AI Generated American Promissory Note

PDF & Word - 2026 Updated

Docaro Pricing

When Do You Need a Promissory Note in the United States?

American Legal Rules for a Promissory Note

Using the wrong structure for a promissory note can invalidate enforceability or lead to unintended liability.

What a Proper Promissory Note Should Include

- Parties InvolvedClearly identify the borrower and lender by their full names and addresses.

- Loan AmountState the exact amount of money being borrowed.

- Interest RateSpecify the interest rate, if any, and how it is calculated.

- Repayment TermsOutline the schedule and method for repaying the loan, including due dates.

- Collateral (if applicable)Describe any assets pledged as security for the loan.

- Default ConsequencesExplain what happens if payments are missed, such as late fees or legal action.

- SignaturesInclude spaces for the borrower and lender to sign and date the note.

Generate Your Document in 4 Easy Steps

Why Use Docaro?

United States

United StatesFree Example Promissory Note Template

Below is a free template example of a Promissory Note for use in the United States generated by our AI model.

The clauses in your actual Promissory Note will vary from this example as they will be entirely bespoke to your requirements as set out in the questionnaire you complete.

Promissory Note

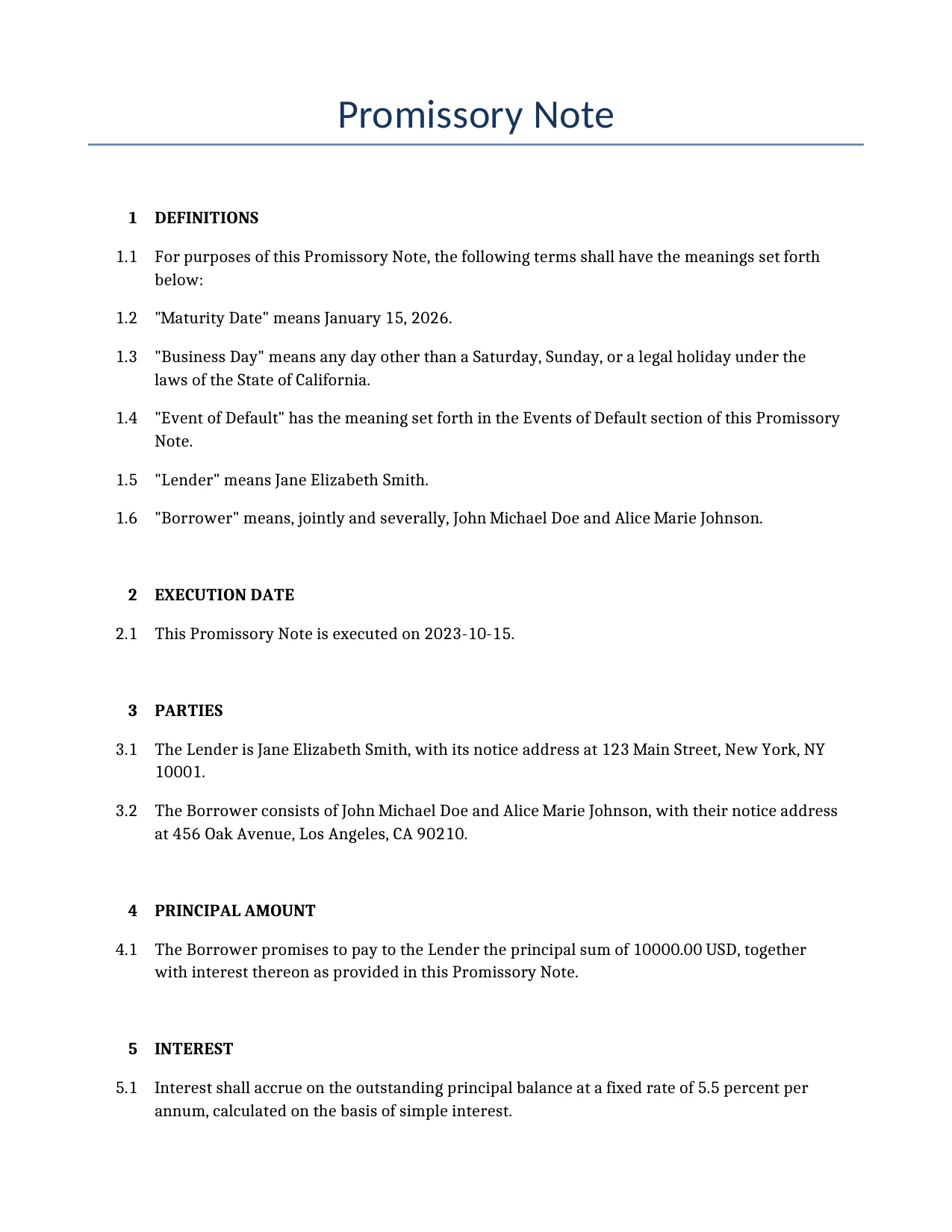

1DEFINITIONS

For purposes of this Promissory Note, the following terms shall have the meanings set forth below:

"Maturity Date" means January 15, 2026.

"Business Day" means any day other than a Saturday, Sunday, or a legal holiday under the laws of the State of California.

"Event of Default" has the meaning set forth in the Events of Default section of this Promissory Note.

