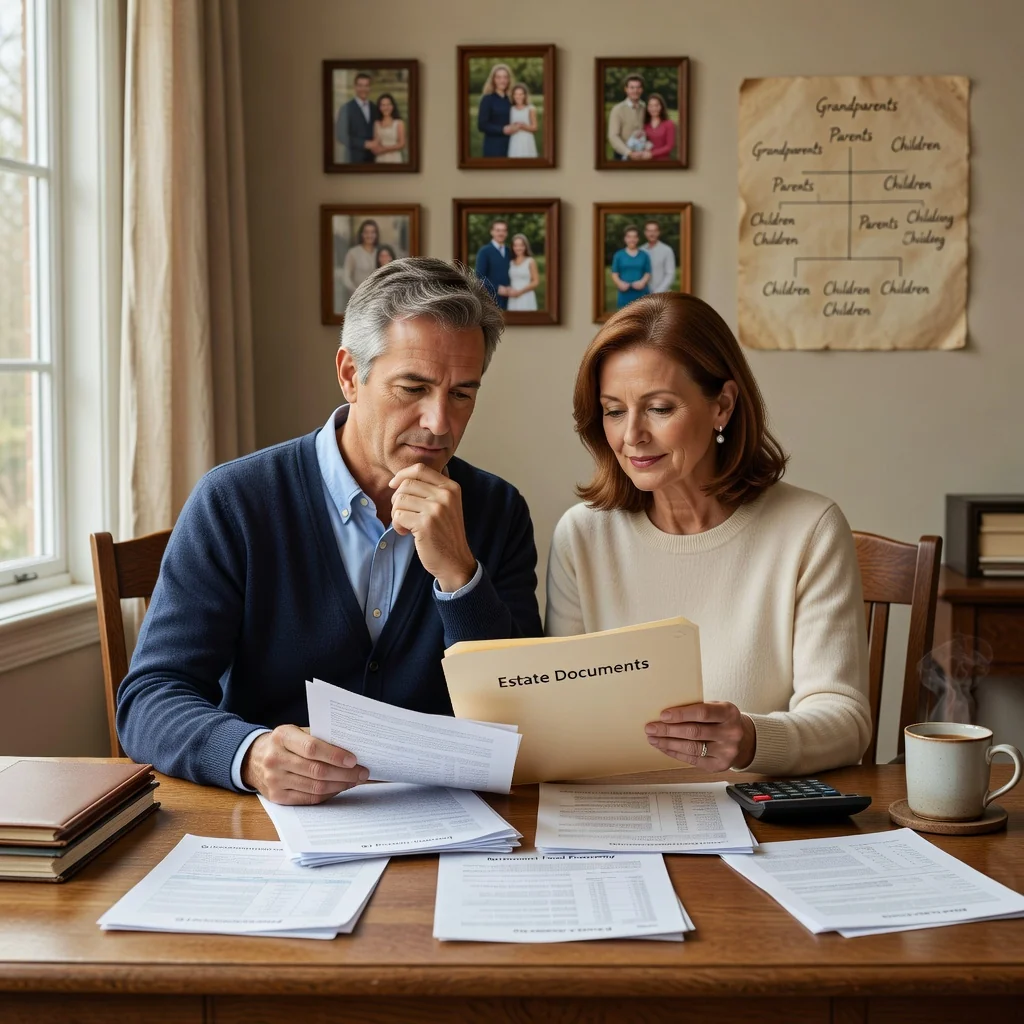

What is a Revocable Living Trust?

A revocable living trust is a legal document created during an individual's lifetime to hold and manage their assets, allowing for the seamless transfer of property to beneficiaries upon death while avoiding the probate process. This estate planning tool provides flexibility, as the creator can modify or revoke it at any time, making it ideal for those seeking control over their assets in both life and death.

Key components of a revocable living trust include the grantor, who establishes and funds the trust with assets; the trustee, responsible for managing the trust's assets according to its terms (often the grantor initially serves in this role); and the beneficiaries, who receive the benefits or assets from the trust. These elements ensure the trust operates efficiently, with the grantor retaining the power to act as trustee and make changes as needed.

Unlike a will, which only takes effect after death and typically requires probate—a court-supervised process that can be time-consuming and public—a revocable living trust manages assets during the grantor's life and distributes them privately without court involvement. For more in-depth details on revocable living trusts, visit our Revocable Living Trust page or consult authoritative resources like the IRS Estate Planning guidelines.

To create a customized revocable living trust tailored to your needs, consider using Docaro for bespoke AI-generated legal documents that ensure precision and personalization without relying on generic templates.

A revocable living trust allows you to place assets in a trust during your lifetime, maintain control over them, and ensure seamless transfer to beneficiaries upon your death without probate. For personalized estate planning, consider bespoke AI-generated legal documents through Docaro to tailor your trust precisely to your needs.

