United Kingdom Mortgage Deed Preparation Information Checklist

Information Item | Why It Is Needed | Importance Level | Example Entry | Common Source |

|---|---|---|---|---|

Borrower details | ||||

Borrower full legal name | Identifies the person granting the charge. | Essential | Alexandra Mary Smith | Passport, driving licence, mortgage offer |

Borrower current residential address | Confirms identity and service contact details. | Essential | 12 Market Street, Bristol BS1 1AA | Party instructions, ID checks, mortgage offer |

Borrower date of birth | Supports identity checks and lender records. | Usually required | 14 March 1985 | Passport, driving licence, lender instructions |

Borrower email and telephone | Enables completion, signing and query handling. | Usually required | alex@example.co.uk 07123 456789 | Party instructions |

Names of all borrowers | All chargors must be correctly named. | Essential | Alex Smith and Priya Patel | Mortgage offer, title register, instructions |

Borrower capacity or role | Shows whether borrower signs personally, as trustee, company or attorney. | Essential | Individual owner and borrower | Title register, trust documents, company records |

Non-borrowing owner details | Owner may need to join in or consent to the charge. | Depends on transaction | Jordan Lee, registered proprietor but not borrower | Title register, lender instructions |

Adult occupier names and consents | Lender may require occupiers to postpone rights. | Depends on transaction | Sam Taylor signs occupier consent form | Lender instructions, occupancy questionnaire |

Company borrower registered name | Identifies corporate chargor exactly. | Essential | Green Homes Limited | Companies House register, certificate of incorporation |

Company registration number | Distinguishes the corporate borrower and supports registration. | Essential | 12345678 | Companies House register |

Company registered office | Records official corporate address. | Usually required | 1 King Street, London EC2V 8AU | Companies House register |

Execution details | ||||

Company signing authority | Confirms who can execute the deed for the company. | Essential | Two directors sign under section 44 | Board minutes, Companies Act 2006 section 44 |

Borrower details | ||||

LLP name and number | Identifies an LLP borrower accurately. | Depends on transaction | Oak Finance LLP, OC123456 | Companies House register, LLP agreement |

Trustee status and trust name | Clarifies capacity and any trust restrictions. | Depends on transaction | Trustees of the Smith Family Trust | Trust deed, title register, solicitor instructions |

Execution details | ||||

Attorney details and power of attorney | Confirms authority to sign the mortgage deed. | Depends on transaction | Pat Morgan signs under LPA dated 1 May 2024 | Power of attorney, Office of the Public Guardian record |

Lender details | ||||

Lender legal name | Identifies the chargee receiving the security. | Essential | ABC Bank plc | Mortgage offer, lender instructions |

Lender address for service | Records lender contact address on deed or register. | Usually required | PO Box 100, London EC1A 1AA | Mortgage offer, lender handbook instructions |

Lender company or registration number | Verifies lender identity where required. | Usually required | Company number 00123456 | Mortgage offer, Companies House, FCA register |

Lender reference or account number | Links deed to the lender case file. | Usually required | Mortgage account 987654321 | Mortgage offer, lender portal |

Lender approved charge form | Many lenders require their standard charge wording. | Essential | ABC Bank standard legal charge | Lender instructions, HM Land Registry approved forms |

Additional clauses | ||||

Standard mortgage conditions edition | Incorporates detailed lender conditions into the charge. | Depends on transaction | ABC Bank Mortgage Conditions 2024 | Mortgage deed, lender instructions |

Property details | ||||

Full property address | Identifies the property being charged. | Essential | Flat 2, 10 High Road, Leeds LS1 4AB | Title register, mortgage offer, contract |

Property postcode | Helps match address to title and lender records. | Essential | LS1 4AB | Title register, Royal Mail address, mortgage offer |

Property description | Clarifies whether property is house, flat, land or mixed-use. | Usually required | Leasehold second-floor flat with parking space | Title register, title plan, lease, valuation |

Tenure | Different charge and consent issues apply to freehold and leasehold. | Essential | Leasehold | Title register, lease |

