Common Deed Of Variation Use Cases In The United Kingdom

Use Case | Purpose | Variation Objective | Typical Assets Affected | Practical Considerations | Advice Considerations |

|---|---|---|---|---|---|

UK-wide | |||||

Equalising unequal shares between siblings | Adjusts the estate so children or siblings receive equal or agreed proportions. | Changing inheritance shares | Cash residue, property sale proceeds, investments, personal possessions. | All beneficiaries losing value must consent check tax read-back wording and administration timing. | Legal and tax advice is useful where values are uncertain or estate accounts are not final. |

Redirecting inheritance to adult children or grandchildren | Passes an inheritance down a generation without the original beneficiary taking it first. | Redirecting assets | Cash legacies, residue, investment portfolios, property interests. | Consider minors, trusts, parental control, and whether the two-year tax deadline can be met. | Advice is recommended if the new beneficiaries are minors or a trust is needed. |

Increasing provision for a surviving spouse or civil partner | Redirects assets to the survivor for financial security and possible spouse exemption. | Providing for another beneficiary | Family home, cash residue, investments, life policy proceeds in the estate. | Check remarriage, care costs, family claims, and transferable nil-rate band effects. | Tax advice is important where spouse exemption or residence nil-rate band planning is involved. |

Redirecting assets from a spouse to children | Moves value directly to children to reduce the survivor's estate or reflect family agreement. | Tax planning | Residue, investment funds, second properties, surplus cash. | May reduce spouse exemption check inheritance tax, care funding and survivor's needs. | Professional advice is strongly recommended because the change can increase current estate tax. |

Creating a discretionary trust for inherited assets | Places inheritance into a flexible trust for a class of beneficiaries. | Providing for another beneficiary | Cash residue, shares, property interests, business assets. | Trustees, trust terms, registration, tax charges and administrative costs must be considered. | Specialist legal and tax advice is usually needed because trust taxation is complex. |

Creating a life interest trust for a surviving partner | Gives one person income or occupation rights while preserving capital for others. | Providing for another beneficiary | Home, investment portfolio, rental property, residue. | Define occupation, income, repair costs, sale powers and ultimate beneficiaries clearly. | Legal advice is essential to draft workable trust terms and understand inheritance tax effects. |

Adding a charitable legacy after death | Redirects part of the estate to a UK charity or qualifying charitable body. | Charitable giving | Cash gifts, residue percentage, quoted shares, sale proceeds. | Confirm charity details, exemption eligibility and whether the 36% IHT rate may apply. | Tax advice is helpful where the charitable gift may change the inheritance tax rate. |

Increasing charity gift to meet the 10% IHT test | Raises the charitable share so the estate may qualify for the 36% inheritance tax rate. | Tax planning, Charitable giving | Residue, cash, quoted investments. | Calculate the baseline amount correctly small changes can affect all taxable beneficiaries. | Specialist tax advice is strongly recommended due to detailed statutory calculations. |

Using nil-rate band planning after first death | Redirects value to non-spouse beneficiaries or a trust to use available inheritance tax allowance. | Tax planning | Cash, property share, investments up to the nil-rate band. | Compare immediate tax, transferable nil-rate band and survivor's future estate position. | Tax advice is needed to avoid wasting allowances or creating unnecessary tax charges. |

Preserving the residence nil-rate band | Redirects a home or estate value to direct descendants to support residence nil-rate band availability. | Tax planning | Main residence, sale proceeds, residue representing home value. | Check direct descendant rules, downsizing rules, estate value taper and trust structure. | Specialist advice is recommended because small drafting choices can affect the relief. |

England and Wales, Scotland, Northern Ireland | |||||

Redirecting a specific property to a different beneficiary | Transfers entitlement to a house, flat or land from one beneficiary to another. | Redirecting assets | Freehold, leasehold, Scottish heritable property, Northern Ireland land. | Check title, mortgage consent, registration requirements, SDLT or devolved land tax risks. | Conveyancing and tax advice is usually needed, especially if debt or consideration exists. |

UK-wide | |||||

Changing percentages of the residuary estate | Alters the percentage shares of what remains after debts, tax and specific gifts. | Changing inheritance shares | Net residue, sale proceeds, bank balances, investments. | Use clear percentages and ensure estate accounts match the varied distribution. | Advice is helpful if tax, debts or asset values may materially change the final residue. |

Increasing or reducing a fixed cash legacy | Changes a set monetary gift to better reflect needs, fairness or estate value. | Changing inheritance shares | Cash at bank, estate residue, investment sale proceeds. | Confirm whether interest on legacies applies and who bears any shortfall. | Legal advice is useful where the will wording or abatement rules are unclear. |

