Deed of Variation Parties and Signatories in the United Kingdom

Party Type | Role Description | Signature Requirement | Consent Considerations | Supporting Evidence | Complexity Level |

|---|---|---|---|---|---|

Beneficiary | |||||

Adult beneficiary redirecting inheritance | Gives up or redirects all or part of inherited entitlement. | Usually required | Must agree to reduce or redirect own entitlement. | Will, estate accounts, ID, entitlement schedule. | Low |

New beneficiary receiving varied gift | Receives benefit created by the variation. | Sometimes required | Needed if accepting obligations, trust terms, or disclaimers. | ID, address, relationship to deceased, bank details if paid. | Low |

Residuary beneficiary | Entitled to the remaining estate after specific gifts and debts. | Usually required | Needed if residue is reduced, redirected, or reallocated. | Will residue clause, estate accounts, beneficiary ID. | Medium |

Specific legacy beneficiary | Receives a named asset, sum, or item under the will. | Usually required | Needed if the legacy is varied or surrendered. | Will clause, asset valuation, ID. | Low |

Pecuniary legacy beneficiary | Receives a fixed cash gift under the will. | Usually required | Needed if the cash legacy is reduced or redirected. | Will clause, estate payment record, ID. | Low |

Intestacy beneficiary | Inherits under statutory intestacy rules where no valid will applies. | Usually required | Needed if statutory share is reduced or redirected. | Family tree, death certificates, letters of administration. | Medium |

Surviving spouse or civil partner | Often receives spouse-exempt inheritance or statutory entitlement. | Usually required | Needed if redirecting spouse-exempt or intestacy entitlement. | Marriage or civil partnership certificate, will, ID. | Medium |

Divorced or former civil partner beneficiary | May be treated as predeceased for will gifts after divorce. | Depends on circumstances | Review divorce effect before assuming any entitlement exists. | Decree absolute or final order, will, legal advice note. | High |

Other Interested Party | |||||

Unmarried partner or cohabitant | May benefit under a will but has no automatic intestacy entitlement. | Depends on circumstances | Needed if their will entitlement is reduced or settled. | Will clause, relationship evidence, claim correspondence. | Medium |

Beneficiary | |||||

Beneficiary who previously disclaimed | Has refused inheritance rather than redirecting it by variation. | Usually not required | Disclaimer may prevent later choosing who receives the benefit. | Disclaimer deed or written disclaimer, probate file. | Medium |

Executor or Personal Representative | |||||

Executor named in the will | Administers the estate under the will and probate grant. | Sometimes required | Needed if variation affects administration, tax, or executor obligations. | Grant of probate, will, executor ID. | Medium |

Administrator on intestacy | Administers estate where there is no valid will or executor. | Sometimes required | Needed if variation changes distributions the administrator must make. | Letters of administration, intestacy schedule, ID. | Medium |

Personal representative making IHT tax statement | Joins where variation affects inheritance tax payable by estate. | Depends on circumstances | Required where extra IHT is payable because of the variation. | IHT calculations, grant, HMRC correspondence. | High |

Beneficiary, Executor or Personal Representative | |||||

Sole executor who is also beneficiary | Acts both as estate administrator and person varying entitlement. | Usually required | Must sign clearly in beneficiary and executor capacities if needed. | Grant, will, ID, capacity wording. | Medium |

Executor or Personal Representative | |||||

Substitute or replacement personal representative | Acts where original executor cannot or will not administer. | Sometimes required | Needed if currently administering affected estate assets. | Grant, renunciation, power reserved notice, ID. | Medium |

Executor who has renounced probate | Named executor who has formally given up the role. | Usually not required | Generally not needed unless also a beneficiary. | Renunciation form, probate registry record, will. | Low |

Trustee | |||||

Trustee of a will trust | Holds or manages estate assets on trust for beneficiaries. | Sometimes required | Needed if trust assets or trust terms are altered. | Will trust clause, trustee appointment deed, ID. | High |

