UK Debt Settlement Repayment Structures

Repayment Structure | How It Works | Complexity Level | Potential Advantages | Potential Risks | Default Risk Level |

|---|---|---|---|---|---|

Single lump sum | |||||

Immediate Full Lump Sum Payment | Debtor pays the agreed settlement amount in one cleared payment on signing or shortly after. | Simple | Fast closure, low administration, low ongoing default risk. | Debtor needs immediate funds creditor may reject if offer is too low. | Low |

Reduced balance settlement | |||||

Discounted Full And Final Lump Sum Settlement | Creditor accepts a lower one-off amount as full settlement and writes off the balance. | Moderate | Clears debt quickly for less than the full balance. | Must confirm balance write-off and credit file treatment in writing. | Low |

Partial Payment With Remaining Balance Preserved | Debtor pays a reduced amount now, but the creditor keeps the right to claim the unpaid balance. | Moderate | Provides immediate cash while preserving creditor rights. | Debtor may wrongly believe the whole debt is settled unless wording is clear. | Medium |

Instalment plan | |||||

Fixed Equal Monthly Instalments | Debt is repaid through equal monthly payments over a fixed period. | Simple | Predictable, easy to budget and simple to monitor. | Missed instalments can delay settlement and require default provisions. | Medium |

Fixed Weekly Instalments | Debtor pays smaller fixed amounts each week until the settlement amount is paid. | Simple | Matches weekly wages and improves short-term affordability. | More payment events increase monitoring and missed-payment risk. | Medium |

Fortnightly Instalments | Debtor pays a fixed amount every two weeks until the agreed sum is cleared. | Simple | Can align with fortnightly pay cycles and reduce monthly cash pressure. | Requires accurate schedule and payment tracking. | Medium |

Quarterly Instalments | Debtor pays larger instalments every three months until completion. | Simple | Useful where income is received quarterly or cash flow is uneven. | Large gaps increase arrears risk and reduce early creditor cash flow. | Medium |

Stepped-Up Instalment Plan | Payments start low and increase at agreed future dates. | Moderate | Helps debtor start paying before income or cash flow improves. | Future higher payments may become unaffordable. | Medium |

Stepped-Down Instalment Plan | Payments start higher and reduce after agreed milestones or dates. | Moderate | Maximises early recovery and helps if debtor expects lower future income. | Initial instalments may be unrealistic and cause early default. | Medium |

Mixed payment arrangement | |||||

Small Instalments With Final Balloon Payment | Debtor pays small regular instalments and a large final payment at the end. | Moderate | Improves short-term affordability while setting a clear final settlement date. | High risk if the debtor cannot fund the final balloon amount. | High |

Upfront Deposit Plus Instalments | Debtor pays an initial amount immediately, then repays the balance by instalments. | Moderate | Shows commitment and gives creditor immediate recovery. | Default can still occur after the initial payment. | Medium |

Deferred payment | |||||

Deferred Lump Sum Payment | Debtor pays one agreed amount on a future fixed date. | Simple | Allows time to raise funds while avoiding multiple instalments. | Creditor receives nothing until the due date funding may not materialise. | High |

Event-Triggered Deferred Payment | Payment becomes due when a defined event occurs, such as a sale, bonus or refinancing. | Complex | Links repayment to a realistic funding source. | Trigger may be delayed, disputed or never occur. | High |

Payment From Property Sale Proceeds | Debt is paid from net proceeds when the debtor sells a property. | Complex | Can produce substantial recovery if sale completes. | Sale delay, insufficient equity and competing secured creditors. | High |

Payment From Refinancing Proceeds | Debtor pays the settlement amount after obtaining new finance or remortgage funds. | Complex | May allow immediate full settlement once funds are released. | Finance may be refused, delayed or subject to conditions. | High |

Payment From Expected Inheritance Or Estate Distribution | Debtor pays when expected estate funds are received. | Complex | Ties repayment to a potentially identifiable future receipt. | Probate delays, disputed entitlement or lower-than-expected distribution. | High |

Payment From Employment Bonus | Settlement is paid from a future bonus or commission payment. | Moderate | Aligns repayment with expected income spike. | Bonus may be discretionary, taxed, reduced or not paid. | High |

Instalment plan | |||||

Seasonal Cash Flow Instalments | Payments are higher in strong trading months and lower or nil in quiet months. | Complex | Reflects genuine seasonal affordability for businesses and sole traders. | Requires detailed schedule and assumptions about trading performance. | Medium |

Income-Contingent Repayment Plan | Payments vary by reference to the debtor’s income during each review period. | Complex | Can be affordable where income fluctuates. | Needs income evidence, review mechanics and dispute handling. | Medium |

Percentage Of Net Profits Repayment | A business debtor pays an agreed percentage of net profits for a defined period. | Complex | Avoids fixed payments that could harm trading viability. | Profit calculation disputes and low recovery if profits fall. | High |

