Deed Of Variation Clause Checklist For The United Kingdom

Clause Name | Clause Purpose | Inclusion Frequency | When Relevant | Drafting Notes | Review Priority |

|---|---|---|---|---|---|

Introductory | |||||

Title and Parties | Identifies the deed and the persons bound by it. | Commonly included | All deeds of variation. | Use full legal names, addresses and capacities, such as beneficiary, executor, trustee or landlord. | High |

Identification of Original Instrument | Defines the will, trust, lease, contract or deed being changed. | Commonly included | Whenever an existing written instrument is varied. | Include date, parties, title and any previous variations or codicils. | High |

Recitals and Background | Explains the context and reason for the variation. | Commonly included | Useful where the facts affect interpretation or tax treatment. | Keep factual statements accurate and avoid creating unintended admissions. | Medium |

Operative | |||||

Effective Date | States when the variation takes effect. | Commonly included | All variations, especially estate, lease and commercial variations. | Specify whether effect is from delivery, death, completion, a past date or a future trigger. | High |

Operative Variation | Sets out the exact legal change being made. | Commonly included | Essential in every deed of variation. | Use precise replacement, deletion, insertion or redirection wording avoid ambiguity. | High |

Replacement Clause | Substitutes new wording for an existing clause. | Commonly included | Where a clause should be fully rewritten rather than amended in fragments. | Quote the old clause reference and the exact new wording. | High |

Deletion of Existing Provision | Removes a clause, gift, obligation or right. | Sometimes included | Where the variation cancels rather than replaces a provision. | Check consequential numbering, cross-references and dependent provisions. | Medium |

Insertion of New Provision | Adds a new clause, condition, gift or obligation. | Sometimes included | Where the original instrument needs additional wording. | State where the new wording is inserted and how numbering is handled. | Medium |

Confirmation of Unvaried Terms | Confirms the original document remains effective except as varied. | Commonly included | Most non-total variations. | Ensure it does not revive provisions intentionally removed or terminated. | Medium |

Beneficiary Consent | Records consent from beneficiaries whose entitlement is affected. | Commonly included | Estate and trust variations reducing or redirecting a beneficiary's interest. | A person cannot usually give up another person's entitlement without authority. | High |

Personal Representatives' Acknowledgement | Records executors' awareness of the estate variation. | Sometimes included | Where executors must administer the estate in line with the variation. | Executors may not need to be parties unless their duties, tax position or liabilities are affected. | Medium |

Trustee Consent | Records trustee agreement where trust property or powers are affected. | Sometimes included | Trust variations or estate variations creating or altering a trust. | Check trust powers, fiduciary duties and whether court approval is needed. | High |

Landlord Consent | Records landlord agreement to a lease variation. | Case-specific | Lease variations affecting rent, term, premises, covenants or alienation. | Check whether lender, superior landlord or management company consent is also required. | High |

Mortgagee or Lender Consent | Records secured lender approval to the variation. | Case-specific | Property or lease variations affecting charged property or security value. | Failure to obtain consent may breach mortgage conditions or affect priority. | High |

Third Party Rights Preservation | Protects or excludes rights of non-parties affected by the variation. | Sometimes included | Commercial, lease or trust documents granting enforceable rights to non-parties. | Consider the Contracts (Rights of Third Parties) Act 1999 and any express consent requirements. | Medium |

Redirection of Gift | Redirects an inheritance or benefit to another person or charity. | Commonly included | Post-death estate planning and family arrangements. | Identify the original gift, new recipient and exact amount, share or asset. | High |

Reduction of Entitlement | Reduces a person's share or benefit under the original instrument. | Sometimes included | Where a beneficiary keeps part but gives up or redirects part. | Distinguish a variation from a disclaimer tax consequences may differ. | High |

Creation of New Trust | Places varied property into a new trust. | Case-specific | Estate planning for minors, vulnerable beneficiaries or asset control. | Include trustees, beneficiaries, powers, perpetuity period and tax advice. | High |

Tax | |||||

Charitable Gift Variation | Redirects property to charity, often for inheritance tax planning. | Case-specific | Where beneficiaries want to increase charitable giving from an estate. | Use the charity's correct legal name and registered charity number. | High |

Inheritance Tax Section 142 Statement | Elects for the variation to be read back for inheritance tax purposes. | Commonly included | Estate variations made within two years of death that affect inheritance tax. | Must be made in writing by affected persons and contain the statutory election wording. | High |

