United Kingdom Debt Settlement Agreement Clause Library

Clause Name | Purpose | Inclusion Frequency | Drafting Notes | Primary Party Affected |

|---|---|---|---|---|

Payment terms | ||||

Settlement Amount | States the sum accepted to settle the debt. | Usually included | Specify currency, exact amount, and whether inclusive of interest, costs, VAT, or fees. | Both parties |

Payment Date | Sets when the settlement sum must be paid. | Usually included | Use a clear calendar date and time zone state if time is of the essence. | Debtor |

Payment Method | Identifies how payment must be made. | Usually included | Include bank details, reference, permitted methods, and who pays transfer charges. | Debtor |

Cleared Funds Requirement | Makes settlement effective only once money is irrevocably received. | Often included | Define receipt as cleared funds in the creditor's nominated account. | Creditor |

Instalment Schedule | Sets staged payments towards the settlement sum. | Often included | List each instalment amount and due date link default consequences to missed instalments. | Debtor |

Early Payment | Allows payment before the agreed due date. | Optional | State whether early payment earns any discount or simply discharges the obligation sooner. | Debtor |

Application Of Payments | States how payments are allocated between principal, interest, costs, and fees. | Optional | Useful where several debts or invoices exist avoid uncertainty over which liability is reduced. | Both parties |

No Set-Off Or Deduction | Requires payment without withholding, set-off, counterclaim, or deduction. | Often included | Consider fairness for consumers and carve out deductions required by law. | Debtor |

Tax Gross-Up | Ensures the creditor receives the agreed net amount if withholding is required. | Situation-specific | Use mainly for business or cross-border debts obtain tax advice before including. | Debtor |

Bank Charges And Transfer Fees | Allocates responsibility for payment processing costs. | Optional | State whether the debtor must pay enough for the creditor to receive the full settlement sum. | Debtor |

Currency Of Payment | Specifies the currency in which the debt must be settled. | Often included | Use GBP unless another currency is intended address exchange rate risk if foreign currency applies. | Both parties |

Release and waiver | ||||

Full And Final Settlement | Confirms the settlement discharges the specified debt once conditions are met. | Usually included | Tie discharge to cleared funds and clearly define the released debt and parties. | Both parties |

Conditional Release | Delays release until the debtor fully performs the settlement obligations. | Usually included | Essential where creditor accepts less than the full debt or payment is by instalments. | Creditor |

Release By Creditor | Releases the debtor from further claims relating to the settled debt. | Usually included | Limit release to known debt unless wider settlement is intended. | Debtor |

Release By Debtor | Releases the creditor from debtor claims connected with the debt or dispute. | Often included | Useful if the debtor alleged overcharging, defective goods, or counterclaims. | Creditor |

Mutual Release | Provides reciprocal releases between creditor and debtor. | Often included | Ensure the scope matches the commercial deal and does not release unrelated liabilities accidentally. | Both parties |

Covenant Not To Sue | Prevents future proceedings over the settled debt. | Often included | Include exceptions for enforcement of the settlement agreement itself. | Both parties |

Waiver Of Interest | Waives contractual, statutory, or default interest as part of settlement. | Optional | State whether waiver applies only after timely settlement payment. | Creditor |

Waiver Of Costs | Waives legal or recovery costs related to the debt. | Optional | Identify whether pre-action, court, enforcement, and solicitor costs are included. | Creditor |

No Admission Of Liability | Confirms settlement is not an admission of liability or wrongdoing. | Often included | Useful where liability, quantum, or counterclaims are disputed. | Both parties |

Reservation Of Rights | Preserves rights not expressly released by the settlement. | Often included | List excluded claims, third-party rights, security, guarantees, and enforcement rights if retained. | Creditor |

Preservation Of Guarantees | Confirms settlement does not release guarantors unless expressly stated. | Situation-specific | Obtain guarantor consent if variation may prejudice guarantee enforcement. | Third party |

Preservation Of Security | Keeps any charge, lien, or security in place until settlement is completed. | Situation-specific | Identify registered security and specify release mechanics after cleared funds. | Creditor |

Credit File Reporting | Records how settlement may be reported to credit reference agencies. | Situation-specific | Do not promise removal of accurate data ensure processing is accurate and lawful. | Debtor |

