Interest Fees And Costs In UK Facility Agreements

Created:

This article explains key interest, fee and cost provisions in UK facility agreements, helping readers assess borrowing terms, risks and obligations. It is part of the AI Generated British Facility Agreement category.

Cost Type | Calculation Basis | Payment Timing | Paying Party | Practical Note |

|---|---|---|---|---|

SONIA-linked interest | ||||

Interest | Compounded SONIA plus margin over each interest period. | Periodic | Borrower. | Standard for many sterling floating-rate facilities needs clear observation shift and lookback mechanics. |

Bank Rate linked interest | ||||

Interest | Bank of England Bank Rate plus margin. | Periodic | Borrower. | Simpler than compounded SONIA but may be less common for larger corporate loans. |

Fixed rate interest | ||||

Interest | Fixed annual percentage on outstanding principal. | Periodic | Borrower. | Gives certainty but may include break costs if repaid early. |

Interest margin | ||||

Interest | Agreed percentage added to benchmark or base rate. | Periodic | Borrower. | Main pricing lever may step up or down by leverage or credit rating. |

Margin ratchet adjustment | ||||

Interest | Margin changes by leverage, loan-to-value or performance thresholds. | Periodic | Borrower. | Can reward deleveraging but increases cost if covenants deteriorate. |

Interest rate floor | ||||

Interest | Benchmark deemed not less than agreed floor, often zero. | Periodic | Borrower. | Protects lender yield borrower may not benefit fully from falling rates. |

Default interest | ||||

Default interest | Normal interest plus default margin on overdue amounts. | On default | Defaulting borrower or obligor. | Must be commercially justifiable to reduce penalty risk. |

Capitalised default interest | ||||

Default interest | Unpaid default interest added to principal at agreed intervals. | On default | Defaulting borrower or obligor. | Can rapidly increase debt compounding periods should be explicit. |

Arrangement fee | ||||

Arrangement fee | Fixed amount or percentage of total commitments. | Upfront | Borrower. | Often non-refundable and payable whether or not the facility is fully drawn. |

Upfront fee | ||||

Arrangement fee | Percentage of each lender's commitment or fixed fee letter amount. | Upfront | Borrower. | May be documented in a confidential fee letter rather than the facility agreement. |

Commitment fee | ||||

Commitment fee | Percentage of undrawn available commitments accruing daily. | Periodic | Borrower. | Charges for committed but unused credit affects revolving facilities significantly. |

Ticking fee | ||||

Commitment fee | Percentage of commitments accruing before first drawdown or closing. | Periodic | Borrower. | Compensates lenders for reserving funds during delayed completion periods. |

Utilisation fee | ||||

Utilisation fee | Percentage of drawn amount, often increasing with utilisation level. | Periodic | Borrower. | Discourages high usage of revolving credit lines. |

Drawdown fee | ||||

Other | Fixed fee or percentage charged per utilisation request. | On each utilisation | Borrower. | Can make frequent small drawings inefficient. |

Rollover fee | ||||

Other | Fixed amount per rollover or renewal of a loan period. | On each utilisation | Borrower. | Relevant where short interest periods are repeatedly renewed. |

Agent fee | ||||

Other | Annual fixed fee under agency or fee letter. | Periodic | Borrower. | Common in syndicated facilities for administering lender communications and payments. |

Security agent fee | ||||

Other | Annual fixed fee or fee letter amount. | Periodic | Borrower or chargor group. | Relevant where security is held on trust for multiple finance parties. |

Agent expenses | ||||

Other | Properly incurred out-of-pocket expenses plus VAT if applicable. | On demand | Borrower. | Borrower should require reasonable evidence and scope limits. |

Lender legal fees | ||||

Legal cost | Reasonable legal costs incurred in negotiation and completion. | Upfront | Borrower. | Often capped for initial documentation but uncapped for enforcement. |

Amendment legal fees | ||||

Legal cost | Reasonable costs for waivers, consents or amendments. | On demand | Borrower requesting change. | Small covenant or timing changes can still trigger lender counsel costs. |

Enforcement legal costs | ||||

Legal cost | Costs of enforcing finance documents after default. | On default | Defaulting borrower, guarantor or security provider. | Usually broad and may include court, insolvency and receiver costs. |

Break costs | ||||

Break cost | Lender loss from repayment before interest period end. | On early repayment | Borrower making early repayment. | Most relevant for fixed-rate or term benchmark funding. |

Prepayment fee | ||||

Other | Percentage of amount prepaid or declining fee schedule. | On early repayment | Borrower. | Can restrict refinancing flexibility distinguish from break costs. |