Lease date, term and parties | Defines the leasehold interest being charged. | Depends on transaction | Lease dated 1 June 2005 for 125 years | Lease, leasehold title register |

Remaining lease term | Lender may require a minimum unexpired term. | Depends on transaction | 86 years unexpired | Lease, title register, lender handbook |

Landlord or freeholder details | May be needed for notice or consent to mortgage. | Depends on transaction | Central Estates Limited | Lease, management pack, title register |

Management company details | May control consents, notices and compliance certificates. | Depends on transaction | High Road RTM Company Limited | Lease, LPE1 pack, title register |

Current and intended property use | Loan and deed terms may restrict residential, buy-to-let or commercial use. | Usually required | Owner-occupied residential home | Mortgage offer, valuation, borrower instructions |

Buildings insurance details | Lender may require insured security from completion. | Usually required | Policy starts on completion for £300,000 rebuild value | Insurance schedule, mortgage offer, lender instructions |

Title information | ||||

HM Land Registry title number | Identifies the registered estate to be charged. | Essential | LN123456 | Official copy register |

Official copy register date | Confirms title information is current enough for drafting. | Usually required | Official copy dated 3 February 2026 | HM Land Registry official copies |

Registered proprietor names | Checks all owners will execute or authorise the charge. | Essential | Alexandra Smith and Priya Patel | Proprietorship register |

Class of title | Lender may require absolute title or extra safeguards. | Usually required | Title absolute | Property register |

Title plan and extent | Confirms the land included in the security. | Usually required | Land edged red on title plan LN123456 | HM Land Registry title plan |

Existing registered charges | Shows charges to redeem, postpone or rank ahead. | Essential | Charge dated 4 April 2020 in favour of XYZ Bank | Charges register, redemption statement |

Restrictions on the register | Registration may require consent, certificate or additional evidence. | Essential | No disposition without management company certificate | Proprietorship register |

Notices, cautions or adverse entries | May affect lender security or require investigation. | Usually required | Agreed notice of lease or option | Charges register, title register |

Easements and rights benefiting or burdening title | Lender may need assurance on access, services and use. | Usually required | Right of way over private road | Property register, transfer, conveyance, lease |

Restrictive and positive covenants | Covenants may affect value, use or lender requirements. | Usually required | No business use without consent | Title register, transfer, conveyance, lease |

Unregistered title deeds root of title | Needed to prove ownership and trigger first registration. | Depends on transaction | Conveyance dated 10 January 1998 | Deed packet, conveyancing file |

Registration details | ||||

Pending Land Registry applications | Pending applications can affect priority or completion timing. | Depends on transaction | Transfer application lodged before new charge | Official search, Land Registry portal |

Loan details | ||||

Purchase price or property value | Supports loan-to-value and registration context. | Usually required | £350,000 | Mortgage offer, contract, valuation |

Loan principal amount | Defines the secured advance or facility amount. | Essential | £250,000 | Mortgage offer, facility letter |

Loan currency | Confirms currency of secured obligations. | Usually required | Pounds sterling | Mortgage offer, facility agreement |

Interest rate and type | Records financial terms secured by the charge. | Usually required | Fixed 4.75% until 30 June 2031 | Mortgage offer, facility agreement |

Mortgage term | Shows duration of loan obligations. | Usually required | 25 years | Mortgage offer |

Repayment method | Clarifies repayment or interest-only obligations. | Usually required | Capital and interest repayment | Mortgage offer |

Expected completion date | Coordinates signing, funds release and registration priority. | Essential | 15 April 2026 | Contract, solicitor instructions, lender completion statement |

Advance or drawdown date | Links charge completion to loan funds release. | Usually required | Funds released on 14 April 2026 | Lender certificate of title, completion statement |

Secured obligations scope | States whether charge secures this loan only or all monies. | Essential | All monies owing to the lender | Mortgage deed, facility agreement, lender instructions |

Additional clauses | ||||

Further advances provisions | May affect priority for future lending. | Depends on transaction | Charge secures further advances by the lender | Mortgage deed, facility agreement |