Beneficiary, Trustee | |||||

Life tenant | Has income or occupation rights during lifetime under a trust. | Usually required | Needed if life interest is surrendered, reduced, or redirected. | Trust instrument, will, property title, ID. | High |

Beneficiary | |||||

Remainderman or capital beneficiary | Receives capital after a life interest or trust period ends. | Depends on circumstances | Needed if future capital interest is reduced or accelerated. | Trust terms, beneficiary class list, actuarial valuation. | High |

Discretionary trust beneficiary | Potential recipient selected at trustees' discretion. | Depends on circumstances | Consent may be unnecessary unless vested rights are affected. | Trust deed, class description, trustee minutes. | High |

Charity | |||||

Charitable beneficiary | Receives charitable gift that may qualify for IHT relief. | Usually required | Needed if charity gift is reduced, redirected, or restricted. | Charity number, authorised signatory evidence, will clause. | Medium |

Charity, Trustee | |||||

Charity trustee or authorised officer | Signs on behalf of charitable organisation if authorised. | Sometimes required | Authority needed under charity governance documents and trustee duties. | Trustee minutes, governing document, Charity Commission entry. | Medium |

Charity | |||||

Exempt charity beneficiary | Charity not registered with Charity Commission but potentially exempt. | Usually required | Confirm legal status and authorised signatory before varying gift. | Exempt status proof, governing body authority, correspondence. | Medium |

HMRC | |||||

HMRC Inheritance Tax | Recognises qualifying variations for IHT if statutory conditions are met. | Usually not required | HMRC clearance or reporting may be needed where IHT changes. | Deed, IHT forms, tax calculations, statement of intent. | High |

HMRC Capital Gains Tax | Recognises qualifying variations for CGT no-disposal treatment. | Usually not required | CGT statement needed if read-back treatment is intended. | Deed, asset values, CGT statement, acquisition evidence. | High |

Minor or Protected Beneficiary | |||||

Minor beneficiary | Child beneficiary unable to give binding consent personally. | Depends on circumstances | Court approval may be needed if entitlement is reduced. | Birth certificate, guardian details, court order if obtained. | High |

Unborn or future beneficiary | Potential future beneficiary within a class gift or trust. | Usually not required | Court may approve arrangement on behalf of unborn interests. | Trust terms, class list, counsel opinion, court order. | High |

Beneficiary lacking mental capacity | Beneficiary unable to make the decision personally. | Depends on circumstances | Attorney, deputy, or Court of Protection authority may be required. | Capacity evidence, LPA, deputyship order, court order. | High |

Other Interested Party | |||||

Attorney under lasting power of attorney | May act for donor if authority covers estate decision. | Depends on circumstances | Check scope gifts and variations may need court approval. | Registered LPA or EPA, donor ID, best interests note. | High |

Other Interested Party, Minor or Protected Beneficiary | |||||

Court of Protection deputy | Court-appointed decision-maker for protected beneficiary. | Depends on circumstances | Deputy order must authorise variation or court approval is needed. | Deputyship order, capacity evidence, court approval. | High |

Minor or Protected Beneficiary, Other Interested Party | |||||

Parent or guardian of minor beneficiary | Represents practical interests of a child beneficiary. | Sometimes required | Cannot usually surrender child's property without proper authority. | Birth certificate, parental responsibility evidence, court order. | High |

Other Interested Party | |||||

Estate creditor | Has claim against estate before beneficiaries receive distributions. | Usually not required | Consent may be needed for settlement affecting creditor rights. | Debt evidence, invoices, settlement agreement, estate accounts. | Medium |

Family provision claimant | Claims reasonable financial provision from the estate. | Depends on circumstances | Needed if variation forms part of settlement or release. | Claim letter, court papers, settlement terms, financial evidence. | High |

Trustee in bankruptcy of beneficiary | Controls bankrupt beneficiary's vested property interests. | Depends on circumstances | Needed if inherited entitlement has vested in bankruptcy estate. | Bankruptcy order, trustee appointment, insolvency register entry. | High |

