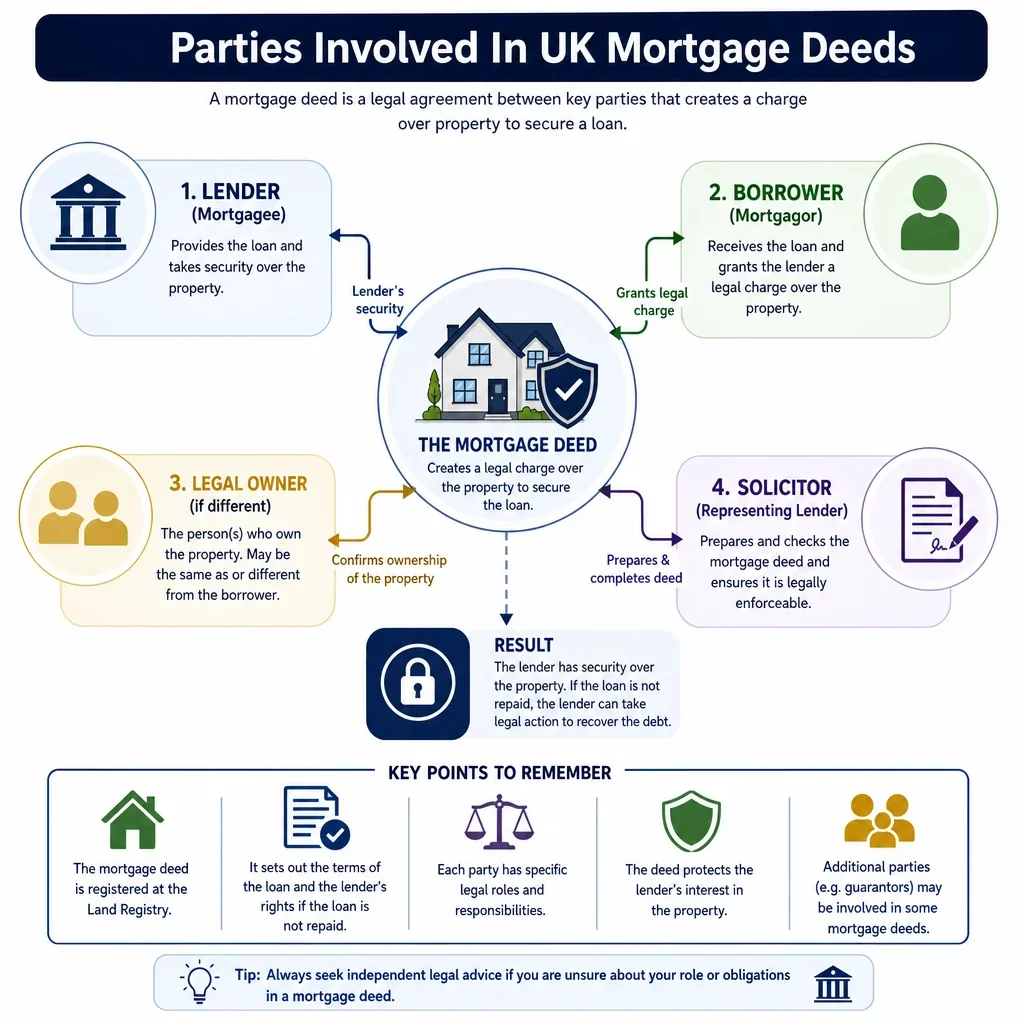

Parties Involved In UK Mortgage Deeds

Created:

Learn who is involved in UK mortgage deeds and why each role matters. This dataset is useful for understanding lender, borrower, and witness responsibilities in the context of AI Generated British Mortgage Deed documents.

