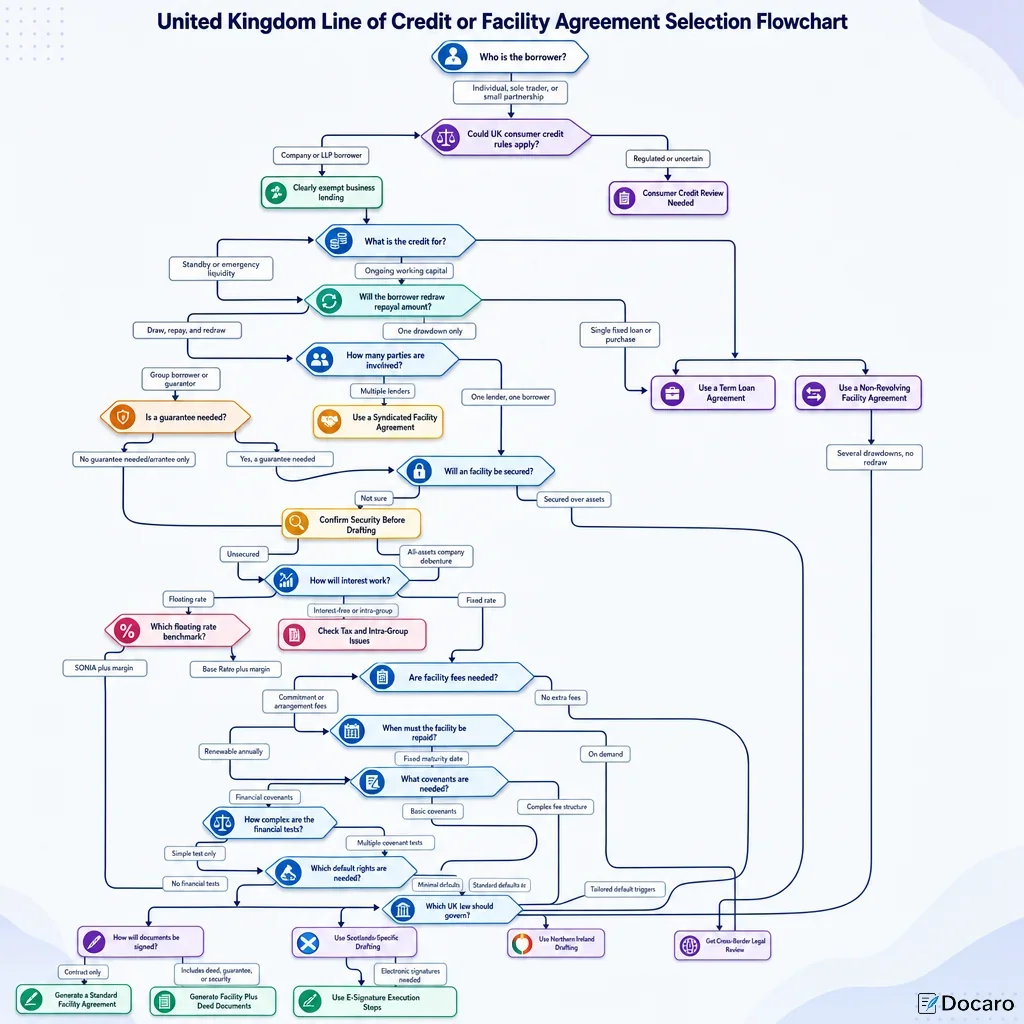

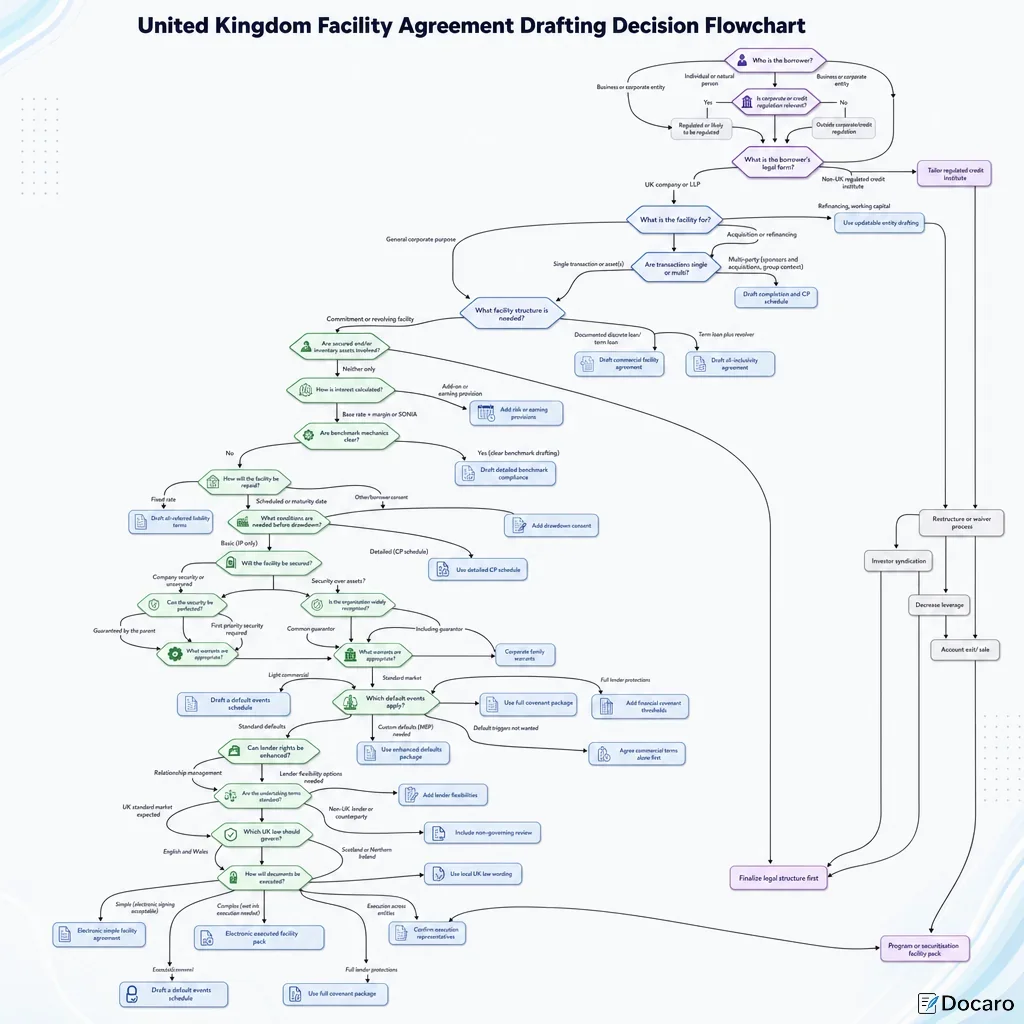

United Kingdom Facility Agreement Drafting Decision Flowchart

Who is the borrower?