Changing gifts of personal possessions | Reallocates jewellery, vehicles, art, furniture or sentimental items by agreement. | Correcting practical issues | Jewellery, cars, artworks, antiques, furniture, family heirlooms. | Identify items precisely, value high-value chattels and record delivery or sale arrangements. | Advice is usually needed only for valuable items, disputes or tax reporting. |

Redirecting a failed or impractical gift | Reallocates a gift that cannot practically be delivered or no longer exists. | Correcting practical issues | Sold property, closed accounts, missing items, obsolete shareholdings. | Confirm whether the gift has legally failed or adeemed before varying entitlements. | Legal advice is recommended because construction of the will may decide the outcome. |

England and Wales, Scotland, Northern Ireland | |||||

Changing who inherits on intestacy | Alters statutory intestacy entitlements where the deceased left no valid will. | Changing inheritance shares | Entire estate, family home, bank accounts, personal possessions. | Identify all statutory beneficiaries and obtain consent from those giving up value. | Legal advice is important because intestacy rules differ across UK jurisdictions. |

Providing for an unmarried partner excluded by intestacy | Redirects inheritance to a cohabiting partner who does not automatically inherit on intestacy. | Providing for another beneficiary | Home share, cash, residue, personal belongings. | Family beneficiaries must agree consider occupation needs and possible family provision claims. | Legal advice is strongly recommended where cohabitation, dependency or housing rights are disputed. |

England and Wales, Northern Ireland | |||||

Settling a potential family provision dispute | Varies the estate to provide reasonable financial provision and avoid litigation. | Providing for another beneficiary | Cash settlement, property occupation rights, residue share. | Settlement should address limitation periods, releases, costs and court approval if needed. | Contentious probate advice is essential because claims and settlements are fact-sensitive. |

Scotland | |||||

Adjusting distribution around Scottish legal rights | Reflects agreement where a spouse, civil partner or children have Scottish legal rights claims. | Changing inheritance shares | Moveable estate, cash, investments, personal property. | Legal rights apply to moveable estate, not heritable property elections need careful handling. | Scottish succession advice is recommended because rules differ from England and Wales. |

UK-wide | |||||

Redirecting inherited business assets | Passes business interests to the person best placed to own or run them. | Redirecting assets | Private company shares, partnership interests, sole trader assets. | Check shareholder agreements, partnership terms, valuations and business relief availability. | Specialist tax and corporate advice is usually required due to relief and control issues. |

Redirecting agricultural property to farming successors | Moves farmland or farm assets to those continuing the farming business. | Redirecting assets | Farmland, farmhouses, tenancies, livestock, farm partnership interests. | Check agricultural property relief, business relief, tenancies, occupation and valuations. | Specialist agricultural tax and property advice is strongly recommended. |

Redirecting a disclaimed inheritance to chosen beneficiaries | Uses a variation instead of a simple disclaimer to control who receives the asset. | Redirecting assets | Cash legacy, residue share, investments, property interest. | A disclaimer normally cannot direct the destination a variation can specify recipients. | Advice is helpful to choose between disclaimer and variation and preserve tax treatment. |

Providing for a disabled or vulnerable beneficiary | Redirects inheritance into suitable arrangements for a vulnerable person's benefit. | Providing for another beneficiary | Cash, investments, property share, residue. | Consider trust type, deputyship, benefits, care funding and trustee suitability. | Specialist advice is essential because tax, benefits and capacity issues overlap. |

Creating arrangements for a minor beneficiary | Redirects or holds inheritance for a child until an appropriate age or event. | Providing for another beneficiary | Cash, investments, education funds, property shares. | Minors cannot consent court or trust arrangements may be needed if rights are reduced. | Legal advice is needed where a minor loses, gains or has restricted access to value. |

Clarifying a misdescribed beneficiary | Records agreed treatment where a beneficiary's name or description is inaccurate. | Correcting practical issues | Any legacy or residue share affected by the description. | Check whether interpretation, rectification or a variation is the correct route. | Legal advice is recommended where identity is uncertain or competing beneficiaries exist. |

Adding a person accidentally omitted from the will | Provides for someone the family accepts should have benefited from the estate. | Providing for another beneficiary | Cash legacy, residue share, property interest. | Beneficiaries giving up value must agree consider whether a claim has been threatened. | Legal advice is important if omission may indicate negligence, undue influence or a claim. |

Changing how an asset is distributed instead of sold | Allows a beneficiary to take an asset directly rather than receiving sale proceeds. | Correcting practical issues | Property, shares, vehicles, valuable chattels, business interests. | Agree valuation, equalisation payments, transfer costs and responsibility for liabilities. | Advice is helpful where asset values change or land tax may be triggered. |