Role Type | Role Description | Signing Requirement | Typical Obligations | Common Evidence Needed |

|---|---|---|---|---|

Individual borrower | ||||

Borrower | Person borrowing money and granting the lender a legal charge over their property. | Usually signs | Repay the loan, pay interest, comply with mortgage conditions and preserve the security. | Proof of identity, address, title ownership, mortgage offer and signed deed. |

Joint borrower | ||||

Borrower | Co-borrower jointly granting security and sharing repayment liability with other borrowers. | Usually signs | Joint and several repayment liability and compliance with all mortgage terms. | ID for each borrower, ownership details, mortgage offer and execution pages. |

Sole proprietor borrower | ||||

Borrower | Only registered owner of the charged property and borrower under the mortgage. | Usually signs | Repay debt, insure property if required and avoid dealings breaching the charge. | Register entries, ID, address evidence, mortgage offer and witnessed signature. |

Third-party security provider | ||||

Other | Property owner giving security for another person's borrowing without being the main borrower. | Usually signs | Allow enforcement against property if the secured borrower defaults. | Independent legal advice certificate, ID, title evidence and signed legal charge. |

Mortgage lender | ||||

Lender | Provides mortgage funds and takes the legal charge as security. | May sign | Advance funds, issue instructions and release security when the debt is redeemed. | Mortgage offer, lender panel instructions, approved charge form and redemption process. |

Bank or building society lender | ||||

Lender | Regulated institutional lender taking a standard legal mortgage over the property. | May sign | Fund the loan and administer the mortgage under regulatory requirements. | FCA permissions, mortgage offer, UK Finance Handbook instructions and charge wording. |

Private lender | ||||

Lender | Individual or entity advancing funds and taking a negotiated legal charge. | May sign | Advance loan funds and provide discharge when secured debt is paid. | Loan agreement, identity checks, source of funds and executed charge. |

Chargee | ||||

Lender | Person or organisation in whose favour the registered charge is created. | May sign | Hold security and deal with discharge or transfer of the charge as required. | Name, address for service, charge terms and registration details. |

Personal guarantor | ||||

Guarantor | Promises to pay or perform the borrower's obligations if the borrower defaults. | May sign | Pay guaranteed sums, costs and interest after borrower default. | ID, guarantee deed, financial information and independent legal advice evidence. |

Corporate guarantor | ||||

Guarantor | Company giving a guarantee or security support for the borrower's obligations. | May sign | Guarantee payment, indemnify lender and comply with corporate security covenants. | Companies House search, board minutes, authority, constitutional documents and executed guarantee. |

Joint proprietor | ||||

Joint proprietor | Co-owner of registered property whose estate is affected by the legal charge. | Usually signs | Join in charging the whole legal estate and observe owner covenants. | Register entries, ID for each proprietor and joint ownership information. |

Beneficial joint tenant | ||||

Joint proprietor | Co-owner whose beneficial interest passes by survivorship rather than by will. | Usually signs | Join in mortgage execution and repayment obligations if also a borrower. | TR1, title register, declaration of trust if any and ID. |

Tenant in common | ||||

Joint proprietor | Co-owner holding a defined beneficial share in the property. | Usually signs | Charge legal title and comply with mortgage terms affecting the property. | Restriction details, declaration of trust, title register and ID. |

Trustee proprietor | ||||

Trustee | Registered trustee holding legal title and granting a mortgage over trust property. | Usually signs | Exercise trustee powers properly and comply with lender and trust terms. | Trust deed, trustee authority, title register, consents and ID. |

Bare trustee or nominee | ||||

Trustee | Legal title holder acting for the beneficial owner in granting security. | Usually signs | Act within trust authority and execute the charge as legal owner. | Nominee deed, beneficial owner instructions, ID and trust authority. |

Company borrower | ||||

Borrower | Company borrowing money and granting a charge over company-owned property. | Usually signs | Repay debt, comply with loan covenants and register registrable company charges. | Company number, articles, board minutes, director authority and Companies House filing. |

Company director | ||||

Company officer | Officer who may execute the deed for a company with proper authority. | May sign | Sign on behalf of company and confirm authorised execution. | Director appointment, board minutes, company register and ID if required. |

Company secretary | ||||

Company officer | Officer who may countersign a company deed with a director. | May sign | Support valid company execution and maintain company records. | Secretary appointment, board authority and execution clause. |

Authorised company signatory | ||||

Company officer | Person authorised by the company to execute the mortgage deed. | May sign | Execute within authority and evidence valid corporate approval. | Written authority, board resolution, articles and identity evidence. |

Independent adult witness | ||||

Witness | Physically observes an individual sign the deed and attests the signature. | Usually signs | Sign witness block and provide name, address and occupation if required. | Full name, address, signature and confirmation of presence at signing. |

Conveyancer as witness | ||||

Witness | Conveyancer who witnesses execution when present and not conflicted. | May sign | Attest signature and follow professional duties on identity and execution. | Witness details, firm record, ID checks and signing attendance note. |

