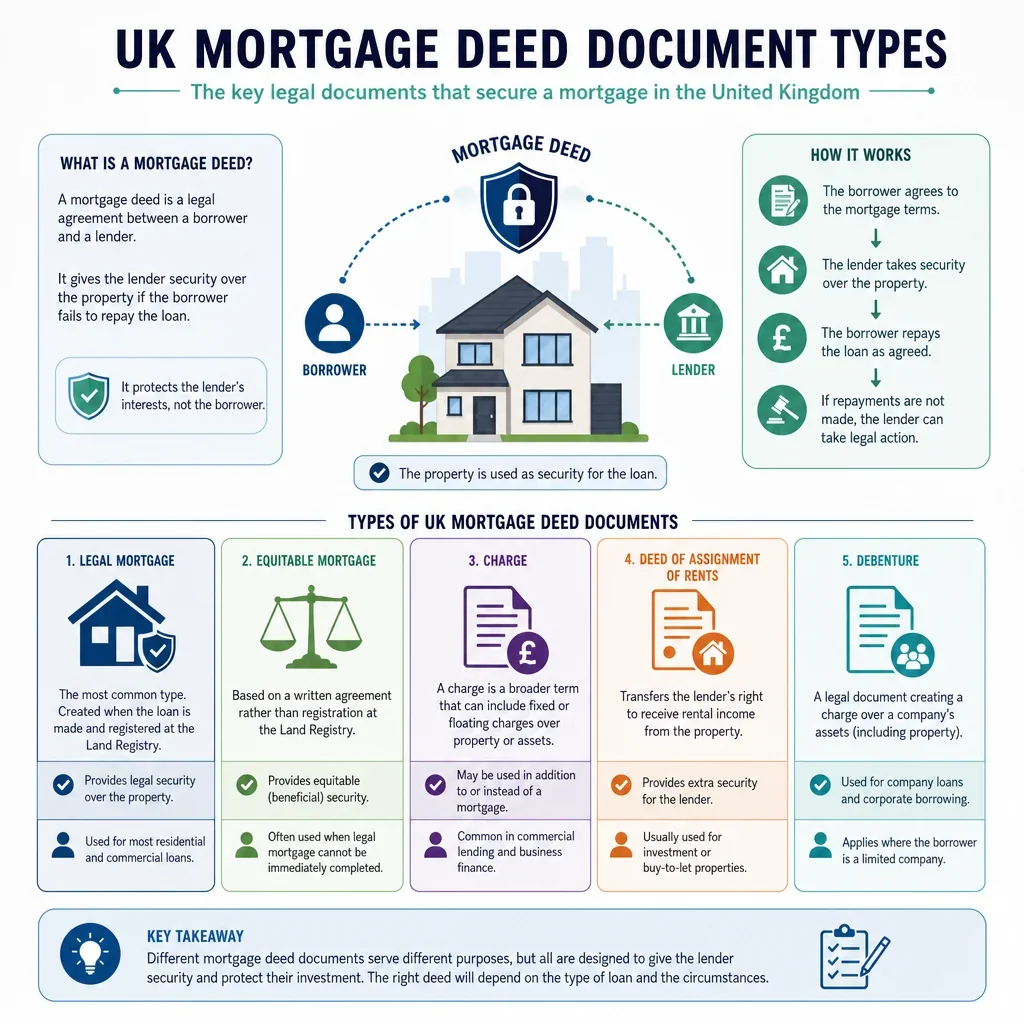

UK Mortgage Deed Document Types

Purpose | Common Use Case | Mortgagor or Chargor | Mortgagee or Chargee | Land Registry Registration | Practical Notes |

|---|---|---|---|---|---|

Legal charge over registered land | |||||

Creates a registered legal mortgage over a registered property title. | Residential Buy-to-let Commercial Mixed use Agricultural | Registered proprietor or borrower granting the charge. | Bank, building society, private lender or other secured creditor. | Usually required | Use the lender's approved form and register promptly to protect priority. |

Mortgage by demise | |||||

Historic legal mortgage method granting a long lease to secure repayment. | Other | Freehold owner granting the mortgage term. | Lender taking the mortgage term as security. | Depends on circumstances | Rare in modern practice legal charge is usually preferred for registered land. |

Mortgage by sub-demise | |||||

Historic leasehold mortgage method granting an underlease as security. | Other | Leaseholder granting an underlease security interest. | Lender receiving leasehold security. | Depends on circumstances | Check lease restrictions and prefer registered legal charge in most transactions. |

Residential mortgage deed | |||||

Secures a home loan against a residential property. | Residential | Homeowner borrower. | Residential mortgage lender. | Usually required | Must match mortgage offer, title number, borrowers and lender conditions. |