Make-whole amount | ||||

Break cost | Discounted value of lost future interest or yield. | On early repayment | Borrower. | Can be substantial in private credit and fixed-yield loans. |

Commitment cancellation fee | ||||

Commitment fee | Fee on cancelled undrawn commitments. | On early repayment | Borrower cancelling commitment. | May apply where lenders reserved capacity for a minimum period. |

Extension fee | ||||

Other | Fixed amount or percentage of extended commitments. | Other | Borrower requesting extension. | Often payable when maturity or availability period is extended. |

Waiver fee | ||||

Other | Fixed fee or percentage agreed for covenant waiver. | On demand | Borrower or relevant obligor. | Can be a hidden cost of covenant pressure or late reporting. |

Consent fee | ||||

Other | Fee payable for lender consent to restricted action. | On demand | Borrower seeking consent. | May apply to acquisitions, disposals, dividends or debt changes. |

Valuation costs | ||||

Other | Valuer fees for initial and updated asset valuations. | Upfront | Borrower or security provider. | Important for real estate, asset finance and borrowing base facilities. |

Revaluation costs | ||||

Other | Costs of periodic or event-driven collateral revaluations. | Periodic | Borrower or security provider. | Can be triggered by covenant breaches or market value concerns. |

Due diligence costs | ||||

Other | Accountant, tax, commercial or technical adviser costs. | Upfront | Borrower or sponsor. | Common in acquisition, project and leveraged finance transactions. |

Monitoring costs | ||||

Other | Costs of lender-appointed monitoring accountant or adviser. | Periodic | Borrower. | Usually negotiated to apply after default or financial underperformance. |

Borrowing base audit costs | ||||

Other | Field exam or audit costs for receivables and inventory. | Periodic | Borrower. | Key cost in asset-based lending frequency should be capped if no default. |

Security registration fees | ||||

Other | Companies House or registry fees for registering security. | Upfront | Chargor or borrower. | UK company charges generally require timely registration to protect security priority. |

Land Registry fees | ||||

Other | Prescribed fee for registering legal charge or land transaction. | Upfront | Borrower or property owner. | Relevant for real estate security and may affect completion funds flow. |

IP security registration costs | ||||

Other | IPO filing fees and adviser costs for registered IP security. | Upfront | Borrower or IP owner. | Important where patents, trade marks or designs are key collateral. |

Special asset registry fees | ||||

Other | Registry and professional fees for ships, aircraft or specialist assets. | Upfront | Borrower or asset owner. | Asset-specific registration can be critical to lender security perfection. |

Stamp taxes on transfers | ||||

Other | Statutory tax if loan security or enforcement involves chargeable transfers. | Other | Usually borrower under tax indemnity if finance-related. | Usually not charged on simple loan advances but may arise on share transfers. |

SDLT funding tax costs | ||||

Other | Statutory land transaction tax where relevant property transfers occur. | Other | Buyer or borrower under transaction documents. | Facility funding should account for SDLT where proceeds finance land acquisition. |

VAT on fees and costs | ||||

Other | VAT added to taxable services at applicable rate. | On demand | Borrower if costs clause is VAT-inclusive or reimbursable. | Interest is generally exempt, but legal and adviser fees may carry VAT. |

UK withholding tax gross-up | ||||

Other | Additional amount so lender receives net scheduled payment. | On demand | Borrower unless exemption or treaty process applies. | Critical for cross-border lending qualifying lender status should be checked. |

Tax indemnity payment | ||||

Other | Indemnifies finance party for tax cost from finance documents. | On demand | Borrower or obligors. | Borrowers negotiate exclusions for lender taxes and avoidable tax costs. |

FATCA deduction cost | ||||

Other | Gross-up or indemnity for FATCA-related withholding if agreed. | On demand | Allocated by FATCA clause often borrower only in limited cases. | Parties should align drafting with lender status and information obligations. |

Increased costs | ||||

Other | Additional regulatory or capital cost attributable to the facility. | On demand | Borrower, subject to exclusions. | Borrowers often seek exclusions for known rules and lender-specific costs. |

Capital adequacy cost | ||||

Other | Cost from regulatory capital or liquidity requirements. | On demand | Borrower if covered by increased costs clause. | May arise from banking regulation changes affecting lender economics. |

Market disruption cost | ||||

Interest | Alternative funding cost if benchmark does not reflect lender cost. | Periodic | Borrower. | Should have objective triggers and lender certification requirements. |

Benchmark replacement adjustment | ||||

Interest | Spread or adjustment applied when benchmark changes. | Periodic | Borrower through adjusted interest rate. | Fallback wording reduces uncertainty after LIBOR transition or benchmark cessation. |

