UK Revocable Trust And Declaration Of Trust Concept Glossary

Concept | Plain English meaning | Use in document | Practical importance | Common caution |

|---|---|---|---|---|

Trust structure | ||||

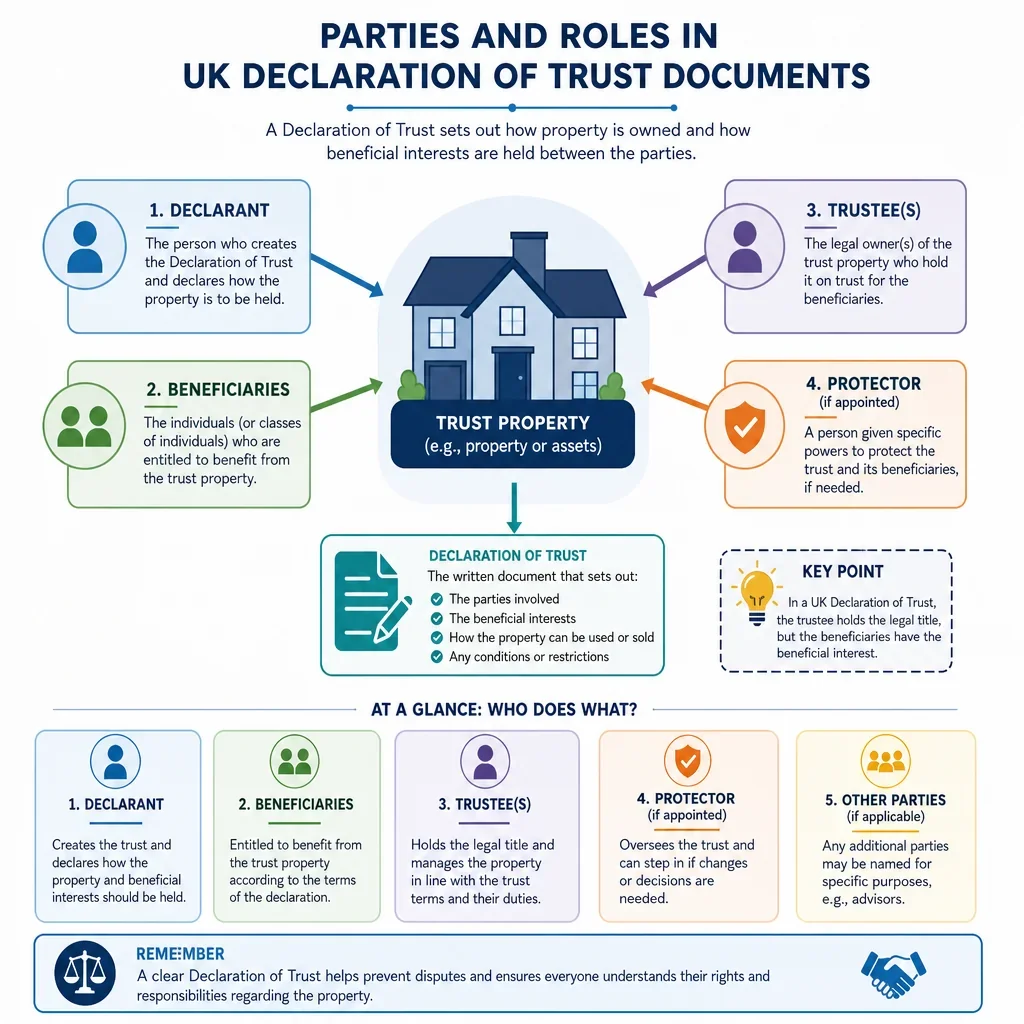

Declaration of Trust | A document stating who really owns property or assets and in what shares. | Usually the main deed setting out the trust property, parties, shares, powers, and revocation terms. | High | It must match the real intention and not conflict with title, mortgage, or tax position. |