Beneficiary, Other Interested Party | |||||

Corporate beneficiary | Company receiving or surrendering estate benefit. | Usually required | Board authority and valid company execution are needed. | Companies House record, board minutes, execution block. | Medium |

Partnership beneficiary | Partnership entitled to or affected by an estate benefit. | Usually required | Check partner authority to bind the partnership. | Partnership agreement, partner authority, tax details. | Medium |

Other Interested Party | |||||

Surviving joint tenant | Receives jointly owned property automatically by survivorship. | Depends on circumstances | Variation may not redirect assets passing outside the estate. | Land Registry title, death certificate, severance evidence. | High |

Tenant in common co-owner | Owns separate share deceased's share may pass by estate. | Sometimes required | Needed if property arrangements or occupation rights change. | Title register, declaration of trust, valuation. | Medium |

Mortgage lender over estate property | Secured creditor with charge over property affected by estate. | Usually not required | Lender consent may be needed for transfer or assumption of debt. | Mortgage statement, title register, lender consent. | Medium |

Spouse of varying beneficiary | May have practical or matrimonial interest in redirected assets. | Usually not required | Consent may be prudent if family settlement or shared property involved. | Marriage certificate, family settlement documents, property evidence. | Low |

Independent witness | Witnesses signatures where deed execution is required. | Usually required | Should be independent, adult, and physically present when signing. | Witness name, address, occupation, signature date. | Low |

Solicitor preparing or advising on deed | Advises on drafting, capacity, tax wording, and execution. | Usually not required | May certify advice or hold completion documents if instructed. | Engagement letter, advice note, ID checks, completion file. | Medium |

Tax adviser or accountant | Calculates IHT or CGT impact and checks HMRC wording. | Usually not required | Not a consenting party unless acting under authority. | Tax computations, asset valuations, HMRC checklist. | Medium |

Beneficiary | |||||

Overseas beneficiary | Beneficiary resident or domiciled outside the UK. | Usually required | Execution formalities, tax residence, and ID checks may be harder. | Notarised ID, apostille if needed, tax residence details. | Medium |

Executor or Personal Representative | |||||

Foreign personal representative | Estate representative appointed under non-UK succession process. | Depends on circumstances | UK reseal, authority, and governing law may need checking. | Foreign grant, resealed grant, legalised documents, translation. | High |

Other Interested Party, Beneficiary | |||||

Assignee of beneficiary's interest | Person who has received beneficiary's estate interest by assignment. | Depends on circumstances | Needed if assigned interest would be reduced or redirected. | Assignment deed, notice to executors, beneficiary ID. | High |

Trustee | |||||

Nominee or bare trustee | Holds legal title for the true beneficial owner. | Sometimes required | Beneficial owner consent remains key nominee may execute transfers. | Declaration of trust, nominee agreement, title documents. | Medium |

Trustee, Other Interested Party | |||||

Pension scheme trustee or administrator | Controls pension death benefits usually outside the estate. | Usually not required | Deed of variation may not alter discretionary pension death benefits. | Scheme rules, nomination form, administrator decision letter. | High |

Trustee | |||||

Life policy trustee | Holds policy proceeds under separate trust outside estate. | Usually not required | Estate variation may not affect policy trust assets. | Policy trust deed, insurer letter, trustee appointment. | High |

Beneficiary | |||||

Donee of redirected asset | Receives asset because original beneficiary redirects it. | Sometimes required | Needed if taking subject to conditions, liabilities, or trust terms. | ID, address, acceptance wording, transfer details. | Low |

Member of a beneficiary class | One of a group, such as children or grandchildren. | Depends on circumstances | All affected adult members may need to consent. | Family tree, birth certificates, class closing analysis. | High |

Executor or Personal Representative, Beneficiary | |||||

Personal representative of deceased beneficiary | Represents a beneficiary who died after becoming entitled. | Depends on circumstances | Needed if deceased beneficiary's vested entitlement is varied. | Second estate grant, death certificate, vesting evidence. | High |