England and Wales, Scotland, Northern Ireland | |||||

Redirecting a share of the family home | Changes who receives the deceased's share of a jointly or solely owned home. | Redirecting assets | Main residence, beneficial share, sale proceeds. | Check survivorship, title, occupation rights, mortgage, registration and residence nil-rate band. | Property and tax advice is recommended because ownership form affects whether variation is possible. |

England and Wales, Northern Ireland | |||||

Varying entitlement to a tenant in common share | Redirects the deceased's defined property share where it passes under will or intestacy. | Redirecting assets | Beneficial share in a house or land held as tenants in common. | A beneficial joint tenancy passes by survivorship and is not usually varied through the estate. | Legal advice is needed to confirm ownership and whether the asset forms part of the estate. |

UK-wide | |||||

Reallocating jointly owned account value included in the estate | Adjusts treatment of the deceased's beneficial contribution to a joint account or investment. | Correcting practical issues | Joint bank accounts, investment accounts, savings products. | Confirm beneficial ownership, survivorship terms and evidence of contributions. | Advice is recommended where ownership is disputed or inheritance tax reporting is affected. |

Redirecting assets before sale to manage capital gains tax | Moves assets to beneficiaries before disposal so tax positions can be planned. | Tax planning | Shares, investment funds, land, rental property, valuable chattels. | Variation must meet CGT conditions and be made before a relevant disposal. | Tax advice is important where assets have risen in value since death. |

Varying inheritance with inheritance tax read-back | Treats the gift for inheritance tax as if made by the deceased, if conditions are met. | Tax planning | Any estate asset or estate entitlement. | Must be in writing, within two years, and contain the statutory IHT statement. | Tax advice is recommended to ensure the deed qualifies and is reported correctly. |

Simplifying complex small gifts | Replaces numerous small or impractical gifts with a simpler agreed distribution. | Correcting practical issues | Small cash legacies, personal possessions, low-value shares. | Ensure each affected beneficiary consents and administration costs do not outweigh benefits. | Advice may be proportionate if many beneficiaries or charities are involved. |

Reallocating gifts to help pay debts or tax | Adjusts entitlements so estate liabilities can be settled fairly and practically. | Correcting practical issues | Cash, residue, sale proceeds, property earmarked for sale. | Executors must still pay debts and tax before distributing beneficiaries' net entitlements. | Legal advice is useful where the estate may be insolvent or gifts must abate. |

England and Wales, Scotland, Northern Ireland | |||||

Adjusting entitlements in a near-insolvent estate | Records a realistic agreed distribution where liabilities consume most estate value. | Correcting practical issues | All estate assets remaining after debts, tax and administration expenses. | Creditors rank ahead of beneficiaries distributions before debts are paid can create risk. | Specialist probate advice is essential if solvency is uncertain. |

UK-wide | |||||

Coordinating estate variation with pension death benefits | Aligns estate gifts with separate pension nominations or trustee decisions. | Tax planning | Estate residue, cash legacies, non-estate pension lump sums. | Many pension death benefits sit outside the estate and cannot be varied as estate assets. | Pensions and tax advice is needed where death benefits and estate planning interact. |

Redirecting life policy proceeds payable to the estate | Changes who benefits from insurance money that falls into the estate. | Redirecting assets | Life insurance payout, death-in-service lump sum if estate payable. | Confirm whether proceeds are estate assets or payable under trust or nomination. | Advice is recommended if policy ownership, trusts or inheritance tax treatment is unclear. |

Varying inheritance involving overseas assets | Redirects UK estate entitlement connected with foreign property or accounts. | Redirecting assets | Foreign bank accounts, overseas land, offshore investments. | Foreign succession, tax and registration rules may not recognise the UK variation. | UK and local foreign advice is usually essential. |

Varying an estate with domicile issues | Manages inheritance tax exposure where the deceased or beneficiaries have cross-border connections. | Tax planning | UK assets, excluded property, offshore accounts, foreign real estate. | Domicile can affect which assets are taxable and whether spouse limits apply. | Specialist cross-border tax advice is strongly recommended. |

Planning gifts to a non-UK domiciled spouse | Adjusts spouse gifts where inheritance tax spouse exemption may be limited. | Tax planning | Cash, property, investments, residue. | Check domicile, election options, exemption limits and future tax residence plans. | Specialist advice is essential due to domicile elections and long-term tax consequences. |

Facilitating a beneficiary buyout of an estate asset | Allows one beneficiary to keep an asset while others receive adjusted value. | Correcting practical issues | Family home, business, farm, holiday property, valuable collections. | Agree valuation date, funding, equalisation payments, tax and transfer mechanics. | Legal and tax advice is recommended where consideration or debt is involved. |