Capital Gains Tax Section 62 Election | Elects for the variation to be read back for capital gains tax purposes. | Commonly included | Estate variations where capital gains tax read-back is desired. | Often paired with an inheritance tax statement but should be separately considered. | High |

Two-Year Death Deadline Confirmation | Confirms the deed is made within two years of death. | Commonly included | Post-death estate variations seeking IHT or CGT read-back. | Record date of death and execution date late deeds may still vary rights but not obtain read-back. | High |

No Consideration Statement | States that no money or money's worth is given for the variation. | Commonly included | Estate variations intended to qualify for tax read-back. | Consideration from outside the estate can prevent statutory tax treatment. | High |

Administrative | |||||

HMRC Notification and Filing | Sets responsibility for notifying HMRC or submitting tax forms. | Sometimes included | Where the variation changes inheritance tax or claimable reliefs. | Use HMRC checklist IOV2 where appropriate do not assume the deed alone is enough. | Medium |

Tax | |||||

Inheritance Tax Liability Allocation | Allocates who bears any inheritance tax arising from the varied gift. | Sometimes included | Where the variation changes taxable beneficiaries, exemptions or estate burdens. | Do not conflict with will tax clauses or statutory tax payment rules. | High |

Stamp Duty Land Tax Consideration Clause | Records whether land variation involves chargeable consideration. | Case-specific | Property, lease or land transaction variations in England or Northern Ireland. | Consider SDLT returns where rent, premium, debt or other consideration changes. | High |

Land Transaction Tax Consideration Clause | Records whether a Welsh land variation triggers LTT issues. | Case-specific | Property or lease variations involving land in Wales. | Use for Wales instead of SDLT consider returns and valuation. | High |

Land and Buildings Transaction Tax Clause | Flags Scottish land transaction tax consequences. | Case-specific | Variations involving Scottish land or Scottish leases. | Scotland has distinct property law and LBTT rules use Scots law drafting. | High |

VAT Treatment | Records how VAT applies to payments under the variation. | Case-specific | Commercial contracts, property transactions and lease variations with payments. | State whether sums are inclusive or exclusive of VAT and who issues invoices. | Medium |

Operative | |||||

Consideration or Premium | States any payment or value exchanged for the variation. | Sometimes included | Commercial, lease, property or settlement variations involving payment. | Avoid in estate tax read-back deeds unless professionally advised. | High |

Release of Claims | Releases parties from specified rights or claims under the original document. | Sometimes included | Commercial settlements, family estate compromises or lease variations. | Define released claims carefully avoid releasing unknown or unrelated claims unintentionally. | High |

Covenant to Observe Varied Terms | Binds parties to comply with the original document as varied. | Commonly included | Lease, contract and settlement variations with continuing obligations. | Confirm whether obligations are joint, several or joint and several. | Medium |

Indemnity | Requires one party to cover specified losses from the variation. | Sometimes included | Where tax, administration costs, consent failure or third-party claims may arise. | Limit scope, triggers, caps and duration broad indemnities need careful review. | High |

Administrative | |||||

Costs and Expenses | States who pays legal, tax, registration and administration costs. | Commonly included | Most deeds involving professional, filing or consent costs. | State whether costs are paid from the estate, by a party or shared. | Medium |

Land Registry Application | Allocates responsibility for registering the variation at HM Land Registry. | Case-specific | Variations affecting registered land or registrable leases in England and Wales. | Check prescribed clauses, title numbers, plans and whether a notice or restriction is needed. | High |

Companies House Filing | Sets filing obligations for company-related variations. | Case-specific | Variations affecting company charges, articles, shareholder rights or corporate parties. | Check Companies Act filings and board or shareholder approvals. | Medium |

Execution | |||||

Corporate Authority | Confirms a company has authorised entry into the deed. | Sometimes included | Where a company, LLP or corporate trustee is a party. | Check board approval and Companies Act 2006 execution rules. | High |

Attorney Execution Authority | Confirms an attorney may sign the deed for a party. | Case-specific | Where a party cannot or does not personally execute the deed. | Verify the power authorises deeds, gifts or estate variations as applicable. | High |

Mental Capacity Confirmation | Records that a party has capacity or that authority exists to act for them. | Case-specific | Elderly, vulnerable or impaired parties, or attorney execution. | A person lacking capacity may need attorney, deputy or court authority. | High |

