Definitions And Interpretation | ||||

Boilerplate | Defines key terms and sets interpretation rules for the agreement. | Usually essential | Defined terms drive default triggers, covenants, interest and repayment mechanics. | All parties |

Facility Amount | ||||

Core commercial term | States the maximum amount the lender agrees to make available. | Usually essential | Specify currency, committed amount, sub-limits and whether increases are permitted. | Borrower and lender |

Type Of Facility | ||||

Core commercial term | States whether the facility is term, revolving, overdraft or another structure. | Usually essential | Facility type affects availability, redraw rights, repayment and commitment fees. | Borrower and lender |

Purpose | ||||

Core commercial term | Limits how the borrower may use loan proceeds. | Usually essential | Align with credit approval breach usually gives lender default rights. | Borrower |

Availability Period | ||||

Core commercial term | Sets the time during which the borrower may draw funds. | Usually essential | State start and end dates unused commitments usually cancel at expiry. | Borrower |

Utilisation Request | ||||

Repayment and payment mechanics | Sets the notice and information required to draw down funds. | Usually essential | Include form, timing, bank account details and irrevocability of request. | Borrower |

Conditions Precedent | ||||

Core commercial term | Lists documents and confirmations required before first drawdown. | Usually essential | Typically includes corporate approvals, constitutional documents, KYC and security documents. | Borrower and lender |

Further Conditions To Utilisation | ||||

Core commercial term | Requires repeated confirmations before each drawing. | Common but transaction-specific | Often requires no default and repeated representations at each utilisation date. | Borrower |

Commitment | ||||

Core commercial term | Records each lender's obligation to make funds available. | Usually essential | In syndicated deals, specify each lender's commitment and several liability. | Lender and borrower |

Repayment Date | ||||

Repayment and payment mechanics | States when borrowed amounts must be repaid. | Usually essential | Use clear maturity date or repayment schedule to avoid payment disputes. | Borrower |

Amortisation Schedule | ||||

Repayment and payment mechanics | Sets instalment amounts and dates for gradual repayment. | Common but transaction-specific | Check consistency with cash flow projections and financial covenant testing. | Borrower |

Bullet Repayment | ||||

Repayment and payment mechanics | Requires repayment of principal in one amount at maturity. | Common but transaction-specific | Creates refinancing risk lender may require cash sweep or tighter covenants. | Borrower |

Revolving Facility Repayment And Redrawing | ||||

Repayment and payment mechanics | Allows repaid amounts to be reborrowed during the availability period. | Common but transaction-specific | Define rollover mechanics, minimum drawings and final repayment clearly. | Borrower and lender |

Voluntary Prepayment | ||||

Repayment and payment mechanics | Allows the borrower to repay early if notice and conditions are met. | Common but transaction-specific | Consider minimum amounts, notice, break costs and whether prepaid sums may be redrawn. | Borrower |

Mandatory Prepayment | ||||

Repayment and payment mechanics | Requires early repayment after specified events such as disposals or insurance receipts. | Common but transaction-specific | Define trigger events, thresholds, reinvestment rights and timing. | Borrower |

Change Of Control | ||||

Events of default | Protects lender if ownership or control of the borrower changes. | Common but transaction-specific | Specify control thresholds and whether event triggers default, cancellation or prepayment. | Borrower and lender |

Cancellation Of Commitments | ||||

Repayment and payment mechanics | Allows undrawn commitments to be cancelled in agreed circumstances. | Usually essential | State whether cancellation is voluntary, automatic, permanent or pro rata. | Borrower and lender |

Currency Of Payment | ||||

Repayment and payment mechanics | Specifies the currency in which payments must be made. | Usually essential | Include currency indemnity if liabilities may be enforced in another currency. | Borrower and lender |

Payments | ||||

Repayment and payment mechanics | Sets how, where and when payments must be made. | Usually essential | Include payment accounts, cut-off times, cleared funds and no set-off wording. | Borrower |

Business Day Convention | ||||

Repayment and payment mechanics | Adjusts payment dates falling on non-business days. | Usually essential | Choose following, modified following or preceding convention align with interest periods. | All parties |

Application Of Payments | ||||

Repayment and payment mechanics | Sets the order in which received payments reduce obligations. | Usually essential | Usually applies costs, fees, interest, default interest, then principal. | Borrower and lender |

Set-Off | ||||

Repayment and payment mechanics | Allows the lender to apply credit balances against amounts owed. | Common but transaction-specific | Borrowers often seek notice rights and limits on cross-currency set-off. | Borrower |

No Set-Off Or Counterclaim | ||||

Repayment and payment mechanics | Requires borrower payments in full without deduction or counterclaim. | Usually essential | Should be drafted clearly, especially where consumer or statutory protections may apply. | Borrower |

Interest Rate | ||||

Interest and fees | Sets how interest on drawn amounts is calculated. | Usually essential | State margin, benchmark, compounding if any, day count and calculation agent. | Borrower and lender |

SONIA Benchmark | ||||

Interest and fees | Uses the Sterling Overnight Index Average as a sterling floating rate benchmark. | Common but transaction-specific | Include observation shift, lookback, compounded rate formula and fallback terms. | Borrower and lender |

Base Rate Interest | ||||

Interest and fees | Links interest to a specified bank base rate or Bank Rate. | Common but transaction-specific | Define whose base rate applies and when changes take effect. | Borrower and lender |

Fixed Rate Interest | ||||

Interest and fees | Applies a stated interest rate for all or part of the facility term. | Common but transaction-specific | Address break costs and prepayment restrictions if lender hedges funding. | Borrower and lender |

Default Interest | ||||

Interest and fees | Increases interest on overdue amounts or during default. | Usually essential | Rate should be proportionate to avoid penalty arguments under English law. | Borrower |

Interest Periods | ||||

Interest and fees | Defines periods for calculating and paying interest. | Usually essential | Align periods with repayment dates, rate-setting dates and business day rules. | All parties |