"Lender" means Jane Elizabeth Smith.

"Borrower" means, jointly and severally, John Michael Doe and Alice Marie Johnson.

2EXECUTION DATE

This Promissory Note is executed on 2023-10-15.

3PARTIES

The Lender is Jane Elizabeth Smith, with its notice address at 123 Main Street, New York, NY 10001.

The Borrower consists of John Michael Doe and Alice Marie Johnson, with their notice address at 456 Oak Avenue, Los Angeles, CA 90210.

4PRINCIPAL AMOUNT

The Borrower promises to pay to the Lender the principal sum of 10000.00 USD, together with interest thereon as provided in this Promissory Note.

5INTEREST

Interest shall accrue on the outstanding principal balance at a fixed rate of 5.5 percent per annum, calculated on the basis of simple interest.

Interest shall begin to accrue on the principal amount on 2024-01-01.

The interest rate specified in this Promissory Note is intended to comply with all applicable usury laws including those of the State of California and in no event shall the interest rate exceed the maximum rate permitted by law.

6PAYMENTS

The Borrower shall make monthly payments of $302.07, of which the allocation between principal and interest will vary with each payment based on standard amortization (approximately $45.83 allocated to interest for the first payment, with the remainder to principal).

The first payment shall be due on 2024-01-15.

All payments shall be made by ACH Transfer.

The Borrower shall fully repay the principal and any remaining interest to the Lender by the Maturity Date of January 15, 2026. There is no balloon payment as the loan amortizes fully over the term.

7PREPAYMENT

The Borrower may prepay the loan in whole or in part before the maturity date.

The Borrower shall provide 10 Business Days Notice to the Lender prior to making any prepayment.

No prepayment penalty shall be imposed on the Borrower for early repayment of the loan.

8LATE PAYMENTS

A grace period of 10 days shall apply before late payment consequences take effect.

A late fee of 5 percent of the overdue payment amount shall be charged for any payment made after the grace period.

Interest shall accrue on any overdue amounts after the grace period at a default rate of 10 percent per annum.

9EVENTS OF DEFAULT

An Event of Default shall occur if the Borrower fails to make any payment when due under this Promissory Note.

An Event of Default shall occur upon breach of any covenant or agreement contained in this Promissory Note.

An Event of Default shall occur upon the insolvency, bankruptcy, or assignment for the benefit of creditors of any Borrower.

An Event of Default shall occur in the event of a cross-default, meaning the Borrower defaults under any other obligation or loan with the Lender or any third party in excess of $1,000.

An Event of Default shall occur upon a material adverse change in the Borrower's financial condition that, in the Lender's reasonable judgment, impairs the ability to repay the loan.

An Event of Default shall occur if a judgment in excess of $5,000 is entered against any Borrower and remains unsatisfied for more than 30 days.

10DEFAULT AND ACCELERATION

The Lender shall provide notice to the Borrower before declaring an event of default. The Borrower shall have a cure period of 10 days after receiving such notice to remedy any default (except for payment defaults, which have a 10-day grace period as set forth above).

Upon the occurrence of an Event of Default, the Lender shall have the right to accelerate the full balance of the loan, making all principal, accrued interest, and other amounts immediately due and payable.

A higher default interest rate of 10 percent per annum shall apply if the Borrower fails to make payments when due.

11REMEDIES

Upon default the Borrower shall be responsible for the Lender's reasonable attorney fees incurred in enforcing this Promissory Note.

The Borrower hereby waives presentment, demand, protest, and notice of dishonor in connection with this Promissory Note.

12REPRESENTATIONS AND WARRANTIES

Each Borrower represents and warrants that it has full authority and legal capacity to enter into this Promissory Note.

Each Borrower represents and warrants that this Promissory Note is a valid and binding obligation, enforceable in accordance with its terms.

Each Borrower represents and warrants that the execution and performance of this Promissory Note will not conflict with or violate any other agreement or law applicable to the Borrower.

Each Borrower represents and warrants that it is financially solvent and that there has been no material adverse change in its financial condition since the date of application for this loan.

13COVENANTS

Affirmative Covenants: The Borrower shall maintain adequate insurance on any collateral (if applicable), pay all taxes when due, and provide annual financial statements to the Lender upon request.

Negative Covenants: The Borrower shall not incur additional debt exceeding $5,000 without the Lender's prior written consent, nor sell or transfer material assets outside the ordinary course of business without such consent.

14JOINT AND SEVERAL LIABILITY

The obligations of the two Borrowers under this Promissory Note shall be joint and several.

15GOVERNING LAW

This Promissory Note shall be governed by and construed in accordance with the laws of the State of California.

16JURISDICTION AND VENUE

The parties consent to the exclusive jurisdiction of the courts of the State of California, located in Los Angeles County, for any action or proceeding arising out of or relating to this Promissory Note.

17WAIVER OF JURY TRIAL

The parties hereby waive any right to a jury trial in any action or proceeding arising out of or relating to this Promissory Note.

This example shows approximately 70% of a typical document and is provided for illustrative purposes only. The remaining content has been omitted.

Every document generated by Docaro is tailored to your specific circumstances, jurisdiction and the information you provide. The completed document includes all applicable clauses and provisions required for your situation.

To generate the full, personalised document, answer a short series of questions and your document will be created instantly.