Late payment administration fee | ||||

Default interest | Fixed fee for missed or late payment processing. | On default | Borrower in payment default. | Should reflect administration cost and not duplicate default interest unfairly. |

Returned payment fee | ||||

Other | Fixed fee for rejected direct debit, CHAPS or transfer. | On default | Borrower. | Operational fee should be proportionate and clearly stated. |

Payment transfer fees | ||||

Other | Bank charges for CHAPS, SWIFT or other transfers. | On each utilisation | Borrower or party initiating transfer. | Small but relevant for multi-currency or frequent drawdown facilities. |

Currency conversion cost | ||||

Other | FX spread, conversion charge or loss on currency mismatch. | On each utilisation | Borrower requiring non-sterling funds. | Important where sterling borrower draws or repays in another currency. |

Currency indemnity | ||||

Other | Indemnity for shortfall after judgment or payment currency conversion. | On demand | Borrower or obligor. | Protects lender if recovered currency differs from facility currency. |

Funding loss indemnity | ||||

Break cost | Lender loss from failed drawdown, late payment or early repayment. | On demand | Borrower causing loss. | Covers costs even where no loan is ultimately advanced. |

Failed utilisation costs | ||||

Break cost | Costs incurred after borrower cancels or fails conditions for drawdown. | On each utilisation | Borrower requesting utilisation. | Borrower should avoid submitting drawdown notices before conditions are certain. |

Conditions precedent costs | ||||

Legal cost | Costs of reviewing CP documents and completion deliverables. | Upfront | Borrower. | Delays in CP delivery can increase lawyer and adviser time costs. |

Accession costs | ||||

Legal cost | Legal and filing costs for new obligor or guarantor accession. | On demand | Borrower group. | Relevant where group structure changes after signing. |

Security release costs | ||||

Legal cost | Costs of releases, DS1 forms, filings and counsel review. | On early repayment | Borrower or security provider. | Should be budgeted when refinancing or selling secured assets. |

Receiver costs | ||||

Other | Receiver remuneration and expenses from secured assets or indemnity. | On default | Security provider or charged assets. | Crystallises during enforcement and can materially reduce recoveries. |

Insolvency practitioner costs | ||||

Other | Administrator, liquidator or adviser remuneration and expenses. | On default | Insolvent estate, borrower or secured assets. | Relevant after enforcement or insolvency event priority affects recoveries. |

Court fees | ||||

Legal cost | Prescribed fees for issuing or progressing claims. | On default | Initially claimant lender recoverable if ordered or indemnified. | Relevant where debt recovery or security enforcement requires proceedings. |

Litigation costs | ||||

Legal cost | Solicitor, barrister, expert and process server costs. | On default | Defaulting obligor if indemnity applies or court orders. | Indemnity wording can affect recoverability beyond normal litigation cost rules. |

Insurance premium costs | ||||

Other | Premiums for required asset, title, credit or key person insurance. | Periodic | Borrower or asset owner. | Failure to maintain insurance may trigger default or lender step-in costs. |

Lender-placed insurance | ||||

Other | Premiums and costs incurred if borrower fails to insure collateral. | On demand | Borrower or security provider. | Often more expensive than borrower-arranged cover. |

Environmental report costs | ||||

Other | Consultant fees for environmental due diligence or remediation review. | Upfront | Borrower or property owner. | Common in property, energy, infrastructure and industrial asset lending. |

Survey costs | ||||

Other | Surveyor fees for building, quantity or condition reports. | Upfront | Borrower or property owner. | May be condition precedent to real estate or development finance drawdown. |

Project monitor fees | ||||

Other | Monitoring surveyor or technical adviser fees during project. | Periodic | Borrower or developer. | Can be payable before each development finance drawdown. |

Account bank fees | ||||

Other | Account opening, maintenance, escrow or blocked account fees. | Periodic | Borrower or account holder. | Relevant where cash controls or secured accounts are required. |

Hedging costs | ||||

Other | Swap premiums, margins, collateral costs or ISDA charges. | Periodic | Borrower or hedge counterparty customer. | May be mandatory to manage floating rate or FX exposure. |

Hedge breakage costs | ||||

Break cost | Close-out or termination amount under hedging documents. | On early repayment | Borrower if hedge is terminated in-the-money for bank. | Early loan repayment may require expensive swap termination. |

Negative carry cost | ||||

Break cost | Loss from lender funding before delayed or cancelled utilisation. | On demand | Borrower if delay is borrower-caused. | Important for underwritten acquisition facilities with uncertain closing dates. |

