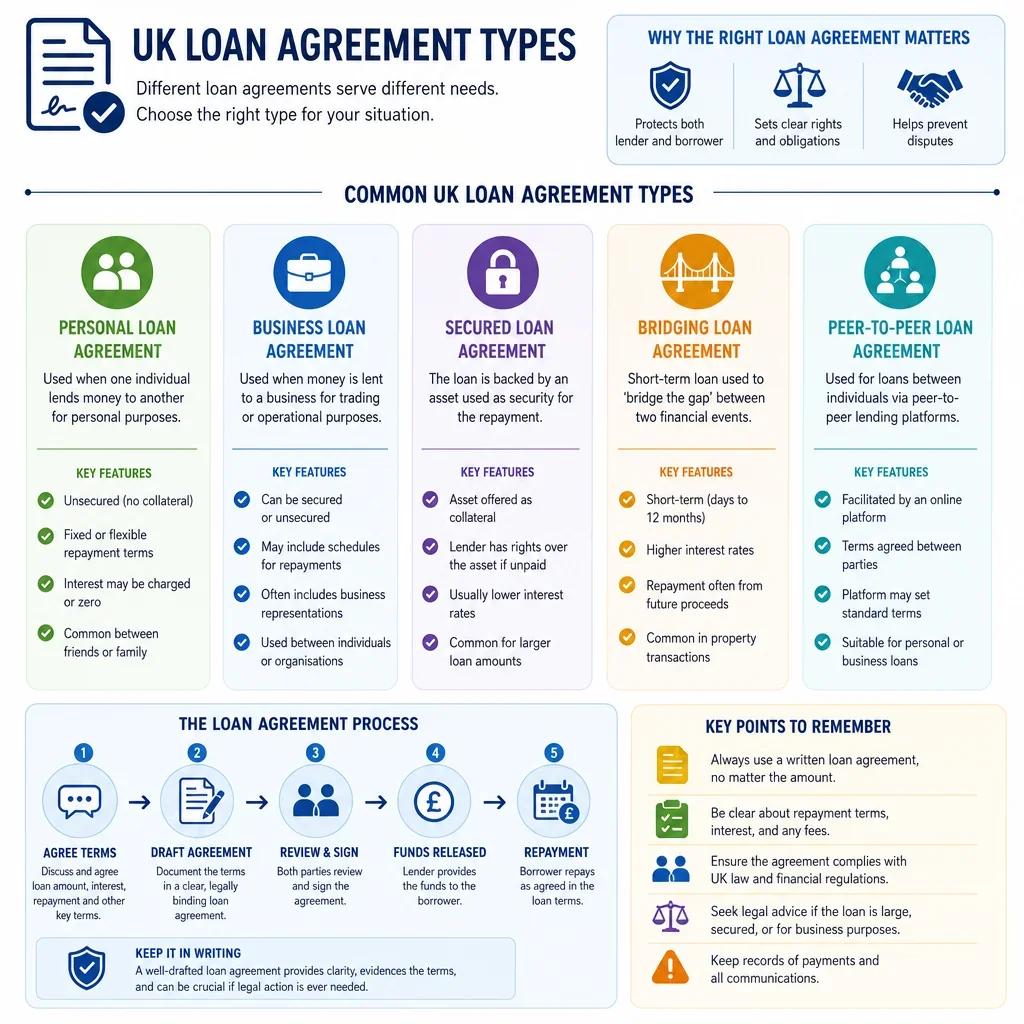

UK Loan Agreement Types

Loan Context | Typical Use Case | Security Position | Complexity Level | Key Considerations |

|---|---|---|---|---|

Family Loan Agreement | ||||

Personal | Money lent between relatives, often for a house deposit, education costs or short-term support. | Unsecured | Low | Record whether the money is a loan or gift, repayment date, interest, default and evidence of transfers. |

Friends Loan Agreement | ||||

Personal | Informal lending between friends where both parties want written repayment terms. | Unsecured | Low | Define amount, repayment timetable, interest, missed payment consequences and whether early repayment is allowed. |