Operative | |||||

Minor Beneficiary Protection | Addresses interests of beneficiaries under 18. | Case-specific | Where a variation affects a child's vested or contingent interest. | Minors cannot usually consent court approval may be needed for prejudicial changes. | High |

Variation of Trusts Act Approval | Records court approval for trust variations affecting protected beneficiaries. | Rarely included | Trust variations involving minors, unborn persons or unascertained beneficiaries. | Do not assume adult beneficiaries can bind protected classes without court approval. | High |

Administrative | |||||

Bankruptcy and Insolvency Check | Confirms whether a beneficiary's interest is controlled by a trustee in bankruptcy. | Case-specific | Where an affected beneficiary is bankrupt or subject to insolvency proceedings. | A bankrupt beneficiary may lack control over estate rights that vest in the trustee in bankruptcy. | High |

Means-Tested Benefits Warning | Flags possible benefit consequences of giving up or redirecting assets. | Rarely included | Where an affected beneficiary receives means-tested benefits or care funding. | Consider deprivation of assets rules before reducing entitlement. | Medium |

Operative | |||||

Family Provision Claim Preservation | Clarifies whether the variation affects possible family provision claims. | Case-specific | Contested estates or excluded dependants and family members. | A variation does not automatically settle all Inheritance Act 1975 claims. | High |

Interpretation | |||||

Governing Law | States which UK jurisdiction's law governs the deed. | Commonly included | All deeds, especially cross-border UK or overseas parties. | England and Wales, Scotland and Northern Ireland have different deed and property rules. | Medium |

Jurisdiction | Specifies which courts may resolve disputes about the deed. | Sometimes included | Commercial, property and cross-border variations. | Align with the original document unless a deliberate change is intended. | Medium |

Definitions | Defines key terms used in the deed. | Commonly included | Where repeated terms, assets, parties or tax concepts need clarity. | Use definitions consistently with the original instrument unless varied. | Medium |

Interpretation Rules | Explains how references, headings, statutes and parties are read. | Sometimes included | Longer deeds or deeds with technical wording. | Avoid boilerplate that conflicts with original definitions or statutory wording. | Low |

Priority of Variation | States that the deed prevails over inconsistent original terms. | Commonly included | Where original wording may conflict with the new variation. | Limit priority to the varied provisions to avoid unintended override. | Medium |

Severability | Keeps valid provisions effective if one provision fails. | Sometimes included | Commercial and lease variations with multiple obligations. | May be unsuitable if provisions are interdependent or tax-driven. | Low |

Entire Agreement | Limits reliance on statements outside the varied documents. | Sometimes included | Commercial and property variations, less often simple estate variations. | Do not exclude fraud align with original document and consumer law limits. | Medium |

Administrative | |||||

Confidentiality | Restricts disclosure of the deed and related terms. | Rarely included | Private settlements, commercial documents or sensitive family arrangements. | Allow disclosure to HMRC, courts, advisers, regulators and registries where needed. | Medium |

Data Protection | Addresses handling of personal data in administering the deed. | Rarely included | Where parties exchange beneficiary, employee, tenant or client personal data. | Consider UK GDPR and Data Protection Act 2018 obligations. | Medium |

Notices | Sets how formal communications under the deed are given. | Sometimes included | Continuing obligations, multiple parties or commercial arrangements. | Specify addresses, email use, deemed receipt and updates. | Low |

Execution | |||||

Counterparts | Allows parties to sign separate copies of the same deed. | Commonly included | Multiple parties signing remotely or at different times. | Ensure final engrossment and delivery process are controlled. | Low |

Electronic Signature | Permits valid electronic signing where legally acceptable. | Sometimes included | Remote signing or digital transaction workflows. | Witnessing requirements still apply for many deeds and must be handled correctly. | Medium |

Execution as a Deed | Ensures the document is executed with deed formalities. | Commonly included | All deeds of variation governed by England and Wales law. | The deed must make clear it is a deed, be validly executed and be delivered. | High |

Witness Attestation | Provides witness details for individual deed signatures. | Commonly included | Where individuals execute under England and Wales deed formalities. | Witness should be independent, present at signing and include name, address and occupation. | High |

Delivery of Deed | Confirms when the deed becomes legally operative. | Commonly included | All deeds where timing of legal effect matters. | Signing alone may not equal delivery state whether delivery is immediate or conditional. | High |