Acknowledgement Of Satisfaction | Confirms the creditor will acknowledge the debt as satisfied after performance. | Optional | Useful for court records, ledgers, credit control files, and customer accounts. | Debtor |

Confidentiality | ||||

Confidentiality | Restricts disclosure of the agreement and settlement terms. | Often included | Include permitted disclosures to advisers, insurers, auditors, tax authorities, courts, and regulators. | Both parties |

Permitted Disclosures | Lists circumstances where disclosure is allowed. | Often included | Carve out legal duties, professional advisers, finance providers, group companies, and enforcement needs. | Both parties |

Non-Disparagement | Prevents damaging public statements about the other party or dispute. | Optional | Keep wording proportionate and preserve truthful statements required by law. | Both parties |

Data Protection | Addresses handling of personal data connected with the debt and settlement. | Situation-specific | Check UK GDPR, Data Protection Act 2018, lawful basis, retention, and credit reporting accuracy. | Both parties |

Default and enforcement | ||||

Events Of Default | Defines what counts as breach of the settlement agreement. | Usually included | Cover missed payment, insolvency, false statements, breach of confidentiality, and failed direct debit. | Debtor |

Grace Period | Allows a short cure period before default consequences apply. | Often included | State length, notice requirements, and whether it applies to every missed payment or only once. | Debtor |

Acceleration On Default | Makes the remaining balance immediately due after default. | Often included | Clarify whether the accelerated amount is the settlement balance or original debt balance. | Debtor |

Reinstatement Of Original Debt | Revives the original debt if the debtor defaults on a discounted settlement. | Often included | Credit payments already made and ensure the remedy is not an unenforceable penalty. | Debtor |

Default Interest | Applies interest to overdue settlement payments. | Often included | For business debts, consider the Late Payment of Commercial Debts (Interest) Act 1998 keep rates proportionate. | Debtor |

Recovery Of Enforcement Costs | Requires the defaulting debtor to pay reasonable enforcement costs. | Often included | Limit to reasonable, properly incurred costs align with any court cost rules. | Debtor |

Existing Judgment Enforcement | Preserves or suspends enforcement of an existing court judgment. | Situation-specific | State whether enforcement is stayed, paused, or resumed on default. | Creditor |

Consent Order Or Tomlin Order | Records settlement of ongoing court proceedings in an enforceable court order. | Situation-specific | Use where proceedings exist ensure schedule terms match the settlement agreement. | Both parties |

Statutory Demand Rights | Preserves creditor rights to use insolvency processes after default. | Situation-specific | Use only for undisputed debts consider Insolvency Act 1986 thresholds and insolvency rules. | Creditor |

Insolvency Event | Treats insolvency steps as default or a trigger for immediate payment. | Often included | Define events separately for individuals and companies consider bankruptcy, liquidation, administration, and IVA/CVA. | Debtor |

No Waiver Of Default | Prevents delay or leniency from waiving enforcement rights. | Often included | State waiver must be written and limited to the specific breach waived. | Creditor |

Default Notice | Requires notice before enforcement or acceleration begins. | Optional | For regulated consumer credit, check statutory default notice requirements. | Debtor |

General legal provisions | ||||

Consideration | Records the value exchanged to make the settlement binding. | Often included | Important where a lesser sum settles a larger debt consider using a deed if consideration is doubtful. | Both parties |

Execution and signing | ||||

Execution As A Deed | Allows the settlement to bind parties without ordinary contractual consideration. | Situation-specific | Use deed formalities under the Law of Property (Miscellaneous Provisions) Act 1989 and Companies Act 2006 if relevant. | Both parties |

General legal provisions | ||||

Identification Of Parties | Identifies the debtor, creditor, and any relevant connected parties. | Usually included | Use full legal names, company numbers, registered offices, and trading names where applicable. | Both parties |

Background And Recitals | Summarises the debt, dispute, and reason for settlement. | Often included | Keep factual avoid admissions unless intended. | Both parties |

Description Of Debt | Defines the liability being settled. | Usually included | Refer to invoices, loan agreements, account numbers, judgment debts, or demand letters. | Both parties |