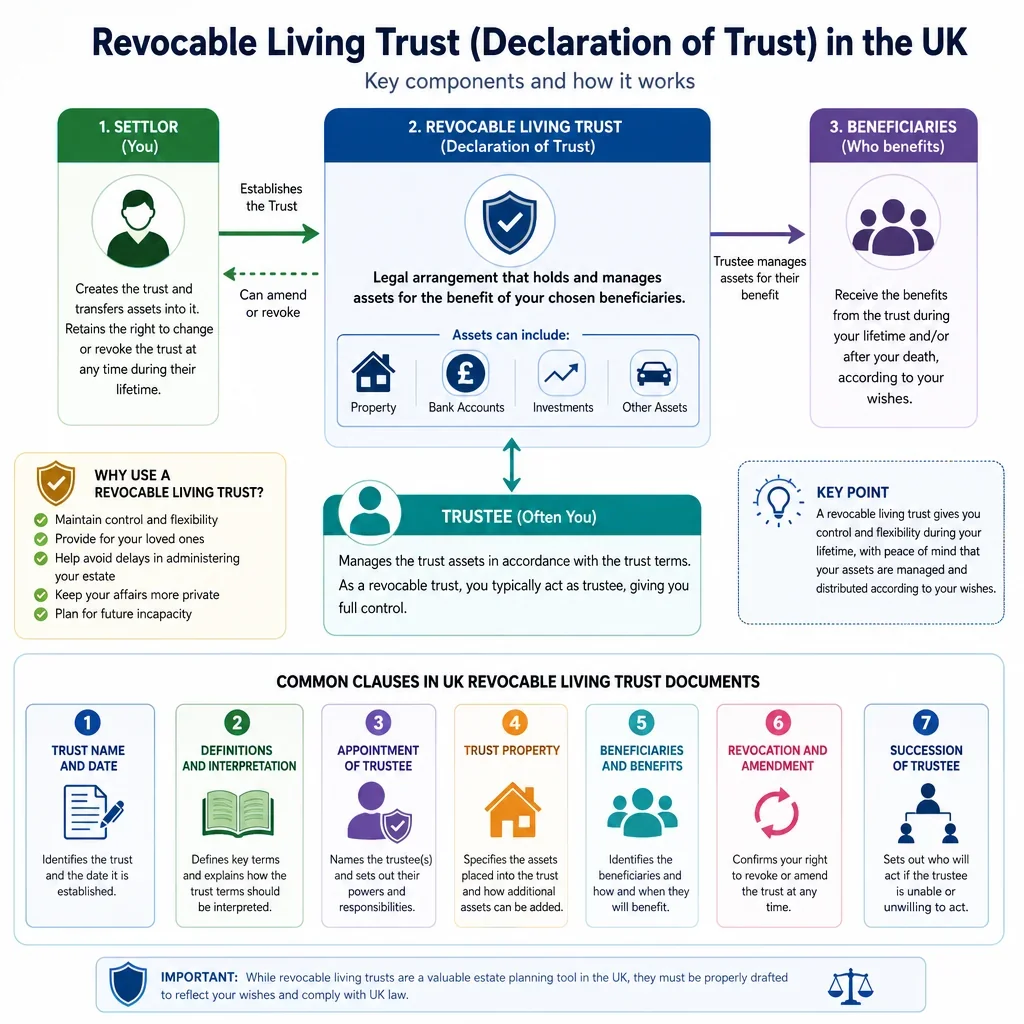

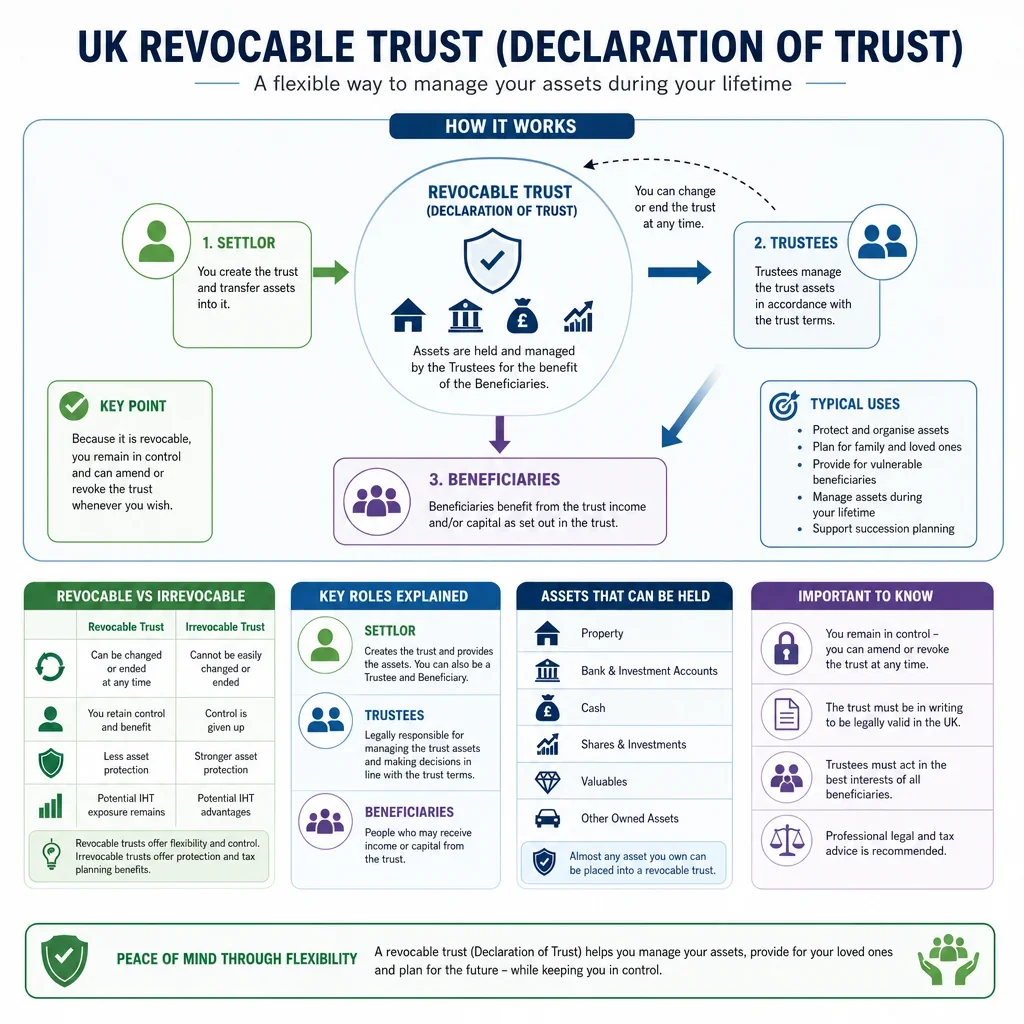

Revocable Living Trust | A lifetime trust that the person creating it can amend or cancel. | Appears in wording allowing the settlor to revoke, amend, or retake the trust property. | High | The phrase is more common in US usage UK tax and succession effects may differ. |

Party role | ||||

Settlor | The person who creates the trust or puts assets into it. | Named as the person declaring or transferring assets into the trust. | High | If the settlor keeps benefits or powers, tax consequences can change. |

Trustee | The person or people legally responsible for holding and managing trust property. | Identified as holding legal title and exercising trust powers and duties. | High | Trustees owe duties and should not treat trust assets as their own. |