Letter of credit commission | ||||

Utilisation fee | Percentage of outstanding LC face amount. | Periodic | Applicant borrower. | Applies where facility includes ancillary or guarantee instruments. |

Issuing bank fee | ||||

Other | Fixed fee or percentage for issuing LC or bank guarantee. | On each utilisation | Applicant borrower. | Separate from lender margin and LC commission. |

LC reimbursement amount | ||||

Other | Amount paid by issuing bank under LC or guarantee. | On demand | Applicant borrower or account party. | Often becomes immediately repayable debt after a beneficiary drawing. |

Ancillary facility charges | ||||

Other | Overdraft, card, bonding or treasury service charges. | Periodic | Borrower using ancillary facility. | Pricing may sit in separate ancillary documents rather than main agreement. |

Ancillary overdraft interest | ||||

Interest | Agreed overdraft rate on daily overdrawn balance. | Periodic | Borrower using overdraft. | Can differ from main revolving loan pricing. |

Mandatory prepayment costs | ||||

Break cost | Break costs and fees triggered by required prepayment event. | On early repayment | Borrower receiving disposal, insurance or excess cash proceeds. | Mandatory prepayments can still carry funding loss costs. |

Change of control prepayment costs | ||||

Break cost | Prepayment, break and accrued interest on change of control. | On early repayment | Borrower or target group. | Should be factored into sale, investment and restructuring transactions. |

Accrued interest on repayment | ||||

Interest | Interest accrued to repayment or prepayment date. | On early repayment | Borrower repaying loan. | Payable in addition to principal and any prepayment premium. |

Default costs indemnity | ||||

Other | Indemnity for losses and costs arising from event of default. | On default | Defaulting obligor or borrower group. | May overlap with legal costs, default interest and enforcement expenses. |

Information breach costs | ||||

Other | Costs incurred due to late accounts, certificates or notices. | On default | Borrower or reporting obligor. | May trigger waiver fees, monitoring costs and default interest risk. |

Compliance review costs | ||||

Other | Accountant or adviser review of covenant compliance. | Periodic | Borrower if required or after breach. | Negotiate when external verification is required and who pays. |

Debt service account shortfall cost | ||||

Default interest | Default interest or fees on failure to fund reserve account. | On default | Borrower required to maintain reserve. | Relevant in project, real estate and acquisition finance structures. |

Reserve account funding cost | ||||

Other | Cash trapped or deposited for debt service or maintenance reserve. | Upfront | Borrower or project company. | Not a fee, but reduces borrower liquidity and should be modelled. |

Lender transfer fee | ||||

Other | Fixed administration fee for assignment or transfer processing. | Other | Usually transferring lender sometimes borrower if requested. | Borrowers should check if lender transfers can create borrower-paid costs. |

KYC and onboarding costs | ||||

Other | Administrative and adviser costs for AML, sanctions and identity checks. | Upfront | Borrower or obligor group if agreed. | Delays in KYC can delay utilisation and increase transaction costs. |

Sanctions compliance costs | ||||

Other | Costs of screening, reporting, freezing or compliance actions. | On demand | Borrower if caused by obligor or transaction issue. | Can block payments or drawdowns where sanctions concerns arise. |

Consumer credit compliance costs | ||||

Other | Costs of regulated credit documentation and compliance if applicable. | Upfront | Lender operationally pricing may reflect cost. | Most corporate facilities are unregulated, but individual borrowers need checking. |

Unfair charge risk adjustment | ||||

Other | Review or reduction of consumer charges that may be unfair. | Other | Lender bears enforceability risk borrower may dispute. | Relevant if facility is with an individual acting outside business purposes. |

Penalty clause exposure | ||||

Default interest | Charges assessed against legitimate interest and proportionality. | On default | Drafting risk for lender payment risk for borrower. | Default fees and rates should not be extravagant or unconscionable. |

Notarisation and legalisation costs | ||||

Legal cost | Notary, apostille and embassy legalisation fees. | Upfront | Borrower or relevant obligor. | Common for overseas obligors or foreign law security documents. |

Translation costs | ||||

Legal cost | Certified translation fees for foreign documents or opinions. | Upfront | Borrower or overseas obligor. | Can affect timing where foreign subsidiaries provide guarantees or security. |

Foreign counsel costs | ||||

Legal cost | Local law advice and opinions for overseas obligors or assets. | Upfront | Borrower group. | Material in cross-border UK law facilities with non-UK collateral. |

Legal opinion costs | ||||

Legal cost | Counsel fees for capacity, enforceability or security opinions. | Upfront | Borrower or issuer of opinion. | Often required as a condition precedent for larger or cross-border deals. |