Consolidating control of inherited company shares | Redirects shares to active family shareholders or successors to avoid fragmented control. | Redirecting assets | Private company shares, voting rights, shareholder loans. | Review articles, shareholder agreements, pre-emption rights and valuation discounts. | Corporate and tax advice is usually required. |

Redirecting inheritance where benefits could be affected | Moves inheritance away from a beneficiary to avoid direct receipt affecting means-tested support. | Redirecting assets | Cash legacy, residue share, property sale proceeds. | Deprivation of capital rules may apply if the beneficiary gives up entitlement. | Benefits and legal advice is essential before varying for this reason. |

England and Wales, Scotland, Northern Ireland | |||||

Redirecting inheritance where care fees are a concern | Changes entitlement where a beneficiary's care funding position may be affected. | Redirecting assets | Cash, home share, investments, residue. | Local authority deprivation of assets rules may be relevant if inheritance is given up. | Care funding and legal advice is strongly recommended. |

Redirecting inheritance during divorce or separation | Moves or structures inheritance where a beneficiary is in relationship breakdown. | Redirecting assets | Cash, property share, investments, trust interests. | Family courts may consider resources avoid sham arrangements and preserve evidence. | Family law and estate tax advice is recommended. |

Redirecting inheritance where a beneficiary has creditor risk | Avoids direct receipt by someone facing bankruptcy, enforcement or creditor pressure. | Redirecting assets | Cash legacy, residue, property share, investments. | Transactions may be challenged if intended to prejudice creditors or insolvency rights. | Insolvency and legal advice is essential before varying. |

UK-wide | |||||

Equalising inheritances after lifetime gifts | Adjusts estate shares to account for substantial gifts made during the deceased's lifetime. | Changing inheritance shares | Residue, cash, property sale proceeds, investments. | Agree which lifetime gifts count and what values or dates are used. | Advice is useful where lifetime gifts may also affect inheritance tax calculations. |

Rebalancing gifts after asset values change | Adjusts inheritances where one gift has become disproportionately valuable or burdensome. | Changing inheritance shares | Property, shares, business interests, cryptocurrency, investments. | Use independent valuations and agree who bears tax, costs and market risk. | Tax and valuation advice is recommended for volatile or high-value assets. |

Redirecting inherited cryptocurrency or digital assets | Transfers entitlement to digital assets to beneficiaries able to manage or liquidate them. | Redirecting assets | Cryptocurrency, exchange accounts, NFTs, digital wallets. | Confirm access, valuation date, security, tax reporting and whether assets can be transferred. | Tax and technical advice is recommended because valuation and control can be difficult. |

Redirecting an investment portfolio to a tax-efficient beneficiary | Moves inherited investments to beneficiaries with suitable tax position or investment objectives. | Tax planning | Quoted shares, funds, bonds, ISAs forming part of the estate. | Consider CGT, income tax on post-death income, transfer fees and market movement. | Tax or financial advice is recommended for large or pregnant-gain portfolios. |

Coordinating variation with inherited ISA planning | Aligns estate distribution with a surviving spouse's additional permitted ISA subscription options. | Tax planning | ISA investments, cash, residue passing to spouse or others. | ISA tax status usually ends on estate administration spouse APS rules are separate. | Financial and tax advice is useful where ISA value is significant. |

England and Wales, Scotland, Northern Ireland | |||||

Redirecting a rental property to one beneficiary | Moves a let property to a beneficiary who will manage or retain it. | Redirecting assets | Buy-to-let property, tenancy deposits, rental arrears, related loans. | Check landlord obligations, mortgage consent, CGT, land tax and income tax from rents. | Property and tax advice is recommended where the property is mortgaged or tenanted. |

Redirecting a holiday home or second home | Allocates a leisure property to beneficiaries who want to keep, use or sell it. | Redirecting assets | Holiday cottage, second home, overseas holiday property, contents. | Agree use, maintenance costs, sale rights, tax and ownership structure. | Legal and tax advice is recommended, especially for shared or overseas ownership. |

UK-wide | |||||

Changing a residuary share to include charities and family | Splits residue between family members and charities in agreed proportions. | Changing inheritance shares, Charitable giving | Net residue, cash, investments, property sale proceeds. | Charity beneficiaries may require formal documentation and accurate estate accounts. | Tax advice is useful if charity exemption changes the inheritance tax burden. |

Passing household contents to a surviving spouse | Redirects household items to the survivor for practical continuity and possible spouse exemption. | Providing for another beneficiary | Furniture, jewellery, cars, household goods, personal effects. | Identify valuable items separately and avoid disputes about sentimental possessions. | Advice is helpful for high-value collections or where beneficiaries disagree. |