Beneficiary | A person entitled to benefit from the trust property or income. | Listed with their entitlement, percentage share, or conditions for receiving benefits. | High | Unclear beneficiary wording can make the trust uncertain or hard to administer. |

Property ownership | ||||

Legal Ownership | The name or names legally registered or recognised as owning the asset. | Used to distinguish registered title holders from people entitled to the value. | High | Legal ownership may not show the true beneficial shares. |

Beneficial Ownership | The right to the economic value, income, or sale proceeds of an asset. | States who owns the underlying benefit and in what proportions. | High | Changing beneficial ownership may have tax, mortgage, and family law consequences. |

Equitable Interest | Another term for a person’s beneficial interest in property. | Used to describe a beneficiary’s entitlement behind the legal title. | Medium | It should not be confused with being named on the Land Registry title. |

Trust structure | ||||

Trust Property | The asset held under the trust, such as land, money, shares, or personal property. | Described in the recitals or schedule with enough detail to identify it. | High | Vague descriptions may make it unclear what the trust covers. |

Express Trust | A trust deliberately created by words, usually in a document. | A Declaration of Trust normally creates or records an express trust. | High | Express trusts may trigger HMRC Trust Registration Service obligations. |

Bare Trust | A trust where the beneficiary has an immediate and fixed right to the asset. | May be used where one person holds title for another absolutely. | Medium | The beneficiary can usually demand transfer if adult and absolutely entitled. |

Fixed Trust | A trust where each beneficiary’s share is set in advance. | Appears as stated percentages or fractions for each beneficiary. | High | Percentages should total 100 percent and match contributions if intended. |

Discretionary Trust | A trust where trustees choose how and when beneficiaries benefit. | Appears as trustee powers to distribute income or capital among a class. | Medium | Discretionary trusts have different tax treatment and need careful drafting. |

Property ownership | ||||

Joint Tenants | Co-owners who own the whole property together, with survivorship on death. | May be referenced when explaining existing ownership before declaring shares. | High | A joint tenant cannot leave their share by will while joint tenancy continues. |

Tenants In Common | Co-owners who each own a distinct share of the property. | Commonly paired with a Declaration of Trust setting out unequal or equal shares. | High | Shares should be recorded clearly and protected by the correct Land Registry restriction. |

Severance Of Joint Tenancy | The process of changing joint tenants into tenants in common. | May be referenced where fixed shares are declared for formerly joint owners. | High | A declaration alone may not update the Land Registry restriction without separate steps. |

Registration or evidence | ||||

Form A Restriction | A Land Registry entry showing the property is held on a trust of land. | May be mentioned as protection for tenants in common or beneficial shares. | High | It does not record the actual percentages the declaration must do that. |

Land Registry Title | The official register showing legal ownership and key restrictions for registered land. | The title number and property address are often included to identify land. | High | Use the exact title number and check registered owners before signing. |

Title Number | The unique Land Registry reference for a registered property. | Included in the property description to avoid doubt over the asset. | Medium | Do not rely only on a postal address where land boundaries or titles differ. |

Party role | ||||

Registered Proprietor | The person named at HM Land Registry as the legal owner of registered land. | Used to identify who currently holds legal title to the property. | High | A beneficiary may not be a registered proprietor. |

Tax or administration | ||||

Mortgage Lender Consent | Permission from a lender before changing ownership rights affecting mortgaged property. | May appear as a condition or acknowledgement where property is mortgaged. | High | Trust arrangements can breach mortgage terms if lender consent is required. |

Document clause | ||||

Trust Deed | A formal written document setting out the trust terms. | The declaration itself may be executed as a deed to create reliable evidence. | High | Deeds have signing and witnessing rules that must be followed. |

Execution As A Deed | Formal signing method required for many important legal documents. | Appears in signing blocks with witness details and deed wording. | High | Incorrect witnessing or missing deed wording can undermine the document. |

Party role | ||||

Witness | An independent person who observes a signature and confirms it. | Included beside signatures with name, address, occupation, and signature. | High | A beneficiary or close party should generally not witness if independence is needed. |

Trust structure | ||||

Certainty Of Intention | Clear wording showing the creator meant to create a trust. | Appears through words such as "declares that the trustees hold on trust". | High | Casual promises or wishes may not create a valid trust. |

Certainty Of Subject Matter | The trust assets and shares must be clearly identifiable. | Reflected in precise property descriptions and exact percentage shares. | High | Unclear assets or uncertain proportions can cause disputes or invalidity. |

Certainty Of Objects | The beneficiaries must be clearly named or identifiable. | Reflected in full names, addresses, classes, or definitions of beneficiaries. | High | Ambiguous beneficiary descriptions can make the trust hard to enforce. |

Document clause | ||||

Revocation Clause | A clause saying how the trust can be cancelled. | States who may revoke, the required notice, and what happens to assets. | High | Without clear revocation wording, the trust may not be easily reversible. |

Amendment Clause | A clause explaining how the trust terms can be changed. | Sets out required consent, form of amendment, and any limits on changes. | High | Changes affecting land, tax, or beneficiaries should be documented formally. |

Trustee Powers | The authority trustees have to manage, invest, sell, or distribute trust assets. | Listed as powers to deal with property, money, insurance, income, and expenses. | High | Powers must be exercised for proper trust purposes and within fiduciary duties. |

Tax or administration | ||||

Trustee Duties | Legal responsibilities trustees must follow when managing trust assets. | Often reflected in management, investment, accounting, and conflict clauses. | High | Trustees can be personally liable for breach of duty. |

Statutory Duty Of Care | A legal duty for trustees to use reasonable care and skill in specified functions. | May be incorporated, modified, or acknowledged in trustee duty clauses. | Medium | Professional trustees may be held to a higher standard. |

