United Kingdom Debt Settlement Agreement Information Checklist

Required Item | Reason Needed | Importance Level | Likely Source | Example Evidence |

|---|---|---|---|---|

Party details | ||||

Creditor legal name | Identifies who is releasing or compromising the debt. | Essential | Creditor | Company record, invoice header, credit agreement, statement. |

Debtor legal name | Identifies who must pay and receive the release. | Essential | Debtor | Passport, driving licence, utility bill, company record. |

Current addresses for all parties | Needed for notices, service, and clear identification. | Essential | Either party | Recent bill, bank statement, Companies House address. |

Company number for any company party | Avoids confusion between companies with similar names. | Essential | Third party record | Companies House register extract. |

Trading names or former names | Links the settlement to invoices or accounts in other names. | Recommended | Either party | Invoices, business letters, Companies House history. |

Legal and administrative details | ||||

Authority of signatories | Confirms each person can bind the party signing. | Essential | Either party | Board approval, director details, power of attorney. |

Party details | ||||

Details of any joint debtors | Determines who is released and who remains liable. | Depends on circumstances | Either party | Joint loan agreement, account terms, court claim. |

Details of guarantors or indemnifiers | Prevents unintended release or preserves guarantor liability. | Depends on circumstances | Creditor | Guarantee, indemnity, director guarantee, security documents. |

Legal and administrative details | ||||

Insolvency status of each party | May affect authority to settle and enforceability. | Recommended | Third party record | Individual Insolvency Register, Companies House insolvency filings. |

Party details | ||||

Executor or administrator details | Needed if debtor or creditor is deceased. | Depends on circumstances | Either party | Grant of probate, letters of administration. |

Debt details | ||||

Type of debt | Determines suitable settlement wording and legal checks. | Essential | Either party | Loan, invoice, rent arrears, credit card, services debt. |

Original contract or credit agreement | Shows the source, terms, and parties to the debt. | Essential | Creditor | Signed contract, loan agreement, order form, terms. |

Account, invoice, or reference number | Precisely identifies the debt being settled. | Essential | Creditor | Account statement, invoice, debt collection letter. |

Original principal amount | Shows the starting balance before interest or payments. | Essential | Creditor | Loan advance, invoice total, opening statement. |

Current outstanding balance | Records the amount being compromised or paid. | Essential | Creditor | Recent statement, ledger, balance confirmation. |

Breakdown of principal, interest, fees, and charges | Clarifies what is waived and what is still payable. | Recommended | Creditor | Statement of account, ledger, interest calculation. |

Interest rate and interest basis | Determines whether interest is included, stopped, or waived. | Recommended | Creditor | Contract clause, credit agreement, statement calculation. |

Any statutory interest claim | Shows whether court or late payment interest is included. | Depends on circumstances | Creditor | Claim form, particulars of claim, interest schedule. |

Late commercial payment interest or compensation | Identifies statutory sums to include or waive. | Depends on circumstances | Creditor | Late payment interest schedule, business invoices. |

Evidence and records | ||||

Payment history | Confirms prior payments and remaining balance. | Essential | Either party | Bank statements, receipts, account ledger, remittance advice. |

Debt details | ||||

Date of last payment | Relevant to limitation and settlement context. | Recommended | Either party | Bank record, receipt, creditor ledger. |

Evidence and records | ||||

Any written acknowledgement of the debt | May affect limitation and admissions wording. | Recommended | Either party | Email admitting debt, signed letter, repayment proposal. |

Legal and administrative details | ||||

Key limitation dates | Helps assess whether the debt may be time-barred. | Recommended | Either party | Contract date, default date, last payment, acknowledgement. |

Scottish prescription position | Scotland has different time-bar rules for obligations. | Depends on circumstances | Either party | Scottish contract, last relevant claim or payment dates. |

Payment details | ||||

Agreed settlement amount | Core commercial term of the settlement. | Essential | Either party | Settlement offer, email acceptance, term sheet. |

Full and final or part settlement basis | Defines whether any balance is released. | Essential | Either party | Written offer terms, negotiation emails. |