Interest Payment Dates | ||||

Interest and fees | States when accrued interest must be paid. | Usually essential | Specify monthly, quarterly, maturity or other dates avoid mismatch with cash flow. | Borrower |

Day Count Fraction | ||||

Interest and fees | Sets the formula for calculating daily interest accrual. | Usually essential | Common sterling market approach is actual days over 365 confirm product terms. | Borrower and lender |

Commitment Fee | ||||

Interest and fees | Charges a fee on undrawn committed amounts. | Common but transaction-specific | State rate, accrual basis, payment dates and whether cancelled commitments stop fee accrual. | Borrower |

Arrangement Fee | ||||

Interest and fees | Charges a fee for arranging or providing the facility. | Common but transaction-specific | Clarify when payable and whether refundable if drawdown does not occur. | Borrower |

Agency Fee | ||||

Interest and fees | Pays an agent for administering a syndicated facility. | Common but transaction-specific | Usually documented in a fee letter define VAT treatment and annual timing. | Borrower and agent |

Break Costs | ||||

Interest and fees | Compensates lender for funding losses caused by early payment or broken interest periods. | Common but transaction-specific | Borrower may request evidence and a cap avoid vague loss calculations. | Borrower |

Costs And Expenses | ||||

Interest and fees | Requires borrower to reimburse agreed transaction and enforcement costs. | Usually essential | Specify legal fees, valuation costs, registration fees and enforcement expenses. | Borrower |

Tax Gross-Up | ||||

Interest and fees | Requires borrower to increase payments if tax withholding applies. | Common but transaction-specific | Consider UK withholding tax, qualifying lender concepts and treaty relief. | Borrower and lender |

Tax Indemnity | ||||

Interest and fees | Protects lender from certain tax liabilities connected with the facility. | Common but transaction-specific | Borrower should seek carve-outs for lender taxes on net income or tax misconduct. | Borrower and lender |

VAT | ||||

Interest and fees | Allocates VAT costs on fees, costs and services under the facility. | Common but transaction-specific | State whether amounts are inclusive or exclusive of VAT and who bears irrecoverable VAT. | Borrower |

FATCA | ||||

Interest and fees | Allocates compliance obligations and withholding risk under FATCA. | Common but transaction-specific | Mainly relevant for cross-border lending or financial institution parties. | Borrower and lender |

Increased Costs | ||||

Interest and fees | Passes certain regulatory or funding cost increases to the borrower. | Common but transaction-specific | Borrowers often negotiate exclusions, mitigation duties and replacement lender rights. | Borrower |

Market Disruption | ||||

Interest and fees | Provides alternative pricing if normal funding or benchmark markets fail. | Common but transaction-specific | Use with benchmark fallback provisions avoid lender-only subjective pricing where possible. | Borrower and lender |

Benchmark Replacement | ||||

Interest and fees | Sets how a discontinued or unavailable interest benchmark is replaced. | Common but transaction-specific | Important after LIBOR transition include consent threshold and adjustment spread. | All parties |

Security | ||||

Security and guarantees | Records collateral granted to secure the borrower's obligations. | Common but transaction-specific | Usually supported by separate debenture, legal charge, pledge or assignment. | Borrower and lender |

Registration Of Charges | ||||

Security and guarantees | Requires registrable security granted by a UK company to be registered. | Specialist advice recommended | Late or missed Companies House registration can make security void against insolvency officials and creditors. | Lender and borrower |

Guarantee | ||||

Security and guarantees | Makes a guarantor liable if the borrower fails to pay or perform. | Common but transaction-specific | Use indemnity wording and check corporate benefit, capacity and execution formalities. | Guarantor |

All Monies Guarantee Or Security | ||||

Security and guarantees | Secures all present and future liabilities owed to the lender. | Common but transaction-specific | Borrowers and guarantors may seek limits by facility, amount or time. | Borrower and guarantor |

Continuing Guarantee | ||||

Security and guarantees | Keeps guarantee liability in force despite repayments or account changes. | Common but transaction-specific | State revocation rights, final discharge mechanics and protection after repayment reversals. | Guarantor |

Guarantee Limitations | ||||

Security and guarantees | Limits guarantee exposure by amount, law or corporate capacity. | Specialist advice recommended | Important for upstream, cross-stream and overseas guarantees insolvency and corporate benefit issues may arise. | Guarantor and lender |

Security Trustee | ||||

Security and guarantees | Allows security to be held on trust for multiple finance parties. | Common but transaction-specific | Common in syndicated lending align with intercreditor and enforcement provisions. | Lenders and security trustee |

Negative Pledge | ||||

Covenants | Restricts the borrower from granting security to other creditors. | Usually essential | Negotiate permitted security exceptions for ordinary trading and existing arrangements. | Borrower |

Pari Passu Ranking | ||||

Covenants | Requires loan obligations to rank at least equally with other unsecured debt. | Usually essential | Subject to statutory preferred creditors and any agreed subordination. | Borrower and lender |

Financial Indebtedness Restrictions | ||||

Covenants | Limits additional borrowing and debt-like obligations. | Common but transaction-specific | Define indebtedness carefully and include permitted debt baskets if needed. | Borrower |

Disposals Restrictions | ||||

Covenants | Restricts sales or transfers of assets outside agreed exceptions. | Common but transaction-specific | Include ordinary-course disposals, obsolete assets and intra-group transfers if appropriate. | Borrower |

Acquisitions Restrictions | ||||

Covenants | Limits acquisitions, investments or mergers by the borrower group. | Common but transaction-specific | Use financial thresholds and permitted acquisition criteria to avoid over-restriction. | Borrower |

Dividends And Distributions Restrictions | ||||

Covenants | Restricts dividends, share buybacks and other value leakage. | Common but transaction-specific | UK companies can only make distributions from distributable profits. | Borrower and shareholders |

Loans And Guarantees Restrictions | ||||

Covenants | Controls lending, guarantees and credit support given by the borrower group. | Common but transaction-specific | Permit ordinary trade credit and intra-group loans where commercially needed. | Borrower |

