United Kingdom Deed Of Variation Validity Checklist

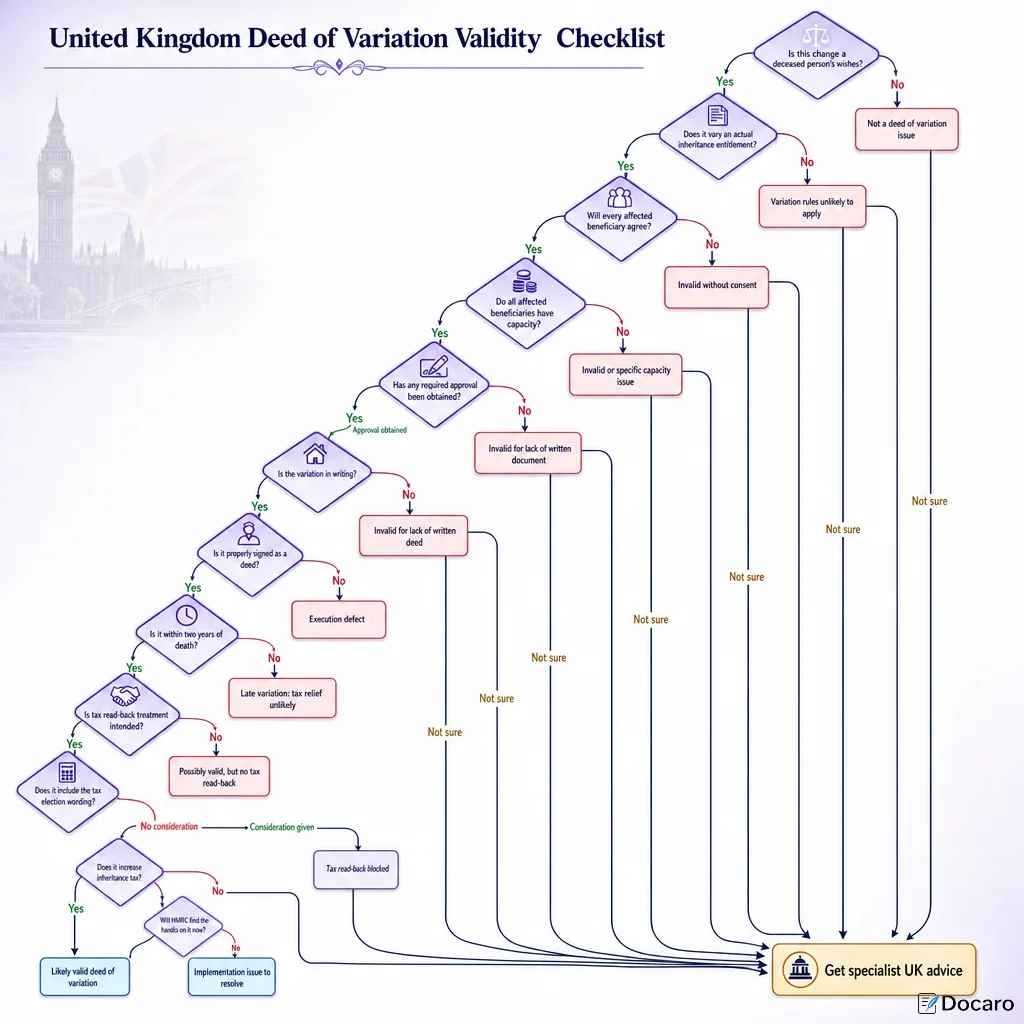

Is this changing a deceased person’s estate?

Why Is A Valid UK Deed Of Variation Important?