Buy-to-let mortgage deed | |||||

Secures a loan over property intended for letting to tenants. | Buy-to-let | Landlord borrower or property-owning company. | Buy-to-let lender. | Usually required | Check letting permissions, tenancy type, licensing and lender consent requirements. |

Commercial legal charge | |||||

Secures business lending against commercial property. | Commercial Mixed use | Company, LLP, partnership or individual property owner. | Commercial lender or secured creditor. | Usually required | Often paired with debenture, guarantees and rent assignment. |

All-monies legal charge | |||||

Secures all present and future liabilities owed to the lender. | Residential Buy-to-let Commercial Mixed use Agricultural | Borrower or third-party property owner. | Lender with ongoing banking relationship. | Usually required | Borrower should check whether future loans are also secured. |

Fixed-sum legal charge | |||||

Secures a specific loan or defined maximum amount. | Residential Buy-to-let Commercial Mixed use | Borrower or property owner granting defined security. | Lender advancing the specified facility. | Usually required | Useful where parties want security limited to a named debt. |

Second charge mortgage deed | |||||

Creates security ranking behind an existing first charge. | Residential Buy-to-let Commercial Mixed use | Property owner with existing mortgage. | Second charge lender. | Usually required | First lender consent and priority arrangements are often needed. |

Equitable charge over land | |||||

Creates non-legal security where legal charge requirements are not met. | Commercial Other | Beneficial owner, contract purchaser or chargor. | Creditor taking equitable security. | Depends on circumstances | Protection may require notice, restriction or land charge registration. |

Mortgage of unregistered land | |||||

Secures lending over land not yet registered at HM Land Registry. | Residential Commercial Agricultural Other | Legal estate owner of unregistered land. | Lender requiring security over unregistered title. | Usually required | A first legal mortgage normally triggers compulsory first registration. |

Legal charge of part | |||||

Secures a loan over part only of a registered title. | Commercial Agricultural Mixed use Other | Owner charging a defined part of the land. | Lender taking security over the defined part. | Usually required | Requires accurate plan and clear identification of charged land. |

Leasehold legal charge | |||||

Secures lending against a leasehold estate. | Residential Buy-to-let Commercial Mixed use | Leaseholder borrower. | Lender secured on the leasehold title. | Usually required | Check alienation, mortgage consent and notice provisions in the lease. |

Shared ownership mortgage deed | |||||

Secures lending over a borrower's shared ownership leasehold interest. | Residential | Shared owner leaseholder. | Shared ownership mortgage lender. | Usually required | Requires compliance with lease, staircasing and landlord consent requirements. |

Guarantor mortgage deed | |||||

Secures another person's borrowing against the guarantor's property. | Residential Buy-to-let Commercial Other | Guarantor property owner. | Lender to the principal borrower. | Usually required | Independent legal advice is commonly required for enforceability and risk disclosure. |

Third-party legal charge | |||||

Secures a borrower's debt using property owned by another person. | Residential Commercial Other | Third-party property owner. | Lender to another borrower. | Usually required | Undue influence risk makes independent advice especially important. |

Deed of priority | |||||

Agrees ranking between two or more secured creditors. | Residential Buy-to-let Commercial Mixed use | Borrower may join to acknowledge priority terms. | First and subsequent secured lenders. | Sometimes required | Register or note priority where needed to bind later parties. |

Deed of postponement | |||||

Postpones one security interest behind another. | Residential Commercial Mixed use Other | Borrower or interest holder may be party. | Lender receiving priority and postponed creditor. | Sometimes required | Common where a second lender or family charge must rank later. |

Intercreditor deed | |||||

Regulates rights, enforcement and priority between multiple creditors. | Commercial Mixed use Other | Corporate borrower or security provider usually joins. | Senior lender, mezzanine lender and other creditors. | Depends on circumstances | Check standstill, enforcement, turnover and release mechanics. |

Deed of substituted security | |||||

Replaces existing mortgaged property with substitute security. | Residential Commercial Agricultural Other | Borrower providing replacement property security. | Existing secured lender. | Usually required | Coordinate discharge of old charge and registration of new charge. |

Deed of variation of mortgage | |||||

Varies terms of an existing registered mortgage or charge. | Residential Buy-to-let Commercial Mixed use Agricultural | Existing borrower or chargor. | Existing secured lender. | Sometimes required | Material changes may affect priority or require consent from later chargees. |

Further advance deed | |||||

Secures additional lending under or alongside an existing charge. | Residential Buy-to-let Commercial Mixed use Agricultural | Existing mortgagor receiving more borrowing. | Existing secured lender. | Depends on circumstances | Priority of further advances depends on register entries and later charges. |

Transfer of registered charge | |||||

Transfers the benefit of an existing registered mortgage to another lender. | Residential Buy-to-let Commercial Mixed use Agricultural | Existing borrower usually not the transferor. | Outgoing and incoming chargee. | Usually required | Use HM Land Registry form TR4 for registered charges. |