Transactions With Affiliates | ||||

Covenants | Requires related-party transactions to be on arm's length terms. | Common but transaction-specific | Define affiliates and exempt ordinary-course or pre-agreed arrangements. | Borrower and shareholders |

Change Of Business | ||||

Covenants | Prevents material change to the borrower's core business. | Common but transaction-specific | Define permitted business broadly enough for normal commercial evolution. | Borrower |

Compliance With Laws | ||||

Covenants | Requires borrower group to comply with applicable laws and regulations. | Usually essential | Often qualified by materiality except for sanctions, anti-bribery and AML laws. | Borrower |

Sanctions Compliance | ||||

Covenants | Prevents dealings that breach UK or other applicable sanctions regimes. | Usually essential | Include use-of-proceeds, sanctioned persons and notification obligations. | Borrower and lender |

Anti-Bribery And Corruption | ||||

Covenants | Requires compliance with anti-bribery laws and policies. | Usually essential | The UK Bribery Act 2010 is central for UK corporate borrowers. | Borrower |

Anti-Money Laundering | ||||

Covenants | Requires parties to avoid money laundering and provide KYC information. | Usually essential | Lenders may need customer due diligence under UK money laundering regulations. | Borrower and lender |

Information Undertakings | ||||

Covenants | Requires delivery of accounts, budgets, compliance certificates and other information. | Usually essential | Set precise deadlines and formats link certificates to covenant testing dates. | Borrower |

Financial Statements | ||||

Covenants | Requires periodic audited or management accounts. | Usually essential | Align with Companies Act filing and audit requirements where relevant. | Borrower |

Financial Covenants | ||||

Covenants | Tests the borrower's financial health against agreed ratios or thresholds. | Common but transaction-specific | Definitions of EBITDA, debt and cash are heavily negotiated. | Borrower and lender |

Leverage Ratio Covenant | ||||

Covenants | Limits debt relative to EBITDA or another earnings measure. | Common but transaction-specific | Agree testing frequency, cure rights and permitted EBITDA add-backs. | Borrower |

Interest Cover Covenant | ||||

Covenants | Tests ability to pay finance charges from earnings or cash flow. | Common but transaction-specific | Ensure finance charges and EBITDA definitions match the business model. | Borrower |

Debt Service Cover Ratio | ||||

Covenants | Measures cash flow against scheduled debt service. | Common but transaction-specific | Common in real estate, project and cash-flow lending define cash flow tightly. | Borrower and lender |

Loan To Value Covenant | ||||

Covenants | Limits loan amount by reference to collateral value. | Common but transaction-specific | Important in real estate finance define valuation process and prepayment cure. | Borrower and lender |

Insurance | ||||

Covenants | Requires appropriate insurance over business, assets or collateral. | Common but transaction-specific | Lender may require noting of interest, loss payee wording or insurance proceeds prepayment. | Borrower |

Tax Compliance | ||||

Covenants | Requires timely payment and filing of material taxes. | Common but transaction-specific | Permit good-faith disputes where reserves are maintained. | Borrower |

Environmental Compliance | ||||

Covenants | Requires compliance with environmental law and permits. | Common but transaction-specific | More important for property, manufacturing, waste, energy and infrastructure borrowers. | Borrower |

Property Undertakings | ||||

Covenants | Maintains property collateral, title and lease compliance. | Common but transaction-specific | Include valuation rights, leases, planning, repairs and title issues for real estate finance. | Borrower |

Authorisations | ||||

Covenants | Requires all material licences, consents and approvals to remain in force. | Usually essential | Tailor to regulated sectors, planning permissions and corporate approvals. | Borrower |

Preservation Of Corporate Existence | ||||

Covenants | Requires borrower and obligors to remain validly existing entities. | Usually essential | Permit solvent reorganisations only with lender consent or agreed conditions. | Borrower and guarantor |

Bank Accounts | ||||

Covenants | Controls where borrower accounts are held and how cash is managed. | Optional | Useful for asset-based, real estate and cash-controlled facilities. | Borrower |

Cash Sweep | ||||

Repayment and payment mechanics | Requires surplus cash to prepay the facility. | Optional | Define excess cash, frequency, retention amounts and cure effects. | Borrower |

Representations And Warranties | ||||

Core commercial term | Records factual statements the lender relies on when providing credit. | Usually essential | State repetition dates and qualify by materiality or knowledge where appropriate. | Borrower and guarantor |

Status And Capacity Representation | ||||

Core commercial term | Confirms each obligor is validly existing and able to contract. | Usually essential | Check incorporation, constitutional documents and corporate power. | Borrower and guarantor |

Binding Obligations Representation | ||||

Core commercial term | Confirms finance documents create valid and binding obligations. | Usually essential | Usually subject to legal reservations such as insolvency and equitable principles. | Borrower, guarantor and lender |

Non-Conflict Representation | ||||

Core commercial term | Confirms finance documents do not breach law, constitution or contracts. | Usually essential | Borrower should review material contracts and existing finance documents. | Borrower and guarantor |

No Default Representation | ||||

Core commercial term | Confirms no default exists under the facility or material contracts. | Usually essential | Define whether it covers defaults, potential defaults and third-party contracts. | Borrower |

No Material Litigation | ||||

Core commercial term | Confirms no material disputes threaten the borrower's position. | Common but transaction-specific | Use monetary thresholds or material adverse effect wording to avoid overbreadth. | Borrower |

Accounts Representation | ||||

Core commercial term | Confirms financial statements give a fair and accurate financial picture. | Usually essential | Tie to accounting standards and disclosed qualifications or audit notes. | Borrower |

Solvency Representation | ||||

Core commercial term | Confirms borrower and obligors are not insolvent. | Usually essential | Consider statutory insolvency tests and directors' duties. | Borrower and guarantor |

Ranking Representation | ||||

Core commercial term | Confirms the lender's claims rank as agreed. | Usually essential | Must be checked against security, intercreditor terms and statutory priorities. | Lender and borrower |