Personal Unsecured Loan Agreement | ||||

Personal | A private personal loan with no collateral supporting repayment. | Unsecured | Low | Check whether consumer credit regulation applies, especially if lending is by way of business. |

Personal Secured Loan Agreement | ||||

Personal, Property | A personal loan backed by specific assets, commonly property or valuable goods. | Secured | Medium | Security must be properly created, documented and registered where required regulated credit rules may apply. |

On-Demand Loan Agreement | ||||

Personal, Business, Director or shareholder, Intra-group | Loan repayable whenever the lender demands repayment, often used for flexible short-term funding. | Either | Low | Demand process, notice period, interest until repayment and practical cash-flow impact on the borrower. |

Fixed-Term Loan Agreement | ||||

Personal, Business, Property, Director or shareholder, Intra-group | Loan with a set maturity date and defined repayment obligations. | Either | Low | State maturity date, repayment schedule, interest periods, prepayment rights and default triggers. |

Instalment Loan Agreement | ||||

Personal, Business | Borrower repays capital and interest through regular scheduled payments. | Either | Low | Include payment dates, amortisation, allocation of payments, late fees and early settlement rights. |

Bullet Repayment Loan Agreement | ||||

Business, Property, Director or shareholder, Intra-group | Interest is paid during the term and principal is repaid in one amount at maturity. | Either | Medium | Assess refinancing risk, maturity repayment source, interest payments and default if the bullet is missed. |

Interest-Free Loan Agreement | ||||

Personal, Business, Director or shareholder, Intra-group | Loan where the parties agree no interest is payable. | Either | Low | Consider tax, benefit-in-kind, transfer pricing and whether no-interest terms create accounting issues. |

Business Loan Agreement | ||||

Business | General funding for a company, LLP, partnership or sole trader. | Either | Medium | Include purpose, repayment, representations, covenants, information rights, events of default and security if required. |

SME Loan Agreement | ||||

Business | Funding for a small or medium-sized UK business for working capital or growth. | Either | Medium | Balance lender protections with practical covenants, reporting obligations and business cash-flow needs. |

Working Capital Loan Agreement | ||||

Business | Short-term funding to cover payroll, stock, suppliers or seasonal cash-flow gaps. | Either | Medium | Set drawdown availability, repayment source, working capital reporting and limits on further debt. |

Revolving Credit Facility Agreement | ||||

Business, Intra-group | Facility allowing repeated drawdowns and repayments up to a committed limit. | Either | High | Needs availability mechanics, utilisation requests, commitment fees, cancellation, covenants and default controls. |

Overdraft Facility Letter | ||||

Business, Personal | Bank account facility permitting borrowing up to an agreed overdraft limit. | Either | Medium | Usually repayable on demand document limit, interest, review dates, fees and cancellation rights. |

Asset Finance Loan Agreement | ||||

Business | Funding used to buy business equipment, vehicles or machinery. | Secured | Medium | Identify asset, ownership, maintenance, insurance, repossession rights and whether hire purchase is more appropriate. |

Equipment Loan Agreement | ||||

Business | Business loan to fund purchase or refinancing of specific equipment. | Secured | Medium | Asset description, title, maintenance, insurance, depreciation, security enforcement and sale restrictions. |

Invoice Finance Facility Agreement | ||||

Business | Funding advanced against unpaid customer invoices or receivables. | Secured | High | Receivables eligibility, assignment, concentration limits, debtor notices, recourse and verification rights. |

Stock Finance Agreement | ||||

Business | Funding secured against inventory or stock held by a trading business. | Secured | High | Valuation, monitoring, insurance, retention of title claims, stock rotation and enforcement practicality. |

Trade Finance Loan Agreement | ||||

Business | Funding imports, exports, purchase orders or supply-chain transactions. | Either | High | Documents, shipping risk, FX exposure, supplier payments, receivables assignment and sanctions compliance. |

Acquisition Finance Loan Agreement | ||||

Business | Funding a company or business acquisition. | Secured | High | Conditions precedent, acquisition documents, leverage, financial assistance restrictions, security and post-completion covenants. |