Loan details | ||||

Regulated mortgage status | Determines regulatory wording and lender requirements. | Depends on transaction | FCA regulated residential mortgage contract | Mortgage offer, FCA MCOB rules, lender instructions |

Buy-to-let or consumer buy-to-let status | Affects loan terms, regulatory treatment and occupancy clauses. | Depends on transaction | Business buy-to-let mortgage | Mortgage offer, borrower declaration, lender instructions |

Redemption statement for existing mortgage | Ensures old charge can be discharged on completion. | Depends on transaction | £198,450.32 valid to 15 April 2026 | Existing lender redemption statement |

Additional clauses | ||||

Priority or deed of postponement details | Sets ranking between competing charges or interests. | Depends on transaction | Second charge postponed to ABC Bank first charge | Existing lender consent, intercreditor agreement |

Execution details | ||||

Date of mortgage deed | Establishes deed date and registration reference. | Essential | 15 April 2026 | Completion file, executed deed |

Execution method | Ensures the mortgage is validly executed as a deed. | Essential | Individual signs as deed before witness | Law of Property (Miscellaneous Provisions) Act 1989 section 1 |

Witness full name and address | Required evidence of valid individual execution. | Essential | Morgan Brown, 8 Park Lane, York YO1 2AB | Executed deed, witness instructions |

Witness independence confirmation | Reduces risk of execution challenge or lender rejection. | Usually required | Witness is not a party to the mortgage | Execution instructions, HM Land Registry practice guide 8 |

Electronic signature arrangement | Digital deeds must meet lender and Land Registry requirements. | Depends on transaction | Qualified electronic signature platform approved by lender | Lender instructions, HM Land Registry electronic signatures guidance |

Independent legal advice requirement | Often needed for guarantors, occupiers or undue influence risk. | Depends on transaction | Guarantor obtains separate solicitor certificate | Lender instructions, solicitor risk assessment |

Board approval or member resolution | Shows corporate authority to borrow and charge property. | Depends on transaction | Board minutes approving mortgage dated 10 April 2026 | Board minutes, articles, LLP agreement |

Seal use details | Needed if entity executes under seal. | Optional | Company seal affixed before two directors | Company articles, execution clause |

Registration details | ||||

Linked transfer or purchase deed details | Registration of purchase and charge may be lodged together. | Depends on transaction | TR1 dated same day as mortgage deed | Completion documents, Land Registry application |

Land Registry application form | Registers the charge against the title. | Essential | AP1 to register legal charge | HM Land Registry form AP1 |

OS1 or OS2 priority search details | Protects priority before registration of the charge. | Essential | OS1 against title LN123456 lodged 1 April 2026 | Land Registry search result |

Priority period expiry date | Application must be lodged before priority protection expires. | Essential | Priority expires 30 April 2026 | OS1 or OS2 search result |

HM Land Registry fee | Correct fee is required for registration application. | Essential | Fee under current Land Registration Fee Order | HM Land Registry fee guidance |

Evidence of discharge of old charge | Removes redeemed charge from the register. | Depends on transaction | Electronic DS1 from existing lender | Existing lender, Land Registry portal |

Restriction compliance certificate or consent | Required to satisfy title restrictions on registration. | Depends on transaction | Certificate signed by management company | Title restriction, landlord, management company |

Identity verification evidence | Land Registry may require identity evidence for parties. | Depends on transaction | ID1 for private individual borrower | HM Land Registry ID1 or ID2 guidance |

Conveyancer name and reference | Identifies applicant and contact for Land Registry requisitions. | Usually required | Smith & Co Solicitors, ref AS/1234 | AP1, solicitor file, lender instructions |

Certificate of title submission | Lender often requires it before releasing funds. | Usually required | Certificate sent two working days before completion | UK Finance Mortgage Lenders Handbook, lender portal |

Companies House charge registration details | Company-created charges usually require Companies House registration. | Depends on transaction | MR01 to be filed within 21 days | Companies Act 2006 Part 25, Companies House guidance |

Additional clauses | ||||

Borrower covenant to pay | Creates core promise to repay secured sums. | Essential | Borrower covenants to pay all secured liabilities | Mortgage deed, lender standard conditions |