Syndication costs | ||||

Arrangement fee | Arranger fees and expenses for syndicating commitments. | Upfront | Borrower or sponsor. | May include flex rights that alter margin or fees before closing. |

Underwriting fee | ||||

Arrangement fee | Percentage of underwritten commitments. | Upfront | Borrower or sponsor. | Compensates arranger for underwriting risk before syndication completes. |

Participation fee | ||||

Arrangement fee | Fee paid to lenders by commitment tier. | Upfront | Borrower or arranger from fee pool. | Can affect allocation of lender commitments in syndicated facilities. |

Structuring fee | ||||

Arrangement fee | Fixed or percentage fee for designing facility structure. | Upfront | Borrower or sponsor. | Often separate from arrangement and agency fees. |

Bookrunner fee | ||||

Arrangement fee | Fee letter amount for managing lender book and allocation. | Upfront | Borrower or sponsor. | Seen in larger syndicated or club facilities. |

Annual review fee | ||||

Other | Fixed yearly fee for credit review or renewal. | Periodic | Borrower. | Common in smaller business and revolving credit facilities. |

Minimum usage fee | ||||

Commitment fee | Fee if average utilisation falls below agreed threshold. | Periodic | Borrower. | Can make a standby line more expensive than expected. |

Clean-down breach cost | ||||

Default interest | Default interest, waiver fee or costs after failure to clean down. | On default | Revolving facility borrower. | Seasonal businesses should ensure clean-down covenant is realistic. |

Compound interest adjustment | ||||

Interest | Daily non-cumulative or cumulative compounded rate methodology. | Periodic | Borrower. | Calculation method affects actual payable interest under SONIA loans. |

Day count interest effect | ||||

Interest | Actual/365, Actual/360 or other agreed day count convention. | Periodic | Borrower through interest calculation. | Day count choice changes effective annual cost, especially in multi-currency loans. |

Business day adjustment effect | ||||

Interest | Payment dates adjusted by following or modified following convention. | Periodic | Borrower through additional accrual days. | Holiday adjustments can slightly increase or shift interest payments. |

General indemnity costs | ||||

Other | Losses, liabilities and expenses from finance documents or transactions. | On demand | Borrower or obligors. | Borrowers should seek exclusions for lender negligence, misconduct and breach. |