Lump sum or instalment structure | Sets how the settlement amount must be paid. | Essential | Either party | Payment schedule, settlement offer, affordability plan. |

Payment due dates | Makes timing obligations clear and enforceable. | Essential | Either party | Agreed schedule, calendar dates, instalment table. |

Payment method | Reduces disputes over how payment must be made. | Recommended | Either party | Bank transfer, card payment, standing order, cheque. |

Creditor bank account details | Ensures payment reaches the correct account. | Essential | Creditor | Bank details letter, invoice, secure payment instruction. |

Required payment reference | Helps allocate funds to the correct debt. | Recommended | Creditor | Account number, invoice number, case reference. |

Cleared funds requirement | Clarifies when settlement takes effect. | Recommended | Creditor | Settlement condition, bank confirmation, receipt wording. |

Consequences of missed or late payment | States whether original debt revives or balance accelerates. | Essential | Either party | Default clause, grace period, acceleration wording. |

Any grace period for late payment | Avoids disproportionate default for minor delays. | Optional | Either party | Agreed term allowing 3, 5, or 7 days. |

Whether time is of the essence | Clarifies strictness of payment deadlines. | Recommended | Either party | Express settlement term, negotiation emails. |

Debtor affordability information | Supports realistic instalments and reduces default risk. | Recommended | Debtor | Income and expenditure form, payslips, bank statements. |

Legal and administrative details | ||||

Tax treatment of written-off amount | May affect accounting, VAT, or taxable income positions. | Depends on circumstances | Either party | Accountant advice, VAT invoice, credit note. |

VAT position on the underlying supply | May require credit notes or affect settlement accounting. | Depends on circumstances | Creditor | VAT invoice, credit note, accountant advice. |

Debt details | ||||

Whether liability or amount is disputed | Determines admission, no-admission, and compromise wording. | Essential | Either party | Dispute letters, complaint emails, defence, mediation notes. |

Legal and administrative details | ||||

Need for no-admission wording | Protects a party settling a disputed claim. | Depends on circumstances | Either party | Settlement negotiations, dispute correspondence. |

Evidence and records | ||||

Without prejudice settlement correspondence | Shows agreed terms while preserving negotiation status. | Recommended | Either party | Offer letters, emails marked without prejudice. |

Evidence of assignment or sale of debt | Confirms current creditor has rights to settle. | Depends on circumstances | Creditor | Deed of assignment, notice of assignment, sale letter. |

Legal and administrative details | ||||

Debt collector authority to settle | Checks agent can bind the creditor to the compromise. | Depends on circumstances | Creditor | Agency authority, creditor confirmation, collection letter. |

Whether the debt is regulated consumer credit | Regulated debts may need extra compliance checks. | Depends on circumstances | Creditor | Credit agreement, pre-contract information, statements. |

FCA authorisation status for creditor or collector | Relevant for regulated debt collection and credit activities. | Depends on circumstances | Third party record | FCA Register entry, firm reference number. |

Evidence and records | ||||

Consumer credit default notice history | May affect enforcement of regulated credit debts. | Depends on circumstances | Creditor | Default notice, termination letter, arrears notices. |

Legal and administrative details | ||||

Any active complaint or ombudsman case | Settlement may need to include complaint resolution terms. | Depends on circumstances | Either party | Complaint correspondence, FOS reference, final response. |

Details of any court proceedings | Settlement should address stay, discontinuance, or judgment. | Depends on circumstances | Either party | Claim form, defence, order, judgment, case number. |

County Court judgment or other judgment details | Determines satisfaction, enforcement, and credit record wording. | Depends on circumstances | Either party | Judgment order, CCJ register entry, court correspondence. |

Evidence and records | ||||

Register of judgments search result | Verifies whether a judgment is registered. | Optional | Third party record | TrustOnline search result or register extract. |

Legal and administrative details | ||||

Current enforcement action | Settlement should pause, withdraw, or satisfy enforcement. | Depends on circumstances | Either party | Warrant, writ, attachment, charging order, bailiff notice. |