Redirecting inheritance for education costs | Sets aside estate value for school, university or training costs of younger beneficiaries. | Providing for another beneficiary | Cash, investments, residue share. | Decide whether funds are held outright, by parents, or in a trust. | Legal advice is useful if beneficiaries are minors or funds need restrictions. |

Providing housing support for a beneficiary | Redirects estate value to help a beneficiary buy, keep or occupy a home. | Providing for another beneficiary | Cash deposit, home share, property sale proceeds, occupation rights. | Clarify whether support is a gift, trust interest, loan or shared ownership arrangement. | Property and tax advice is recommended where land or loans are involved. |

Changing who bears inheritance tax between beneficiaries | Adjusts beneficiaries' shares so tax is borne in an agreed way. | Tax planning | Taxable legacies, residue, exempt gifts, property gifts. | Will wording and statutory tax burden rules can affect net shares. | Tax and legal advice is recommended because net-of-tax drafting can be complex. |

Redirecting inheritance into an existing family trust | Adds estate value to an existing trust structure for family wealth management. | Redirecting assets | Cash, investments, business shares, property interests. | Review trust powers, tax status, trustee acceptance and reporting obligations. | Specialist trust and tax advice is usually required. |

England and Wales, Scotland, Northern Ireland | |||||

Documenting a mediated inheritance agreement | Turns a family settlement into a legally documented change to estate distribution. | Changing inheritance shares | Residue, property, cash, personal possessions, trust interests. | Ensure settlement terms, releases, confidentiality and tax wording are consistent. | Legal advice is recommended before signing any mediated estate settlement. |

UK-wide | |||||

Varying where an original beneficiary has died shortly after | Redirects entitlement involving a beneficiary's own estate or successors. | Redirecting assets | Inherited residue share, cash legacy, property interest. | Personal representatives of the deceased beneficiary may need to sign double tax risk may arise. | Legal and tax advice is important where two estates interact. |

England and Wales, Scotland, Northern Ireland | |||||

Reallocating a gift where a beneficiary cannot be traced | Resolves practical distribution issues where a beneficiary is missing or unresponsive. | Correcting practical issues | Cash legacy, residue share, personal possessions. | A missing beneficiary cannot consent court, insurance or tracing may be needed instead. | Legal advice is essential before reallocating a missing person's entitlement. |

UK-wide | |||||

Reflecting a non-binding letter of wishes | Changes legal entitlements to match wishes expressed outside the will. | Changing inheritance shares | Personal possessions, cash gifts, residue, charitable gifts. | The letter may be persuasive but not binding affected beneficiaries must agree. | Legal advice is useful if the letter conflicts with the will or suggests a dispute. |

Updating an outdated will by agreement after death | Adjusts estate distribution where the will no longer reflects family or financial circumstances. | Changing inheritance shares | Residue, property, cash, investments, personal possessions. | Confirm capacity concerns, later wills, codicils and all affected beneficiaries' agreement. | Legal advice is recommended if the will may be invalid, revoked or ambiguous. |

Providing for stepchildren or non-biological family members | Redirects estate value to family members not adequately covered by the will or intestacy. | Providing for another beneficiary | Cash legacy, residue share, property interest, personal possessions. | Check legal relationship, adoption status, dependency and whether existing beneficiaries agree. | Legal advice is recommended where family status affects entitlement or potential claims. |

England and Wales, Scotland, Northern Ireland | |||||

Replacing a charity that has merged or changed name | Redirects a charitable gift to the correct successor or intended charity. | Correcting practical issues, Charitable giving | Cash charity legacy, residuary charity share, specific asset gift. | Check charity registration, merger records, cy-près issues and executor authority. | Charity law advice may be needed if the intended recipient is uncertain. |

UK-wide | |||||

Redirecting a gift to a qualifying charity | Changes a charitable destination to one that qualifies for UK inheritance tax relief. | Tax planning, Charitable giving | Cash legacy, quoted shares, residue percentage. | Confirm the recipient meets UK charity tax relief conditions before signing. | Tax and charity advice is recommended for overseas or non-standard charities. |

Adjusting entitlement to estate income during administration | Clarifies who receives income generated by estate assets before final distribution. | Changing inheritance shares | Dividends, interest, rent, business profits during administration. | Estate income tax rules differ from inheritance tax treatment of capital entitlements. | Tax advice is useful where the estate receives significant income before distribution. |

Redirecting inheritance to a community or environmental charity | Uses estate value to support a charitable cause agreed by the beneficiaries. | Charitable giving | Cash, land, residue percentage, quoted shares. | Check charity status, gift restrictions and whether land is suitable for charitable transfer. | Advice is recommended for gifts of land or restricted charitable purposes. |