Percentage Of Turnover Or Revenue Sweep | Debtor pays a fixed percentage of turnover until the settlement cap is reached. | Complex | Simpler than profit share and scales with trading receipts. | Needs reporting rights and may strain cash flow despite low margins. | Medium |

Token Payment Plan | Debtor makes small token payments, often temporarily, where little disposable income is available. | Moderate | Maintains contact and shows willingness to pay during hardship. | Debt reduces slowly and creditor may still pursue recovery. | High |

Temporary Reduced Instalments | Creditor accepts lower payments for a limited period before normal or revised payments resume. | Moderate | Gives short-term breathing space without abandoning repayment. | Arrears may grow unless interest and charges are addressed. | Medium |

Mixed payment arrangement | |||||

Payment Holiday Followed By Instalments | No payments are made for an agreed period, then scheduled instalments begin. | Moderate | Allows immediate crisis recovery before repayment starts. | Creditor receives delayed cash and debtor may not recover financially. | High |

Deferred payment | |||||

Moratorium With Review Date | Creditor pauses collection until a review date when repayment terms are reassessed. | Moderate | Useful where affordability is uncertain but expected to improve. | No guaranteed repayment unless follow-on terms are agreed. | High |

Instalment plan | |||||

Interest-Free Instalment Settlement | Creditor freezes interest and charges while debtor pays agreed instalments. | Moderate | Debt reduces predictably and affordability improves. | Agreement should state if interest restarts after default. | Medium |

Instalment Plan With Continuing Interest | Debtor pays instalments while contractual or agreed interest continues to accrue. | Moderate | Compensates creditor for time to payment. | Balance may reduce slowly or increase if payments are too low. | Medium |

Judgment Debt Instalments With Interest Consideration | A judgment debt is paid by instalments, with wording addressing any applicable judgment interest. | Moderate | Can manage enforcement risk while preserving court judgment rights. | Interest and enforcement position must be checked carefully. | Medium |

County Court Judgment Instalment Order | Court may order a judgment debt to be paid by instalments, often after an affordability application. | Moderate | Provides court-recognised payment terms and may reduce immediate enforcement pressure. | Court process and failure to pay may allow enforcement to continue. | Medium |

Tomlin Order Payment Schedule | Court proceedings are stayed on confidential settlement terms set out in a schedule. | Complex | Combines settlement flexibility with easier enforcement if breached. | Requires careful court wording and may need legal advice. | Medium |

Consent Judgment With Stayed Enforcement | Judgment is entered or agreed, but enforcement is stayed while payments are made. | Complex | Gives creditor strong protection and debtor a chance to avoid enforcement. | Judgment affects credit position and enforcement may resume after breach. | Medium |

Reduced balance settlement | |||||

Reduced Instalments With Acceleration On Default | Creditor accepts reduced scheduled payments, but the full balance becomes due if debtor defaults. | Moderate | Encourages compliance and protects creditor if settlement fails. | Harsh default consequences can cause dispute if not clearly drafted. | Medium |

Suspended Balance Write-Off After Completion | Creditor writes off part of the balance only after all agreed payments are made. | Moderate | Rewards completion while protecting creditor during the plan. | Debtor may lose the discount after a minor breach unless cure rights are included. | Medium |

Immediate Write-Off With Instalments On Reduced Balance | Creditor immediately reduces the debt and debtor repays only the reduced balance by instalments. | Moderate | Gives debtor certainty that the old balance will not be revived. | Creditor has weaker protection if debtor defaults later. | Medium |

Instalment plan | |||||

Pro Rata Settlement Across Multiple Creditors | Available money is divided between creditors in proportion to the size of each debt. | Complex | Treats creditors consistently and can support affordability arguments. | Individual creditors may refuse or pursue separate enforcement. | Medium |

Informal Debt Management Plan Payments | Debtor makes affordable regular payments to creditors, often through a debt management plan provider. | Moderate | Can simplify multiple unsecured debt repayments. | Not legally binding on creditors and may affect credit record. | Medium |

Individual Voluntary Arrangement Contributions | Debtor makes agreed contributions under a formal insolvency arrangement supervised by an insolvency practitioner. | Complex | Can bind creditors if approved and may write off remaining qualifying debt. | Formal insolvency consequences, fees and failure risk. | Medium |

Company Voluntary Arrangement Contributions | Company pays creditors under a formal CVA approved by creditors and supervised by an insolvency practitioner. | Complex | Can restructure company debts while trading continues. | Approval thresholds, supervision costs and termination on default. | Medium |

HMRC Time To Pay Arrangement | Tax debt is paid to HMRC by agreed instalments over time. | Moderate | May prevent immediate HMRC enforcement if terms are maintained. | Interest may continue and HMRC can cancel after missed payments. | Medium |

Deferred payment | |||||

Breathing Space Followed By Settlement Plan | Eligible enforcement and contact are paused during breathing space, then settlement terms are agreed or resumed. | Moderate | Creates protected time to obtain debt advice and prepare realistic terms. | It is a pause, not a debt write-off or payment plan by itself. | High |