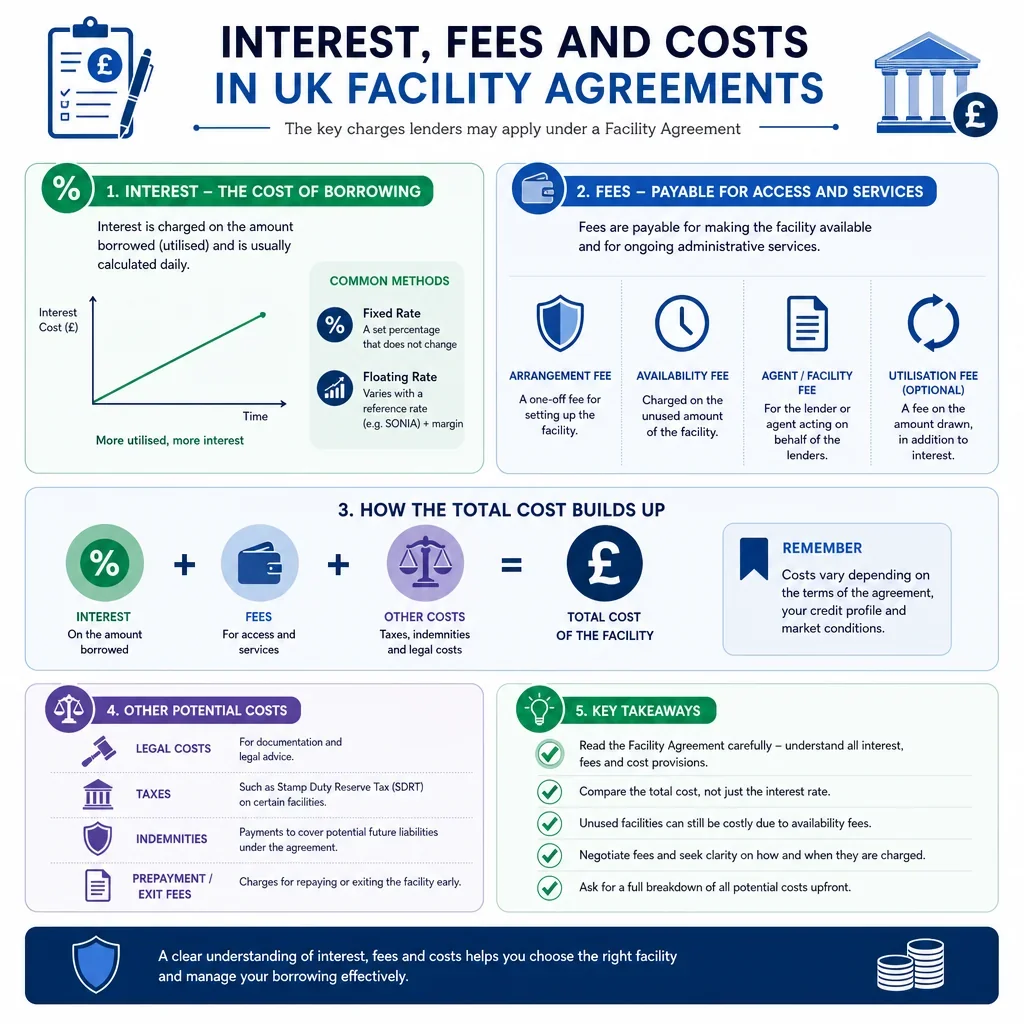

What Interest, Fees And Costs Should A UK Facility Agreement Cover?

A UK facility agreement should state not only the headline interest rate, but also when interest is compounded, how benchmarks are replaced, what fees apply to undrawn or cancelled amounts, and which enforcement and legal costs are recoverable. Borrowers should check the total cost of borrowing across the full facility life, while lenders should ensure fee triggers and cost indemnities are drafted clearly.

Which Charges Most Affect Borrower Cash Flow?

- Margin, SONIA or Bank Rate interest, commitment fees and utilisation fees usually affect recurring cash flow and should be modelled before signing.

- Arrangement, agency, security and valuation fees can create material upfront costs even before the first drawdown.

- Break costs, prepayment fees and cancellation fees can make refinancing or early repayment more expensive than expected.

What Should Borrowers Negotiate In A Facility Agreement?

- Caps, thresholds or reasonableness wording for legal costs, monitoring costs, audit fees and enforcement expenses.

- Clear calculation mechanics for default interest, compounded interest and market disruption costs.

- Whether VAT, stamp taxes, gross-up amounts and increased costs are payable only where properly incurred and evidenced.

Why Do UK Tax And Regulatory Costs Matter?

UK withholding tax, FATCA-related deductions, stamp duty and VAT can change the net economics of a loan. Facility agreements commonly include tax gross-up and indemnity provisions so that the lender receives the intended net amount, subject to negotiated exceptions.

Want to Generate Your own Facility Agreement?

Docaro AI can help you write your own Facility Agreement for use in the United Kingdom in minutes.

FAQs

A UK facility agreement usually sets out the interest rate, how interest is calculated, payment dates, default interest, arrangement fees, commitment fees, legal costs, and any indemnities or break costs.