Increasing provision for a financially dependent adult child | Redirects estate value to an adult child with dependency, disability or financial need. | Providing for another beneficiary | Cash, residue, property occupation rights, trust fund. | Consider benefits, care funding, housing, trust protection and family agreement. | Legal, tax and benefits advice is recommended for dependency-based variations. |

Adjusting shares to reflect family loans or advances | Accounts for loans, advances or informal financial help received from the deceased. | Changing inheritance shares | Residue, cash, property sale proceeds, debt claims. | Distinguish enforceable debts from gifts and agree evidence, values and interest. | Legal advice is recommended where debt status is disputed or undocumented. |

England and Wales, Scotland, Northern Ireland | |||||

Replacing an unsuitable will trust arrangement | Changes trust-based entitlement where the original trust is impractical or tax-inefficient. | Correcting practical issues | Trust fund, property, investments, residue. | Existing trust interests, trustee powers, minor beneficiaries and court approval may matter. | Trust law and tax advice is essential before altering trust arrangements. |

UK-wide | |||||

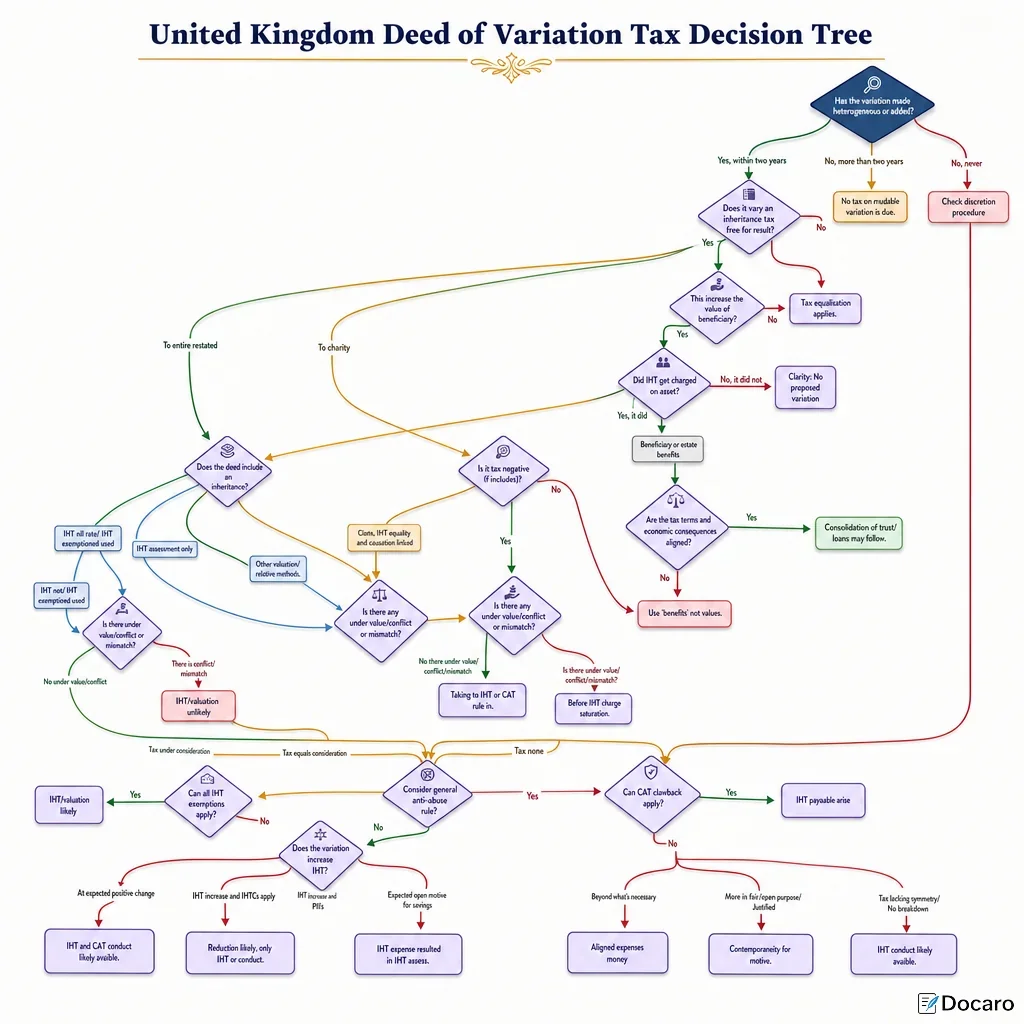

Using statutory IHT variation treatment under section 142 | Provides the statutory basis for treating qualifying variations as made by the deceased for IHT. | Tax planning | Any estate assets or inheritance entitlements within the statutory conditions. | Variation must satisfy statutory requirements, including timing and no consideration rules. | Professional tax advice is recommended to ensure section 142 treatment is valid. |