Conditional Delivery or Escrow | Delays effectiveness until specified conditions are met. | Rarely included | Where consents, completion, payment or registration must occur first. | State the release conditions and who controls release of signed documents. | Medium |

Administrative | |||||

Schedules and Annexures | Attaches detailed amended wording, asset lists or plans. | Sometimes included | Complex variations, property descriptions, lists of assets or revised clauses. | Ensure schedules are clearly incorporated and initialled if signing practice requires. | Medium |

Property Description and Plan | Identifies land affected by the variation. | Case-specific | Lease, easement, covenant or land transfer variations. | Use title numbers and compliant plans where boundaries or demise change. | High |

Operative | |||||

Rent Variation | Changes the rent payable under a lease. | Case-specific | Commercial or residential lease variations affecting rent. | Check rent review, service charge, SDLT or LTT consequences and lender consent. | High |

Term Variation | Extends, shortens or otherwise changes the lease term. | Case-specific | Lease extensions, surrenders and regrants, or commercial renegotiations. | Major term changes may operate as a surrender and regrant with tax and registration effects. | High |

Demise or Premises Variation | Changes the premises or extent of property let. | Case-specific | Adding, removing or redefining leased space. | Use accurate plans and check registration, SDLT and superior title issues. | High |

Service Charge Variation | Changes service charge obligations or apportionments. | Case-specific | Lease variations affecting shared costs, management or estate services. | Residential service charge changes may require statutory and reasonableness analysis. | High |

Covenant Variation | Changes positive or restrictive covenants. | Case-specific | Property, lease or commercial obligations need amendment. | Check enforceability, benefiting land, registration and third-party consent. | High |

Easement Variation | Changes rights of way, services or other easements. | Case-specific | Land transactions involving access, utilities, drainage or rights over land. | Use precise plans and consider Land Registry entries and benefiting land. | High |

Guarantor Consent and Confirmation | Confirms a guarantor remains bound after the variation. | Case-specific | Leases, loans or commercial contracts supported by a guarantee. | Material variations may discharge a guarantor unless they consent or the guarantee permits changes. | High |

Security Preservation | Preserves existing security, charges or guarantees after the variation. | Case-specific | Loan, finance, lease or property documents with security support. | Check registration of charges and whether priority is affected. | High |

Interpretation | |||||

No Waiver | Confirms the variation does not waive unrelated rights or breaches. | Sometimes included | Commercial, lease or dispute-related variations. | List known breaches separately if any are waived or reserved. | Medium |

Administrative | |||||

Further Assurance | Requires parties to sign further documents to perfect the variation. | Sometimes included | Property, trust, estate or multi-step commercial variations. | Useful for registration, tax filings and later corrective documents. | Low |

Future Amendments | States how later changes to the varied document must be made. | Sometimes included | Continuing commercial, lease or trust arrangements. | Require written deed if future changes also need deed formalities. | Medium |

Tax | |||||

Independent Tax Advice Acknowledgement | Records that parties are responsible for taking tax advice. | Sometimes included | Estate, trust, property and commercial variations with tax consequences. | Does not replace correct statutory wording or professional advice. | Medium |

Administrative | |||||

Independent Legal Advice Acknowledgement | Records that parties had opportunity to take legal advice. | Sometimes included | Family, estate, guarantor, vulnerable party or unequal bargaining situations. | Useful evidence but not a cure for undue influence, incapacity or defective consent. | Medium |

Execution | |||||

Voluntary Execution Statement | Records that parties enter the deed freely and voluntarily. | Sometimes included | Family estate variations, gifts, guarantees and vulnerable parties. | Consider separate advice where pressure, dependency or conflict is possible. | Medium |

Operative | |||||

Correction of Mistake | Corrects an error in the original instrument or earlier variation. | Case-specific | Typographical, drafting or description errors affecting rights. | Do not use as a substitute for rectification where court order may be required. | High |

Trustee Powers Confirmation | Confirms trustees have power to enter or implement the variation. | Case-specific | Trust deeds, settlements and estate variations involving trustees. | Review the trust instrument, Trustee Act powers and fiduciary constraints. | High |

Interpretation | |||||

Perpetuity Period | Sets or preserves the perpetuity period for new trust interests. | Case-specific | Variations creating or altering trusts after 6 April 2010. | Check Perpetuities and Accumulations Act 2009 and existing trust periods. | Medium |