Tax Representation | ||||

Core commercial term | Confirms tax filings and payments are materially up to date. | Common but transaction-specific | Borrower should disclose disputes and obtain materiality qualifications. | Borrower |

Events Of Default | ||||

Events of default | Lists events that allow lender remedies such as acceleration or cancellation. | Usually essential | Negotiate cure periods, materiality thresholds and notice requirements. | Borrower and lender |

Non-Payment Default | ||||

Events of default | Triggers default if borrower fails to pay on time. | Usually essential | Consider short grace periods for administrative or technical payment failures. | Borrower |

Breach Of Covenant Default | ||||

Events of default | Triggers default if borrower breaches undertakings. | Usually essential | Operational covenants often have cure periods financial covenant breaches may not. | Borrower |

Misrepresentation Default | ||||

Events of default | Triggers default if a representation is materially untrue or misleading. | Usually essential | Negotiate materiality and cure where inaccuracies can be remedied. | Borrower and guarantor |

Cross-Default | ||||

Events of default | Triggers default if other financial debt defaults. | Common but transaction-specific | Borrower should seek thresholds, grace periods and cross-acceleration rather than cross-default. | Borrower |

Insolvency Default | ||||

Events of default | Triggers default if borrower becomes unable to pay debts or insolvent. | Usually essential | Use UK statutory insolvency concepts carefully and include relevant overseas equivalents. | Borrower and lender |

Insolvency Proceedings Default | ||||

Events of default | Triggers default on administration, liquidation, receivership or similar proceedings. | Usually essential | Include moratorium, restructuring plan and creditor action where relevant. | Borrower and lender |

Creditor Process Default | ||||

Events of default | Triggers default if enforcement action is taken against borrower assets. | Common but transaction-specific | Use monetary thresholds and cure periods for disputed or minor claims. | Borrower |

Unlawfulness And Invalidity Default | ||||

Events of default | Triggers default if obligations become unlawful, invalid or unenforceable. | Usually essential | Coordinate with illegality prepayment and sanctions provisions. | All parties |

Repudiation And Rescission Default | ||||

Events of default | Triggers default if an obligor rejects or challenges finance documents. | Common but transaction-specific | Useful where guarantors or security providers might dispute obligations. | Borrower and guarantor |

Cessation Of Business Default | ||||

Events of default | Triggers default if the borrower stops carrying on material business. | Common but transaction-specific | Qualify by materiality and permit disposals or reorganisations allowed by the agreement. | Borrower |

Audit Qualification Default | ||||

Events of default | Triggers default if auditors qualify accounts in a serious way. | Optional | Limit to going concern or material adverse qualifications, not technical notes. | Borrower |

Material Adverse Change | ||||

Events of default | Allows action if a serious adverse change affects credit risk. | Common but transaction-specific | Often resisted by borrowers due to uncertainty define objective limbs if possible. | Borrower and lender |

Acceleration | ||||

Events of default | Allows lender to declare amounts immediately due after default. | Usually essential | State notice mechanics, automatic acceleration events and cancellation effects. | Borrower and lender |

Enforcement | ||||

Security and guarantees | Sets when and how lender may enforce rights, security and guarantees. | Usually essential | Secured enforcement may involve insolvency, receivership and security document rules. | Borrower, guarantor and lender |

Illegality | ||||

Repayment and payment mechanics | Allows cancellation or prepayment if lending becomes unlawful. | Usually essential | Include lender notification, mitigation and affected-lender mechanics. | Borrower and lender |

Mitigation | ||||

Boilerplate | Requires affected finance parties to reduce avoidable costs or adverse effects. | Common but transaction-specific | Relevant to tax gross-up, increased costs, illegality and market disruption. | Lender |

Indemnities | ||||

Interest and fees | Protects lender against specified losses linked to the facility. | Usually essential | Define covered losses, exclusions, evidence requirements and mitigation. | Borrower |

Facility Agent Provisions | ||||

Boilerplate | Sets the agent's role, duties and protections in syndicated lending. | Common but transaction-specific | Important only where multiple lenders participate define instructions and liability limits. | Agent and lenders |

Majority Lender Decisions | ||||

Boilerplate | Sets lender voting thresholds for consents, waivers and amendments. | Common but transaction-specific | Reserve all-lender consent for economics, maturity, security releases and core terms. | Borrower and lenders |

Pro Rata Sharing | ||||

Boilerplate | Ensures lenders share recoveries proportionately in syndicated facilities. | Common but transaction-specific | Coordinate with set-off, enforcement proceeds and intercreditor arrangements. | Lenders |

Assignments And Transfers By Lenders | ||||

Boilerplate | Allows lenders to transfer or assign rights to new finance parties. | Common but transaction-specific | Borrower may seek consent rights, transfer restrictions and tax cost protection. | Borrower and lenders |

No Assignment By Borrower | ||||

Boilerplate | Prevents borrower transferring obligations without lender consent. | Usually essential | Consider permitted reorganisations or successor borrowers if group structure may change. | Borrower |

Confidentiality | ||||

Boilerplate | Protects confidential commercial, financial and transaction information. | Usually essential | Allow disclosures to regulators, affiliates, advisers, transferees and credit insurers. | All parties |

Data Protection | ||||

Boilerplate | Allocates obligations for personal data used in credit administration and KYC. | Common but transaction-specific | UK GDPR and Data Protection Act 2018 may apply to personal guarantor and beneficial owner data. | All parties |

Notices | ||||

Boilerplate | Sets how formal communications are given and deemed received. | Usually essential | Include email rules, deemed receipt times and address update mechanics. | All parties |

Electronic Communications | ||||

Boilerplate | Permits notices, documents and instructions to be sent electronically. | Common but transaction-specific | Clarify authorised email addresses, platform use and cyber-risk allocation. | All parties |

Amendments And Waivers | ||||

Boilerplate | Sets how the agreement can be changed or rights waived. | Usually essential | Require written agreement and specify lender consent thresholds in syndicated deals. | All parties |