Using statutory CGT variation treatment under section 62 | Provides CGT read-back treatment for qualifying post-death variations or disclaimers. | Tax planning | Chargeable assets such as shares, land, investment funds and valuable chattels. | The variation must contain the required election and meet timing conditions. | CGT advice is recommended where assets may be sold after death. |

England and Wales, Northern Ireland | |||||

Court-approved variation where beneficiaries cannot consent | Allows the court to approve certain trust variations for minors, unborn or unascertained beneficiaries. | Correcting practical issues | Trust assets, will trusts, minor beneficiaries' contingent interests. | Court approval may be needed where a beneficiary cannot give valid consent. | Specialist trust litigation advice is essential for court-approved variations. |

England and Wales | |||||

Varying an estate to resolve a 1975 Act claim | Settles or prevents claims for reasonable financial provision from an estate. | Providing for another beneficiary | Cash settlements, property occupation rights, trust funds, residue shares. | Claims have procedural and timing risks settlements may need careful releases or approval. | Contentious probate advice is essential where a claim is possible or issued. |

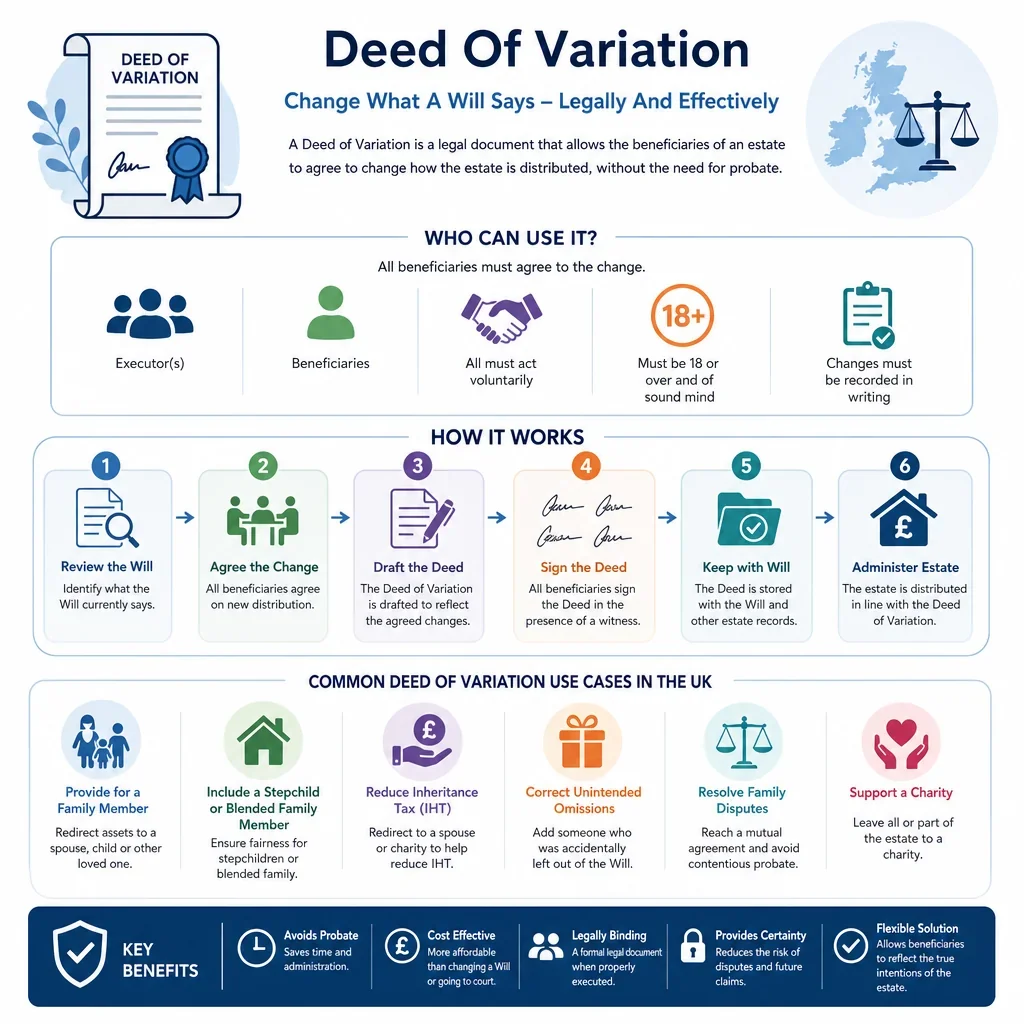

When Is A Deed Of Variation Commonly Used In The UK?