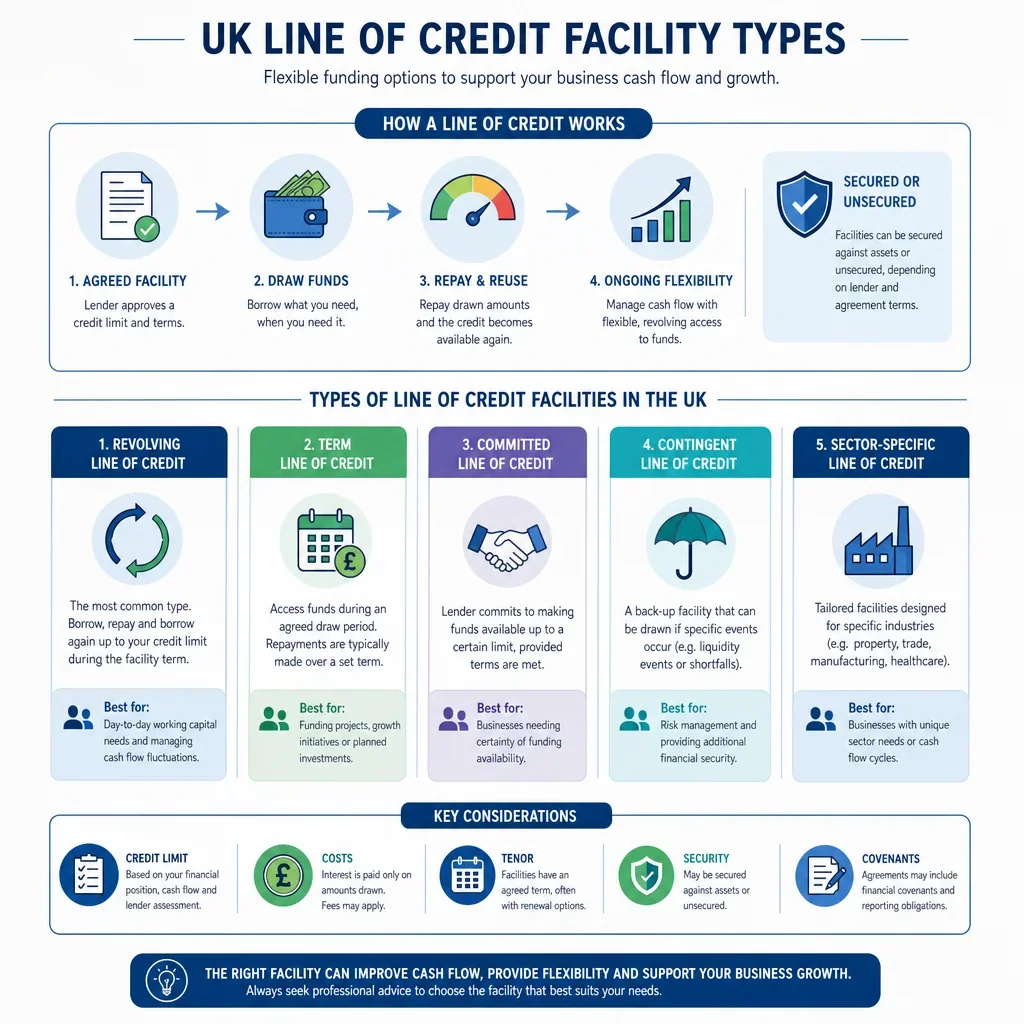

Why Is The Right Facility Agreement Important In The UK?

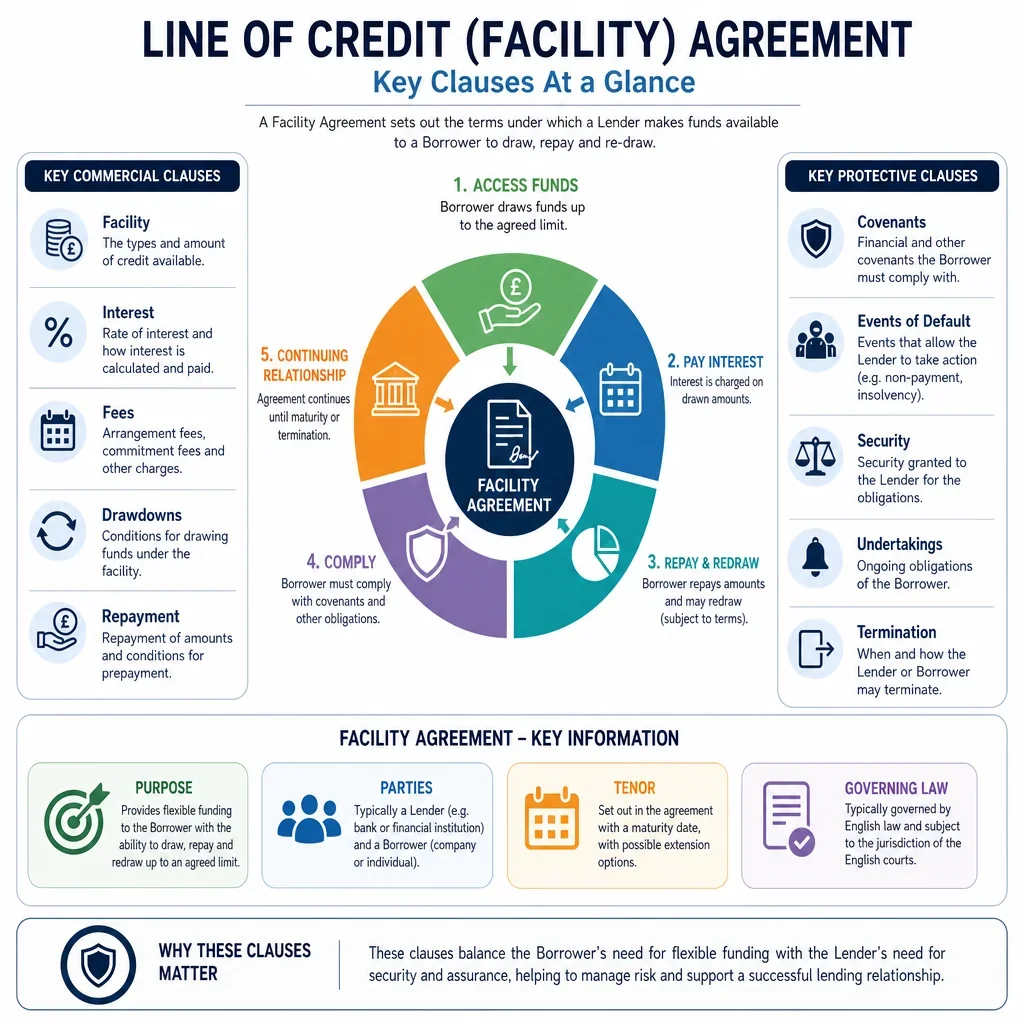

A UK facility agreement sets the legal and commercial rules for a line of credit. It should clearly state who can borrow, how much can be drawn, when money must be repaid, how interest is calculated, and what happens if the borrower defaults.