Instalment plan | |||||

Direct Debit Instalment Plan | Creditor collects agreed instalments automatically from the debtor’s bank account. | Moderate | Reduces missed payments and administration if debtor has stable funds. | Failed collections, indemnity claims and mandate administration. | Low |

Standing Order Instalment Plan | Debtor instructs their bank to send fixed payments to the creditor on set dates. | Simple | Simple recurring payment method controlled by the debtor. | Creditor cannot vary or collect payments debtor can cancel without creditor consent. | Medium |

Post-Dated Cheque Instalments | Debtor provides cheques dated for future instalment dates. | Moderate | Gives creditor payment instruments in advance. | Cheques may bounce and are less practical than electronic payment. | High |

Recurring Card Payment Instalments | Instalments are collected using a continuous card payment authority or recurring card setup. | Moderate | Convenient for online settlement flows and card-based users. | Card expiry, cancellations, chargebacks and failed authorisations. | Medium |

Single lump sum | |||||

Escrowed Lump Sum Settlement | Settlement funds are held by a third party and released when agreed conditions are met. | Complex | Protects both parties where payment and release are conditional. | Escrow fees, condition disputes and release delays. | Low |

Solicitor-Held Completion Funds | Funds are held by a solicitor and released on agreed completion terms. | Complex | Useful for high-value or conditional settlements needing professional handling. | Requires clear stakeholder terms and compliance with solicitors’ accounts rules. | Low |

Third-Party Funded Lump Sum | A family member, investor or other third party provides funds for a one-off settlement. | Moderate | Can unlock full and final settlement where debtor lacks personal savings. | Must clarify payer identity, gift or loan status, and release conditions. | Low |

Instalment plan | |||||

Guarantor-Backed Instalment Plan | Debtor pays by instalments and a guarantor agrees to pay if the debtor defaults. | Complex | Improves creditor security and may justify longer repayment time. | Guarantee enforceability, independent advice and affordability issues. | Low |

Secured Instalment Settlement | Instalment obligations are supported by security over an asset. | Complex | Reduces creditor exposure and may enable more generous terms. | Security documentation, priority and enforcement can be complex. | Low |

Charging Order Supported Repayment | Judgment debt repayment is supported by a charge over land, securities or other qualifying assets. | Complex | Gives creditor security while allowing repayment over time. | Court process, property priority issues and possible order for sale. | Low |

Mixed payment arrangement | |||||

Asset Return Plus Balance Instalments | Debtor returns goods or assets and pays any remaining agreed balance by instalments. | Complex | Reduces outstanding value and may avoid litigation over goods. | Asset valuation, condition disputes and title issues. | Medium |

Reduced balance settlement | |||||

Set-Off Against Mutual Debts | Parties reduce or extinguish amounts owed by offsetting mutual debts. | Complex | Can settle without cash moving both ways. | Disputes over validity, timing and amount of cross-claims. | Low |

Mixed payment arrangement | |||||

Contra Trading Or Services In Lieu | Debtor provides goods or services to reduce or satisfy the debt. | Complex | Useful where debtor lacks cash but has valuable services or stock. | Valuation, VAT, delivery quality and acceptance disputes. | High |

Assignment Of Receivables To Pay Debt | Debtor assigns customer receivables or other debts to the creditor as payment source. | Complex | Links repayment to identifiable income owed to debtor. | Notice, collection, priority and debtor-customer disputes. | Medium |

Invoice Proceeds Sweep | Specified invoices are paid into an account or to the creditor until the settlement is met. | Complex | Can accelerate recovery from business debtor cash receipts. | Customer non-payment and disputes over collected sums. | Medium |

Instalment plan | |||||

Voluntary Payroll Deduction Repayment | With consent, employer deducts agreed sums from wages and pays the creditor or debt account. | Complex | Automated source deduction can reduce missed payments. | Employment, consent, data protection and wage deduction issues. | Low |

Attachment Of Earnings Order Payments | Employer deducts court-ordered amounts from wages to pay a judgment debt. | Complex | Reliable enforcement route for employed judgment debtors. | Requires court process and depends on employment status and protected earnings. | Low |

Single lump sum | |||||

Third Party Debt Order Recovery | Money owed to the debtor by a third party, often a bank, is redirected to satisfy judgment debt. | Complex | Can produce direct recovery from available funds. | Requires court order and may fail if insufficient funds exist. | Low |

Instalment plan | |||||

Controlled Goods Agreement Instalments | Debtor keeps controlled goods while paying enforcement debt by agreed instalments. | Complex | May avoid immediate removal of goods if payments are maintained. | Missed payments may lead to removal and sale of goods plus fees. | Medium |

Mixed payment arrangement | |||||

Arrears Capitalisation Into New Instalment Balance | Arrears are rolled into a revised balance and repaid through a new schedule. | Moderate | Resets the plan and avoids immediate enforcement. | May increase total cost and extend indebtedness. | Medium |