Cumulative Remedies | ||||

Boilerplate | Confirms rights and remedies are additional, not exclusive. | Usually essential | Supports enforcement flexibility but cannot override mandatory law. | Lender |

No Waiver | ||||

Boilerplate | Prevents delay or partial exercise from waiving rights. | Usually essential | Still use express reservation of rights when managing defaults. | Lender |

Severability | ||||

Boilerplate | Keeps the agreement effective if one provision is invalid. | Usually essential | May not save a commercially essential invalid provision consider replacement wording. | All parties |

Counterparts | ||||

Boilerplate | Allows parties to sign separate copies of the same agreement. | Usually essential | Useful for remote completion and multi-party facilities. | All parties |

Electronic Signatures | ||||

Boilerplate | Allows execution using electronic signatures where legally valid. | Optional | Extra care is needed for deeds, witnesses and registrable security documents. | All parties |

Execution As A Deed | ||||

Boilerplate | Ensures deed execution where required for guarantees or security. | Specialist advice recommended | Companies Act 2006 section 44 governs company execution of documents. | Borrower, guarantor and lender |

Third Party Rights | ||||

Boilerplate | Controls whether non-parties can enforce terms. | Usually essential | Usually excludes the Contracts (Rights of Third Parties) Act 1999 or grants limited rights. | All parties and finance parties |

Entire Agreement | ||||

Boilerplate | Confirms the written agreement supersedes prior negotiations and understandings. | Usually essential | Cannot exclude fraud consider carve-outs for fee letters and security documents. | All parties |

Governing Law | ||||

Boilerplate | States which law governs the agreement. | Usually essential | UK facility agreements often choose English law check security law separately. | All parties |

Jurisdiction | ||||

Boilerplate | Identifies courts that may hear disputes. | Usually essential | Choose exclusive or non-exclusive jurisdiction consider enforcement abroad. | All parties |

Arbitration | ||||

Boilerplate | Refers disputes to private arbitration instead of courts. | Optional | Less common for standard UK bank lending consider enforcement and interim remedies. | All parties |

Process Agent | ||||

Boilerplate | Appoints a UK agent to receive legal proceedings for overseas parties. | Common but transaction-specific | Important for non-UK borrowers or guarantors in English-law facilities. | Overseas borrower or guarantor |

Service Of Process | ||||

Boilerplate | Sets agreed methods for serving court documents. | Common but transaction-specific | Must be consistent with court rules and any process agent appointment. | All parties |

Consumer Credit And Regulatory Status | ||||

Other | Addresses whether the facility is regulated credit or exempt lending. | Specialist advice recommended | Consumer Credit Act and FCA perimeter issues can affect enforceability and authorisation. | Lender and borrower |

FCA Authorisation | ||||

Other | Confirms any required regulatory permissions for lending activities. | Specialist advice recommended | Regulated lending without permission can create serious regulatory and enforceability risk. | Lender |

Hedging Arrangements | ||||

Other | Requires or permits hedging of interest rate, currency or commodity risk. | Optional | Coordinate with security, intercreditor ranking, close-out amounts and FCA issues. | Borrower and hedge providers |

Intercreditor Arrangements | ||||

Security and guarantees | Regulates priority, enforcement and turnover between creditor classes. | Specialist advice recommended | Essential where senior, mezzanine, shareholder or hedging debt co-exist. | Lenders, borrower and other creditors |

Subordination | ||||

Security and guarantees | Ranks one creditor's claims behind another's claims. | Specialist advice recommended | Use payment blockage, turnover and insolvency wording coordinate with intercreditor terms. | Subordinated creditors and senior lender |

Release Of Security And Guarantees | ||||

Security and guarantees | Sets when collateral and guarantees are released. | Usually essential | Define full discharge, permitted disposals, refinancing release and Companies House filings. | Borrower, guarantor and lender |

Default Cure Rights | ||||

Events of default | Allows borrower to remedy certain breaches before lender enforcement. | Common but transaction-specific | Specify cure period, eligible defaults and whether repeated cures are limited. | Borrower and lender |

Equity Cure | ||||

Covenants | Allows shareholder funds to cure financial covenant breaches. | Optional | Negotiate frequency, amount, EBITDA treatment and mandatory prepayment use. | Borrower, shareholders and lender |

Margin Ratchet | ||||

Interest and fees | Adjusts margin based on leverage, rating or other performance metrics. | Optional | Tie changes to compliance certificates and specify when adjustments take effect. | Borrower and lender |

Sustainability Linked Loan Provisions | ||||

Other | Links pricing or reporting to agreed sustainability performance targets. | Optional | Targets should be measurable, ambitious and supported by reporting and verification. | Borrower and lender |

Funding Rate Confidentiality | ||||

Interest and fees | Protects lender funding cost information used in rate calculations. | Optional | Balance lender confidentiality with borrower verification rights for costs claimed. | Borrower and lender |

What Clauses Matter Most In A UK Facility Agreement?

A UK facility agreement is not just a statement of loan amount and interest. The most important clauses usually define the facility, purpose, availability, repayment, interest, fees, representations, covenants, events of default and enforcement rights. If these clauses are vague, the parties may disagree about when funds must be advanced, when repayment is due, or when the lender can accelerate the debt.

Which Facility Agreement Clauses Need The Most Care?

- Security, guarantees and priority clauses need careful drafting because enforceability often depends on company law, registration requirements and insolvency priority rules in the UK.

- Financial covenants, information undertakings and events of default are heavily negotiated because they control how early the lender can intervene if the borrower\'s risk profile changes.

- Interest, default interest, fees and break costs should be clear and commercially justifiable to reduce disputes over calculation and enforceability.

- Illegality, sanctions, tax gross-up, FATCA/CRS and anti-money laundering provisions are especially important where lenders, borrowers or payments cross borders.

When Is Specialist Advice Recommended?

Specialist UK legal advice is strongly recommended for secured lending, syndicated lending, regulated consumer or SME credit, real estate finance, acquisition finance, project finance and any agreement involving guarantees, debentures, intercreditor arrangements or cross-border tax and sanctions issues.