Legal charge wording | Creates the security interest over the property. | Essential | Borrower charges the property by way of legal mortgage | Law of Property Act 1925, Land Registration Act 2002 |

Repair and maintenance obligations | Protects value of lender security. | Usually required | Borrower must keep property in good repair | Lender standard mortgage conditions |

Insurance covenant | Protects lender if property is damaged. | Usually required | Borrower must insure with reputable insurer | Mortgage offer, lender standard conditions |

Letting or occupation restrictions | Prevents unauthorised tenancies affecting security. | Depends on transaction | No letting without lender consent | Mortgage offer, lender conditions |

Leasehold compliance covenant | Ensures borrower complies with lease to protect the charged leasehold title. | Depends on transaction | Borrower must pay rent and service charge | Lease, lender mortgage conditions |

Restriction on further charges | Prevents borrower creating competing security without consent. | Usually required | No second charge without lender written consent | Mortgage deed, facility agreement |

Events of default | Defines when lender enforcement rights may arise. | Usually required | Missed payment, insolvency or breach of covenant | Mortgage conditions, facility agreement |

Lender enforcement and power of sale wording | Sets lender remedies if borrower defaults. | Usually required | Statutory and contractual powers apply on default | Law of Property Act 1925 sections 101 and 103 |

Receiver appointment powers | Allows lender to appoint receiver where applicable. | Depends on transaction | Lender may appoint receiver after default | Law of Property Act 1925, mortgage conditions |

Guarantor details and guarantee wording | Adds personal or corporate support for secured obligations. | Depends on transaction | Director guarantees company mortgage obligations | Facility agreement, lender instructions |

Registration details | ||||

Application for lender restriction | Some lenders require a register restriction to control future dispositions. | Depends on transaction | RX1 restriction requiring lender consent | Mortgage deed, Land Registry form RX1, lender instructions |

Notice of charge requirement | Lease may require notice to landlord after mortgage. | Depends on transaction | Notice of charge served with £75 registration fee | Lease, landlord requirements, management pack |

SDLT or land transaction return status | Purchase registration may need tax return certificate before charge registration. | Depends on transaction | SDLT5 certificate available for purchase registration | HMRC SDLT return, conveyancer file |

Welsh LTT return status | Welsh purchase registration may need LTT certificate. | Depends on transaction | LTT certificate issued by WRA | Welsh Revenue Authority return |

Property details | ||||

Jurisdiction of property | Scotland uses standard securities, not English mortgage deeds. | Essential | England and Wales | Property address, title register, Registers of Scotland search |

Northern Ireland title and registration status | Northern Ireland has separate land registration requirements. | Depends on transaction | Folio AN12345, County Antrim | Land Registry Northern Ireland records |

Welsh property address or bilingual requirements | May help match Welsh title and local authority records. | Optional | Tŷ Gwyn, Aberystwyth SY23 1AA | Title register, local authority records, borrower instructions |

Title information | ||||

Home rights or matrimonial interests | Registered home rights may affect lender priority or require consent. | Depends on transaction | Class F land charge or home rights notice | Title register, land charges search, Family Law Act 1996 |

Registration details | ||||

Bankruptcy search result | Protects lender against insolvency entries affecting borrower title. | Usually required | K16 clear against borrower full name | Land Charges Department search result |

Title information | ||||

Local land charges search issues | Local entries may affect property value or lender conditions. | Usually required | Tree preservation order or planning enforcement notice | Local authority search, HM Land Registry LLC service |

Property details | ||||

Planning and building regulation issues | Unauthorised works may affect lender security or require indemnity. | Depends on transaction | Loft conversion lacks completion certificate | Local search, seller replies, planning portal |

Environmental or flood risk issues | May affect valuation, insurance and lender approval. | Depends on transaction | High surface water flood risk | Environmental search, Environment Agency flood map |

Title information | ||||

Chancel repair liability entry or risk | Potential liability may affect lender or insurance requirements. | Depends on transaction | No registered notice indemnity policy obtained | Title register, chancel search, conveyancer file |