Minor or Protected Beneficiary, Beneficiary | |||||

Bereaved minor trust beneficiary | Child beneficiary under special IHT trust rules. | Depends on circumstances | Variation may affect favourable trust tax treatment and court approval. | Will trust terms, age evidence, IHT advice. | High |

Disabled beneficiary trust beneficiary | Beneficiary whose trust may qualify for special IHT treatment. | Depends on circumstances | Capacity, benefits, and tax treatment require specialist review. | Medical evidence, benefits evidence, trust terms, capacity assessment. | High |

Beneficiary | |||||

Recipient of agricultural property | Receives farmland or farming assets potentially qualifying for APR. | Usually required | Variation may affect agricultural property relief and valuations. | Farm accounts, tenancy, valuation, occupation evidence. | High |

Recipient of business property | Receives business or shares potentially qualifying for BPR. | Usually required | Variation may affect business property relief and control. | Company records, accounts, share certificates, valuation. | High |

Beneficiary, Trustee | |||||

Nil-rate band trust beneficiary | Interested in arrangements affecting nil-rate band planning. | Depends on circumstances | Variation may affect transferable nil-rate band availability. | Will, trust accounts, IHT calculations, spouse estate records. | High |

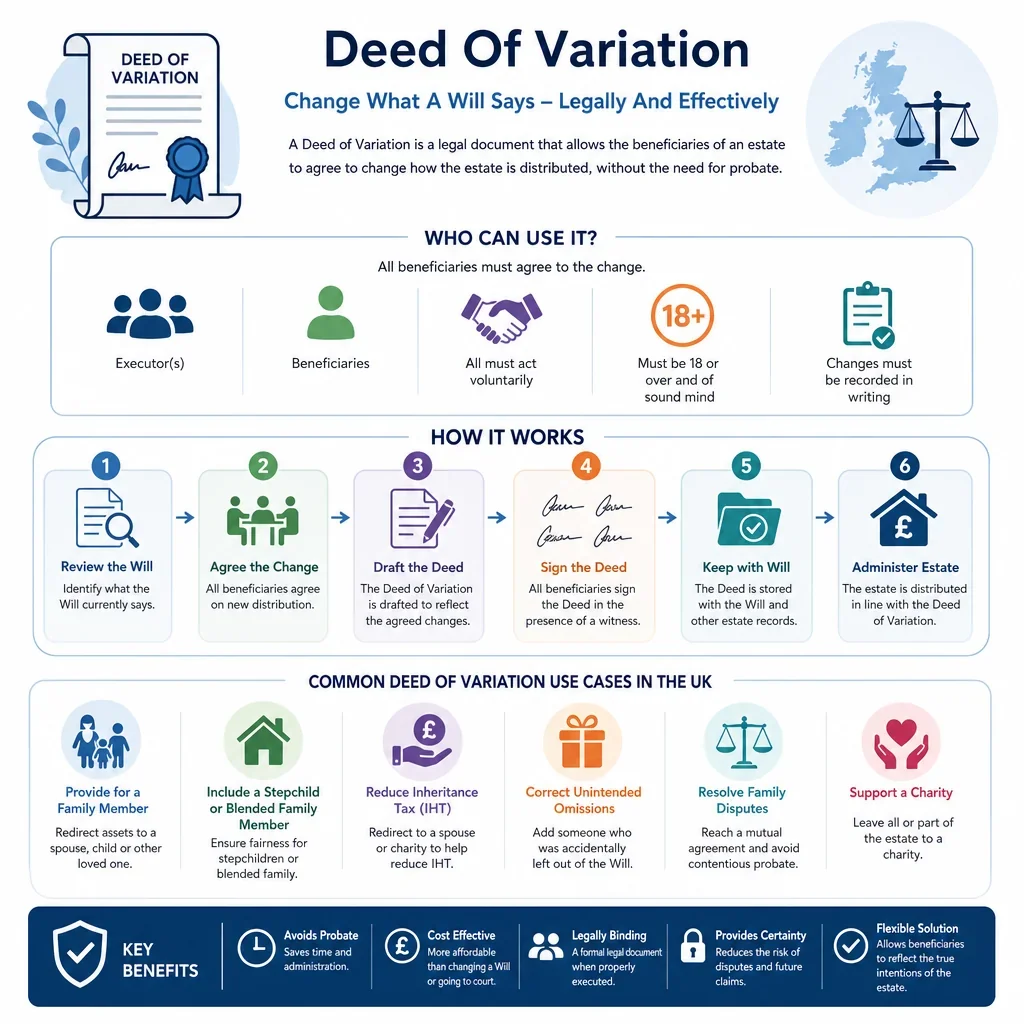

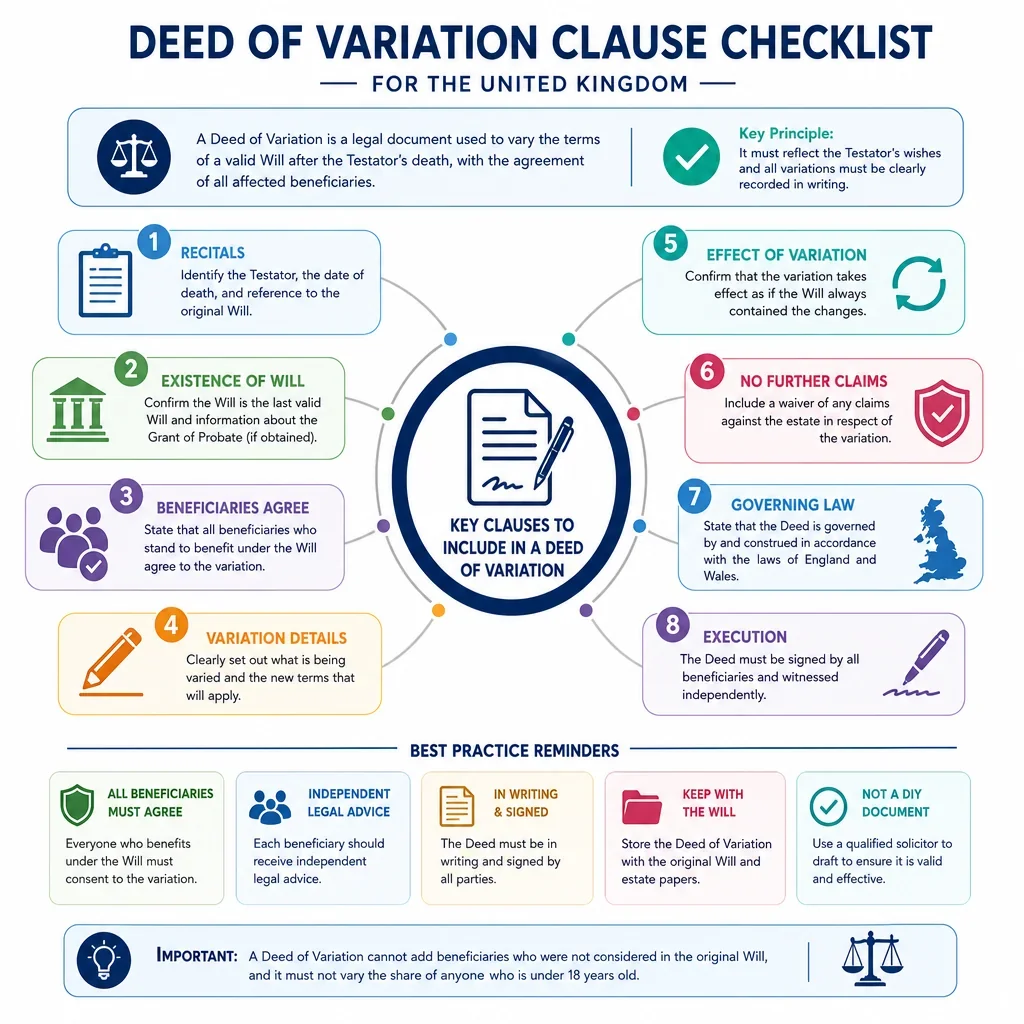

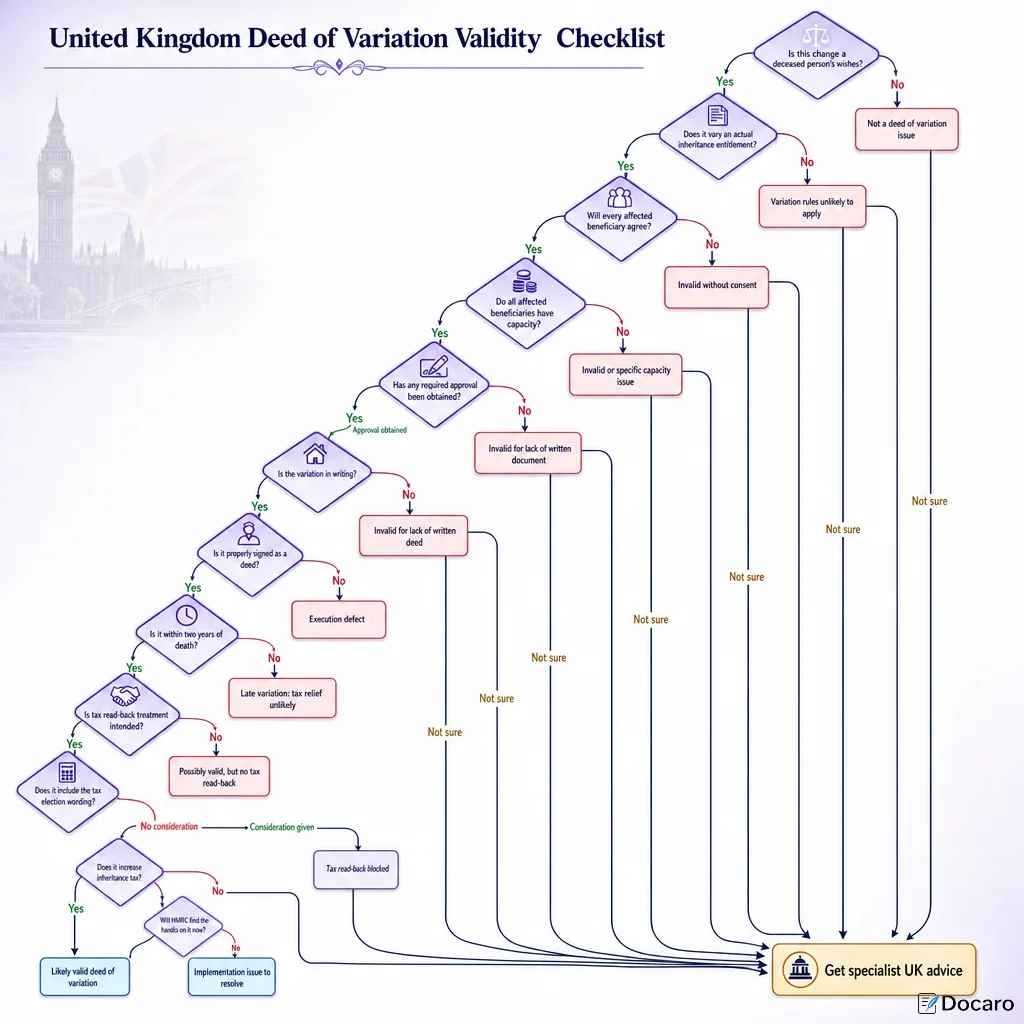

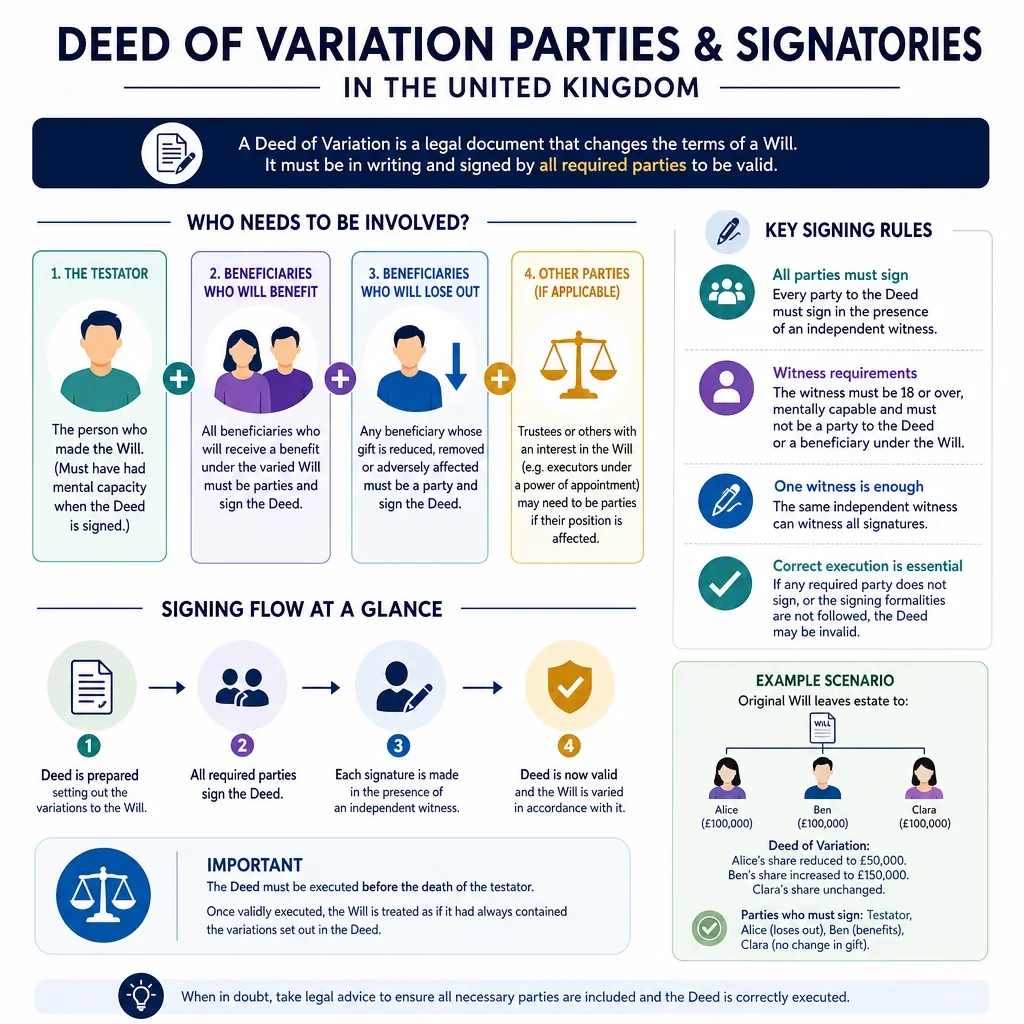

Who Needs To Sign A UK Deed Of Variation?