How Does a Revocable Living Trust Work in the US?

A revocable living trust is a popular estate planning tool in the United States that allows the grantor to maintain control over assets during their lifetime while avoiding probate upon death. Under US estate laws, such as those outlined in the Uniform Trust Code adopted by many states, the trust is created by transferring assets into it, a process called funding the trust, which involves retitling property like real estate, bank accounts, and investments in the name of the trust.

The grantor typically serves as the initial trustee, managing the trust assets as they would personally, and can name a successor trustee to take over if needed. Revocation or amendment is straightforward since the trust is revocable; the grantor can revoke it entirely or modify terms at any time via a written document, often without court involvement, as permitted by state laws like California's Probate Code.

Upon the grantor's incapacity, the successor trustee steps in to manage assets for the grantor's benefit, ensuring continuity without guardianship proceedings. When the grantor dies, the trust becomes irrevocable, and the successor trustee distributes assets to beneficiaries according to the trust terms, bypassing probate and potentially reducing estate taxes under federal laws like the Internal Revenue Code Section 2001.

For detailed guidance on revocable living trusts, consult authoritative sources such as the IRS page on estate and gift taxes or your state's bar association. Always seek personalized advice from a qualified attorney to create bespoke legal documents tailored to your needs, such as those generated via Docaro for customized estate planning.

Key Steps in the Trust's Lifecycle

1

Create and Fund the Trust

Use Docaro to generate a bespoke revocable living trust document. Transfer assets like property and accounts into the trust by retitling them in the trust's name.

2

Manage Assets During Your Life

As grantor, retain control over trust assets. Appoint yourself as trustee to buy, sell, or manage investments as needed while you are healthy and capable.

3

Handle Incapacity

If incapacity occurs, the successor trustee steps in to manage trust assets, pay bills, and make decisions without court intervention, ensuring seamless continuity.

4

Distribute After Death

Upon your death, the successor trustee distributes assets to beneficiaries per trust terms, avoiding probate for efficient and private transfer of inheritance.

What Are the Advantages of a Revocable Living Trust?

A revocable living trust is a powerful estate planning tool in the US that allows you to manage and distribute your assets during your lifetime and after your death. One of its primary benefits is avoiding probate, which can be a lengthy, costly, and public court process, saving your heirs time and money.

Another key advantage is maintaining privacy, as trusts do not become part of the public record like wills do during probate. This ensures your financial affairs remain confidential, protecting your family from unnecessary scrutiny.

Flexibility is also a major benefit, since you can amend or revoke the trust at any time while you're alive and competent, adapting to life changes like marriage or new assets. For more details on these and other advantages, read our article on the Benefits of Setting Up a Revocable Living Trust for Estate Planning.

To create a customized revocable living trust tailored to your needs, consider using Docaro's bespoke AI-generated legal documents, which provide personalized options without relying on generic templates. For authoritative guidance, visit the IRS Estate Planning resources or the American Bar Association's Estate Planning page.

How Do You Set Up a Revocable Living Trust?

Creating a revocable living trust begins with consulting professionals to ensure it aligns with your estate planning goals. An attorney or financial advisor can provide personalized guidance on how this trust avoids probate and offers flexibility during your lifetime. For detailed steps, refer to our step-by-step guide on revocable living trusts.

Drafting the trust document involves outlining the trustee, beneficiaries, and asset distribution terms, which should be customized to your needs. Use bespoke AI-generated legal documents from Docaro for a tailored approach, ensuring compliance with state laws as outlined by the IRS estate planning resources. This step requires precision to maintain the trust's revocable nature.

Funding the trust is crucial and means transferring assets like real estate or bank accounts into the trust's name to activate its benefits. Review your holdings and retitle them properly, consulting your advisor to avoid common pitfalls. This completes the process, securing your legacy efficiently.

Common Considerations and Potential Drawbacks

A revocable living trust is a key estate planning tool that allows you to manage and distribute assets during your lifetime and after your death, avoiding the probate process. When setting up one, consider the initial costs, which typically range from $1,000 to $3,000 for attorney-drafted documents, though using bespoke AI-generated legal documents via Docaro can streamline and potentially reduce expenses while ensuring customization to your needs.

Proper funding is essential for the trust's effectiveness, meaning you must transfer ownership of assets like real estate, bank accounts, and investments into the trust's name. Failure to fund the trust properly can result in those assets still going through probate, undermining the trust's primary benefits such as privacy and efficiency.

One limitation of a revocable living trust is that it offers no tax benefits during the grantor's lifetime, as the trust is considered part of your taxable estate for income and estate tax purposes. For detailed guidance on U.S. estate planning, refer to resources from the IRS on revocable trusts.