Operative | |||||

Reservation of Rights | Preserves rights not expressly varied or released. | Sometimes included | Dispute, lease or commercial variations where rights may be unclear. | Coordinate with release, no waiver and confirmation clauses. | Medium |

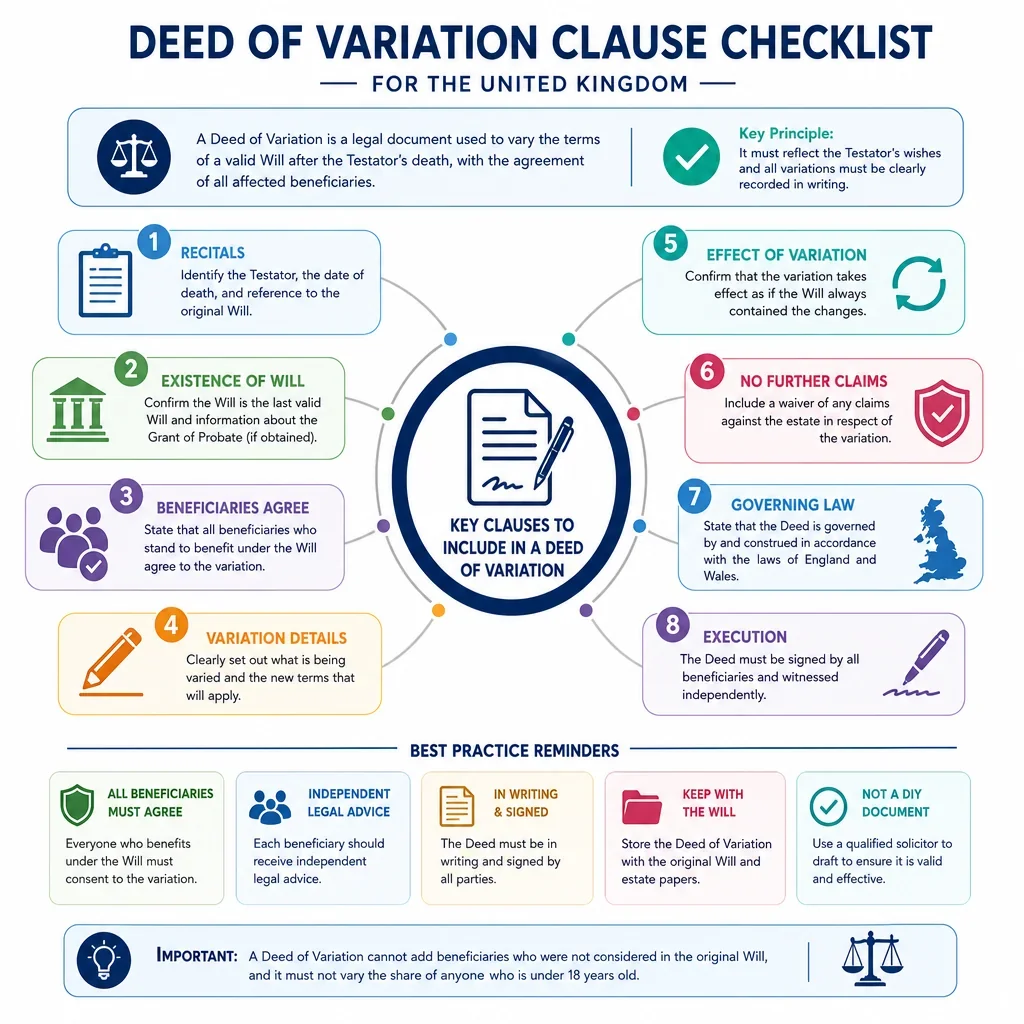

What Clauses Matter Most In A UK Deed Of Variation?

The highest-risk clauses are the operative variation wording, party identification, original document identification, consent, tax declarations and execution clauses. These provisions determine whether the deed actually changes the intended rights and whether it is likely to be accepted for the intended legal or tax purpose.