Borrower's conveyancer | ||||

Conveyancer | Acts for the borrower on title, execution, completion and registration steps. | Does not usually sign | Advise borrower, check title, arrange execution and submit registration application. | Client ID, source of funds, title documents, mortgage offer and signed charge. |

Lender's conveyancer | ||||

Conveyancer | Acts for the lender and ensures the mortgage is valid security. | Does not usually sign | Follow lender instructions, report title issues and protect lender priority. | Lender instructions, certificate of title, searches, signed deed and priority search. |

Panel conveyancer | ||||

Conveyancer | Conveyancer on the lender's panel often acting for both borrower and lender. | Does not usually sign | Comply with UK Finance Handbook and manage any conflict or separate representation. | Panel status, lender instructions, client ID, mortgage offer and certificate of title. |

Licensed conveyancer | ||||

Conveyancer | Regulated conveyancing specialist handling mortgage deed completion and registration. | Does not usually sign | Advise on title, meet lender conditions and submit Land Registry applications. | Client care, ID checks, title records, mortgage offer and signed deed. |

Solicitor | ||||

Conveyancer | Qualified lawyer advising on mortgage deed terms, execution and registration. | Does not usually sign | Advise client, verify identity, manage undertakings and complete registration. | Retainer, ID documents, title papers, lender instructions and execution evidence. |

Chartered legal executive | ||||

Conveyancer | Authorised legal professional who may conduct conveyancing work where permitted. | Does not usually sign | Handle title checks, client advice and registration tasks within authorisation. | Regulated status, retainer, ID checks and file authority. |

Attorney under power of attorney | ||||

Other | Person authorised to execute the mortgage deed for the borrower or proprietor. | Signs only in limited cases | Act within the power, in the donor's interests and disclose attorney capacity. | Original or certified power of attorney, ID and lender acceptance. |

Donor of power of attorney | ||||

Borrower | Borrower or proprietor whose attorney signs the mortgage deed on their behalf. | Signs only in limited cases | Remain bound by the mortgage executed under valid authority. | ID, capacity evidence if relevant and valid attorney appointment. |

Personal representative | ||||

Trustee | Executor or administrator dealing with estate property and any mortgage transaction. | Signs only in limited cases | Act for the estate and execute documents within probate authority. | Grant of probate or letters of administration, death certificate and ID. |

Beneficiary | ||||

Other | Person with a beneficial interest that may be affected by the mortgage. | May sign | Give consent or postpone interest where required by trust or lender. | Trust deed, consent, ID and evidence of beneficial interest. |

Adult occupier | ||||

Other | Adult living at the property who is not a borrower or registered owner. | May sign | Consent to the mortgage and postpone occupation rights to lender security. | Occupier consent form, ID, age confirmation and independent advice if required. |

Non-owning spouse or civil partner | ||||

Other | Partner with possible home rights despite not being registered owner. | May sign | Consent to mortgage and postpone any home or occupation rights where required. | Consent or postponement, ID and marital or civil partnership status information. |

Person in actual occupation | ||||

Other | Occupier whose rights may affect priority if not postponed or overreached. | May sign | Disclose occupation and sign consent or postponement if required by lender. | Occupier enquiry, consent form, ID and occupation details. |

Existing mortgage lender | ||||

Lender | Current charge holder whose security may be redeemed or postponed. | May sign | Provide redemption statement, discharge, consent or deed of priority if needed. | Redemption statement, DS1 or e-DS1, consent and charge details. |

Second charge lender | ||||

Lender | Lender taking a later-ranking charge behind an existing mortgage. | May sign | Advance funds subject to prior charge and observe priority arrangements. | First lender consent, deed of priority, mortgage offer and signed charge. |

Priority deed party | ||||

Other | Existing or new charge holder agreeing priority between secured debts. | May sign | Agree ranking, enforcement proceeds and limits of secured liabilities. | Executed deed of priority, charge details and lender consents. |

HM Land Registry | ||||

Other | Registers legal charges and updates the registered title after completion. | Does not usually sign | Process applications, enter charges and maintain the land register. | AP1, certified deed, ID evidence if needed, fee and supporting consents. |

Companies House | ||||

Other | Receives registrations of many company-created charges. | Does not usually sign | Register charge particulars and issue certificate of registration. | MR01, certified charge instrument, company number and filing fee. |