Management Buyout Loan Agreement | ||||

Business, Director or shareholder | Finance provided to a management team or acquisition vehicle to buy a business. | Secured | High | Equity contribution, subordination, acquisition documents, conflicts, warranties and target group security. |

Project Finance Loan Agreement | ||||

Business, Property | Funding a ring-fenced project where repayment depends mainly on project cash flows. | Secured | High | Due diligence, step-in rights, construction risk, revenue contracts, reserve accounts and security package. |

Syndicated Loan Agreement | ||||

Business, Property | Large loan provided by multiple lenders under one coordinated facility agreement. | Either | High | Agency provisions, lender voting, transfer rights, pro rata sharing, security trustee and amendment mechanics. |

Bilateral Facility Agreement | ||||

Business, Property | Business loan facility between one lender and one borrower or borrower group. | Either | Medium | Facility size, conditions precedent, covenants, drawdown mechanics, fees, defaults and security. |

Mezzanine Loan Agreement | ||||

Business, Property | Higher-risk junior debt sitting behind senior debt, often in acquisitions or property deals. | Secured | High | Intercreditor terms, payment blockage, second-ranking security, equity warrants and higher pricing. |

Subordinated Loan Agreement | ||||

Business, Director or shareholder, Intra-group | Debt agreed to rank behind senior creditors on insolvency or enforcement. | Either | High | Subordination wording, payment restrictions, insolvency ranking, turnover provisions and intercreditor consistency. |

Convertible Loan Agreement | ||||

Business, Director or shareholder | Debt that may convert into shares, commonly used for startup or growth investment. | Unsecured | High | Conversion trigger, valuation cap, discount, qualifying round, shareholder approvals and Companies Act allotment rules. |

Convertible Loan Note Instrument | ||||

Business, Director or shareholder | Instrument creating loan notes that can convert into shares under defined conditions. | Unsecured | High | Investor rights, transferability, conversion mechanics, interest, redemption, pre-emption and securities law issues. |

Loan Note Instrument | ||||

Business, Director or shareholder, Intra-group | Company issues debt securities to one or more noteholders. | Either | High | Redemption, transferability, noteholder meetings, listing, financial promotion and withholding tax. |

Director Loan Agreement | ||||

Director or shareholder, Business | Loan between a company and one of its directors, in either direction. | Either | Medium | Check shareholder approval, conflicts, tax on overdrawn loan accounts and board authorisation. |

Director-to-Company Loan Agreement | ||||

Director or shareholder, Business | Director lends personal funds to support company cash flow or expansion. | Either | Low | Record interest, repayment priority, subordination to bank debt and board approval of connected-party terms. |

Company-to-Director Loan Agreement | ||||

Director or shareholder, Business | Company lends money to a director or connected person. | Either | Medium | May require member approval consider corporation tax charge on close company loans and benefit-in-kind rules. |

Shareholder Loan Agreement | ||||

Director or shareholder, Business | Shareholder lends to, or borrows from, a company outside ordinary share capital. | Either | Medium | Address ranking, repayment, interest, conflicts, minority protections and subordination to external lenders. |

Shareholder-to-Company Loan Agreement | ||||

Director or shareholder, Business | Shareholder injects repayable funds into the company instead of buying more shares. | Either | Low | Clarify whether funds are debt or equity, repayment priority, interest and treatment on sale or insolvency. |

Company-to-Shareholder Loan Agreement | ||||

Director or shareholder, Business | Company advances money to a shareholder, often in a close company context. | Either | Medium | Check distributable profits, close company tax rules, connected persons and whether the payment is a disguised distribution. |

Founder Loan Agreement | ||||

Director or shareholder, Business | Startup founder lends money to the company before external investment or revenue. | Unsecured | Low | Keep terms investor-friendly address repayment deferral, conversion, interest and conflicts with future funding rounds. |

Employee Loan Agreement | ||||

Personal, Business | Employer lends to an employee for travel, relocation, training or hardship support. | Unsecured | Medium | Payroll deductions need written authority consider taxable cheap loan benefit and termination repayment. |

Relocation Loan Agreement | ||||

Personal, Business | Employer-funded loan to help an employee move home for work. | Unsecured | Low | Address repayment if employment ends, payroll deduction consent and tax treatment of employment-related loans. |