Want to Generate Your own Facility Agreement?

Docaro AI can help you write your own Facility Agreement for use in the United Kingdom in minutes.

FAQs

A Facility Agreement is a legal contract setting out the terms of a loan or line of credit, including the amount available, interest, repayment terms, fees, security, and default provisions.

Show All FAQs

You Might Also Be Interested In

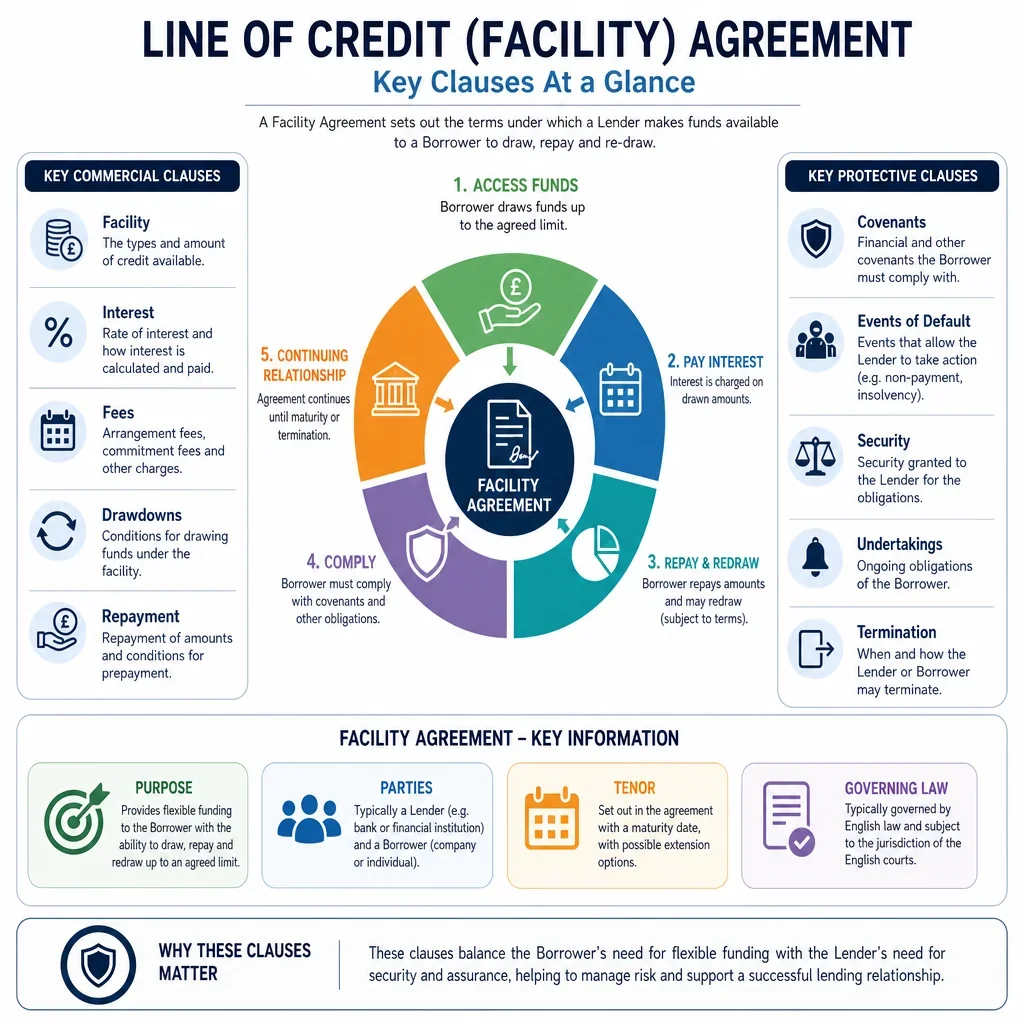

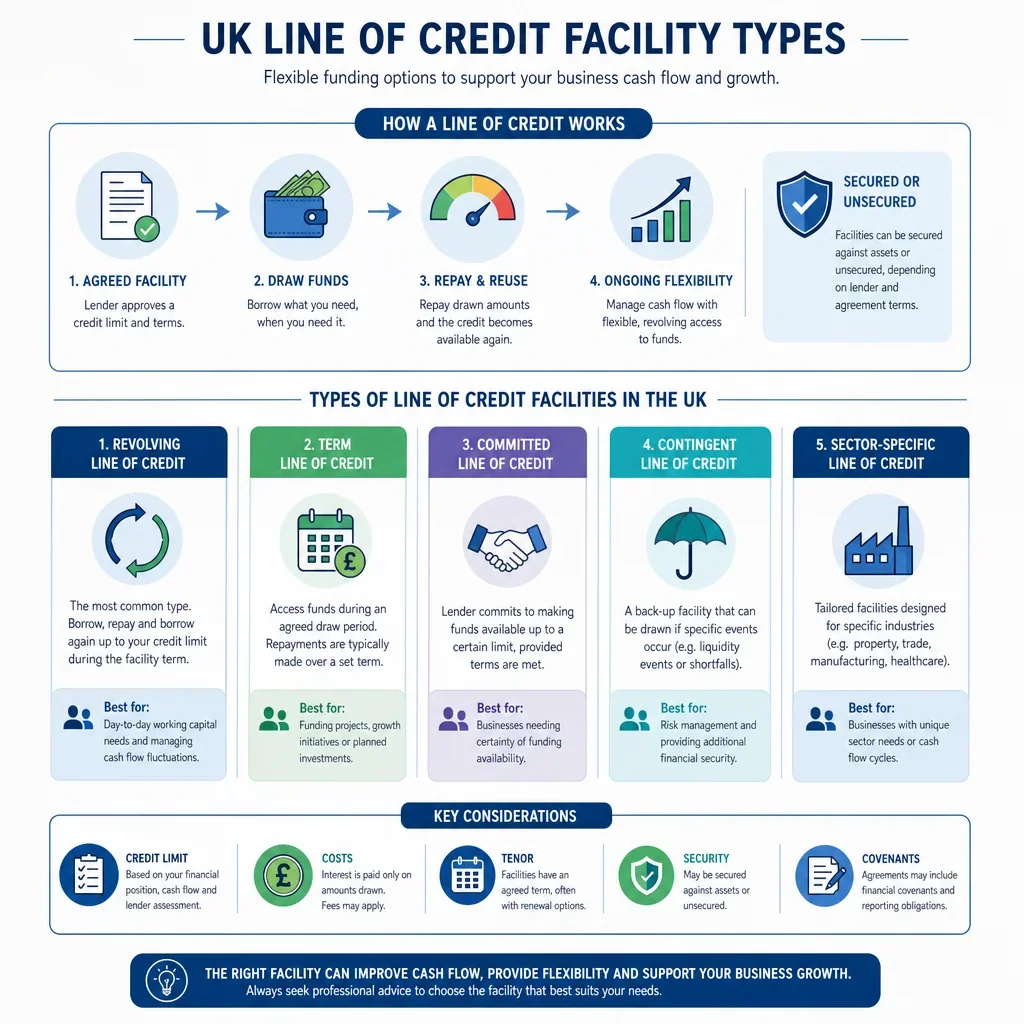

UK line of credit facility types explained for borrowers, lenders and advisers comparing flexible finance options.

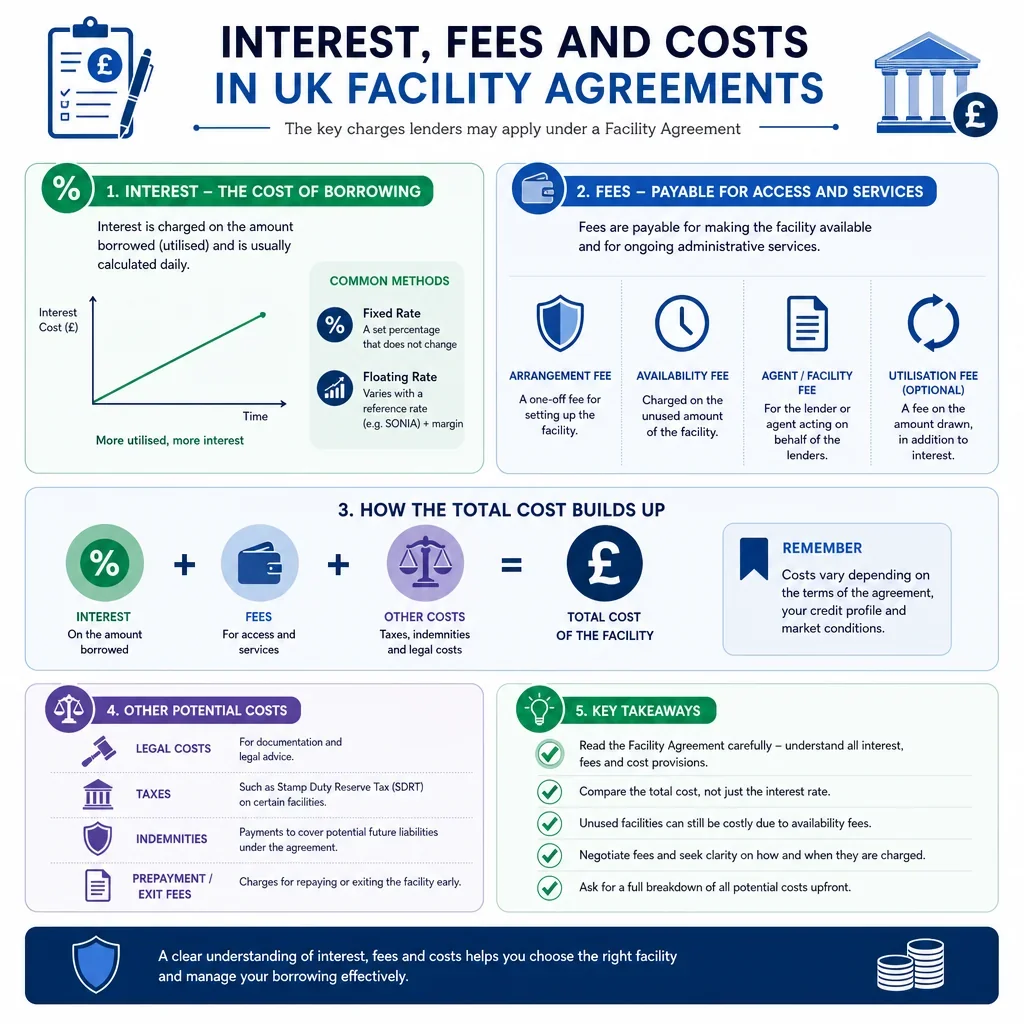

Understand interest, fees and costs in UK facility agreements, including key terms, borrower obligations and common risks.