Instalment plan | |||||

Catch-Up Instalments For Arrears | Normal payments continue and extra sums are added until arrears are cleared. | Moderate | Repairs default without rewriting the whole agreement. | Higher short-term payments may be unaffordable. | Medium |

Instalment Plan With Grace Period | Late payment is not a default if cured within a short agreed grace period. | Moderate | Reduces disputes over minor delays and bank processing issues. | Repeated late payments may undermine creditor confidence. | Medium |

Reduced balance settlement | |||||

Early Payment Discount Settlement | Debtor pays by an early deadline to receive an agreed discount. | Simple | Incentivises fast payment and improves creditor cash flow. | Deadline and discount loss consequences must be clear. | Low |

Prompt Payment Rebate After Completion | Debtor pays the full scheduled amount but receives a rebate after timely completion. | Moderate | Encourages compliance while protecting creditor until the end. | Rebate conditions can be disputed if not precise. | Low |

Single lump sum | |||||

Release Only After Cleared Funds | Creditor’s release takes effect only when settlement funds have cleared irrevocably. | Simple | Protects creditor against failed transfers or reversed payments. | Debtor may need proof of payment and exact release timing. | Low |

Simultaneous Payment And Release Exchange | Payment and release documents are exchanged at the same completion meeting or time. | Moderate | Balances settlement risk between debtor and creditor. | Requires coordination and clear completion mechanics. | Low |

Mixed payment arrangement | |||||

Non-Cash Asset Transfer Settlement | Debtor transfers agreed assets instead of, or alongside, cash payment. | Complex | Can settle where debtor holds valuable but illiquid assets. | Valuation, title, tax, volatility and transfer risk. | High |

Stock Transfer Against Debt | Business debtor transfers stock at an agreed valuation to reduce the debt. | Complex | Provides value where cash is unavailable. | Valuation, ownership, quality, VAT and resale risk. | Medium |

Reduced balance settlement | |||||

Debt-For-Equity Settlement | Creditor accepts shares or equity rights in place of some or all cash repayment. | Complex | Can preserve cash and give creditor upside if the business recovers. | Valuation, dilution, shareholder rights and regulatory issues. | High |

Deferred payment | |||||

Replacement Loan Note Settlement | Old debt is replaced by a new loan note with revised maturity and payment terms. | Complex | Creates formal long-term repayment instrument with clearer investor rights. | May amount to complex refinancing and require specialist drafting. | Medium |

Mixed payment arrangement | |||||

Third-Party Assumption Or Novation Of Debt | A third party assumes payment obligations, with creditor consent, replacing or joining the original debtor. | Complex | May improve repayment prospects if new payer is stronger. | Release, consent and continuing liability must be precise. | Medium |

Instalment plan | |||||

Joint Debtor Split Instalments | Co-debtors each pay agreed shares of the settlement schedule. | Complex | Allocates payment responsibility between multiple debtors. | One debtor’s default may affect all unless liability rules are clear. | Medium |

Reduced balance settlement | |||||

Several Liability Settlement Shares | Each debtor settles only their agreed share and receives a separate release for that share. | Complex | Allows partial resolution where co-debtors have different affordability. | Must preserve or release claims against other debtors clearly. | Medium |

Instalment plan | |||||

Hardship Review Instalment Plan | Payments are reviewed periodically against the debtor’s hardship circumstances and affordability. | Complex | Supports realistic repayment for vulnerable or financially distressed debtors. | Variable terms require evidence, review process and clear discretion limits. | Medium |

Regulated Consumer Credit Arrears Arrangement | A regulated lender agrees affordable arrears repayment terms for a consumer credit borrower. | Complex | Can align debt recovery with FCA expectations on fair treatment and forbearance. | Regulatory compliance, notices and affordability assessment may be required. | Medium |

Mixed payment arrangement | |||||

Consumer Credit Agreement Variation Settlement | Repayment terms of a regulated consumer credit agreement are varied or compromised by agreement. | Complex | Can restructure consumer credit debt while keeping statutory rights in view. | Consumer Credit Act compliance, notices and enforceability issues. | Medium |

Reduced balance settlement | |||||

Settlement Conditional On Credit File Update | Debtor pays agreed amount and creditor updates credit reporting as settled or partially settled. | Moderate | Addresses a key debtor concern and documents reporting expectations. | Credit reference agency reporting may show partial settlement and historic defaults. | Low |

Instalment plan | |||||

Confidential Staged Settlement Payments | Debtor pays staged sums while the settlement amount and terms remain confidential. | Moderate | Useful for commercial disputes where public terms could affect negotiations. | Confidentiality exceptions and enforcement disclosure must be drafted. | Medium |

Legal Costs Debt Instalment Settlement | Assessed, agreed or ordered legal costs are paid over time by scheduled instalments. | Moderate | Avoids immediate costs enforcement while preserving payment timetable. | Interest, enforcement and assessment status must be addressed. | Medium |

Rent Arrears Repayment Plan | Tenant pays ongoing rent plus agreed arrears instalments. | Moderate | May help preserve tenancy and avoid possession action. | Non-payment of rent or arrears may still lead to possession proceedings. | High |