Additional clauses | ||||

Title indemnity policy details | May satisfy lender where title defect cannot be resolved quickly. | Depends on transaction | Lack of building regulations indemnity for £350,000 | Conveyancer file, insurer policy, lender approval |

Property details | ||||

Shared ownership lease and staircasing terms | Mortgage must fit lease, rent and housing provider consent rules. | Depends on transaction | 45% share with housing association consent required | Shared ownership lease, housing provider instructions |

Title information | ||||

Help to Buy or equity loan charge details | Existing equity loan may require consent or redemption. | Depends on transaction | Homes England equity charge to be postponed | Title register, equity loan administrator |

Right to Buy discount or resale restriction | Restrictions or repayment liabilities may affect lender security. | Depends on transaction | Right to Buy charge within discount repayment period | Title register, transfer, Housing Act 1985 |

Property details | ||||

New build warranty details | Lender may require acceptable structural warranty. | Depends on transaction | NHBC Buildmark policy number 123456 | Developer pack, warranty provider, lender handbook |

New build completion or building control certificate | Confirms property is complete or acceptable for mortgage completion. | Depends on transaction | Final building control certificate dated 8 April 2026 | Developer, building control, warranty provider |

Registration details | ||||

Landlord certificate of compliance | May be required to satisfy leasehold title restriction. | Depends on transaction | Certificate under restriction in favour of freeholder | Title register, landlord, management company |

Additional clauses | ||||

First lender consent to second charge | First charge terms may prohibit later charges without consent. | Depends on transaction | Written consent from ABC Bank to second legal charge | Existing mortgage conditions, first lender consent letter |

Loan details | ||||

First or second charge ranking | Determines priority and drafting of postponement clauses. | Essential | First legal charge | Title register, lender instructions |

Additional clauses | ||||

All-monies or specific-loan charge type | Defines what debts are secured by the mortgage. | Essential | Specific advance under offer dated 1 April 2026 | Mortgage offer, facility agreement, lender instructions |

Title information | ||||

Multiple title numbers included | Ensures every parcel or leasehold interest is charged and registered. | Depends on transaction | LN123456 and LN654321 | Title registers, title plans, lender valuation |

Separate parking or storage title | Ancillary titles may need to be included in the charge. | Depends on transaction | Parking space title LN999999 included | Title register, lease, sale contract |

Filed deeds referred to on the register | Contains detailed covenants, rights or restrictions not fully set out on register. | Usually required | Transfer dated 2 February 1990 contains covenants | HM Land Registry filed deeds |

Property details | ||||

Boundary or extent discrepancies | Discrepancies may affect valuation and lender security. | Depends on transaction | Garage outside red edging on title plan | Title plan, survey, valuation, inspection |

Borrower details | ||||

Borrower address for legal notices | Specifies where formal notices may be served. | Usually required | The charged property and borrower email address | Mortgage deed, lender instructions, borrower instructions |

Lender details | ||||

Lender address for legal notices | Specifies where borrower or third parties serve formal notices. | Usually required | Security Department, ABC Bank plc, London | Mortgage deed, lender conditions |

Additional clauses | ||||

Data protection and credit reference wording | Lender may require borrower acknowledgements for account administration. | Optional | Borrower acknowledges lender privacy notice | Mortgage offer, lender privacy notice |

Loan details | ||||

Payment mandate or direct debit details | Needed for loan servicing but usually not part of the deed itself. | Optional | Direct debit from account ending 1234 | Lender completion pack, borrower instructions |

Mortgage offer expiry date | Completion must occur while offer remains valid. | Essential | Offer expires 30 June 2026 | Mortgage offer |

Special conditions in mortgage offer | Conditions may need satisfaction before deed completion. | Essential | Retention pending roof repair confirmation | Mortgage offer, valuation report, lender instructions |

Retention amount and conditions | Affects funds available on completion and security terms. | Depends on transaction | £5,000 retained until damp works completed | Mortgage offer, valuation, lender instructions |