Debt details | ||||

Court fees and legal costs position | Clarifies whether costs are included or waived. | Depends on circumstances | Creditor | Costs schedule, judgment, court fee receipt, solicitor bill. |

Legal and administrative details | ||||

Need for a Tomlin order or consent order | May be needed to settle live court proceedings. | Depends on circumstances | Either party | Draft order, claim number, schedule of terms. |

Discontinuance or withdrawal requirements | Sets how court action ends after settlement. | Depends on circumstances | Creditor | Notice of discontinuance, consent, court order. |

Scottish decree or Simple Procedure case details | Scottish proceedings need different settlement handling. | Depends on circumstances | Either party | Simple Procedure claim, decree, court correspondence. |

Northern Ireland court claim or decree details | Northern Ireland procedure may affect settlement steps. | Depends on circumstances | Either party | Small claim, civil bill, decree, court correspondence. |

Debt details | ||||

Details of any security for the debt | Determines whether charges or security are released. | Depends on circumstances | Creditor | Mortgage, charge, debenture, Land Registry title. |

Evidence and records | ||||

Land Registry title and charge entries | Verifies property charges affected by settlement. | Depends on circumstances | Third party record | Official copy register, title plan, charge entry. |

Registered company charge details | Shows security registered against a company debtor. | Depends on circumstances | Third party record | Companies House charge register, MR01, satisfaction filing. |

Legal and administrative details | ||||

Security release requirements | Sets documents needed to discharge charges after payment. | Depends on circumstances | Creditor | DS1, deed of release, Companies House satisfaction filing. |

Rights reserved against non-settling parties | Preserves claims against co-debtors or guarantors if intended. | Depends on circumstances | Creditor | Guarantee, joint liability clause, reservation wording. |

Credit reference agency reporting position | Records agreed updates after payment or settlement. | Depends on circumstances | Creditor | Credit file entry, creditor reporting policy, CRA records. |

Agreed credit file update wording | Avoids disagreement over satisfied or partially settled status. | Depends on circumstances | Either party | Settlement letter, credit file screenshot, CRA guidance. |

Evidence and records | ||||

Receipt or completion confirmation | Proves settlement payment and release completion. | Recommended | Creditor | Paid receipt, balance zero letter, email confirmation. |

Legal and administrative details | ||||

Personal data handling requirements | Needed where sharing financial and identity data. | Recommended | Either party | Privacy notice, consent record, data processing policy. |

Confidentiality requirements | Controls disclosure of settlement terms. | Optional | Either party | Confidentiality clause, permitted disclosure list. |

Non-disparagement requirement | May be relevant for business debt disputes. | Optional | Either party | Agreed public statement, reputation clause. |

Debt details | ||||

Whether the debt is owed to HMRC | HMRC debts require specific time-to-pay processes. | Depends on circumstances | Debtor | HMRC demand, tax account, time-to-pay agreement. |

Tenancy or lease details for rent arrears | Rent arrears settlements may affect possession or deposit issues. | Depends on circumstances | Either party | Tenancy agreement, rent statement, deposit record. |

Public authority debt details | Public debts may have statutory recovery processes. | Depends on circumstances | Debtor | Council tax bill, liability order, repayment plan. |

Student loan debt status | Student loans have specific repayment and write-off rules. | Depends on circumstances | Debtor | Student Loans Company statement, repayment plan. |

Benefit overpayment recovery details | Benefit overpayments may have special recovery rules. | Depends on circumstances | Debtor | DWP letter, overpayment decision, repayment schedule. |

Whether the debt is a priority debt | Priority debts may carry serious non-payment consequences. | Recommended | Debtor | Mortgage arrears, rent arrears, council tax, utilities. |

Legal and administrative details | ||||

Debt adviser or solicitor involvement | Useful for communications and vulnerability handling. | Optional | Debtor | Authority to act, adviser letter, solicitor details. |

Breathing Space moratorium status | May restrict collection action and interest during moratorium. | Depends on circumstances | Debtor | Breathing Space notification, debt adviser confirmation. |