Deed of release or discharge of registered charge | |||||

Releases a registered mortgage from the property title. | Residential Buy-to-let Commercial Mixed use Agricultural | Borrower whose secured debt has been repaid. | Existing lender releasing the charge. | Usually required | Lender executes DS1 or electronic discharge to remove the charge. |

Electronic discharge notification | |||||

Electronically notifies HM Land Registry that a charge is discharged. | Residential Buy-to-let Commercial Mixed use | Borrower whose mortgage is redeemed. | Lender using electronic discharge service. | Usually required | Only available to lenders using Land Registry electronic discharge channels. |

Deed of partial release of mortgage | |||||

Releases part of the charged land from an existing mortgage. | Commercial Agricultural Mixed use Other | Borrower retaining a charge over remaining land. | Existing lender releasing part of its security. | Usually required | Requires plan and DS3 or suitable deed identifying released land. |

Form DS3 release of part | |||||

Land Registry form releasing part of land from a registered charge. | Commercial Agricultural Mixed use Other | Borrower seeking release of part of charged title. | Registered chargee giving the release. | Usually required | Use where only part of the registered title is discharged. |

Mortgage securing guarantee obligations | |||||

Secures payment obligations under a guarantee or indemnity. | Commercial Residential Other | Guarantor or indemnifier owning property. | Creditor benefiting from the guarantee. | Usually required | Ensure secured obligations are clearly defined and advice is documented. |

Company legal charge over land | |||||

Creates property security granted by a company or LLP. | Commercial Buy-to-let Mixed use Agricultural | Company or LLP property owner. | Corporate lender or secured creditor. | Usually required | Also register most company charges at Companies House within 21 days. |

Debenture with fixed and floating charges | |||||

Creates security over company assets, often including land and receivables. | Commercial Mixed use Agricultural Other | Company or LLP borrower. | Bank, asset lender or security trustee. | Sometimes required | Land charging provisions may need Land Registry protection plus Companies House filing. |

Security trust deed | |||||

Allows a security trustee to hold mortgage security for creditors. | Commercial Mixed use Other | Borrower or security provider. | Security trustee for finance parties. | Depends on circumstances | Useful for syndicated lending and changing lender groups. |

Assignment of rent by way of security | |||||

Assigns rental income to support repayment of property lending. | Buy-to-let Commercial Mixed use | Landlord borrower assigning rental income. | Property lender or security trustee. | Not usually required | Tenant notices and rent account controls may be needed. |

Charge over rent deposit account | |||||

Secures obligations using money held in a rent deposit account. | Commercial Mixed use | Tenant or depositor granting account security. | Landlord or lender taking account security. | Not usually required | Control, account terms and insolvency ranking should be checked. |

Charge over deposit account supporting mortgage | |||||

Creates cash collateral for mortgage or development funding obligations. | Commercial Mixed use Other | Borrower, sponsor or cash collateral provider. | Lender or account bank. | Not usually required | Account control and notice terms determine security strength. |

Development finance legal charge | |||||

Secures staged lending for construction or redevelopment projects. | Commercial Mixed use Residential | Developer or site-owning SPV. | Development lender or security trustee. | Usually required | Usually paired with step-in rights, assignments and monitoring obligations. |

Bridging loan legal charge | |||||

Secures short-term bridging finance against property. | Residential Buy-to-let Commercial Mixed use | Borrower needing short-term property finance. | Bridging lender. | Usually required | Check exit strategy, default interest and first or second ranking status. |

Regulated residential mortgage deed | |||||

Secures a mortgage that is regulated under UK financial services rules. | Residential | Individual borrower occupying or connected to the dwelling. | Authorised mortgage lender or administrator. | Usually required | Ensure FCA perimeter, offer and consumer protections are addressed. |

Lifetime mortgage deed | |||||

Secures equity release borrowing repayable on death, sale or long-term care. | Residential | Older homeowner borrower. | Lifetime mortgage provider. | Usually required | Advice, occupancy rights and early repayment charges are critical. |

Home purchase plan legal charge | |||||

Supports Islamic or alternative home finance ownership arrangements. | Residential | Customer or trustee depending on finance structure. | Home purchase plan provider or financier. | Depends on circumstances | Structure must match title ownership, trust and FCA requirements. |

Murabaha or diminishing musharakah security deed | |||||

Provides property security for Sharia-compliant acquisition finance. | Residential Commercial Mixed use | Customer, trustee or property-owning vehicle. | Islamic bank, financier or security trustee. | Usually required | Ensure security aligns with beneficial ownership and finance structure. |