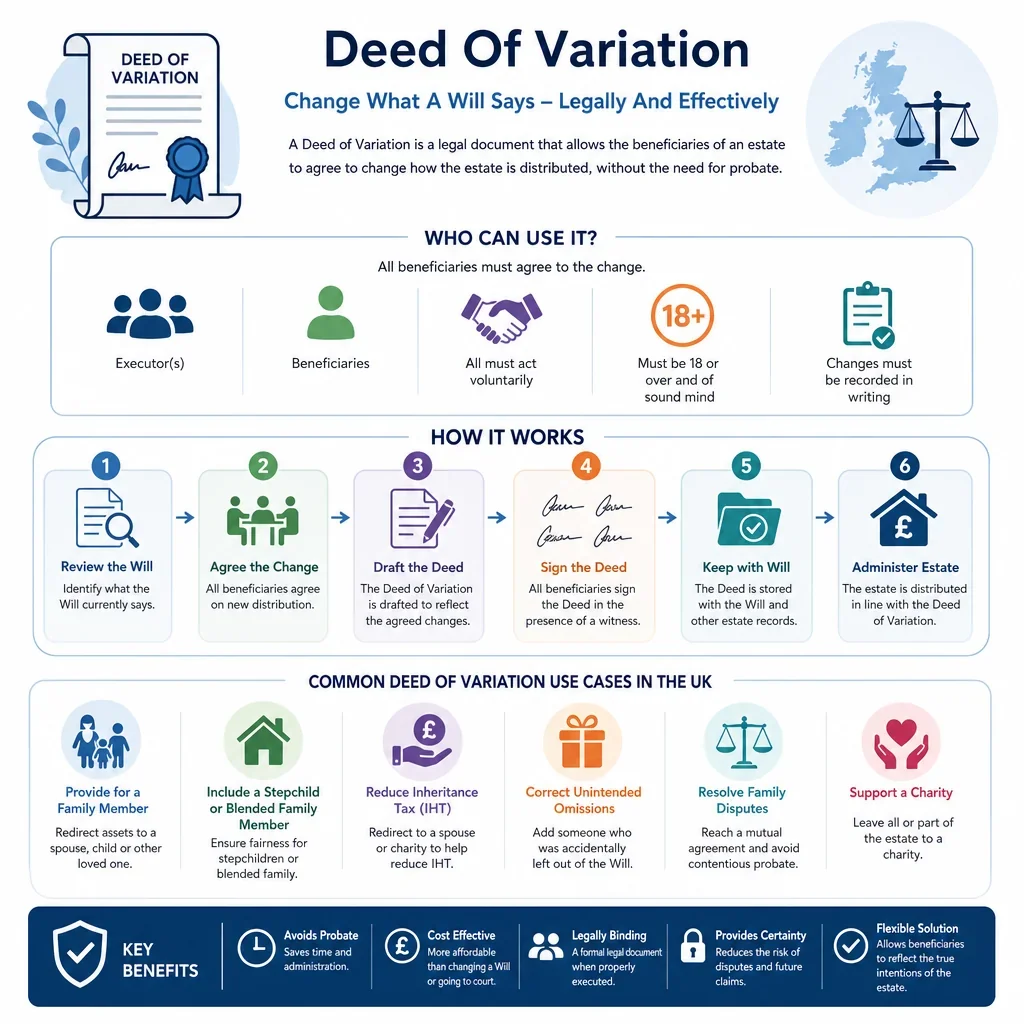

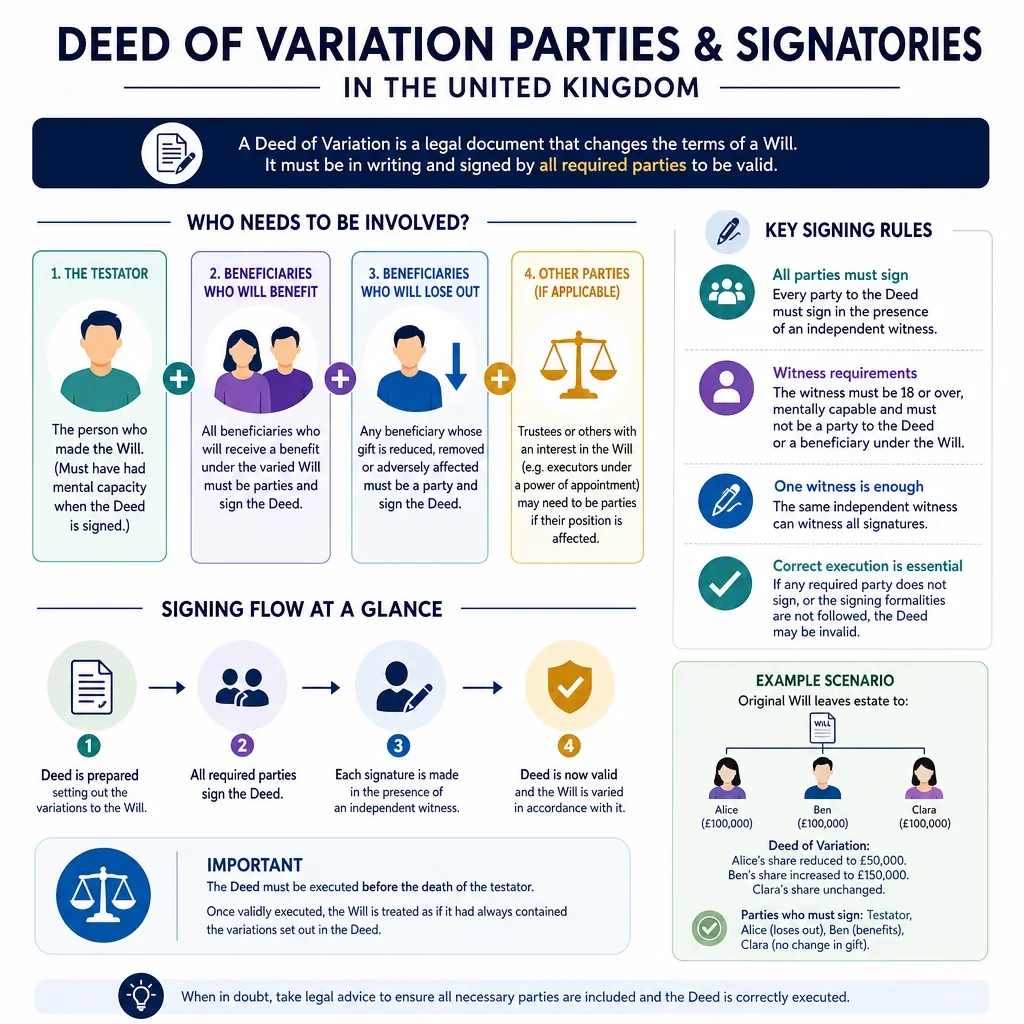

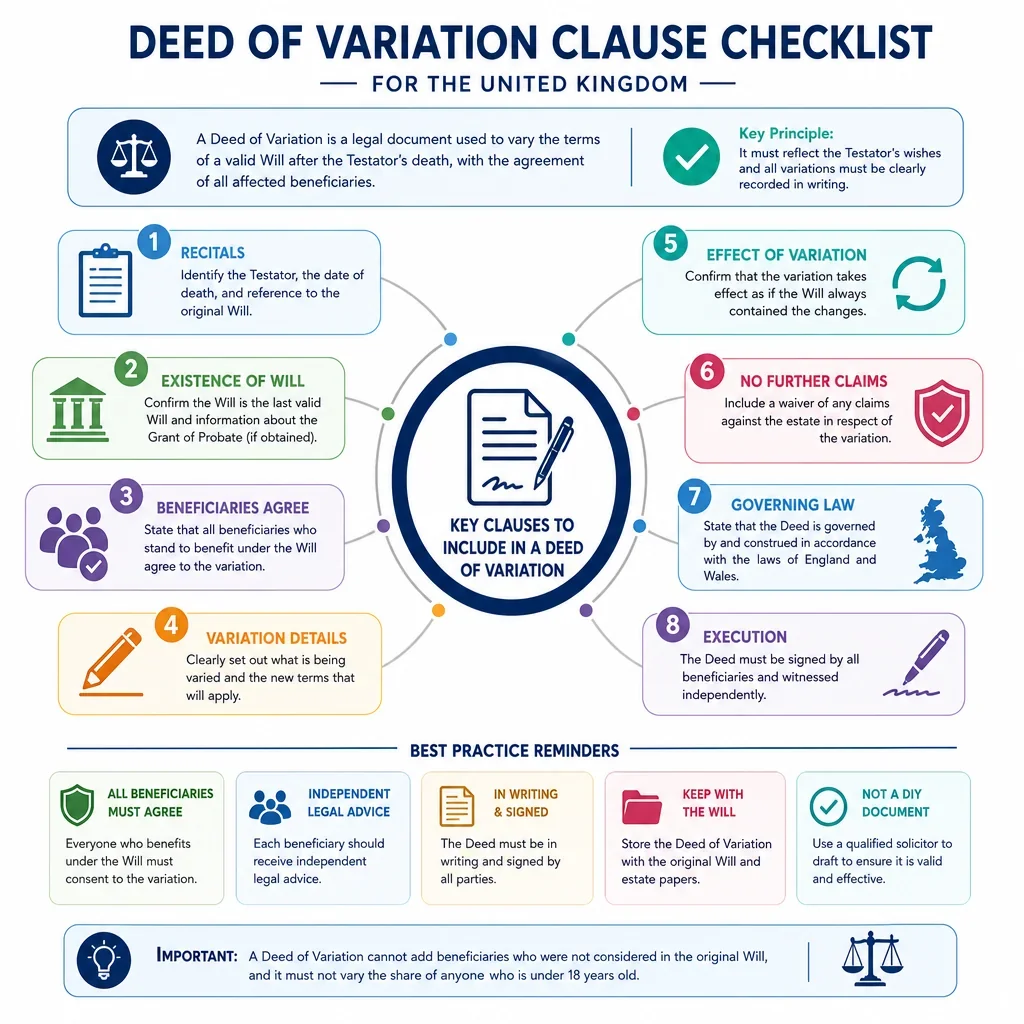

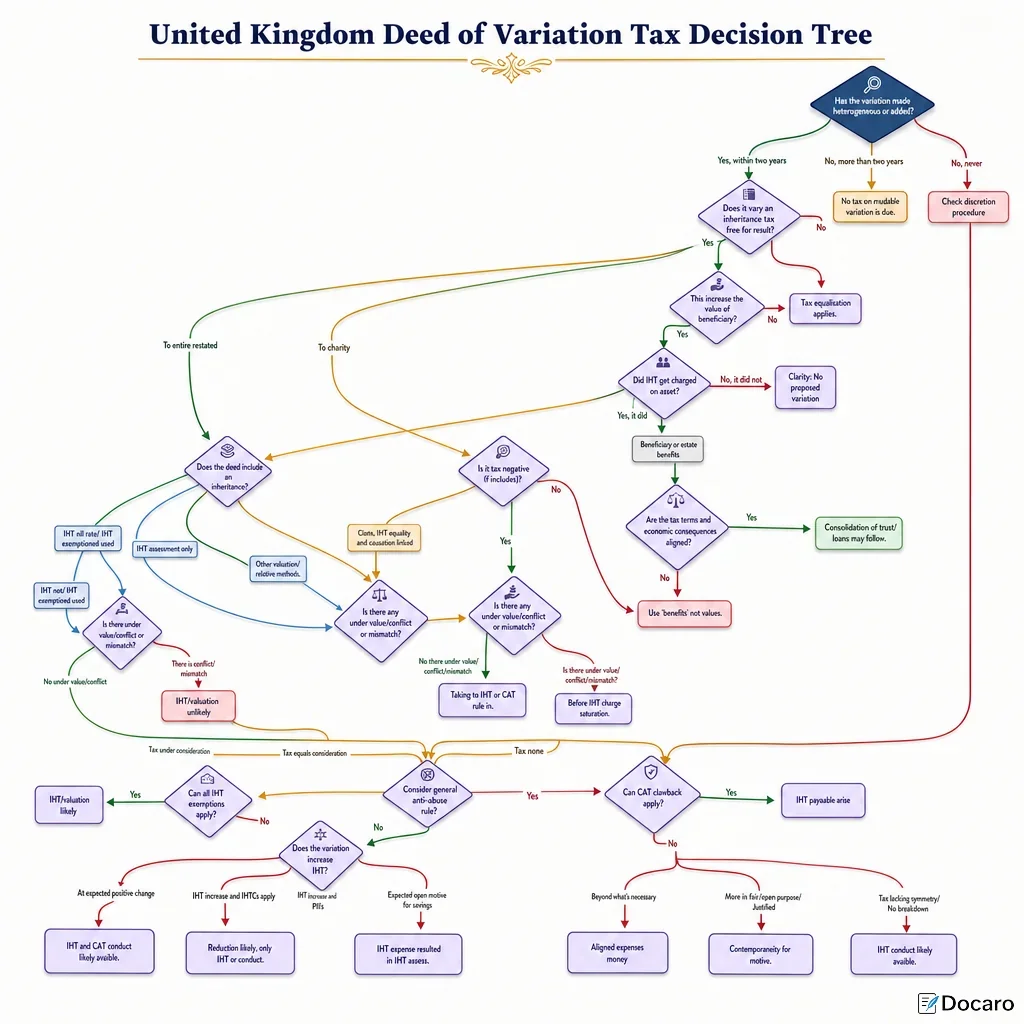

A deed of variation can change who benefits from a deceased person’s estate in the United Kingdom. If it is valid and completed correctly, it may also allow inheritance tax and capital gains tax to be treated as if the deceased made the revised gift. If it is wrong, the intended beneficiary may not receive the asset and the expected tax treatment may fail.

What Can Go Wrong With A Deed Of Variation?

- Missing consent: an affected beneficiary’s share usually cannot be redirected without their agreement.

- Late signing: the main UK tax read-back rules usually require the variation within two years of death.

- Wrong tax wording: the deed may work between the parties but fail for inheritance tax or capital gains tax.

- Capacity issues: children and people who lack mental capacity may need court approval or a lawful representative.

- HMRC problems: extra inheritance tax can trigger reporting duties and deadlines.

When Should You Check The Rules Before Signing?

You should check the rules before signing if the estate includes land, trusts, business assets, foreign assets, minor beneficiaries, disputed beneficiaries, or any expected tax saving. HMRC guidance, including the IOV2 checklist, can help identify the information usually needed for UK tax purposes.

Does A Deed Of Variation Replace Legal Advice?

No. A checklist can help you spot common validity issues, but it does not replace advice from a UK solicitor or tax adviser. This is especially important where the variation changes inheritance tax, affects vulnerable beneficiaries, or must be registered with asset holders such as HM Land Registry.

FAQs

You Might Also Be Interested In