Show All FAQs

You Might Also Be Interested In

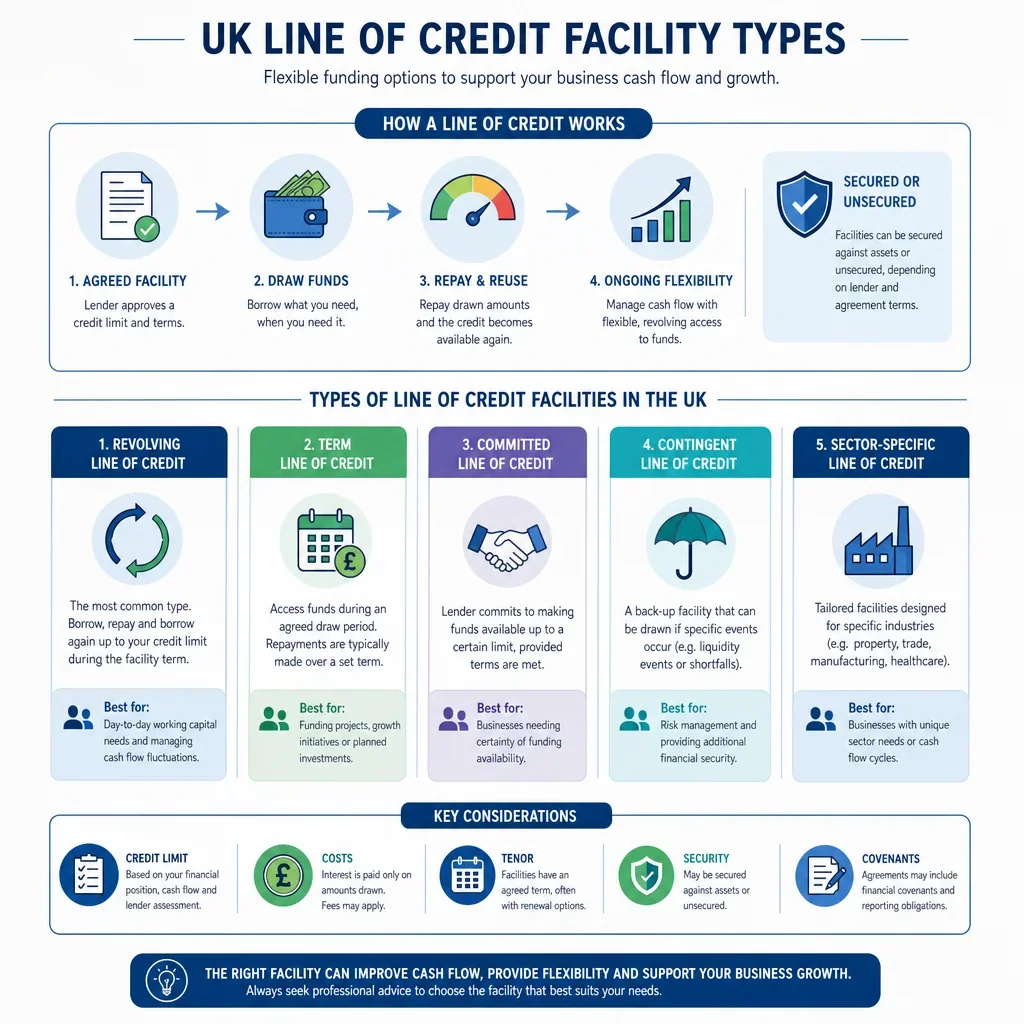

UK line of credit facility types explained for borrowers, lenders and advisers comparing flexible finance options.