Agricultural charge | |||||

Secures farming assets, stock and agricultural property interests. | Agricultural | Farmer or agricultural business. | Agricultural lender or bank. | Depends on circumstances | Separate agricultural charges registration may apply beyond Land Registry. |

Farm mortgage legal charge | |||||

Secures lending over farmland, farm buildings and rural title. | Agricultural | Farmer, landowner or farming company. | Agricultural bank or rural lender. | Usually required | Check tenancies, subsidies, rights of way and environmental restrictions. |

Fixed charge over fixtures and plant | |||||

Secures fixtures, plant and equipment associated with mortgaged property. | Commercial Agricultural Mixed use | Business owner or property company. | Asset or property lender. | Depends on circumstances | Define fixtures versus chattels and coordinate with asset finance claims. |

Floating charge over property assets | |||||

Secures changing business assets connected with property operations. | Commercial Mixed use Agricultural Other | Company or LLP borrower. | Corporate lender or security trustee. | Not usually required | Companies House registration is normally essential for company charges. |

Occupier consent and postponement deed | |||||

Postpones an occupier's rights behind the lender's mortgage. | Residential Buy-to-let | Adult occupier or non-owning spouse usually signs. | Residential or buy-to-let lender. | Not usually required | Important where occupier has actual occupation or potential overriding rights. |

Spousal consent to mortgage deed | |||||

Confirms a spouse consents to mortgage and postpones occupancy claims. | Residential | Non-owning spouse or civil partner. | Mortgage lender relying on the consent. | Not usually required | Independent advice may be needed where influence or disadvantage is possible. |

Board minutes approving mortgage deed | |||||

Records company authority to grant mortgage security. | Commercial Buy-to-let Mixed use Agricultural | Company granting the charge. | Lender relying on corporate authority. | Not usually required | Check articles, conflicts, benefit and execution authority. |

Shareholder resolution approving mortgage security | |||||

Approves mortgage security where company constitution or transaction requires it. | Commercial Mixed use Other | Company security provider and its members. | Lender seeking evidence of authority. | Not usually required | Useful for substantial transactions, conflicts or group guarantees. |

Power of attorney to execute mortgage deed | |||||

Authorises an attorney to sign mortgage documents for another party. | Residential Commercial Mixed use Agricultural Other | Borrower, company or absent property owner. | Lender relying on attorney execution. | Sometimes required | Land Registry may require evidence of the attorney's authority. |

Trustee legal charge | |||||

Creates security over property held by trustees. | Residential Commercial Agricultural Other | Trustees of land or settlement trustees. | Lender to trustees or beneficiaries. | Usually required | Check trustee powers, beneficiary consent and overreaching requirements. |

Personal representative mortgage deed | |||||

Secures borrowing over estate property administered by personal representatives. | Residential Commercial Agricultural Other | Executors or administrators of the estate. | Estate lender or secured creditor. | Usually required | Grant of probate or letters of administration may be required. |

Joint borrower legal charge | |||||

Secures a mortgage granted by co-owners or joint borrowers. | Residential Buy-to-let Commercial Mixed use | Joint tenants or tenants in common. | Lender to all or selected co-owners. | Usually required | All registered proprietors usually need to execute the charge. |

Charge over beneficial interest in property | |||||

Secures a beneficiary's interest rather than the legal title. | Residential Commercial Other | Beneficiary or beneficial owner. | Creditor taking equitable security. | Depends on circumstances | Protection may be by restriction, not a registered legal charge. |

Charging order over land | |||||

Court-created security for a judgment debt over property. | Residential Commercial Other | Judgment debtor property owner. | Judgment creditor. | Usually required | Usually protected by notice or restriction depending on title ownership. |

Restriction protecting lender consent | |||||

Prevents registration of dealings without lender consent or certificate. | Commercial Residential Mixed use Other | Registered proprietor subject to restriction. | Lender or beneficiary of restriction. | Usually required | Use where lender wants control beyond the registered charge entry. |

Unilateral notice for equitable mortgage | |||||

Protects an equitable mortgage or security interest on the register. | Residential Commercial Other | Owner whose title is subject to claimed interest. | Creditor claiming equitable security. | Usually required | Does not prove validity it protects priority of the claimed interest. |

Agreed notice for security interest | |||||

Registers an agreed notice of a mortgage-related third-party interest. | Commercial Residential Other | Registered proprietor acknowledging the interest. | Beneficiary of the security interest. | Usually required | Requires proprietor consent or evidence of the protected interest. |

Mortgagee consent to lease deed | |||||

Confirms lender consent to grant or vary a lease of mortgaged property. | Buy-to-let Commercial Mixed use Agricultural | Landlord borrower granting the lease. | Lender whose charge affects the property. | Depends on circumstances | Needed where mortgage conditions restrict letting or lease priority. |