Service Charge Arrears Instalments | Leaseholder pays service charge arrears by agreed instalments alongside current charges. | Moderate | Can avoid escalation to forfeiture or debt proceedings. | Current charges may continue to accrue and lease terms may add costs. | Medium |

Reduced balance settlement | |||||

Mortgage Shortfall Settlement Plan | Former borrower settles a mortgage shortfall by lump sum, instalments or reduced balance compromise. | Complex | Can resolve a significant post-sale debt for less than the claimed balance. | Limitation, interest, secured lender policy and credit reporting issues. | Medium |

Instalment plan | |||||

Council Tax Arrears Repayment Plan | Debtor agrees instalments with the council to clear overdue council tax. | Moderate | May avoid or pause enforcement action if accepted and maintained. | Councils can use enforcement powers if payments are missed. | High |

Utility Arrears Payment Plan | Energy or utility arrears are repaid through an affordable plan agreed with the supplier. | Moderate | Can spread arrears and maintain supply arrangements. | Ongoing usage costs continue and affordability must be reviewed. | Medium |

Hire Purchase Arrears Repayment Plan | Borrower pays missed hire purchase instalments while maintaining or varying the agreement. | Complex | May avoid termination or repossession if lender agrees. | Consumer credit protections, default notices and goods repossession rules may apply. | High |

High-Cost Credit Affordable Repayment Plan | High-cost credit debt is repaid over time under affordable terms agreed with the lender. | Complex | Can reduce immediate pressure and align repayments with affordability. | Regulated credit rules, interest, charges and complaints issues may arise. | Medium |

Supplier Debt Trade Repayment Plan | Business repays supplier arrears over time, often while new orders are on cash terms. | Moderate | Can preserve trading relationship and supply continuity. | New credit exposure and retention of title issues may remain. | Medium |

Mixed payment arrangement | |||||

Cash-On-Delivery Plus Arrears Instalments | Debtor pays for new goods immediately and pays old arrears by scheduled instalments. | Moderate | Limits new debt while enabling continued supply. | Operational pressure if debtor cannot fund both current and arrears payments. | Medium |

Instalment plan | |||||

Licence Fee Or Royalty Arrears Instalments | Accrued licence fees or royalties are paid over time under a revised schedule. | Moderate | Maintains commercial licence while arrears are cleared. | Termination rights, audit rights and future royalty reporting must align. | Medium |

Deferred payment | |||||

Payment From Insurance Proceeds | Debt is paid when a pending insurance claim is admitted and proceeds are received. | Complex | Connects repayment to a specific expected external payment. | Claim may be declined, delayed, reduced or paid to another party. | High |

Payment From Litigation Or Claim Proceeds | Debt is paid from damages, settlement proceeds or compensation received by the debtor. | Complex | Uses an identifiable recovery source without immediate debtor cash. | Underlying claim may fail, settle low or be absorbed by legal costs. | High |

Mixed payment arrangement | |||||

Asset Sale Lump Sum Plus Instalments | Debtor pays an initial sum from asset sale and clears the remainder by instalments. | Complex | Combines immediate recovery with manageable balance repayment. | Sale proceeds may be lower than expected and instalments may still fail. | Medium |

Minimum Instalment Plus Surplus Sweep | Debtor pays a fixed minimum and additional amounts when surplus cash is available. | Complex | Ensures baseline recovery while accelerating repayment in good periods. | Surplus definition and reporting can be contentious. | Medium |

Reduced balance settlement | |||||

Capped Instalment Settlement | Debtor pays instalments only until an agreed settlement cap is reached. | Moderate | Gives debtor certainty on maximum amount payable. | Creditor must accept lower recovery if cap is below full balance. | Medium |

Instalment plan | |||||

Open-Ended Affordable Payments Until Review | Debtor pays an affordable amount indefinitely until formal review or renegotiation. | Moderate | Flexible where future circumstances are uncertain. | No clear end date and debt may persist for years. | Medium |

Reduced balance settlement | |||||

Payments For Fixed Term Then Review Write-Off | Debtor pays what is affordable for a fixed term, then creditor reviews and may write off the balance. | Complex | Balances affordability with possible final closure. | Write-off is uncertain unless objective conditions are agreed. | Medium |

Token Payments Then Compassionate Write-Off | Debtor makes small payments or provides evidence of hardship before creditor agrees a write-off. | Complex | Can resolve debts where long-term repayment is unrealistic. | Creditor discretion, evidence burden and credit file consequences. | High |