Trust structure | ||||

Trust Of Land | A trust where the trust property includes land. | Used for homes, buy-to-let property, or land held for beneficiaries. | High | Land trusts interact with Land Registry rules, co-ownership, and lender requirements. |

Trusts Of Land And Appointment Of Trustees Act 1996 | The main Act governing many trusts of land in England and Wales. | May be referenced in clauses about trustee powers, sale, occupation, and land management. | High | Scottish and Northern Irish property rules differ. |

Tax or administration | ||||

Trustee Act 2000 | An Act setting rules on trustee powers, investment, delegation, and duty of care. | May be incorporated or varied by trustee power and investment clauses. | Medium | Some statutory powers can be expanded or restricted by the trust instrument. |

Property ownership | ||||

Law Of Property Act 1925 | A key property law statute affecting land ownership and trusts in England and Wales. | Relevant to co-ownership, legal estates, and trust interests in land. | Medium | It is technical and should not be cited without understanding the specific section. |

Document clause | ||||

Declaration Of Beneficial Shares | A clause stating each person’s percentage or fraction of the beneficial interest. | Often states shares such as 50:50, 70:30, or another fixed split. | High | Shares should reflect the agreed deal, not just mortgage payments or informal assumptions. |

Property ownership | ||||

Unequal Beneficial Shares | Ownership of the benefit is split in different proportions between people. | Used where contributions or intentions are not equal. | High | Record exact percentages and consider how future payments affect the split. |

Document clause | ||||

Floating Share Formula | A formula that changes shares based on future contributions or events. | Used to calculate beneficial shares when contributions may change over time. | Medium | Complex formulas can cause disputes unless contribution evidence is kept. |

Registration or evidence | ||||

Financial Contributions | Money paid toward purchase price, deposit, mortgage, improvements, or costs. | May be recited to explain why beneficial shares are equal or unequal. | Medium | Keep proof of payments if shares depend on contributions. |

Document clause | ||||

Occupation Rights | Rights for a beneficiary to live in or use trust land. | May state who may occupy, on what terms, and who pays outgoings. | Medium | Occupation rights may conflict with sale plans, mortgage terms, or co-owner interests. |

Power Of Sale | Trustees’ authority to sell trust property. | Sets when trustees can sell and whether consent is needed. | High | Sale powers should not ignore beneficiary rights or agreed consent requirements. |

Property ownership | ||||

Proceeds Of Sale | Money left after selling an asset and paying sale costs and secured debts. | States how net sale proceeds are divided between beneficiaries. | High | Define whether mortgage debt, tax, and sale expenses are deducted first. |

Tax or administration | ||||

Income Entitlement | The right to receive income generated by trust property. | States who receives rent, dividends, interest, or other trust income. | Medium | Income allocation can affect income tax reporting. |

Property ownership | ||||

Capital Entitlement | The right to the asset value or sale proceeds, not just income. | Used to distinguish ownership of the asset from rights to income. | High | Do not assume income shares and capital shares are automatically the same. |

Document clause | ||||

Property Outgoings | Costs such as mortgage payments, insurance, repairs, service charges, and council tax. | Allocates who must pay ongoing costs for trust property. | Medium | Payment of costs does not always change beneficial shares unless the deed says so. |

Repair And Improvement Costs | Money spent maintaining or improving the trust property. | May state whether costs are shared equally, by shares, or reimbursed first. | Medium | Improvements and repairs may be treated differently for tax and sharing purposes. |

Indemnity Clause | A promise to reimburse someone for specified losses or liabilities. | Protects trustees or co-owners for costs incurred properly for the trust. | Medium | It should not excuse fraud, dishonesty, or deliberate breach of trust. |

Tax or administration | ||||

Trustee Liability | The risk that trustees may be personally responsible for trust breaches or debts. | Addressed through duty, indemnity, insurance, and limitation clauses. | High | Trustees should understand obligations before accepting appointment. |

Party role | ||||

Replacement Trustee | A new trustee appointed when another trustee retires, dies, or is removed. | Appears in appointment and succession clauses for trustee changes. | Medium | Trust property may need formal transfer to the new trustees. |

Tax or administration | ||||

Appointment Of Trustees | The process of adding or replacing trustees. | Sets who can appoint trustees and what formalities apply. | Medium | Appointments should be documented and reflected in asset records where needed. |

Retirement Of Trustee | The process for a trustee to step down. | May state how a trustee retires and who must consent. | Medium | There must usually be sufficient continuing trustees or replacement arrangements. |

Party role | ||||

Protector | A person given oversight or consent powers over trustee decisions. | May appear in clauses requiring consent for sale, amendment, or distributions. | Low | Protector powers should be clear to avoid blocking administration. |

Attorney Under Lasting Power Of Attorney | A person authorised to make decisions for someone under a registered LPA. | May be relevant if a party signs or acts through an attorney. | Medium | Attorney authority must cover the act and comply with the Mental Capacity Act framework. |

Tax or administration | ||||

Mental Capacity | The ability to understand and make the decision to create or change a trust. | Relevant to signing validity, attorney involvement, and later challenges. | High | A trust signed without capacity may be challenged. |

Undue Influence | Improper pressure causing someone to sign or agree against free choice. | Usually addressed by independent signing, explanation, and evidence of consent. | Medium | Transactions benefiting a dominant party are more vulnerable to challenge. |

Registration or evidence | ||||

Independent Legal Advice | Separate legal advice for a party before signing. | May be acknowledged where a party gives up rights or accepts risk. | Medium | Especially important where shares are unequal or one party is vulnerable. |

Document clause | ||||

Governing Law | The legal system used to interpret the trust. | States whether the trust is governed by England and Wales, Scotland, or Northern Ireland law. | High | UK property and trust rules differ by jurisdiction. |