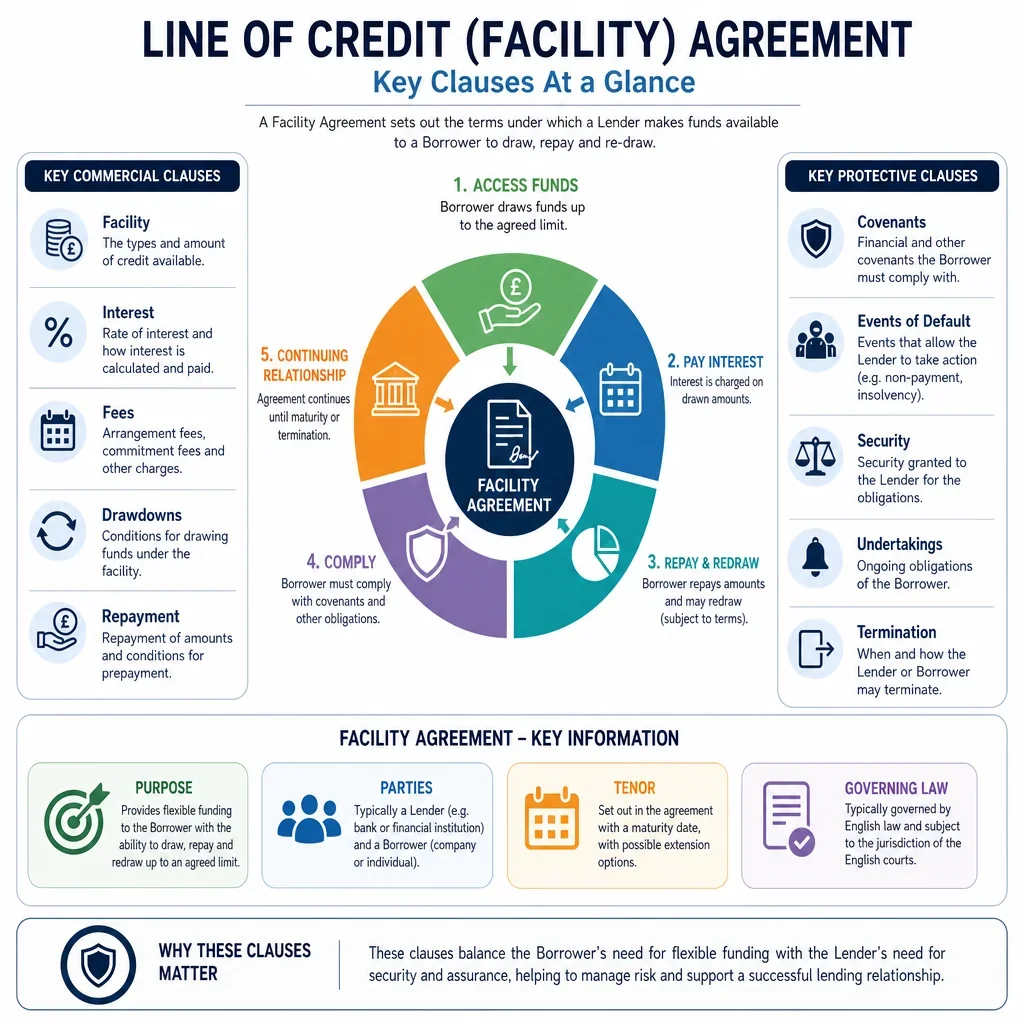

United Kingdom facility agreement clause guide covering key terms, drafting points, and practical insights for better agreements.

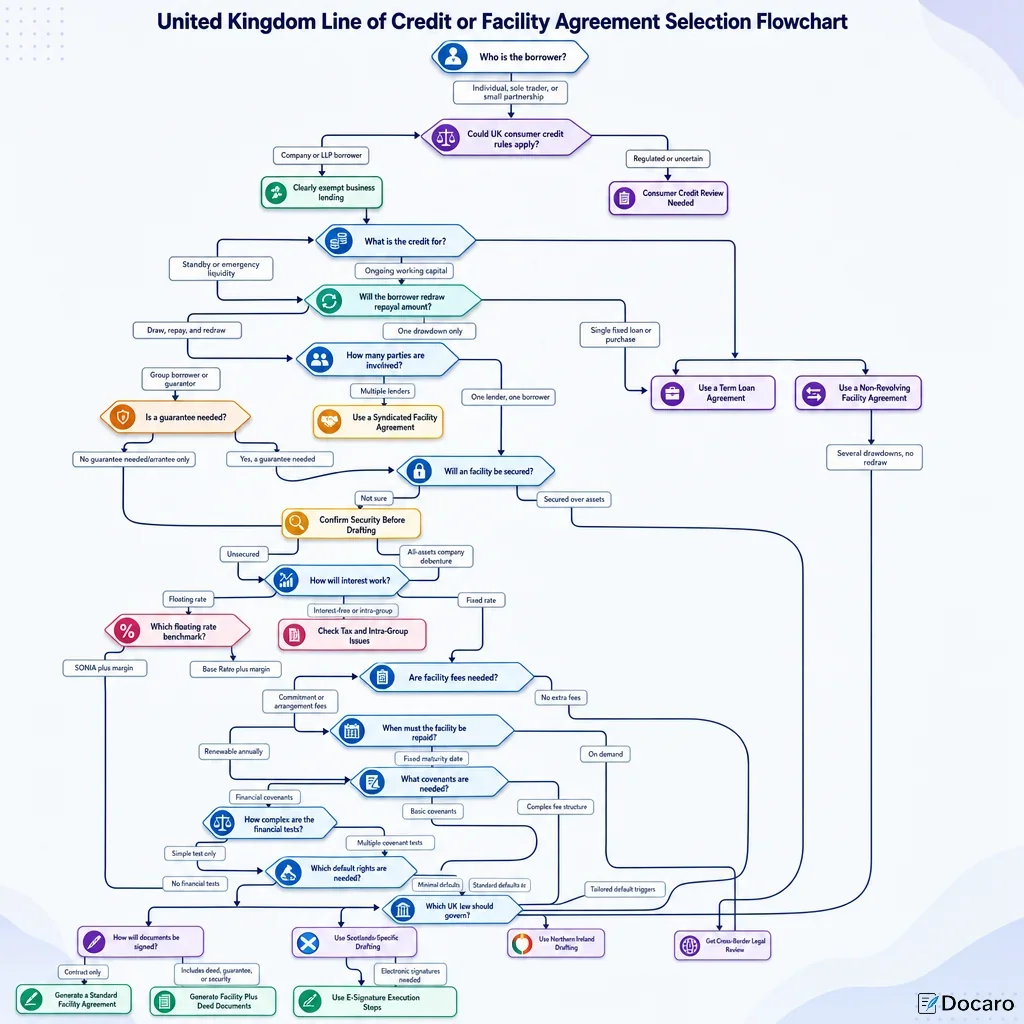

United Kingdom flowchart to choose the right line of credit or facility agreement for your financing needs.

Use this United Kingdom facility agreement flowchart to choose drafting steps, key clauses, and lender-borrower options with confidence.