Landlord consent to leasehold mortgage | |||||

Confirms landlord consent to a tenant charging leasehold property. | Residential Commercial Mixed use | Leaseholder borrower. | Leasehold mortgage lender. | Not usually required | Check lease clause requiring consent before charging. |

Management company mortgage consent deed | |||||

Records management company consent or covenant for leasehold mortgage dealings. | Residential Mixed use | Flat owner or leaseholder borrower. | Leasehold lender relying on consent. | Depends on circumstances | Often required by leasehold title restrictions before registration. |

Mixed-use property mortgage deed | |||||

Secures lending over property with residential and commercial elements. | Mixed use | Owner of mixed-use property. | Mixed-use or commercial lender. | Usually required | Assess residential regulation, leases, planning use and valuation split. |

Portfolio legal charge | |||||

Secures one facility over multiple property titles. | Buy-to-let Commercial Mixed use Agricultural | Portfolio landlord, investor or property company. | Portfolio lender or security trustee. | Usually required | List title numbers carefully and manage cross-collateralisation risk. |

Cross-collateral mortgage deed | |||||

Allows several properties to secure one or more related debts. | Buy-to-let Commercial Mixed use Agricultural | Borrower or group security providers. | Lender with security over multiple assets. | Usually required | Releasing one property may require lender valuation and partial discharge. |

Legal charge over airspace or development rights | |||||

Secures lending over separable development or airspace interests. | Commercial Mixed use Other | Developer or rights holder. | Development lender or investor. | Depends on circumstances | Requires precise title structure, plans and rights of support or access. |

Charge over option or pre-emption rights | |||||

Secures contractual land acquisition rights as collateral. | Commercial Agricultural Other | Option holder or buyer with contract rights. | Lender funding acquisition or development. | Depends on circumstances | Protect underlying option by notice and check assignability. |

Assignment of sale proceeds by way of security | |||||

Assigns property sale proceeds to repay secured debt. | Commercial Residential Other | Seller or borrower entitled to sale proceeds. | Creditor expecting repayment from completion funds. | Not usually required | Coordinate with conveyancer undertakings and completion statement. |

Escrow deed for mortgage completion funds | |||||

Controls release of funds pending mortgage completion or registration steps. | Commercial Residential Mixed use Other | Borrower, buyer or seller depending on transaction. | Lender or stakeholder benefiting from escrow conditions. | Not usually required | Use precise release conditions tied to searches, completion and registration. |

Self-build mortgage legal charge | |||||

Secures staged lending for an owner-led residential build. | Residential Other | Self-build borrower or plot owner. | Self-build mortgage lender. | Usually required | Drawdowns depend on planning, build stage, insurance and valuation. |

Right to Buy mortgage deed | |||||

Secures lending for purchase of a council or housing association home. | Residential | Right to Buy purchaser. | Residential mortgage lender. | Usually required | Check discount repayment restrictions and landlord conveyancing conditions. |

Equity loan second charge | |||||

Secures an equity loan behind the buyer's main mortgage. | Residential | Homebuyer receiving equity loan assistance. | Equity loan administrator or government-backed chargee. | Usually required | Redemption and sale usually require administrator consent and repayment calculation. |

Local authority legal charge | |||||

Secures council loans, grants, deferred payment or housing assistance. | Residential Other | Property owner receiving local authority funding. | Local authority. | Usually required | Check statutory scheme, repayment triggers and priority with existing lender. |

Deferred payment agreement legal charge | |||||

Secures adult social care fees deferred against a property. | Residential Other | Care recipient or property owner. | Local authority. | Usually required | Repayment normally arises on sale, death or termination of agreement. |

Security over park home pitch rights | |||||

Secures obligations linked to a park home or pitch agreement. | Residential Other | Park home owner or occupier. | Specialist lender or creditor. | Not usually required | Park homes are usually not registered land use specialist security wording. |

Release of guarantor legal charge | |||||

Releases a guarantor's property from mortgage security. | Residential Commercial Other | Guarantor whose property was charged. | Lender releasing guarantor security. | Usually required | Ensure guarantee and property charge are both released if intended. |

Deed of rectification of mortgage | |||||

Corrects errors in an executed mortgage or security deed. | Residential Buy-to-let Commercial Mixed use Agricultural Other | Original mortgagor or chargor. | Original lender or chargee. | Sometimes required | Use carefully where title number, parties, plan or obligations were wrong. |

Deed of confirmation of mortgage security | |||||

Confirms existing security remains effective after amendments or events. | Commercial Buy-to-let Mixed use Agricultural Other | Existing security provider. | Existing lender or security trustee. | Depends on circumstances | Useful on refinancing amendments, borrower changes or facility restatements. |

Accession deed to mortgage security | |||||

Adds a new borrower, guarantor or lender to security arrangements. | Commercial Mixed use Other | New obligor or security provider. | Existing finance parties or security trustee. | Depends on circumstances | May require new Land Registry or Companies House filings. |