Mortgage broker | ||||

Other | Intermediary arranging or advising on the mortgage product before deed completion. | Does not usually sign | Advise on suitable mortgage products and submit application information. | FCA status, disclosure documents, application data and affordability information. |

Valuer or surveyor | ||||

Other | Assesses property value and condition for lending or buyer due diligence. | Does not usually sign | Provide valuation report and disclose material property risks. | Valuation report, surveyor credentials and property inspection information. |

Buildings insurer | ||||

Other | Provides buildings insurance protecting the lender's security and owner's property. | Does not usually sign | Issue policy and note lender interest if required by mortgage terms. | Policy schedule, cover start date, insured risks and lender interest noting. |

Freeholder or landlord | ||||

Other | Owner of the freehold or landlord under a lease affecting leasehold security. | May sign | Give consent, licence to charge or notice receipt if required by the lease. | Lease, licence to charge, notice requirements and receipted notice. |

Management company | ||||

Other | Company managing leasehold or estate obligations relevant to lender security. | May sign | Acknowledge notices, provide information pack or consent under estate documents. | Management pack, accounts, insurance details, notices and consent documents. |

Commonhold association | ||||

Other | Company managing commonhold land where a unit is mortgaged. | May sign | Provide commonhold information and deal with association consents if required. | Commonhold community statement, association information and consent evidence. |

Local authority | ||||

Other | Public authority whose searches, consents or charges may affect the property. | Signs only in limited cases | Provide search data, consent or discharge of local land charges where needed. | Local search, planning documents, building regulation records and charge information. |

Trustee in bankruptcy | ||||

Trustee | Insolvency office-holder controlling a bankrupt owner's property interest. | Signs only in limited cases | Realise or deal with bankrupt estate property within insolvency powers. | Bankruptcy order, appointment evidence, consent and title restriction details. |

Liquidator or administrator | ||||

Other | Office-holder managing an insolvent company's property or security transactions. | Signs only in limited cases | Act within insolvency powers and protect creditors' interests. | Appointment documents, Companies House records, consent or court order if needed. |

Receiver | ||||

Other | Person appointed by a mortgagee to manage or realise secured property. | Signs only in limited cases | Collect income, manage property or sell within mortgage powers. | Appointment deed, mortgage terms, title and authority evidence. |

LLP borrower | ||||

Borrower | Limited liability partnership borrowing and charging LLP-owned property. | Usually signs | Repay borrowing, comply with security covenants and file registrable charges. | LLP number, member authority, agreement, Companies House filing and executed charge. |

LLP member | ||||

Company officer | Member who may sign a mortgage deed for the LLP if authorised. | May sign | Execute within LLP authority and evidence member approval. | Member appointment, LLP resolution, authority and identity if required. |

Partnership borrower | ||||

Borrower | Partnership borrowing where partners or trustees may hold legal title. | Usually signs | Repay partnership debt and bind partners according to authority and agreement. | Partnership agreement, partner authority, title ownership and ID. |

Partner | ||||

Other | Individual partner who may sign or authorise borrowing for a partnership. | May sign | Bind partnership within authority and may share liability for partnership debts. | |

Vulnerable or non-commercial surety | ||||

Guarantor | Person giving guarantee or security where undue influence risk may arise. | May sign | Guarantee or secure another's borrowing after proper explanation and advice. | Independent legal advice certificate, conflict checks, ID and signed guarantee. |

Overseas borrower | ||||

Borrower | Borrower outside the UK executing a mortgage deed for UK property. | Execute validly abroad, repay loan and meet lender certification requirements. | Certified ID, notarised or witnessed deed, address evidence and tax residency details. | |

Notary public | ||||

Other | Authenticates signatures, identity or authority, especially for overseas execution. | May sign | Certify execution, identity or corporate authority where required. | Passport, proof of address, document authority and notarial certificate. |

Interpreter or translator | ||||

Other | Assists a party who cannot sufficiently read or understand English. | May sign | Translate or explain document content accurately and independently. | Interpreter details, translation certificate and attendance note. |

Court-appointed deputy | ||||

Other | Person authorised by the Court of Protection to act for a borrower lacking capacity. | Signs only in limited cases | Act within deputyship order and in the person's best interests. | Deputyship order, ID, lender consent and Court of Protection authority if needed. |