Jurisdiction Clause | A clause saying which courts may deal with disputes. | Often paired with governing law wording. | Medium | It cannot always override mandatory property or consumer rules. |

Recitals | Introductory background statements explaining the facts and purpose. | Describe the property, contributions, parties, and intention behind the trust. | Medium | Recitals should be accurate because they may influence interpretation. |

Definitions Clause | A section defining key terms used in the document. | Defines terms such as trust property, beneficiaries, net proceeds, and trustees. | Medium | Defined terms must be used consistently throughout the deed. |

Schedule | An attachment listing detailed information separately from the main clauses. | May list property details, beneficiaries, assets, or contribution history. | Low | Schedules must be completed and referenced correctly before signing. |

Tax or administration | ||||

Trust Accounts | Records showing trust assets, income, expenses, and distributions. | May require trustees to keep records and provide information to beneficiaries. | Medium | Poor records make tax reporting and disputes harder. |

Trust Bank Account | A separate account used for trust money. | May be required for rent, sale proceeds, or trust income. | Medium | Mixing trust money with personal money creates accounting and liability risks. |

Registration or evidence | ||||

HMRC Trust Registration Service | HMRC’s online register for many UK and some non-UK trusts. | Not usually a clause, but trustees may need details from the deed to register. | High | Registration duties can apply even when the trust has no immediate tax to pay. |

Tax or administration | ||||

Trust Registration Deadline | The date by which trustees must register or update trust information with HMRC. | Usually handled administratively after signing, not within the trust deed. | High | Late or missed registration can expose trustees to HMRC penalties. |

Registration or evidence | ||||

Excluded Trust For TRS | A trust type that may not need registration unless it becomes taxable. | Relevant when trustees assess whether registration is required after signing. | Medium | Do not assume a co-ownership declaration is automatically excluded. |

Tax or administration | ||||

Income Tax On Trust Income | Tax on rent, interest, dividends, or other income arising from trust assets. | Relevant where the deed allocates income or rent to beneficiaries. | High | Tax treatment depends on trust type and beneficiary entitlement. |

Capital Gains Tax | Tax that may arise when trust property is sold or transferred at a gain. | Relevant to sale, transfer, revocation, and beneficiary entitlement clauses. | High | Changing beneficial ownership can be a disposal for CGT purposes. |

Inheritance Tax | Tax that may apply to transfers into, within, or out of certain trusts. | Relevant where assets are settled for others or retained for estate planning. | High | Revocable trusts and retained benefits may not remove assets from an estate. |

Stamp Duty Land Tax | Tax that may apply to land transactions in England and Northern Ireland. | Relevant if beneficial interests in land are transferred for consideration or debt assumption. | High | Mortgage debt or other consideration can trigger SDLT even without a cash payment. |

Land And Buildings Transaction Tax | The Scottish tax on land and property transactions. | Relevant if the trust involves Scottish land or transfers of Scottish property interests. | Medium | Scottish land tax rules differ from SDLT. |

Land Transaction Tax | The Welsh tax on land and property transactions. | Relevant if the trust involves Welsh land or property interest transfers. | Medium | Welsh land tax rules differ from SDLT. |

Reservation Of Benefit | A gift where the giver keeps using or benefiting from the asset. | Relevant where the settlor transfers property but continues to live in or enjoy it. | High | It may prevent the asset leaving the estate for inheritance tax. |

Pre-Owned Assets Tax | An income tax charge that can apply where someone benefits from assets they formerly owned. | Relevant to home or asset planning where the settlor keeps occupation or use. | Medium | Trusts used for home ownership planning can trigger complex anti-avoidance rules. |

Deprivation Of Assets | Giving away or restructuring assets to reduce care fee assessments. | Relevant where a trust is intended to move home value away from the settlor. | High | Local authorities may still treat deliberately transferred assets as owned. |

Bankruptcy And Creditor Risk | The risk that a person’s beneficial interest may be claimed by creditors. | May influence beneficiary rights, trustee powers, and asset protection expectations. | Medium | A trust is not automatically effective asset protection against existing creditors. |

Matrimonial Or Civil Partnership Claims | Possible claims over property when a marriage or civil partnership ends. | Relevant where beneficial ownership affects relationship property arrangements. | Medium | A trust deed may be considered by a family court but may not be decisive. |

Document clause | ||||

Cohabitation Agreement | A wider agreement between unmarried partners about finances and property. | May sit alongside a Declaration of Trust for property ownership shares. | Medium | A declaration of trust may not cover all relationship financial issues. |

Tax or administration | ||||

Interaction With A Will | How trust ownership affects what can pass under a person’s will. | Relevant where tenants in common can leave beneficial shares by will. | High | Joint tenancy survivorship may override will wishes unless severed. |

Property ownership | ||||

Right Of Survivorship | The rule that a deceased joint tenant’s interest passes to the surviving joint owner. | Relevant when deciding whether to hold as joint tenants or tenants in common. | High | It can defeat an intended gift of a property share in a will. |

Party role | ||||

Minor Beneficiary | A beneficiary who is under 18. | May require age conditions, trustee holding powers, or parental receipt wording. | Medium | Minors cannot usually give valid consent or receipt for capital themselves. |

Vulnerable Beneficiary | A beneficiary who may qualify for special trust tax treatment due to disability or age. | May require specific drafting if vulnerable person tax treatment is intended. | Medium | Special tax treatment has strict conditions and should not be assumed. |

Document clause | ||||

Trust Period | The time during which the trust operates. | States when the trust begins and when it ends or can be wound up. | Medium | Perpetuity and accumulation rules may matter for long-running trusts. |