Deed of assumption of mortgage obligations | |||||

Transfers or assumes mortgage obligations with lender consent. | Residential Commercial Buy-to-let Other | Incoming borrower or continuing security provider. | Existing lender consenting to assumption. | Sometimes required | Often used with transfer of equity or corporate restructurings. |

Transfer of equity with mortgage covenant | |||||

Changes ownership while preserving or creating mortgage obligations. | Residential Buy-to-let | Outgoing, incoming and continuing co-owners. | Existing lender consenting to ownership change. | Usually required | Lender consent is usually needed before releasing or adding borrowers. |

Overseas company legal charge over UK land | |||||

Secures UK land owned or acquired by an overseas entity. | Commercial Residential Mixed use Other | Overseas entity owning UK land. | UK or international lender. | Usually required | Check overseas entity ID and registration restrictions before completion. |

Legal charge over property in Wales | |||||

Creates mortgage security over registered Welsh land. | Residential Buy-to-let Commercial Agricultural Mixed use | Welsh property owner or borrower. | Lender secured on Welsh land. | Usually required | HM Land Registry covers England and Wales Welsh tax and devolved rules may matter. |

Standard security over Scottish property | |||||

Creates the main form of heritable security over Scottish land. | Residential Buy-to-let Commercial Agricultural Mixed use | Scottish property owner granting standard security. | Creditor in the standard security. | Not usually required | Register with Registers of Scotland, not HM Land Registry. |

Legal charge over Northern Ireland property | |||||

Creates mortgage security over land in Northern Ireland. | Residential Buy-to-let Commercial Agricultural Mixed use | Northern Ireland property owner or borrower. | Lender secured on Northern Ireland land. | Not usually required | Use Northern Ireland land registration processes, not HM Land Registry. |

Legal charge with receiver powers | |||||

Creates security and contractual powers to appoint a receiver on default. | Buy-to-let Commercial Mixed use Agricultural | Landlord, investor or commercial borrower. | Lender with enforcement rights. | Usually required | Review express receiver powers, rent collection and enforcement triggers. |

Legal charge with power of sale | |||||

Creates security including lender sale rights after default. | Residential Buy-to-let Commercial Mixed use Agricultural | Borrower or property owner. | Lender with statutory and contractual sale rights. | Usually required | Statutory power arises under Law of Property Act 1925 subject to conditions. |

Mortgage deed with consolidation clause | |||||

Allows lender to link repayment across separate mortgages where valid. | Commercial Buy-to-let Agricultural Other | Borrower with multiple secured properties or debts. | Lender seeking consolidated security rights. | Usually required | Express wording is needed to preserve consolidation rights. |

Mortgage deed securing future advances | |||||

Secures further or future lending under the same charge. | Commercial Buy-to-let Residential Mixed use Agricultural | Borrower expecting additional drawdowns. | Lender funding present and future advances. | Usually required | Register obligations and priority arrangements affect future advance ranking. |

Mortgage deed with negative pledge | |||||

Restricts the borrower from creating later security without consent. | Commercial Buy-to-let Mixed use Agricultural | Borrower agreeing not to grant competing security. | Lender seeking priority protection. | Depends on circumstances | May be backed by restrictions, covenants and event of default wording. |

Charge over freehold reversion subject to leases | |||||

Secures lending over landlord's reversionary interest and rental stream. | Buy-to-let Commercial Mixed use | Freehold landlord or property investor. | Investment property lender. | Usually required | Review occupational leases, rent deposits and tenant rights before completion. |

Charge over headlease subject to underleases | |||||

Secures a borrower's headlease interest in income-producing property. | Commercial Mixed use Buy-to-let | Headlease tenant or property investor. | Leasehold investment lender. | Usually required | Check superior landlord consent, forfeiture risk and underlease income. |

New-build plot mortgage deed | |||||

Secures purchase finance over a newly built or newly created title. | Residential Buy-to-let | New-build buyer or investor. | Residential or buy-to-let lender. | Usually required | Check estate transfers, plans, warranties, roads, sewers and title setup. |

Shared equity legal charge | |||||

Secures an equity stake or shared equity loan against the home. | Residential | Homebuyer receiving shared equity funding. | Equity provider, developer or public body. | Usually required | Check valuation formula, sale restrictions and priority behind main lender. |

Consent dealing with matrimonial home rights | |||||

Addresses spouse or civil partner home rights affecting mortgaged property. | Residential | Spouse, civil partner or property owner. | Lender requiring priority over home rights. | Depends on circumstances | Registered home rights may affect lender priority and completion requirements. |