Training Cost Loan Agreement | ||||

Personal, Business | Employer funds training costs to be repaid if conditions are not met. | Unsecured | Medium | Avoid penalty-style repayment include sliding scale, deduction consent and employment law fairness. |

Intercompany Loan Agreement | ||||

Intra-group, Business | Loan between companies in the same corporate group. | Either | Medium | Arm's-length terms, transfer pricing, corporate benefit, withholding tax and board approvals. |

Parent-to-Subsidiary Loan Agreement | ||||

Intra-group, Business | Parent company funds a subsidiary for operations, investment or restructuring. | Either | Medium | Document commercial purpose, repayment capacity, transfer pricing, thin capitalisation and local law constraints. |

Subsidiary-to-Parent Loan Agreement | ||||

Intra-group, Business | Subsidiary lends surplus cash to its parent company or treasury vehicle. | Either | Medium | Check corporate benefit, distributable reserves concerns, directors' duties, transfer pricing and insolvency risk. |

Group Cash Pooling Loan Agreement | ||||

Intra-group, Business | Group companies centralise cash balances with a treasury company or lead bank. | Either | High | Set pooling mechanics, set-off, interest allocation, transfer pricing, insolvency separation and bank documentation. |

Group Treasury Loan Agreement | ||||

Intra-group, Business | Central treasury company lends to group entities under standardised intra-group terms. | Either | High | Benchmark pricing, FX risk, withholding tax, cross-border enforcement and local corporate approvals. |

Bridge Loan Agreement | ||||

Property, Business, Personal | Short-term finance pending sale, refinance, investment round or completion of another transaction. | Secured | High | Exit route, default interest, valuation, security, fees and regulated mortgage activity if secured on a home. |

Property Development Finance Agreement | ||||

Property, Business | Loan funding land purchase, construction or refurbishment for a development project. | Secured | High | Drawdowns tied to monitoring surveyor reports, planning, cost overruns, pre-sales, warranties and exit finance. |

Commercial Property Loan Agreement | ||||

Property, Business | Loan to buy or refinance offices, shops, warehouses or other commercial premises. | Secured | High | Valuation, title, leases, environmental issues, loan-to-value covenant, insurance and security registration. |

Buy-To-Let Loan Agreement | ||||

Property, Personal, Business | Loan secured on a residential investment property let to tenants. | Secured | High | Check whether consumer buy-to-let rules apply, rental cover, tenancy terms, licensing and mortgage conditions. |

Second Charge Loan Agreement | ||||

Property, Personal, Business | Loan secured by a second-ranking charge over property behind a first mortgage lender. | Secured | High | Needs first lender consent, priority arrangements, Land Registry registration and possible FCA mortgage regulation. |

Legal Charge Secured Loan Agreement | ||||

Property, Business, Personal | Loan agreement supported by a legal charge over registered or unregistered land. | Secured | High | Charge must be correctly executed, registered at Land Registry and, for companies, often at Companies House. |

Debenture Secured Loan Agreement | ||||

Business | Business loan secured by a company debenture over multiple asset classes. | Secured | High | Register company charges within 21 days define fixed and floating charge assets and enforcement rights. |

Share Charge Loan Agreement | ||||

Business, Director or shareholder | Loan secured over shares held by a borrower or obligor. | Secured | High | Check company articles, share certificates, blank transfers, control rights, financial assistance and perfection steps. |

Personal Guarantee Supported Loan Agreement | ||||

Business, Property, Director or shareholder | Business or property loan where an individual guarantees repayment. | Either | Medium | Guarantor should understand liability, independent advice expectations, demand process and limitation periods. |

Cross-Guarantee Group Loan Agreement | ||||

Business, Intra-group | Group companies guarantee each other's liabilities under a group facility. | Either | High | Corporate benefit, financial assistance, guarantee limitations, board approvals and insolvency clawback risk. |

Refinancing Loan Agreement | ||||

Business, Property, Personal, Intra-group | New loan used to repay and replace existing debt. | Either | Medium | Coordinate repayment, release of existing security, new security, break costs and priority arrangements. |