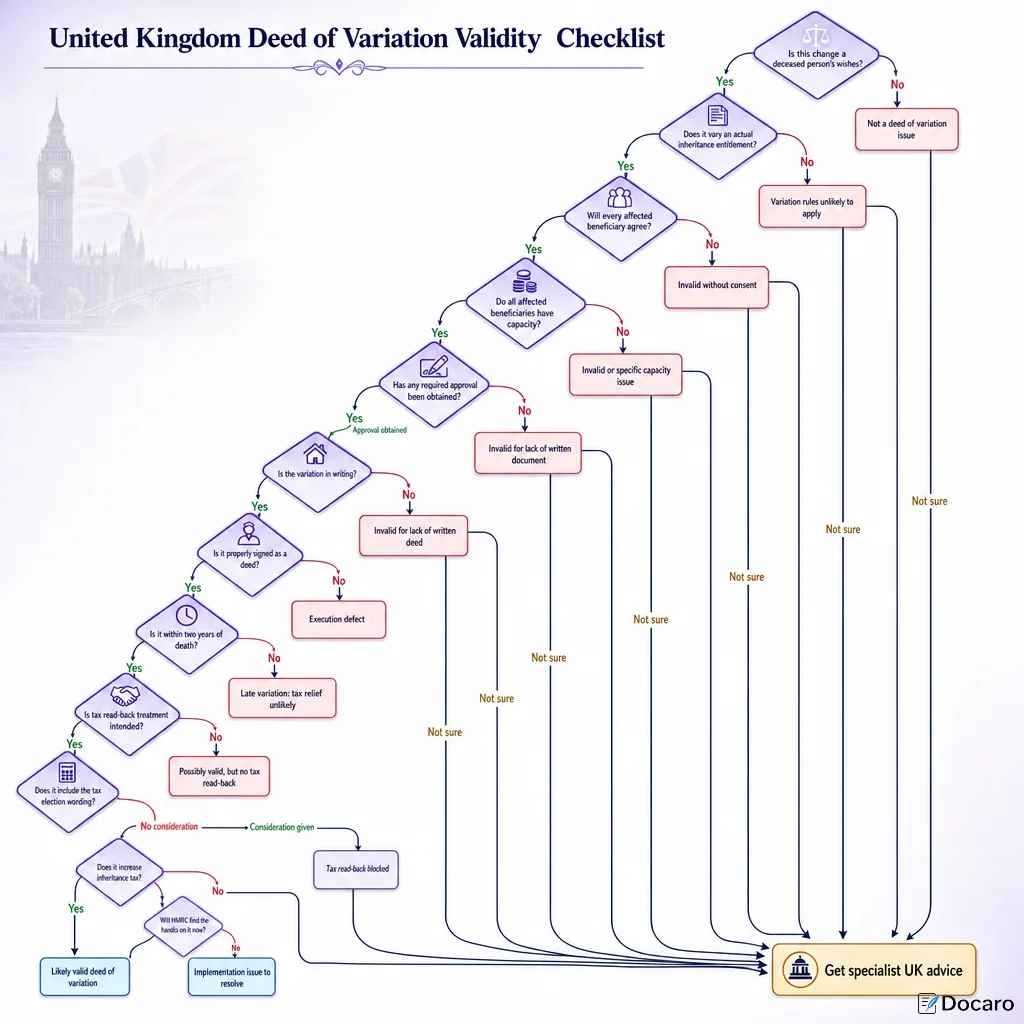

A deed of variation is most often used after a death to change who benefits from an estate, redirect a specific asset, improve inheritance tax or capital gains tax outcomes, or solve practical estate administration problems. In England and Wales, Scotland and Northern Ireland, the tax treatment depends on strict conditions, especially where the parties want the change to be treated for inheritance tax or capital gains tax as if it had been made by the deceased.

What Are The Main Tax Points To Check Before Varying An Inheritance?

- Two-year deadline: for inheritance tax and capital gains tax read-back treatment, the variation usually needs to be made within two years of death and contain the required tax statements.

- Affected beneficiaries must agree: a beneficiary whose entitlement is reduced must usually consent, and minors or unborn beneficiaries cannot personally consent.

- No payment for giving up inheritance: tax read-back treatment can be lost if a beneficiary is compensated for making the variation.

- Charity variations can reduce inheritance tax: redirecting part of an estate to charity may qualify for charity exemption and, in some cases, the reduced 36% inheritance tax rate where the charitable legacy meets the statutory threshold.

Which Deed Of Variation Use Cases Need Extra Care?

Variations involving trusts, business or agricultural assets, pensions, jointly owned property, overseas assets, insolvency, divorce, means-tested benefits, or vulnerable beneficiaries usually need specialist advice. These cases can affect tax reliefs, trustee duties, property registration, family provision claims and the risk that a variation is challenged or treated differently for non-tax purposes.

FAQs

You Might Also Be Interested In