Perpetuity Period | The maximum period before certain future trust interests must vest. | May be included in trusts with future or contingent beneficiaries. | Low | Less relevant for simple fixed co-ownership trusts, but important for complex trusts. |

Trust structure | ||||

Perpetuities And Accumulations Act 2009 | An Act modernising rules on long-running future interests and accumulations. | Relevant to long-term or complex trust duration clauses. | Low | Simple lifetime declarations may not need detailed perpetuity drafting. |

Tax or administration | ||||

Personal Data In Trust Documents | Names, addresses, dates of birth, and financial details included in the deed. | Used to identify parties, beneficiaries, witnesses, and assets. | Low | Store signed deeds securely because they contain sensitive personal and financial data. |

Registration or evidence | ||||

Evidence Of Intention | Documents or facts showing what the parties intended about ownership. | The deed is primary evidence of intended beneficial ownership. | High | Later informal statements may not override a properly executed declaration. |

Trust structure | ||||

Resulting Trust | A trust implied where contributions suggest ownership was not meant to follow legal title. | A clear declaration can reduce reliance on implied resulting trust arguments. | Medium | Implied trusts are fact-sensitive and often disputed. |

Constructive Trust | A trust recognised by a court because fairness and conduct require it. | A declaration can help avoid later arguments about informal promises and reliance. | Medium | Court outcomes depend heavily on evidence of agreement and conduct. |

Common Intention Constructive Trust | An implied property interest based on shared intention and reliance. | A written declaration records the parties’ intention and reduces uncertainty. | Medium | Do not rely on informal conversations when a deed can record ownership clearly. |

Property ownership | ||||

Presumption Of Advancement | An old presumption that some transfers to close family were intended as gifts. | A clear declaration can displace arguments about gift presumptions. | Low | Presumptions are uncertain and should not replace express drafting. |

Tax or administration | ||||

Consideration | Value given for a transaction, such as money, debt assumption, or other benefit. | May be recited where interests are transferred or shares are adjusted. | Medium | Consideration can affect SDLT, CGT, and enforceability analysis. |

Document clause | ||||

Nominal Consideration | A small stated amount used to evidence a formal transaction. | Sometimes appears in deed recitals or operative wording. | Low | Nominal consideration does not necessarily avoid tax consequences. |

Property ownership | ||||

Transfer Of Equity | Changing who legally owns a property without a full sale to a third party. | May be needed alongside a declaration if legal owners are changing. | High | A declaration of trust alone may not transfer legal title. |

Registration or evidence | ||||

TR1 Transfer Form | HM Land Registry form used to transfer the whole of a registered title. | May be used alongside a declaration when legal title changes. | Medium | The TR1 trust panel can affect co-ownership evidence and should be completed carefully. |

Application To Enter A Restriction | A Land Registry application to add a restriction protecting a trust or co-owner interest. | Administrative step after signing where a restriction is needed on the title. | High | Signing a deed does not always update the register automatically. |

Property ownership | ||||

Overreaching | A mechanism by which beneficiaries’ interests shift from land to sale money on a proper sale. | Relevant to sale provisions and why two trustees may be needed for land sales. | Medium | Beneficiaries may not block a buyer if interests are properly overreached. |

Tax or administration | ||||

Two Trustees For Sale Of Trust Land | A common requirement for sale money to be paid to at least two trustees or a trust corporation. | Relevant where trustees may sell land and give a good receipt for proceeds. | Medium | A sole trustee of land can create practical sale and conveyancing issues. |

Document clause | ||||

Consent To Sale Clause | A clause requiring specified people to agree before trust property is sold. | Sets whether all beneficiaries, certain trustees, or a protector must consent. | Medium | Too-strict consent requirements can deadlock a future sale. |

Dispute Resolution Clause | A clause explaining how disagreements should be handled. | May require negotiation, mediation, expert determination, or court action. | Medium | It should not prevent urgent court applications where needed. |

Notices Clause | A clause saying how formal communications must be sent. | Used for revocation notices, amendment notices, trustee changes, or consent requests. | Low | Outdated addresses can make notices difficult to prove. |

Entire Agreement Clause | A clause saying the written document is the full agreement on the subject. | Helps prevent reliance on side discussions about beneficial ownership. | Low | It may not exclude fraud, mistake, or statutory rights. |

Counterparts | Separate identical copies signed by different parties as one document. | Allows parties in different places to sign matching copies. | Low | Each counterpart should be identical and properly dated. |

Electronic Signature | Signing a document using an electronic method rather than wet ink. | May be used if deed execution, witnessing, and platform evidence requirements are met. | Medium | Witnessing of deeds generally still requires the witness to be physically present. |

Registration or evidence | ||||

Date Of Declaration | The date the trust is declared or the deed takes effect. | Appears at the start of the deed and in execution dating. | Medium | Dating affects tax, registration, priority, and evidence of intention. |

Completion Of The Deed | Final signing, dating, and delivery of the document so it takes effect. | Occurs when all required parties execute and the deed is delivered. | High | Unsigned drafts or undelivered deeds may not be legally effective. |

Document clause | ||||

Delivery Of Deed | An act showing the signer intends the deed to be legally effective. | Usually implied by deed wording and completion steps. | Medium | Signing alone may not be enough if delivery is expressly conditional. |

Registration or evidence | ||||

Original Deed Storage | Keeping the signed original safely for future proof. | Not usually a clause, but essential after execution. | Medium | A lost original can make proof of terms harder, especially on sale or dispute. |

Certified Copy | A copy confirmed as a true copy of the original. | May be supplied to advisers, lenders, HMRC, or Land Registry where needed. | Low | Do not circulate more personal data than necessary. |