Debt Consolidation Loan Agreement | ||||

Personal, Business | One loan used to repay several existing debts and simplify repayment. | Either | Medium | Compare total cost, term extension, security risk, early repayment fees and consumer credit protections. |

Promissory Note | ||||

Personal, Business | Short written promise to pay a specified sum, often simpler than a full loan agreement. | Unsecured | Low | May be negotiable include clear parties, amount, due date, interest and whether transfer is permitted. |

Term Sheet For Loan Facility | ||||

Business, Property, Intra-group, Director or shareholder | Non-binding heads of terms used before a detailed loan agreement is prepared. | Either | Medium | Mark binding and non-binding terms, exclusivity, fees, confidentiality and conditions to lending. |

Facility Letter | ||||

Business, Property, Personal | Short-form lender letter setting out terms of a loan or credit facility. | Either | Medium | Ensure acceptance, conditions, repayment, pricing, security and incorporated standard terms are clear. |

Loan Amendment And Restatement Agreement | ||||

Business, Property, Intra-group, Director or shareholder | Existing loan is amended and restated into an updated full agreement. | Either | High | Preserve security, guarantees and priority obtain consents and avoid unintended novation or release. |

Loan Variation Agreement | ||||

Personal, Business, Property, Director or shareholder, Intra-group | Parties change existing loan terms such as maturity, interest or repayment dates. | Either | Medium | Check guarantor consent, secured creditor priority, regulatory re-documentation and board or member approvals. |

Forbearance Agreement | ||||

Business, Property, Personal | Lender agrees temporarily not to enforce after default, subject to conditions. | Either | High | Reserve rights, acknowledge defaults, set cure plan, require waivers and preserve security and guarantees. |

Loan Assignment Agreement | ||||

Business, Property, Personal, Intra-group | Existing lender transfers loan rights to a new lender or group company. | Either | Medium | Notice to debtor, transfer restrictions, security transfer, data protection and whether novation is needed. |

Loan Novation Agreement | ||||

Business, Property, Personal, Intra-group | Original loan party is replaced by a new party with consent of all relevant parties. | Either | Medium | May release old obligations preserve guarantees, security, priority and regulatory status by express drafting. |

Peer-To-Peer Lending Agreement | ||||

Personal, Business | Loans arranged through an online platform between investors and borrowers. | Either | High | Platform authorisation, client money, consumer credit status, disclosure and assignment mechanics are important. |

Crowdfunding Loan Agreement | ||||

Business, Personal | Multiple lenders advance funds to a borrower through a crowdfunding structure. | Either | High | Regulatory permissions, investor communications, platform terms, lender voting and enforcement coordination. |

Partnership Loan Agreement | ||||

Business | Loan to or from a partnership, LLP or partner in a trading structure. | Either | Medium | Check partner authority, liability, partnership deed, profit drawings and security over partnership assets. |

LLP Member Loan Agreement | ||||

Business, Director or shareholder | LLP member lends money to, or borrows from, the LLP. | Either | Medium | Review LLP agreement, member authority, capital accounts, tax treatment and insolvency repayment risk. |

Charity Loan Agreement | ||||

Business, Property | Loan to or by a charity for operations, property or social investment. | Either | High | Trustee powers, charity benefit, conflicts, secured borrowing, disposal restrictions and Charity Commission guidance. |

Loan To Trustees Agreement | ||||

Personal, Property, Business | Loan made to trustees for trust property, investment or beneficiary funding purposes. | Either | High | Confirm trustee borrowing powers, liability limits, trust assets, indemnities and beneficiary interests. |

Hire Purchase Agreement | ||||

Personal, Business | Goods are hired with an option or obligation to purchase after instalments are paid. | Secured | High | Consumer hire purchase may be regulated ownership, termination, repossession and statutory notices matter. |

Conditional Sale Agreement | ||||

Personal, Business | Buyer pays by instalments and title passes only when conditions are met. | Secured | High | Consumer credit rules, title retention, repossession rights, default notices and total price disclosures. |

