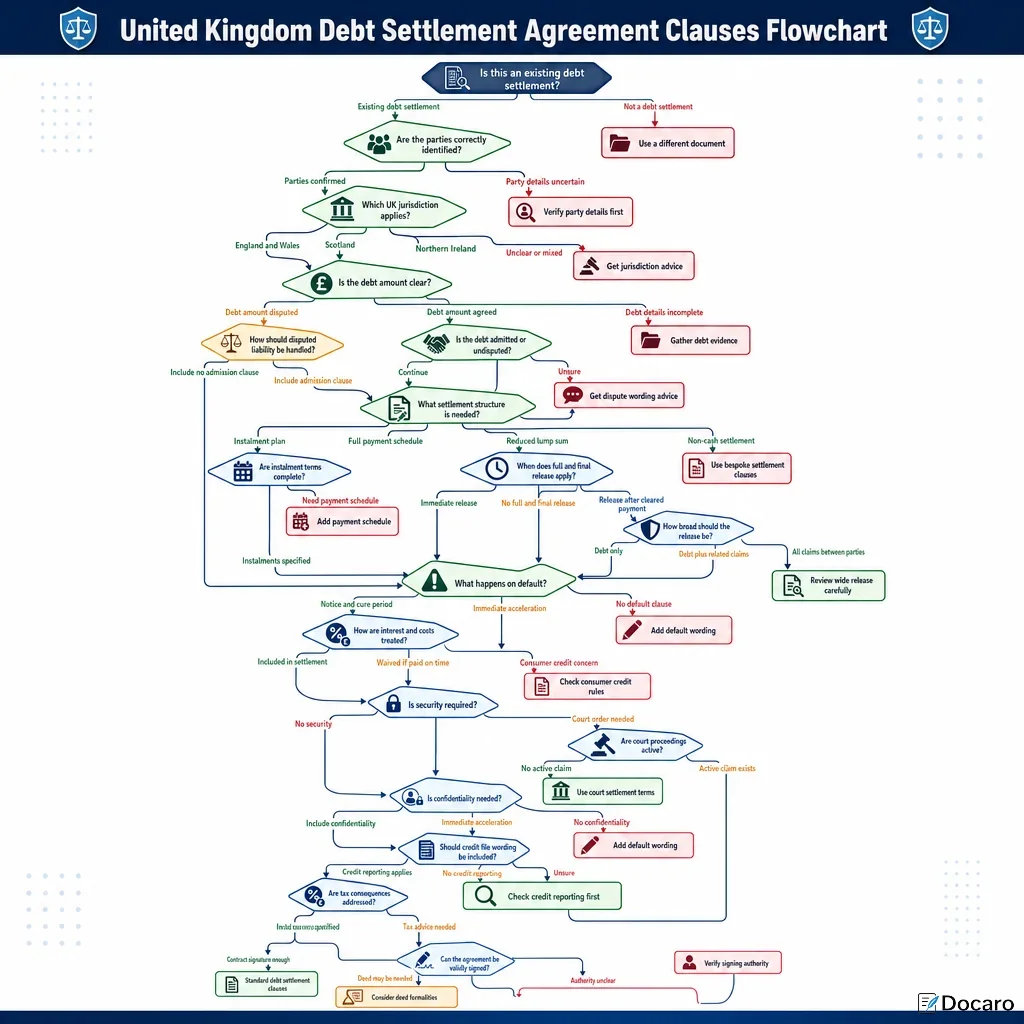

United Kingdom Debt Settlement Agreement Clauses Flowchart

Is this an existing debt settlement?

Why Do The Right Debt Settlement Clauses Matter In The UK?

A debt settlement agreement can decide whether a creditor can recover money and whether a debtor is released from further liability. In the United Kingdom, unclear settlement wording can lead to disputes about the amount owed, whether payment was full and final, what happens after default, and which court has jurisdiction.

How Can Clear Clauses Prevent Future Debt Disputes?

Clear clauses identify the parties, the debt, the payment terms, and the effect of settlement. This reduces the risk that a debtor believes the debt has been settled while the creditor believes a balance, interest, or costs remain outstanding.

Why Is Default Wording Important?

If payments are missed, the agreement should explain the consequences. A well drafted default clause can cover notice, cure periods, acceleration, revived balances, interest, and enforcement. Without it, both sides may face uncertainty and extra cost.

What UK Issues Should A Debt Settlement Agreement Cover?

- Jurisdiction: England and Wales, Scotland, and Northern Ireland have different legal systems.

- Full and final settlement: The release should say when it takes effect and what claims it covers.

- Consumer and credit reporting rules: Credit file wording must be accurate and realistic.

- Court proceedings: Existing claims may need a consent order, Tomlin order, stay, or discontinuance wording.

- Tax and accounting: Debt write-offs and interest may have tax consequences.

For general official guidance, users can review GOV.UK money claim guidance, Citizens Advice debt guidance, and ICO credit information guidance.

FAQs

You Might Also Be Interested In