Solicitor undertaking to redeem mortgage | |||||

Undertakes to repay and discharge an existing mortgage on completion. | Residential Buy-to-let Commercial Mixed use | Seller or borrower acting through conveyancer. | Buyer, lender or conveyancer relying on redemption. | Not usually required | Critical where sale proceeds redeem an existing charge after completion. |

Solicitor undertaking to register legal charge | |||||

Confirms conveyancer will apply to register lender's charge after completion. | Residential Buy-to-let Commercial Mixed use Agricultural | Borrower represented by conveyancer. | Lender relying on post-completion registration. | Not usually required | Does not itself create security it supports completion risk management. |

Certificate of title for mortgage lender | |||||

Certifies title investigation before lender releases mortgage funds. | Residential Buy-to-let Commercial Mixed use | Borrower whose conveyancer certifies title. | Mortgage lender receiving the certificate. | Not usually required | Lender relies on solicitor certification before advancing funds. |

Counterpart mortgage deed | |||||

Allows parties to sign separate counterparts of the same mortgage deed. | Commercial Residential Mixed use Other | Borrower or security provider signing a counterpart. | Lender or security trustee signing another counterpart. | Depends on circumstances | Execution must satisfy deed formalities and lender completion requirements. |

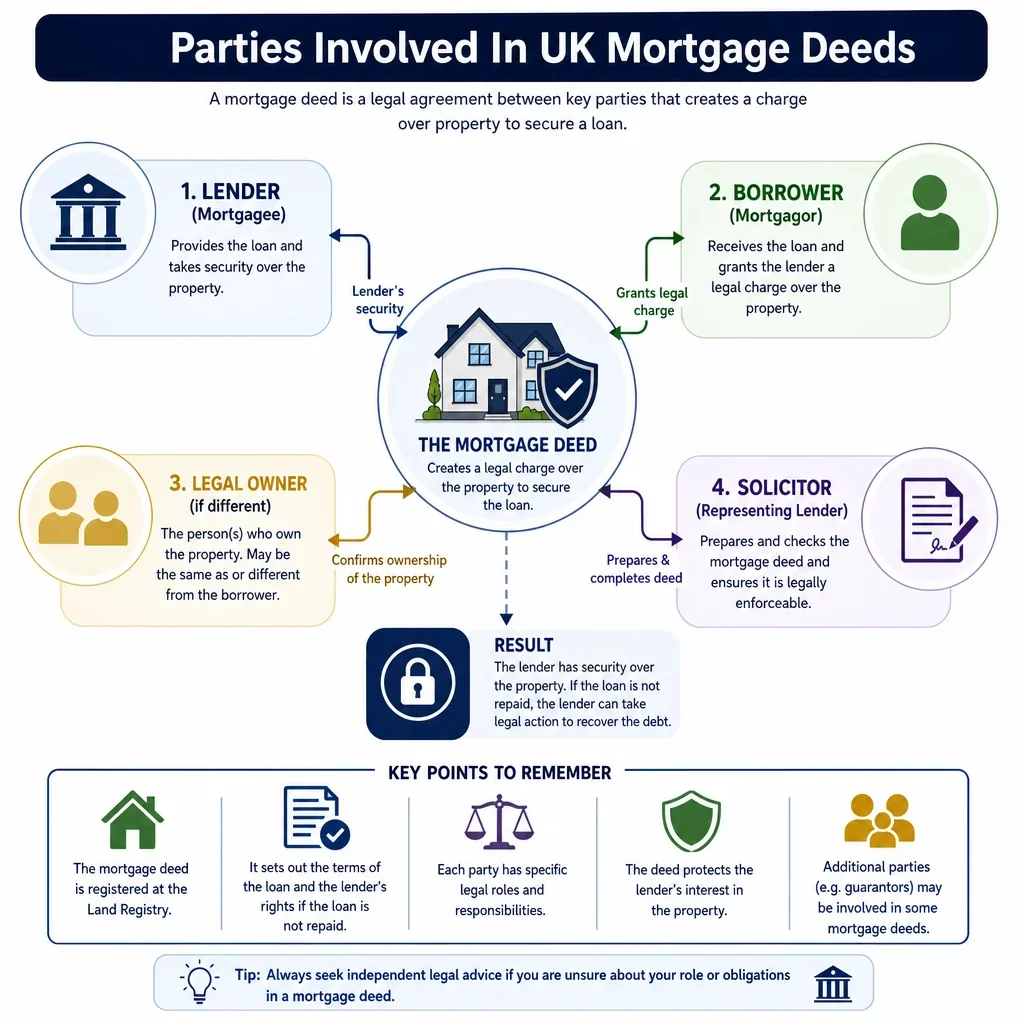

Which UK Mortgage Deed Type Should Be Used?

Most UK property security is created by a legal charge by deed over registered land, not by transferring ownership to the lender. For registered land, the charge will normally need HM Land Registry registration to take effect as a registered charge and to protect the lender\'s priority.