Debt Relief Order status | May prevent normal settlement or collection of included debts. | Depends on circumstances | Debtor | DRO notice, Insolvency Service record. |

Individual Voluntary Arrangement status | Settlement may require supervisor involvement or approval. | Depends on circumstances | Debtor | IVA proposal, supervisor letter, insolvency register entry. |

Bankruptcy status | Trustee or official receiver may control settlement. | Depends on circumstances | Third party record | Bankruptcy order, official receiver letter, register entry. |

Company liquidation, administration, or CVA status | Insolvency office-holder may need to approve settlement. | Depends on circumstances | Third party record | Companies House filings, administrator notice, CVA proposal. |

Debtor vulnerability or reasonable adjustment needs | Supports fair handling and suitable communications. | Depends on circumstances | Debtor | Adjustment request, adviser letter, communication preferences. |

Notice and communication details | States where formal notices must be sent. | Recommended | Either party | Postal address, email address, solicitor contact. |

Governing law and jurisdiction preference | Important where parties or assets are in different UK nations. | Recommended | Either party | Original contract clause, settlement term sheet. |

Signing method and execution requirements | Determines wet ink, e-signature, deed, or witness needs. | Recommended | Either party | Execution block, board minutes, witness details. |

Whether settlement should be executed as a deed | May be useful where consideration or release issues arise. | Depends on circumstances | Either party | Legal advice, deed execution blocks, witness details. |

Consideration for the settlement | Supports enforceability of compromise terms. | Recommended | Either party | Payment promise, early payment, mutual release, deed. |

Scope of release | Defines claims, interest, fees, and parties released. | Essential | Either party | Release wording, list of debts, reserved claims. |

Whether releases are mutual or creditor-only | Clarifies whether both sides give up claims. | Recommended | Either party | Dispute summary, counterclaim details, release clause. |

Debt details | ||||

Any debtor counterclaim or set-off | May affect settlement amount and release wording. | Depends on circumstances | Debtor | Counterclaim letter, defective goods evidence, defence. |

Evidence and records | ||||

Underlying goods or services dispute evidence | Explains why a reduced settlement is agreed. | Depends on circumstances | Debtor | Complaint emails, photos, expert report, refund request. |

Mediation or ADR outcome | May contain agreed settlement terms or confidentiality duties. | Optional | Either party | Mediation agreement, settlement note, ADR correspondence. |

Previous settlement offers | Avoids inconsistency with earlier agreed or rejected terms. | Recommended | Either party | Offer emails, letters, call notes, term sheet. |

Any verbal settlement discussions | Helps confirm or correct the written terms. | Optional | Either party | Call notes, meeting minutes, follow-up email. |

Party details | ||||

Solicitor or representative contact details | Ensures notices and drafts go to authorised representatives. | Optional | Either party | Engagement letter, authority to act, solicitor email. |

Identity verification documents | Reduces fraud risk and confirms party identity. | Recommended | Either party | Passport, photocard licence, proof of address. |

Payment details | ||||

Source of funds for settlement payment | May be required for AML checks on larger payments. | Depends on circumstances | Debtor | Bank statement, sale completion statement, payslips. |

Legal and administrative details | ||||

Sanctions screening result | Helps avoid prohibited payments to sanctioned persons. | Depends on circumstances | Third party record | OFSI consolidated list search, compliance check record. |

Payment details | ||||

Payment currency | Avoids exchange rate disputes for non-sterling debts. | Recommended | Either party | Contract currency clause, invoice, settlement offer. |

Party details | ||||

Overseas party or asset details | May affect governing law, service, and enforcement terms. | Depends on circumstances | Either party | Foreign address, overseas company extract, asset details. |

Payment details | ||||

Exchange rate calculation method | Needed if debt or payment is in different currencies. | Depends on circumstances | Either party | Bank of England rate, bank quote, agreed rate table. |

Legal and administrative details | ||||

Whether complaints are included in the release | Important where financial, consumer, or service complaints exist. | Depends on circumstances | Either party | Complaint reference, final response, settlement wording. |