Facility agreement or loan agreement reference | Links the deed to the underlying loan terms. | Depends on transaction | Facility letter dated 1 April 2026 | Facility agreement, mortgage offer |

Additional clauses | ||||

Other security documents | Ensures mortgage deed fits wider security package. | Depends on transaction | Debenture, guarantee and rent deposit charge | Facility agreement, lender solicitor instructions |

Property details | ||||

Valuation report reference | Confirms property accepted as security by lender. | Usually required | Valuation dated 20 March 2026 at £350,000 | Lender valuation, mortgage offer |

Registration details | ||||

Solicitor undertakings required by lender | Lender may rely on undertakings for completion and registration. | Usually required | Undertaking to register charge promptly after completion | Lender instructions, UK Finance Handbook |

Requisition contact details | Allows quick response to Land Registry registration queries. | Usually required | postcompletion@smithsolicitors.co.uk | AP1, conveyancer details |

Order of registration applications | Transfer, discharge and charge must be registered in correct order. | Essential | Register transfer, remove old charge, register new charge | Completion statement, AP1, title register |

Title information | ||||

Co-ownership and Form A restriction status | Shows whether beneficial ownership restriction affects dispositions. | Usually required | Form A restriction registered | Proprietorship register, trust deed, Land Registry guidance |

Borrower details | ||||

Beneficial owner or trust beneficiary consent | May be needed where legal owners hold on trust. | Depends on transaction | Adult beneficiary consents to mortgage | Trust deed, lender instructions, solicitor advice |

Overseas borrower service address | Provides practical address for notices and lender contact. | Depends on transaction | UK service address care of solicitor | Borrower instructions, lender requirements |

Overseas entity ID | Overseas entities may need registration before property dispositions. | Depends on transaction | OE123456 | Register of Overseas Entities, Companies House |

Sanctions screening result | Lenders and professionals must avoid prohibited dealings. | Usually required | No match on UK sanctions list | UK sanctions list, compliance checks |

Source of funds for borrower contribution | Required for AML checks and lender completion requirements. | Usually required | Savings from salary held for 3 years | Bank statements, conveyancer AML file |

Source of wealth evidence | Supports enhanced due diligence where risk is higher. | Depends on transaction | Business sale proceeds documented by completion statement | AML file, bank statements, sale documents |

Loan details | ||||

Gifted deposit details and donor declaration | Lender may require donor to confirm gift is not repayable or secured. | Depends on transaction | £25,000 gift from parent with no interest retained | Donor declaration, bank statements, lender instructions |

Borrower details | ||||

Donor occupation or interest in property | Donor may need to postpone any interest to lender. | Depends on transaction | Parent donor will not live at property | Gifted deposit letter, lender instructions |

Spouse or civil partner consent where relevant | May protect lender against home rights or occupation claims. | Depends on transaction | Civil partner signs occupier consent | Occupancy questionnaire, lender instructions, Family Law Act 1996 |

Known insolvency or IVA status | Insolvency may restrict ability to grant valid security. | Depends on transaction | No bankruptcy order or IVA disclosed | Borrower declaration, bankruptcy search, Insolvency Register |

Execution details | ||||

Borrower capacity to execute deed | A deed signed without capacity may be challenged. | Depends on transaction | No capacity concerns identified | Client meeting notes, medical evidence, Mental Capacity Act 2005 |

Language or interpreter requirements | Helps ensure borrower understands deed before signing. | Depends on transaction | Independent interpreter required for signing meeting | Borrower instructions, solicitor assessment |