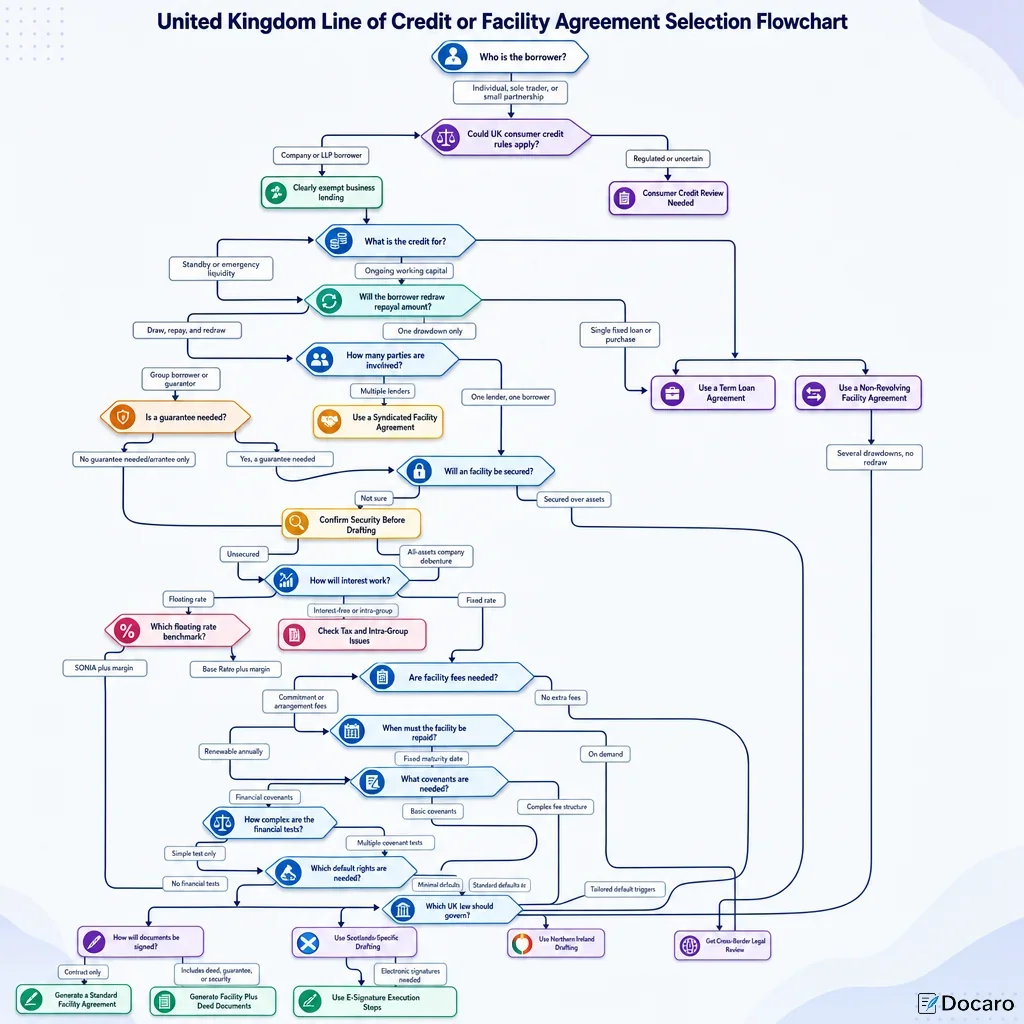

United Kingdom flowchart to choose the right line of credit or facility agreement for your financing needs.

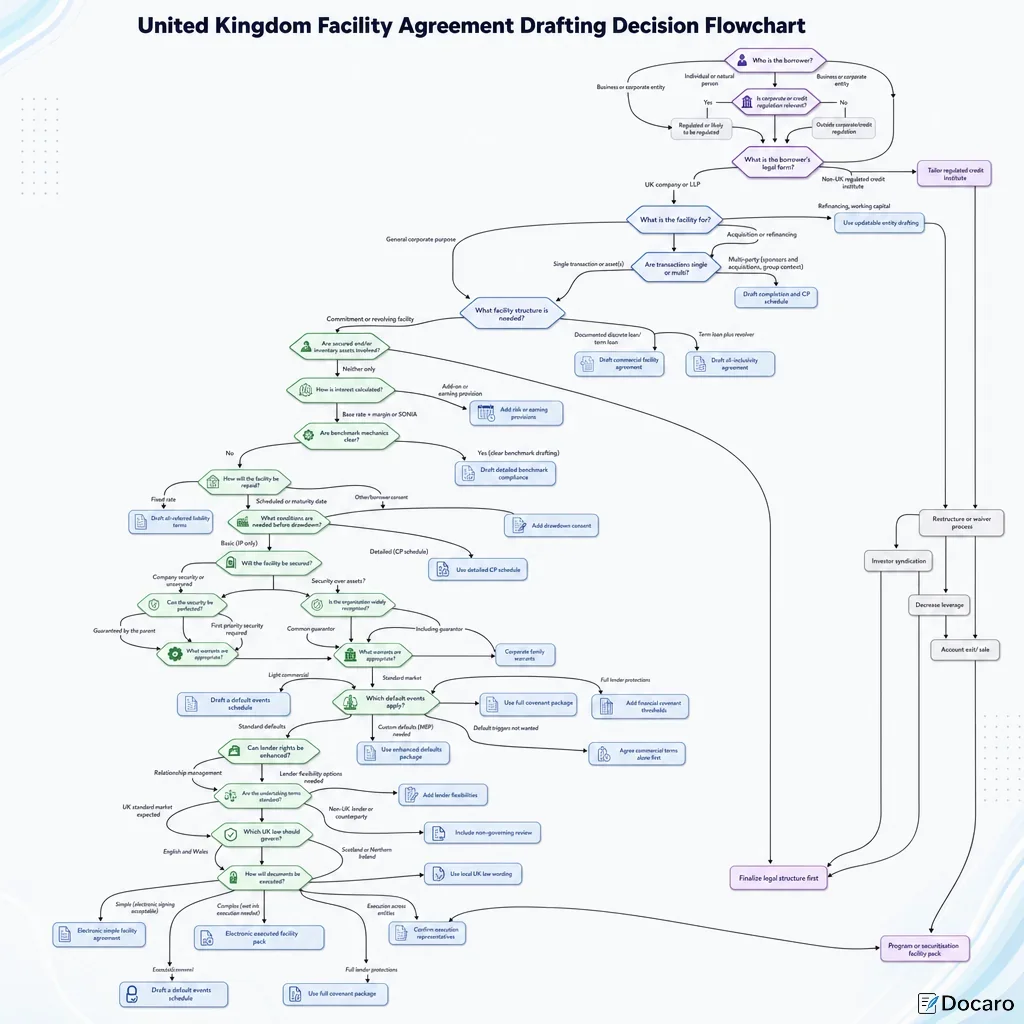

Use this United Kingdom facility agreement flowchart to choose drafting steps, key clauses, and lender-borrower options with confidence.