Acknowledgement Of Debt | Records that the debtor acknowledges the debt or settlement liability. | Often included | Written acknowledgement or part payment may affect limitation under section 29 Limitation Act 1980. | Debtor |

Disputed Debt Settlement | Confirms the settlement compromises a disputed liability. | Situation-specific | Combine with no admission wording and mutual release where liability is contested. | Both parties |

Limitation Position | Addresses whether the debt may be time-barred or limitation has been extended. | Situation-specific | Simple contract debt claims are commonly subject to six years in England and Wales check facts carefully. | Both parties |

Consumer Credit Compliance | Flags rules applying to regulated consumer credit debts. | Situation-specific | Check Consumer Credit Act 1974, FCA CONC, arrears notices, default notices, and forbearance duties. | Creditor |

Consumer Fairness | Helps ensure consumer terms are transparent and fair. | Situation-specific | Avoid unfair penalties, hidden charges, imbalance, or unclear release wording for consumers. | Debtor |

Tax Consequences | Allocates responsibility for tax arising from settlement or debt release. | Situation-specific | Debt releases can have tax effects include no tax advice wording and recommend accounting advice. | Both parties |

Payment terms | ||||

VAT Treatment | States whether VAT is included, excluded, or not applicable. | Situation-specific | Clarify VAT on supplies, costs, or compensation seek tax advice for commercial disputes. | Both parties |

General legal provisions | ||||

Authority To Enter Agreement | Confirms each signer has power to bind the relevant party. | Often included | Check board approval, delegated authority, partners, trustees, attorneys, and insolvency officeholders. | Both parties |

Representations And Warranties | Records key statements relied on when settling. | Optional | May cover authority, ownership of debt, no assignment, solvency, and accuracy of information. | Both parties |

Assignment Of Debt | Confirms whether the debt or settlement rights may be assigned. | Situation-specific | Check legal assignment requirements under section 136 Law of Property Act 1925 and notice to debtor. | Both parties |

Third Party Rights | Controls whether non-parties can enforce the agreement. | Often included | Exclude or expressly include rights under the Contracts (Rights of Third Parties) Act 1999. | Third party |

Entire Agreement | States that the written settlement is the complete agreement. | Often included | Preserve liability for fraud and avoid excluding mandatory consumer rights. | Both parties |

Variation | Requires changes to be agreed in writing. | Often included | State who must sign variations be careful with informal extensions or payment changes. | Both parties |

Severance | Keeps the rest of the agreement effective if one term is invalid. | Often included | Useful where default interest, costs, or restrictions might be challenged. | Both parties |

Notices | Sets how formal notices must be served. | Often included | Include addresses, email use, deemed service timing, and service on companies. | Both parties |

Governing Law | Chooses the law governing the settlement agreement. | Usually included | Specify England and Wales, Scotland, or Northern Ireland as appropriate. | Both parties |

Jurisdiction | Identifies which courts may hear disputes about the agreement. | Usually included | Align with governing law and the parties' locations consider exclusive or non-exclusive wording. | Both parties |

Dispute Resolution | Sets a process for resolving settlement disputes before court action. | Optional | May include escalation, mediation, or negotiation do not obstruct urgent enforcement rights. | Both parties |

Execution and signing | ||||

Counterparts | Allows each party to sign separate copies of the agreement. | Often included | Useful for remote signing state all counterparts form one agreement. | Both parties |

Electronic Signatures | Permits signing by electronic signature where legally valid. | Often included | Check deed witnessing and identity evidence Law Commission confirms electronic signatures can be valid in English law. | Both parties |

Company Execution | Sets how a company signs the settlement validly. | Situation-specific | Companies may execute under section 44 Companies Act 2006 by authorised signatories or director plus witness. | Both parties |

Witnessing Formalities | Provides for witness signatures where the agreement is a deed or requires witnessing. | Situation-specific | For individuals executing deeds, signature must be witnessed record witness name, address, and occupation. | Both parties |

Effective Date | States when the agreement begins to operate. | Usually included | Distinguish signing date from settlement completion date and release date. | Both parties |

Settlement Completion Confirmation | Requires written confirmation once settlement obligations are fulfilled. | Optional | Useful where debtor needs proof for accounts, credit control, or enforcement records. | Debtor |

What Clauses Matter Most In A UK Debt Settlement Agreement?