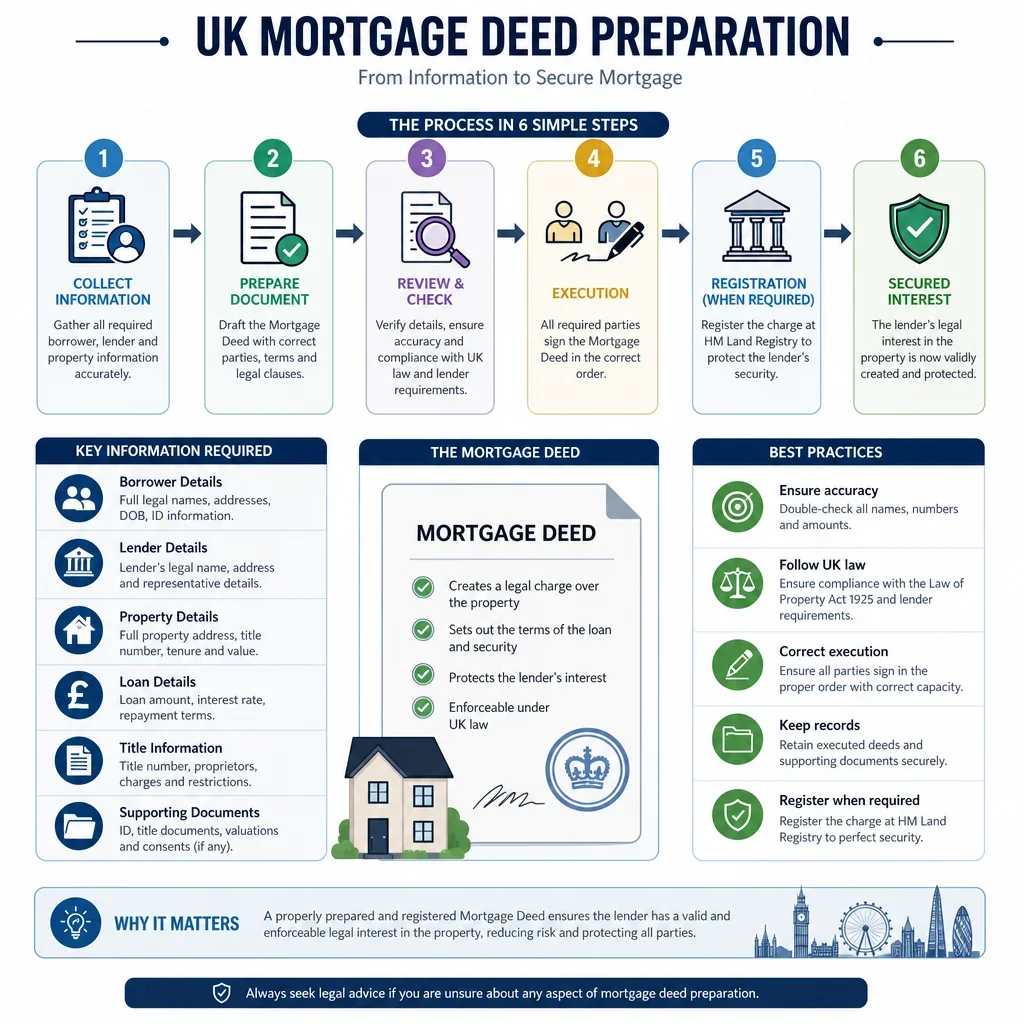

What Information Is Needed To Prepare A UK Mortgage Deed?

A mortgage deed normally depends on accurate borrower identity details, lender details, property title information, loan information, execution arrangements and Land Registry registration requirements. For registered land in England and Wales, the deed must identify the charged property clearly, usually by title number and address, and be capable of registration at HM Land Registry.

Why Do Title Numbers, Existing Charges And Restrictions Matter?

Title information is critical because the new mortgage must be registered against the correct registered estate and must comply with any existing restrictions, priorities or consent requirements shown on the register. A prior lender, management company, landlord or shared ownership provider may need to consent before the new charge can be completed or registered.

What Execution Details Should Borrowers Check Before Signing?

A mortgage deed must be executed as a deed. For an individual borrower, this usually means signing in the presence of an independent witness who also signs and gives their details. Companies, LLPs and attorneys have different execution rules, so capacity and authority should be checked before signing.

What Registration Details Are Usually Required After Completion?

The application to register a charge typically needs the correct title number, lender identity, mortgage deed or approved lender charge, priority search details, any required certificates or consents, and the appropriate HM Land Registry fee. Delays or errors can risk loss of priority or a requisition from HM Land Registry.

FAQs

You Might Also Be Interested In