Tax or administration | ||||

Anti-Money Laundering Checks | Identity and source of funds checks required in many professional transactions. | Not normally included in the deed, but relevant to property, tax, and professional advice. | Low | Professionals may require ID and source of funds evidence before acting. |

Registration or evidence | ||||

Trust Beneficial Owner Information | Information about settlors, trustees, beneficiaries, and controlling persons. | Deed details help trustees supply required TRS information. | Medium | TRS records must be kept accurate and updated when trust details change. |

Unique Taxpayer Reference Or Unique Reference Number | HMRC reference issued after trust registration or tax registration. | Usually kept in administration records, not in the original deed. | Low | Use the correct reference when filing returns or updating TRS details. |

Tax or administration | ||||

Settlor-Interested Trust | A trust where the settlor or certain close family can benefit. | Relevant where the settlor remains a beneficiary or can revoke the trust. | High | Income tax and inheritance tax effects can differ from non-settlor-interested trusts. |

Trust structure | ||||

Nominee Arrangement | One person holds legal title for another without broad trustee discretion. | May be documented where title is held for the true owner as nominee. | Medium | TRS treatment depends on the exact arrangement and exclusions. |

Declaration By Sole Legal Owner | A sole registered owner declares they hold some or all benefit for others. | Used when legal title stays in one name but beneficial ownership is shared. | High | Mortgage, insolvency, tax, and Land Registry protection should be checked. |

Declaration By Joint Legal Owners | Joint registered owners record how they share the beneficial interest. | Common for couples, relatives, or investors buying property together. | High | Check whether the Land Registry title should show a Form A restriction. |

Life Interest | A right to benefit from property during someone’s lifetime. | May give someone occupation or income for life before capital passes to others. | Medium | Life interest trusts have distinct tax and succession effects. |

Party role | ||||

Remainderman | A person entitled to capital after an earlier interest, such as a life interest, ends. | Named where property passes after a life tenant dies or a condition ends. | Low | Remainder interests should be clearly defined to avoid future disputes. |

Document clause | ||||

Age Contingency | A condition that a beneficiary must reach a stated age before receiving capital. | Used for minor or young beneficiaries, such as entitlement at 18, 21, or 25. | Low | Age conditions can alter tax treatment and trust duration. |

Party role | ||||

Default Beneficiary | A person who benefits if the primary arrangement fails or a condition is not met. | Named to avoid uncertainty if a beneficiary dies or cannot take. | Low | Default gifts should not contradict revocation or amendment powers. |

Document clause | ||||

Death Of A Beneficiary | What happens if a beneficiary dies before the trust ends or property is sold. | May state whether the share passes to the estate, survivors, or substitutes. | Medium | Do not assume a beneficiary’s share automatically passes to co-owners. |

Tax or administration | ||||

Insolvency Of A Beneficiary | What happens when a beneficiary cannot pay debts or becomes bankrupt. | May affect distributions, creditor claims, and trustee decision-making. | Low | Protective wording may not defeat existing creditor rights. |

Document clause | ||||

Confidentiality Clause | A clause limiting disclosure of trust terms or information. | May restrict sharing except with HMRC, Land Registry, lenders, advisers, or law. | Low | It cannot block mandatory disclosures to authorities or courts. |

Tax Indemnity | A promise that specified parties will bear or reimburse particular tax liabilities. | May allocate tax risk on transfers, sale, rent, or revocation. | Medium | Private indemnities do not change who HMRC can assess under tax law. |

No Tax Advice Statement | A statement that the deed does not provide tax advice. | Often included where parties should obtain their own tax advice. | Low | It does not remove real tax liabilities created by the arrangement. |

Registration or evidence | ||||

Mistake In A Trust Deed | An error in wording, parties, property details, or shares. | May require correction, rectification, amendment, or court involvement. | Medium | Do not hand-edit signed deeds without clear legal advice and evidence. |

Rectification | Correction of a document so it matches the parties’ true prior intention. | Relevant if the signed declaration contains a drafting mistake. | Medium | Rectification can be difficult and may require court evidence. |

Document clause | ||||

Variation Of Trust | Changing trust terms after creation. | May be allowed by amendment powers or require beneficiary consent or court approval. | High | Variation may cause tax disposals or require consent from all affected parties. |

Trust structure | ||||

Saunders V Vautier Rule | Adult beneficiaries absolutely entitled can often require trustees to transfer trust property. | Relevant to bare trusts and fixed trusts with adult beneficiaries. | Medium | It may not apply where beneficiaries are minors, unascertained, or not absolutely entitled. |

Property ownership | ||||

Beneficial Joint Tenancy Declaration | A statement that co-owners share the benefit jointly rather than in separate shares. | Used where survivorship is intended for the beneficial interest. | Medium | It may conflict with a will leaving a separate property share. |

Beneficial Tenancy In Common Declaration | A statement that co-owners hold distinct beneficial shares. | Used to record equal or unequal shares that can pass under a will. | High | The title should normally show a Form A restriction for tenants in common. |

Business Or Partnership Property | Assets used or owned in connection with a business or partnership. | May need separate terms if trust property is business-related. | Medium | Company, partnership, tax, and lender documents may restrict trust arrangements. |

Company Shares As Trust Property | Company shares held by trustees for beneficiaries. | Requires share details, company name, class, number, and transfer restrictions. | Medium | Articles, shareholder agreements, PSC rules, and tax should be checked. |

Bank Or Investment Account As Trust Property | Cash or investments held under trust terms. | Identified by account provider, account number, portfolio reference, or schedule. | Medium | Financial institutions may require their own trust account forms and due diligence. |

Personal Chattels As Trust Property | Moveable personal items such as jewellery, art, vehicles, or furniture. | Listed in a schedule with identifying descriptions and values if needed. | Low | Ownership evidence and insurance should match the trust arrangement. |