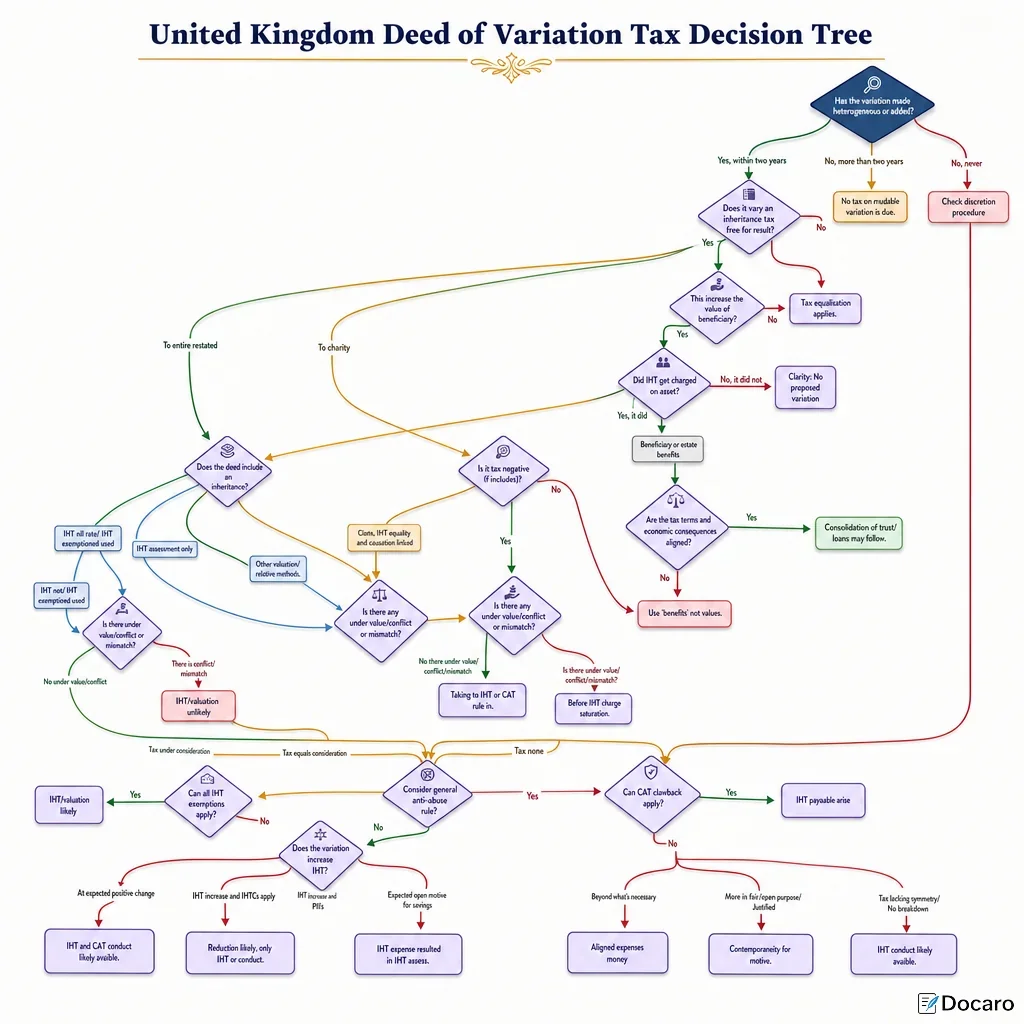

When Is A Tax Clause Needed In A Deed Of Variation?

For variations of a deceased person\'s estate, inheritance tax and capital gains tax statements are often crucial. UK tax treatment commonly depends on strict statutory conditions, including timing and the wording of the election. The relevant legislation is section 142 Inheritance Tax Act 1984 and section 62 Taxation of Chargeable Gains Act 1992.

Why Is Consent Important?

A deed of variation should normally include the consent of every person whose entitlement is reduced, redirected or burdened. Extra care is needed where a beneficiary is a minor, lacks capacity, is bankrupt, is a trustee, or where the variation affects settled property or third-party rights.

What Drafting Checks Reduce The Risk Of Invalid Variation?

- Identify the original document precisely, including date, parties and any earlier amendments.

- Use clear operative wording showing exactly which clause, gift, share, covenant or right is varied.

- State the effective date and whether the variation takes effect from signing, an earlier date, death, completion or another trigger.

- Check execution formalities, because a deed must be signed, witnessed where required and delivered to be effective.

- Do not rely on generic tax wording; tax clauses should match the type of variation and the parties\' objectives.

FAQs

You Might Also Be Interested In