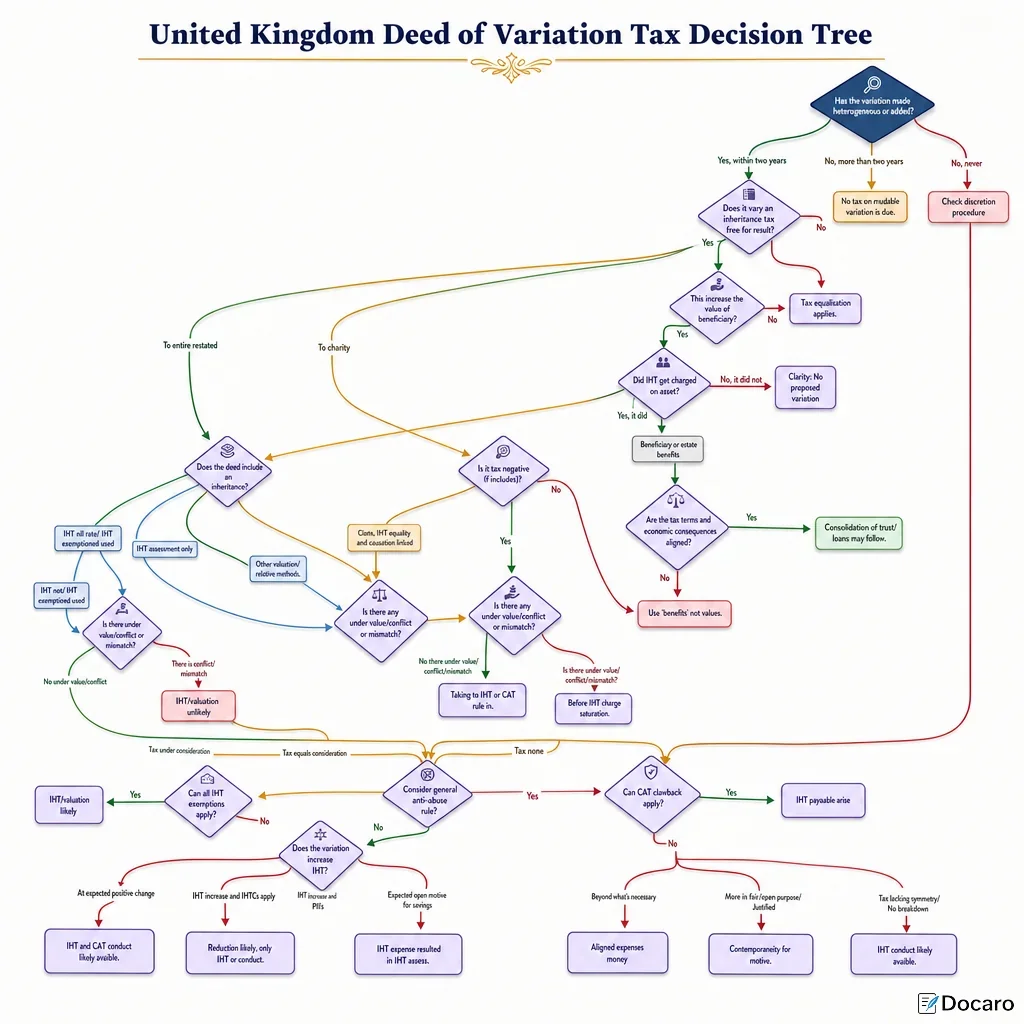

The people giving up or redirecting inheritance are normally the essential signatories. A deed of variation is effective for tax purposes only if it is made by the person or people who would otherwise benefit from the estate and contains the required tax statements where inheritance tax or capital gains tax treatment is intended.

When Do Executors Or Trustees Need To Join?

Executors are not always needed if the variation only redirects a beneficiary's entitlement, but they are commonly required where the variation changes inheritance tax, affects estate administration, or imposes obligations on them. Trustees should be involved where the affected asset is held in a trust or the variation changes trust interests.

Can A Minor Or Protected Beneficiary Sign?

No practical deed should rely on a minor or protected beneficiary personally signing away an entitlement. Where a variation would reduce the interest of a child or a person lacking mental capacity, court approval or an authorised representative may be needed, making the matter high complexity.

What Evidence Helps Avoid Problems?

- Use the will, codicils, grant of probate or letters of administration to identify personal representatives and beneficiaries.

- Use death certificates, family tree evidence and intestacy calculations where there is no will.

- Use charity registration details, company authorisations, powers of attorney, deputyship orders or trust documents where a signatory acts in an official capacity.

- Keep HMRC-focused wording precise where the deed is intended to be read back for inheritance tax or capital gains tax.

FAQs

You Might Also Be Interested In