Tax or administration | ||||

Insurance Of Trust Property | Insurance cover for property held in trust. | May require trustees or occupiers to keep adequate insurance in place. | Medium | The insurer should know the correct ownership and occupation facts. |

Rental Income | Income received from letting trust property. | The deed may state who receives rent and who pays letting expenses. | Medium | Rent must be reported for tax according to the correct beneficial entitlement. |

Principal Private Residence Relief | CGT relief that may apply when selling a main home. | Relevant where the trust property is someone’s home. | Medium | Trust ownership and occupation facts can affect availability of relief. |

Higher Rates For Additional Dwellings | Extra land transaction tax rates that may apply to additional residential property. | Relevant if trust arrangements affect residential property ownership interests. | Medium | Beneficial interests can count for surcharge analysis, not just legal title. |

Property ownership | ||||

Non-UK Assets | Assets outside the United Kingdom included in or affected by the trust. | May require separate governing law, transfer, and local law provisions. | Medium | Foreign law may not recognise or apply the trust as expected. |

Trust structure | ||||

Scottish Trust And Property Differences | Scotland has distinct property and trust law rules from England and Wales. | Governing law and property clauses should be adapted for Scottish assets. | High | Do not use England and Wales land wording for Scottish land without review. |

Property ownership | ||||

Northern Ireland Property Differences | Northern Ireland has its own land registration and property law procedures. | Relevant when trust property is in Northern Ireland. | Medium | Land Registry and tax steps may differ from England and Wales. |

Party role | ||||

Same Person As Trustee And Beneficiary | A person can hold legal duties as trustee while also having a beneficial interest. | Common where co-owners are trustees of land and beneficiaries. | Medium | The document should distinguish the person’s trustee capacity from beneficiary capacity. |

Trust structure | ||||

Sole Trustee And Sole Beneficiary | The same person is both the only trustee and the only beneficiary. | Usually avoided because a trust may collapse if legal and beneficial ownership merge. | Medium | There may be no meaningful trust if one person holds all legal and beneficial interests. |

Merger Of Legal And Beneficial Interests | A trust may end if the same person holds all legal and beneficial ownership. | Relevant when revocation or transfers return all interests to one person. | Low | Check whether the trust still exists after transfers or revocation. |

Document clause | ||||

Trustee Remuneration | Payment to trustees for acting or providing professional services. | States whether trustees may charge fees and on what basis. | Low | Non-professional trustees may need express authority to be paid. |

Tax or administration | ||||

Delegation By Trustees | Trustees appointing agents or professionals to carry out functions. | May allow trustees to instruct solicitors, accountants, agents, or investment managers. | Low | Trustees may still need to supervise delegates properly. |

Document clause | ||||

Investment Powers | Trustees’ authority to invest trust money or assets. | Sets or confirms how trustees may invest trust funds. | Medium | Trustees should consider suitability, diversification, and advice duties. |

Power Of Advancement | Trustees’ power to pay capital early for a beneficiary’s benefit. | May allow early capital payments for education, housing, or support. | Low | It should be consistent with fixed shares and beneficiary rights. |

Power Of Maintenance | Trustees’ power to use income for a beneficiary’s maintenance or education. | Relevant where beneficiaries are minors or not immediately entitled to income. | Low | Income application should match the beneficiary’s entitlement and tax position. |

Party role | ||||

Trust Corporation | A corporate trustee with recognised status for trust administration and conveyancing. | May act as trustee or receive sale proceeds for overreaching purposes. | Low | Ordinary companies are not automatically trust corporations. |

Corporate Trustee | A company appointed to act as trustee. | Named as trustee with company number and registered office. | Low | Check company authority, execution method, and whether professional regulation applies. |

Charitable Beneficiary | A charity named to benefit from the trust. | May be named as a beneficiary or default recipient of remaining assets. | Low | Use the charity’s correct registered name and number. |

Trust structure | ||||

Private Purpose Trust Issue | A trust for a purpose rather than identifiable beneficiaries may be invalid. | Relevant if the deed tries to hold assets for vague purposes only. | Low | Most private trusts need identifiable beneficiaries who can enforce them. |

Registration or evidence | ||||

Letter Of Wishes | A non-binding note explaining the settlor’s preferences. | May guide trustees where they have discretion. | Low | It should not contradict binding trust terms or be treated as a deed. |

Memorandum Of Wishes | Another name for a letter recording non-binding guidance to trustees. | Kept with trust papers to assist discretionary decisions. | Low | It is guidance, not a substitute for clear trust drafting. |

What Should You Check Before Using A UK Declaration Of Trust?

A UK Declaration of Trust should clearly identify the legal owner, the beneficial owner, the trust property, each person’s shares, and whether the arrangement is intended to be revocable. For land, the document should align with the Land Registry title and any Form A restriction or other registered restriction.

Why Does Beneficial Ownership Matter?

Beneficial ownership decides who is entitled to the economic value of the property, such as sale proceeds, rental income, or equity growth. This may differ from the names shown as registered proprietors at HM Land Registry.

When Is Extra Tax Or Registration Advice Needed?

- If the trust affects land, income, capital gains, inheritance tax, or stamp duty land tax, tax advice may be needed before signing.

- Many express trusts must be considered for HMRC Trust Registration Service requirements, even where no tax is immediately due.

- A declaration about jointly owned land should not contradict the mortgage terms, Land Registry title, or any transfer deed.

Why Is Revocation Wording Important?

If the trust is intended to be revocable, the document should say who can revoke it, how revocation is made, and what happens to the trust property afterward. Without clear wording, changing or ending the trust may be difficult.

FAQs

You Might Also Be Interested In