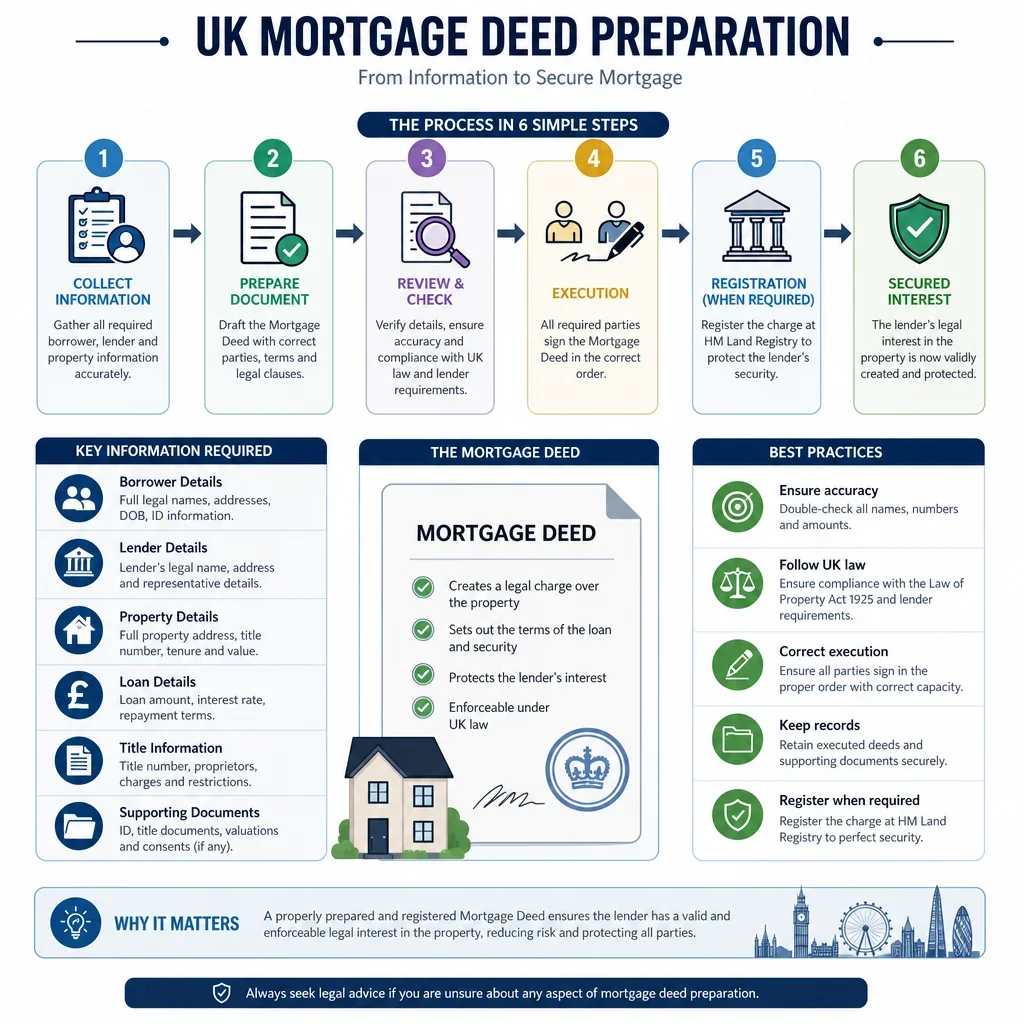

When Is HM Land Registry Registration Usually Needed?

Registration is usually required for legal charges over registered land and for many charges created on first registration or by remortgage. It may also be needed when an existing charge is varied, transferred, postponed, substituted or released. Some supporting documents, such as consents, occupier waivers and board minutes, are not normally registered as standalone deeds but are often required by the lender before completion.

What Extra Documents Are Common For Companies And Specialist Lending?

Corporate borrowers commonly need company charges, board approvals and Companies House registration in addition to Land Registry registration. Commercial, mixed-use, agricultural and development transactions often add debentures, assignments of rent, rent deposit charges, postponement deeds, intercreditor deeds or agricultural charges, depending on the assets and priority structure.

What Should Borrowers And Lenders Check Before Signing?

- Execution formalities: mortgage deeds must be validly executed as deeds, with correct witnessing or corporate execution.

- Priority: second charges, further advances and refinancing often require consent, priority or postponement arrangements.

- Scope of liability: all-monies charges, guarantees, indemnity mortgages and debentures may secure more than one loan or obligation.

- Property type: leasehold, shared ownership, agricultural, commercial and development property usually need additional consents or tailored wording.

- Release and discharge: a DS1, END or other release document is commonly needed when a registered mortgage is repaid.

FAQs

You Might Also Be Interested In