Known claims to exclude from release | Prevents accidental waiver of unrelated claims. | Recommended | Either party | Reserved rights list, separate dispute documents. |

Documents or property to return | May form part of settlement performance. | Optional | Either party | Original title documents, goods, keys, account cards. |

Payment details | ||||

Direct debit or standing order cancellation details | Prevents unintended payments after settlement. | Optional | Debtor | Bank instruction, mandate reference, cancellation confirmation. |

Refund process for overpayments | Covers accidental excess payments after settlement. | Optional | Either party | Refund clause, bank details, reconciliation statement. |

Allocation of settlement payment among multiple debts | Avoids uncertainty where several accounts exist. | Depends on circumstances | Creditor | Account list, allocation table, creditor statement. |

Party details | ||||

Details of multiple creditors | Ensures all necessary releasing parties sign. | Depends on circumstances | Either party | Syndicated loan, joint invoice, assignment chain. |

Legal and administrative details | ||||

Account closure requirements | Confirms whether the account ends after settlement. | Optional | Creditor | Closure letter, zero balance statement, account terms. |

Effect on ongoing supply or services | Important if creditor continues trading with debtor. | Depends on circumstances | Either party | Service contract, future payment terms, supply suspension notice. |

Factual confirmations or warranties required | Records reliance on facts such as authority and balance. | Recommended | Either party | Balance warranty, authority warranty, no assignment warranty. |

Prior agreements to supersede or preserve | Clarifies whether earlier settlement terms still apply. | Recommended | Either party | Earlier repayment plan, forbearance letter, side agreement. |

Process for varying the settlement | Controls later changes to payment dates or amounts. | Recommended | Either party | Written variation clause, email approval requirement. |

Whether independent legal advice was obtained | Useful for significant, disputed, or vulnerable-party settlements. | Optional | Either party | Solicitor certificate, advice confirmation, engagement email. |

Evidence and records | ||||

Evidence settlement is voluntary | Reduces risk of later challenge for pressure or unfairness. | Recommended | Either party | Cooling-off time, advice record, clear written acceptance. |

Legal and administrative details | ||||

Translation or accessibility needs | Helps ensure parties understand the settlement terms. | Depends on circumstances | Either party | Interpreter details, translated draft, accessibility request. |

Capacity or protected party issues | May require representative authority or court approval. | Depends on circumstances | Either party | Power of attorney, deputyship order, litigation friend details. |

Mental capacity concerns | Affects ability to enter a binding settlement. | Depends on circumstances | Either party | Capacity assessment, deputyship order, attorney authority. |

Party details | ||||

Power of attorney authority | Confirms an attorney can sign for a party. | Depends on circumstances | Either party | LPA, EPA, ordinary power of attorney, access code. |

Legal and administrative details | ||||

Agreement date and effective date | Shows when obligations and releases start. | Essential | Either party | Signed agreement, dated acceptance, completion email. |

Payment details | ||||

Conditions before release becomes effective | Clarifies whether release depends on full payment or other acts. | Recommended | Either party | Cleared funds clause, withdrawal of claim, signed deed. |

Legal and administrative details | ||||

Post-settlement actions and deadlines | Tracks credit file updates, court filings, and releases. | Recommended | Either party | Action list, filing deadline, CRA update confirmation. |