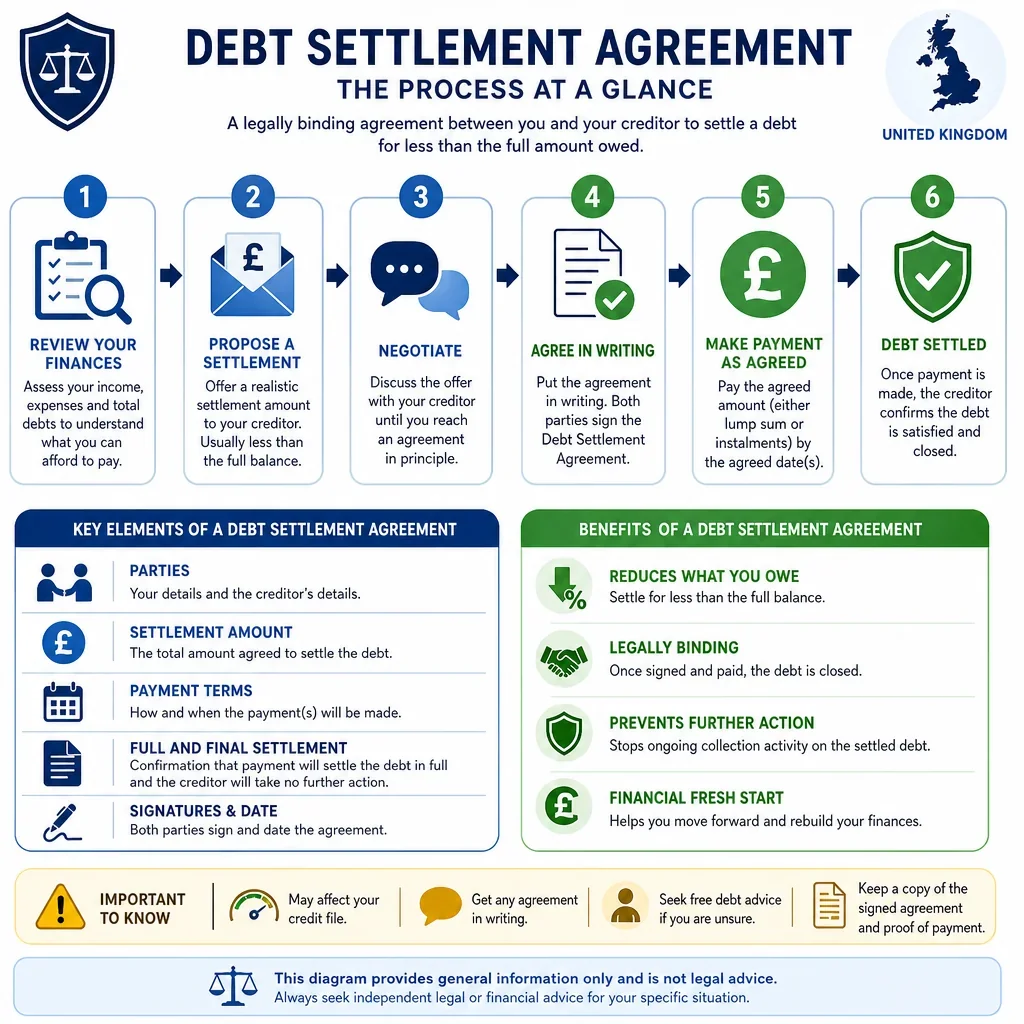

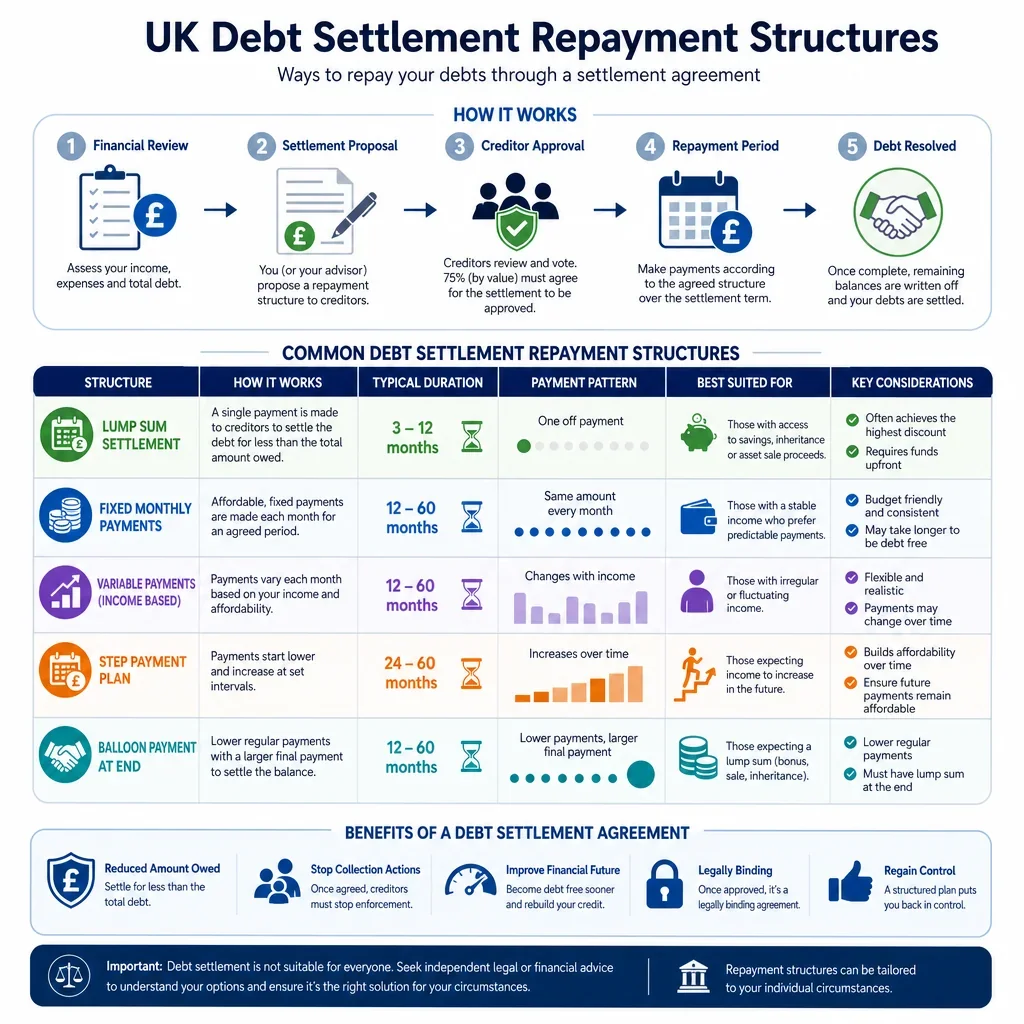

What Repayment Structure Is Usually Best For A UK Debt Settlement Agreement?

Lump sum settlements are usually the simplest to document and have the lowest ongoing default risk, because the creditor gives the release only after receiving cleared funds. They are often suitable where the debtor has access to savings, refinancing or third-party support.