Choosing the wrong structure can create avoidable risk. A document that ignores consumer credit rules, security registration, tax withholding, execution formalities, or UK insolvency issues may be difficult to enforce or may fail to protect the lender.

What Can Go Wrong With A Poorly Drafted Facility Agreement?

- Regulatory risk: lending to individuals, sole traders, or small partnerships may trigger consumer credit requirements.

- Security risk: a registrable company charge may be ineffective against an administrator, liquidator, or creditor if not registered correctly.

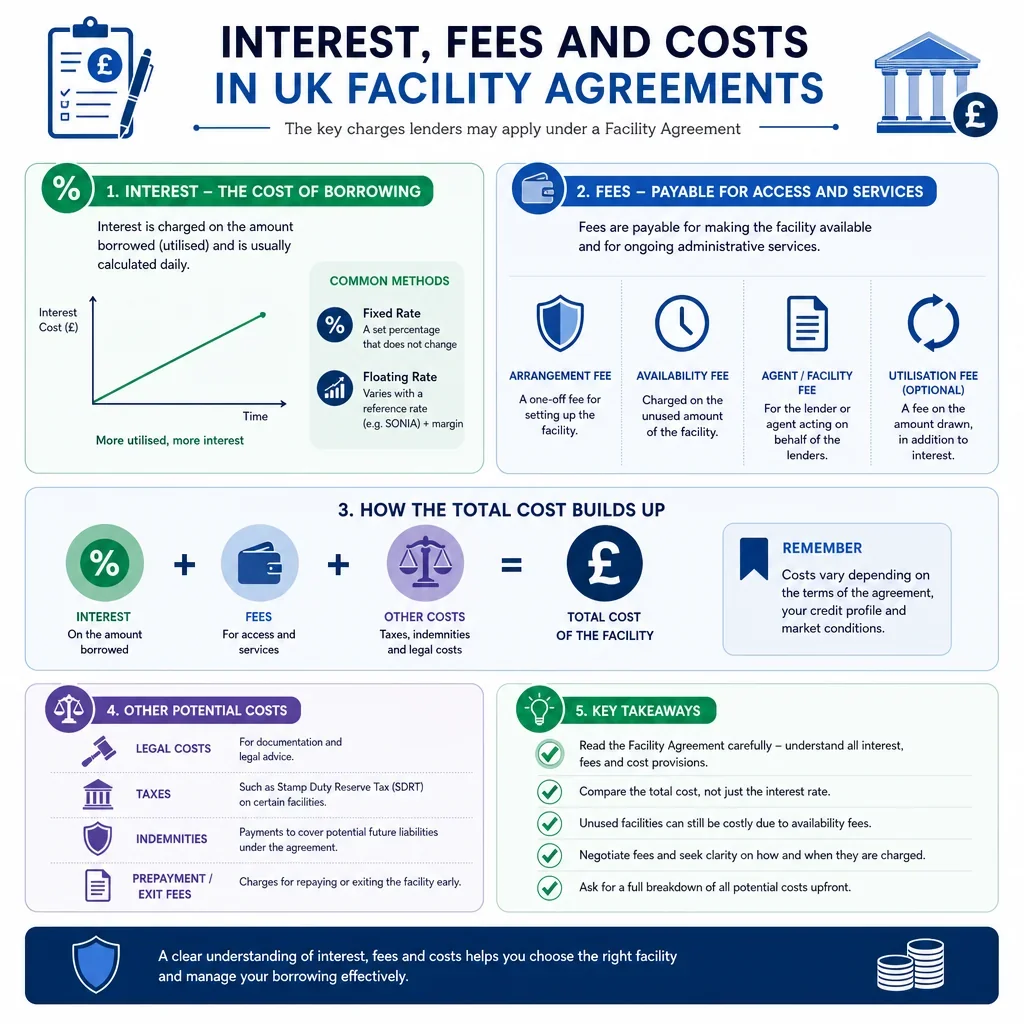

- Interest disputes: unclear fixed, floating, SONIA, or default interest wording can lead to payment disagreements.

- Tax cost: UK withholding tax on interest can affect the amount actually received by the lender.

- Execution problems: deeds, guarantees, and security documents must be signed and delivered correctly.

How Does A Decision Tool Help Draft A UK Facility Agreement?

A structured decision process helps identify whether the facility should be a simple unsecured business credit line, an uncommitted facility letter, a secured facility pack, or a more complex multi-facility agreement. It also helps flag when specialist advice is needed before the document is generated.

For official guidance, users may need to review resources from the FCA, Companies House, the Bank of England, and HMRC.

FAQs

You Might Also Be Interested In