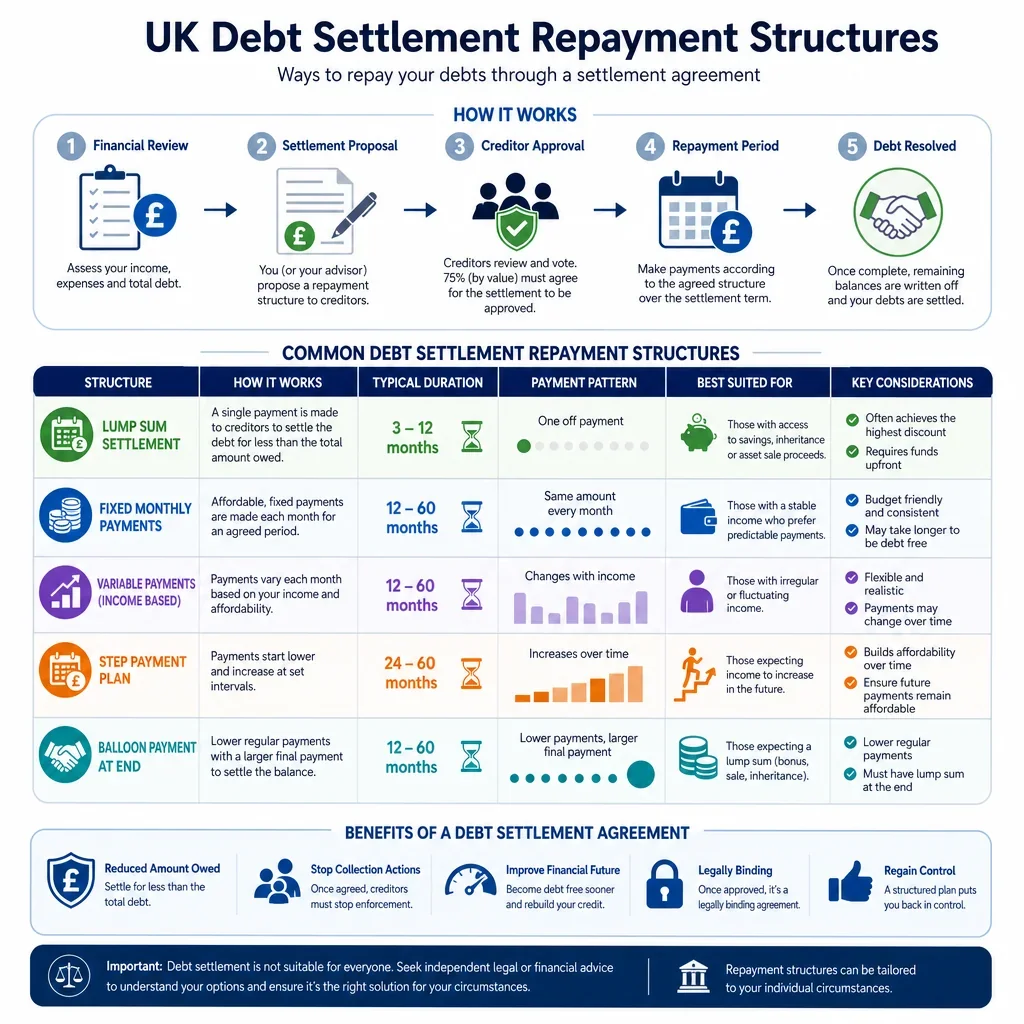

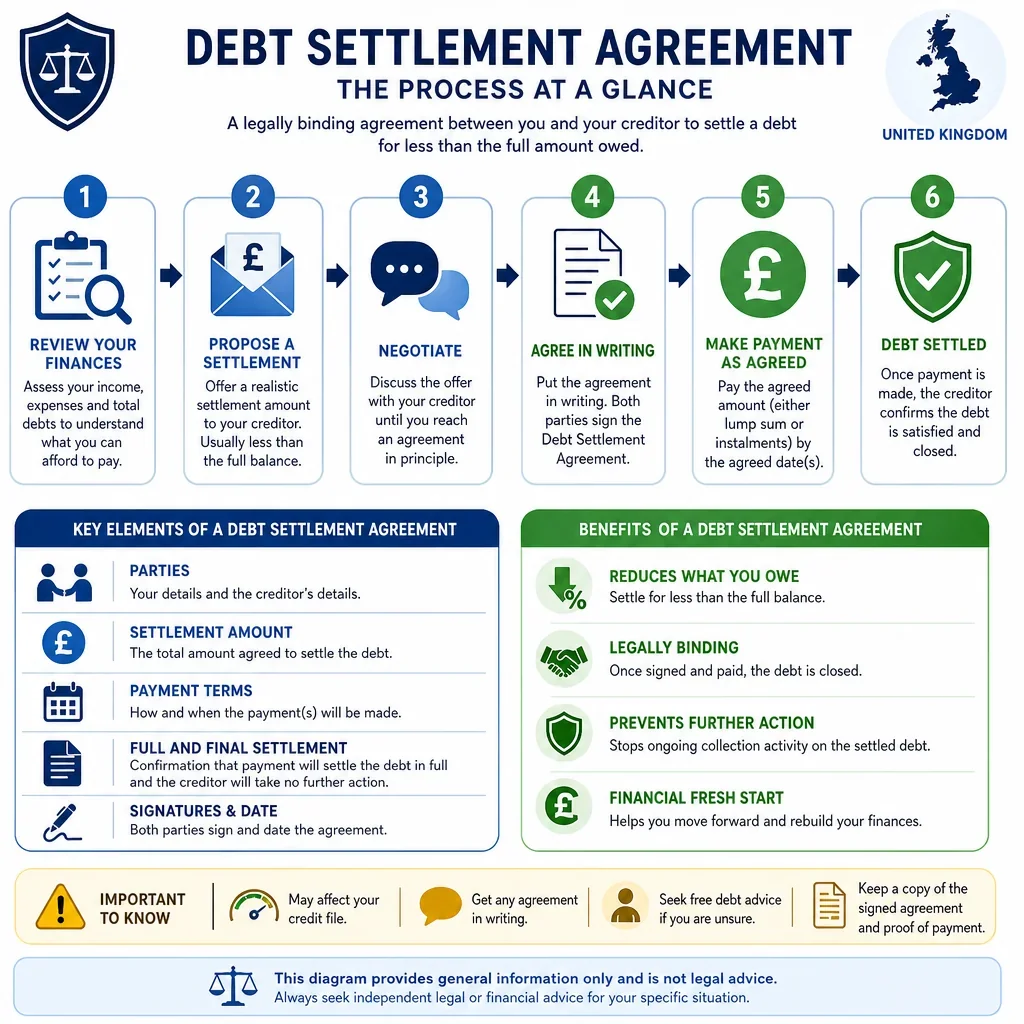

A UK debt settlement agreement should usually state the settlement amount, payment deadline, method of payment, and whether payment is in full and final settlement. Without clear payment and release wording, the creditor may retain scope to argue that only part of the debt was compromised.

When Should A Creditor Release The Debtor?

The safest approach for a creditor is to make any release conditional on cleared funds. Clauses such as conditional release, reservation of rights, and automatic reinstatement on default help avoid accidentally discharging the original debt before the settlement sum is actually received.

Why Are Default Clauses Important In Debt Settlement Agreements?

Where payment is made by instalments, the agreement should specify any grace period, default interest, acceleration of the balance, recovery of enforcement costs, and whether the creditor may enforce an existing judgment or guarantee. These clauses are especially important where the creditor is accepting less than the full amount owed.

What UK Legal Issues Should Be Checked Before Signing?

- Consideration: if a creditor accepts a lesser sum, the agreement should be drafted as a binding compromise, ideally with clear mutual obligations or execution as a deed where appropriate.

- Limitation: acknowledgement or part payment can affect limitation periods for simple contract debts under the Limitation Act 1980.

- Consumer credit: regulated debts may require extra care under the Consumer Credit Act 1974 and FCA rules.

- Tax and VAT: compromises, write-offs, interest and VAT treatment may need accounting advice, particularly for business debts.

FAQs

You Might Also Be Interested In