Instalment plans can make settlement affordable, but they need more detailed drafting: exact due dates, payment method, missed-payment consequences, whether interest is frozen, and when the debt is treated as finally settled.

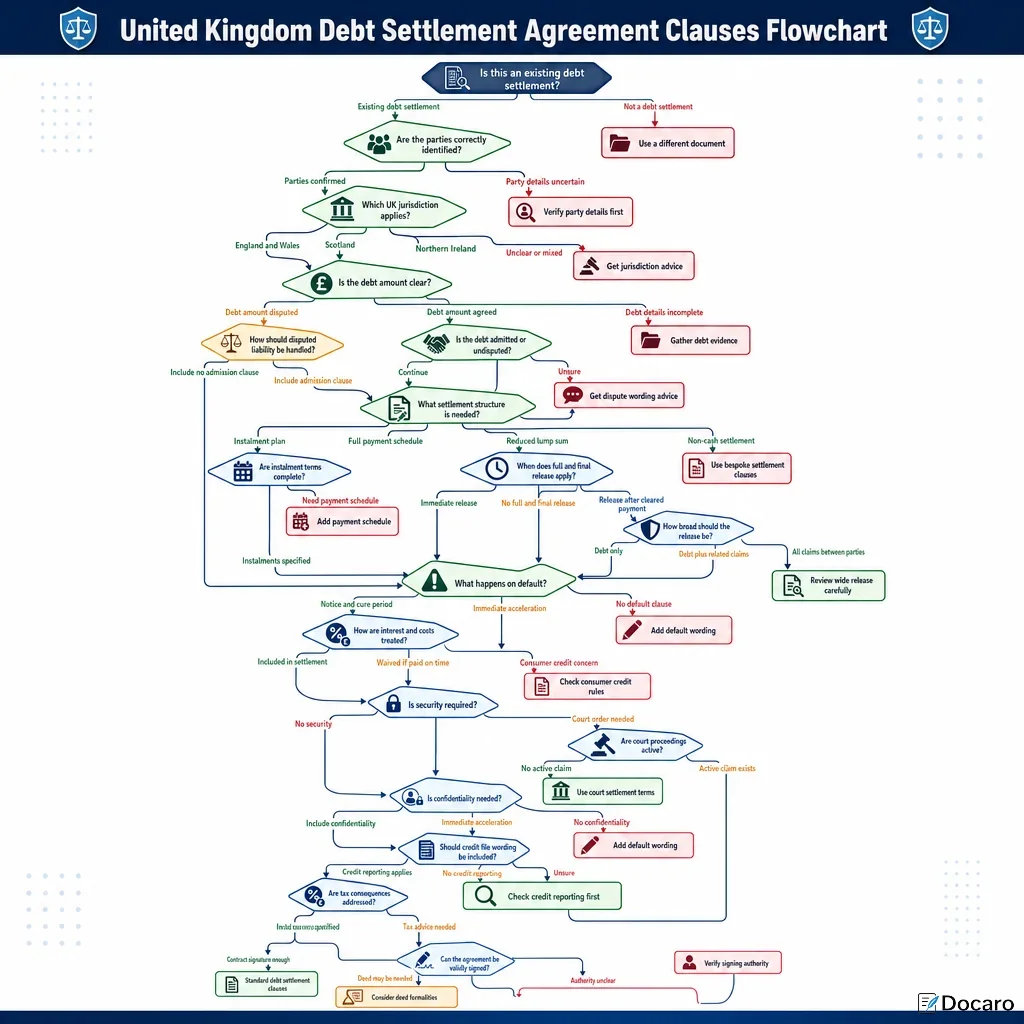

When Should A Debt Settlement Agreement Include Stronger Protections?