Court of Protection | ||||

Other | Court authorising decisions for people who lack mental capacity. | Does not usually sign | Approve property or mortgage decisions where legal authority is insufficient. | Court order, capacity evidence, deputy details and transaction documents. |

Minor beneficiary | ||||

Other | Child with beneficial interest legal title is held by adult trustees. | Does not usually sign | No deed obligations personally interest managed by trustees. | Trust evidence, trustee authority and any court or guardian consent. |

Leaseholder borrower | ||||

Borrower | Borrower charging a long leasehold interest rather than freehold title. | Usually signs | Repay loan, comply with mortgage and continue lease covenants. | Lease, title register, landlord consent or notice, insurance and service charge data. |

Freeholder borrower | ||||

Borrower | Borrower charging a freehold estate registered in their name. | Usually signs | Repay loan, preserve title, insure and comply with restrictive covenants. | Freehold title register, ID, searches, mortgage offer and executed charge. |

Equitable charge holder | ||||

Lender | Creditor with security that may not be a registered legal charge. | May sign | Record or protect security by notice or restriction where appropriate. | Security agreement, title protection application and borrower consent. |

Restriction beneficiary | ||||

Other | Person whose consent or certificate may be needed under a title restriction. | May sign | Provide consent, certificate or evidence satisfying the restriction. | Restriction wording, consent, certificate and identity or authority evidence. |

Mortgage administrator or servicer | ||||

Other | Entity administering the mortgage account on behalf of the lender or owner. | Does not usually sign | Administer payments, statements, arrears processes and redemption requests. | Servicing authority, account details and redemption statement arrangements. |

Transferee of charge | ||||

Lender | New holder of an existing mortgage charge after assignment or transfer. | May sign | Take benefit of charge and maintain register details after transfer. | Transfer of charge, lender details, AP1 and evidence of authority. |

Security trustee | ||||

Trustee | Holds mortgage security on trust for lenders or finance parties. | May sign | Hold, enforce and release security according to finance documents. | Security trust deed, facility agreement, execution authority and lender details. |

Facility agent | ||||

Other | Coordinates lenders under a syndicated or commercial facility. | May sign | Administer facility notices, conditions precedent and lender communications. | Facility agreement, agency appointment and signing authority. |

Parent or family contributor | ||||

Guarantor | Family member providing guarantee, gifted deposit or supporting security. | May sign | Confirm gift, waive interest or guarantee obligations depending on arrangement. | Gift letter, ID, source of funds and independent legal advice if guaranteeing. |

Gifted deposit donor | ||||

Other | Person providing deposit funds without taking a legal or beneficial interest. | May sign | Confirm funds are a non-repayable gift and no property interest is claimed. | Gift declaration, ID, bank statements and source of funds evidence. |

Who Usually Signs A UK Mortgage Deed?

The borrower or legal owner giving the charge usually signs the mortgage deed, and the signature must normally be witnessed because a deed executed by an individual requires attestation. A lender may not sign every standard mortgage deed, but will usually be named as the chargee and will execute where its form or transaction structure requires it.

When Do Extra Parties Need To Sign?

- Joint proprietors normally all sign if they are charging the registered title.

- Guarantors sign where they guarantee the borrower\'s obligations or give supporting security.

- Trustees, attorneys, personal representatives and company officers sign only where the borrower is a trust, estate, company, LLP or represented party.

- Adult occupiers may be asked to sign a consent or postponement form so the lender\'s mortgage has priority over occupation rights.

What Evidence Is Commonly Needed Before Completion?

Conveyancers commonly check identity, title, authority to sign, lender instructions, Companies House details for corporate borrowers, powers of attorney, probate documents and any required consents. For registered land, the charge must normally be completed by registration at HM Land Registry, so the signing process must support registration requirements as well as the lender\'s conditions.

Want to Generate Your own Mortgage Deed?

Docaro AI can help you write your own Mortgage Deed for use in the United Kingdom in minutes.

FAQs

The main parties are the borrower (mortgagor) and the lender (mortgagee). Other parties may include co-owners, guarantors, trustees, witnesses, conveyancers and, in some cases, occupiers giving consent.

Show All FAQs

You Might Also Be Interested In

Learn about UK mortgage deed document types, their uses, and how this dataset helps identify relevant deed formats and clauses.

United Kingdom mortgage deed checklist covering the key details needed for accurate preparation and review.