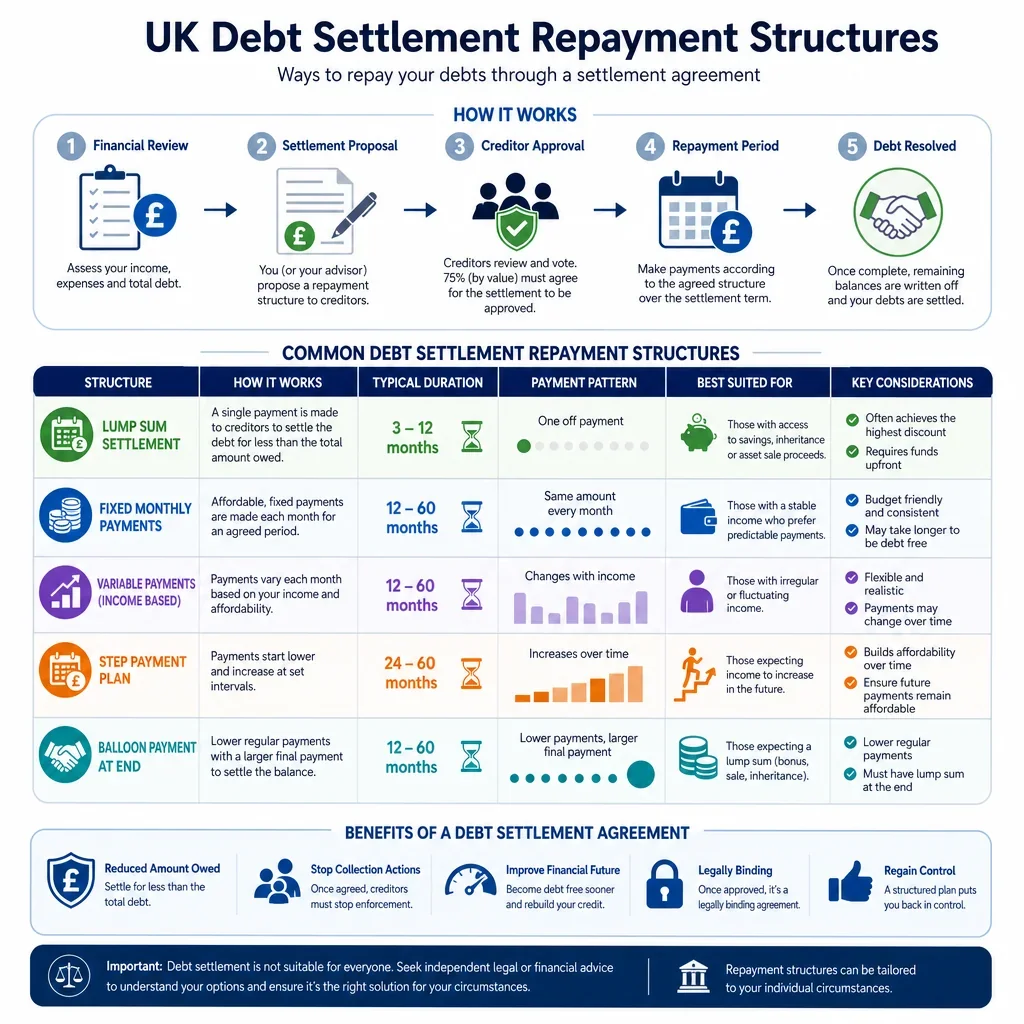

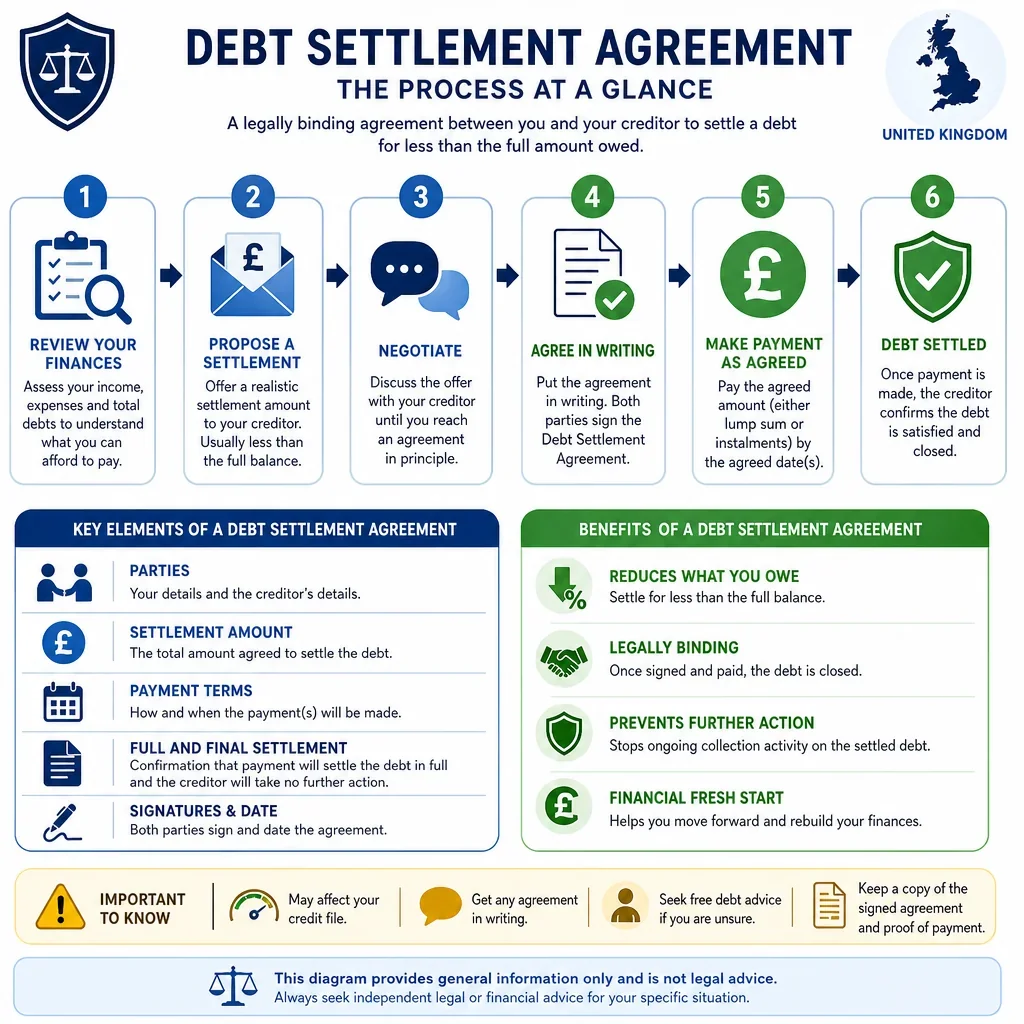

What Information Do You Need Before Preparing A UK Debt Settlement Agreement?

A useful debt settlement agreement should identify the parties, the debt, the settlement amount, payment dates, and what happens if payment is late or incomplete. For UK use, it is also important to check whether the debt is regulated consumer credit, secured, disputed, already subject to court proceedings, or close to limitation, as these facts can change the wording and risk profile of the agreement.

Why Is Evidence Of The Debt Important?

The agreement should be based on reliable records such as invoices, loan agreements, statements, account ledgers, correspondence, or court documents. Evidence helps confirm the amount owed, whether interest or fees are being compromised, and whether the creditor can safely state that the settlement is in full and final settlement.

What UK Legal Checks Matter Most?

- Limitation: in England and Wales, many simple contract debts have a six-year limitation period, so dates of last payment or written acknowledgement can be important.

- Consumer credit: regulated credit debts may require special care, including checking the original agreement, statements, default notice history, and any FCA-regulated collection activity.

- Court claims or judgments: if there is a CCJ, decree, charging order, warrant, attachment, or enforcement action, the settlement should say how those proceedings will be stayed, discontinued, satisfied, or updated.

- Security and guarantees: mortgages, charges, personal guarantees, or co-debtors should be expressly dealt with so that rights are not released accidentally.

What Should Be Agreed About Payment?

The parties should record whether payment is by lump sum or instalments, the due dates, bank details, allocation of payments, and whether time is of the essence. If the settlement is conditional on cleared funds, that should be made explicit. The agreement should also state whether interest stops immediately, only after full payment, or continues after default.

Why Do Credit File And Confirmation Terms Matter?

If the debt has been reported to credit reference agencies, the parties should agree what update the creditor will make after settlement, such as marking the account as partially settled or satisfied where appropriate. A written completion confirmation or receipt is also useful evidence that the agreed settlement has been performed.

FAQs

You Might Also Be Interested In