- Long-term, back-loaded, income-contingent or seasonal plans usually carry higher default risk and should include review dates, information obligations, cure periods and clear acceleration wording.

- Reduced balance settlements should state whether payment is accepted in full and final settlement, whether any balance is written off, and when credit file reporting will be updated.

- Deferred payments should identify the trigger date or event precisely, such as completion of a property sale, receipt of bonus, or insurance payout.

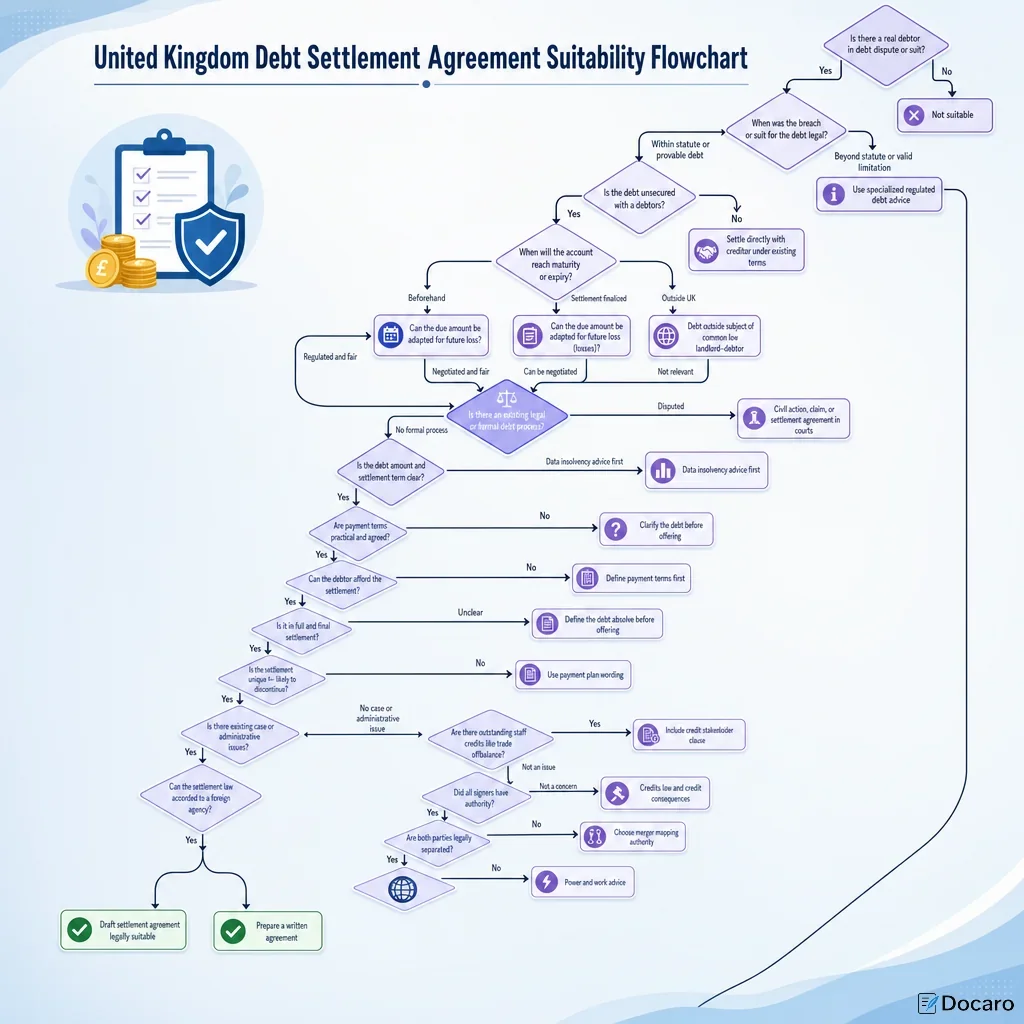

What UK Legal And Regulatory Issues Commonly Affect Repayment Structures?

Where the debt is consumer credit, parties should consider whether the arrangement is regulated by the Consumer Credit Act 1974 and FCA consumer credit rules. If the debtor is an individual in financial difficulty, affordability and fair treatment are especially important. Court judgment debts may also be affected by enforcement rules and procedures, including instalment orders under the County Courts Act 1984.

For higher-risk structures, a debt settlement agreement should avoid vague promises and record the commercial bargain clearly: amount payable, timing, method, concessions, default consequences, release wording and any security or guarantee.

FAQs

You Might Also Be Interested In