Sale And Leaseback Financing Agreement | ||||

Business, Property | Owner sells an asset and leases it back to release capital while retaining use. | Secured | High | Sale validity, lease terms, accounting, tax, registration, asset control and recharacterisation risk. |

Vendor Loan Agreement | ||||

Business, Property | Seller finances part of the purchase price owed by the buyer. | Either | Medium | Align with sale agreement, retention of title or security, repayment source and buyer default remedies. |

Deferred Consideration Loan Agreement | ||||

Business, Property | Unpaid sale price is structured as a repayable debt after completion. | Either | Medium | Coordinate with warranties, set-off rights, completion accounts, security and acceleration on buyer default. |

Earn-Out Loan Agreement | ||||

Business | Contingent acquisition payment is documented as debt once earn-out conditions are met. | Unsecured | High | Define earn-out trigger, accounts basis, dispute process, set-off, tax and repayment timing. |

Start-Up Loan Agreement | ||||

Business, Director or shareholder | Early-stage company borrows money before revenue, investment or bank finance is available. | Unsecured | Medium | Cash runway, founder guarantees, conversion rights, repayment deferral and compatibility with future investment. |

Social Enterprise Loan Agreement | ||||

Business | Loan funding a community interest company, charity trading arm or social enterprise. | Either | Medium | Mission restrictions, asset locks, grant conditions, social impact covenants and board approvals. |

Community Interest Company Loan Agreement | ||||

Business | Loan to or from a CIC for community-purpose activities or asset funding. | Either | Medium | Check asset lock, community benefit, dividend and interest caps, security and regulator requirements. |

Agricultural Loan Agreement | ||||

Business, Property | Finance for farms, rural land, livestock, machinery or seasonal agricultural cash flow. | Either | Medium | Seasonality, land title, tenancies, subsidies, livestock security, equipment and environmental compliance. |

Professional Practice Loan Agreement | ||||

Business | Funding for law, accountancy, dental, medical or other professional practices. | Either | Medium | Partnership terms, professional regulation, drawings, goodwill valuation, partner guarantees and client account separation. |

Franchise Finance Loan Agreement | ||||

Business | Loan to buy, launch or expand a franchise business. | Either | Medium | Review franchise agreement, franchisor consent, step-in rights, territory, fees and business plan assumptions. |

Intellectual Property Secured Loan Agreement | ||||

Business | Loan secured against patents, trade marks, copyright or other intellectual property assets. | Secured | High | Value IP, identify ownership, register security where relevant, preserve licences and manage enforcement risk. |

Which UK Loan Agreement Type Should You Use?

The right form depends mainly on who is lending, why the money is being borrowed, and whether repayment is backed by security. Simple family, friend, employee, director or shareholder loans are often documented with a short unsecured agreement, but property finance, business acquisition finance, intra-group lending and loans supported by debentures or legal charges usually need more detailed drafting.

When Is A Secured Loan Agreement Needed In The UK?

A loan is usually documented as secured where the lender expects recourse to specific assets if the borrower defaults, such as land, shares, receivables, equipment or wider company assets. Company security is commonly registered at Companies House under the Companies Act 2006, Part 25, and land security will normally involve Land Registry requirements.

Which Loan Agreements Need Extra Regulatory Care?

Some lending arrangements may be regulated consumer credit or mortgage activity, especially personal loans, hire purchase, conditional sale, second charge lending and bridging or development finance involving individuals. The Consumer Credit Act 1974 and FCA perimeter rules can affect form, wording, disclosures, enforcement and whether the lender needs authorisation.

What Are The Most Important Drafting Points?

- Repayment mechanics: on-demand, fixed-term, instalment, bullet, revolving and bridge loans all need different repayment wording.

- Interest: interest rate, default interest, compounding, withholding tax and whether interest is paid or rolled up should be clear.

- Security: secured business and property loans should identify the collateral and any separate debenture, legal charge, share charge or assignment.

- Company approvals: director, shareholder and intra-group loans may need board minutes, shareholder approvals, distributable profits analysis or conflicts management.

- Default rights: business and property loans often need events of default, acceleration, financial covenants and information undertakings.

FAQs

You Might Also Be Interested In