Loan Repayment Structures In The United Kingdom

Repayment Category | How It Works | Common Term Length | Borrower Flexibility | Drafting Considerations |

|---|---|---|---|---|

Bullet repayment at maturity | ||||

Single repayment | Borrower pays interest during the term and repays all principal on the final maturity date. | Short term Medium term | Medium | Define maturity date, interest payment dates, final repayment amount and any refinancing or extension rights. |

Interest-free bullet repayment | ||||

Single repayment | Borrower repays the original principal in one amount on the due date with no contractual interest. | Short term Flexible | Medium | State that no interest accrues, but address default interest, tax, connected-party issues and late payment consequences. |

Principal and accrued interest at maturity | ||||

Single repayment | No periodic payments are made all principal and accrued interest are paid together at maturity. | Short term Medium term | High | Specify compounding, day-count convention, interest period and whether unpaid interest is capitalised. |

Discounted advance with face-value repayment | ||||

Single repayment | Lender advances less than the face amount and borrower repays the full face amount at maturity. | Short term | Medium | Make the discount, effective cost, repayment amount and any regulated credit implications clear. |

Equal principal instalments | ||||

Instalments | Borrower repays the same amount of principal each period, plus interest on the reducing balance. | Medium term Long term | Low | Attach an amortisation schedule and state how interest is recalculated after prepayment or default. |

Equal total payment amortisation | ||||

Instalments | Borrower pays a fixed total amount each period, with interest reducing and principal increasing over time. | Medium term Long term | Low | Include repayment formula, interest rate assumptions, reset process and consequences of rate changes. |

Fixed monthly instalments | ||||

Instalments | Borrower pays a fixed amount every month until the loan is repaid or the term ends. | Medium term Long term | Low | State payment date, amount, allocation between interest and principal, and treatment of bank holidays. |

Quarterly instalments | ||||

Instalments | Borrower repays principal and interest every quarter, usually on fixed quarter dates. | Medium term Long term | Medium | Define quarter dates, business day adjustment, interest periods and payment allocation. |

Weekly instalments | ||||

Instalments | Borrower makes weekly repayments, often for short-term personal or small business borrowing. | Short term | Low | Specify recurring due day, failed payment fees, affordability checks and any consumer credit disclosures. |

Fortnightly instalments | ||||

Instalments | Borrower pays a fixed or scheduled amount every two weeks. | Short term Medium term | Low | Avoid ambiguity by defining payment intervals, first payment date and final balancing payment. |

Annual instalments | ||||

Instalments | Borrower pays principal and interest once each year during the loan term. | Long term | Medium | State annual payment date, interest accrual between payments and default position if payment date is missed. |

Stepped-up repayments | ||||

Instalments | Repayments start lower and increase at agreed dates or after agreed events. | Medium term Long term | High | Set step dates, increased amounts, affordability assumptions and whether missed steps trigger default. |

Stepped-down repayments | ||||

Instalments | Repayments start higher and reduce at agreed dates or after a target balance is reached. | Medium term | Medium | Clarify reduction triggers, revised schedule and whether overpayments affect later instalments. |

Graduated repayment plan | ||||

Instalments | Scheduled repayments gradually rise over time, usually to match expected income growth. | Long term | High | Include a complete schedule and state whether interest is capitalised during lower-payment periods. |

Balloon repayment | ||||

Instalments | Borrower makes smaller instalments during the term and a large final repayment at maturity. | Medium term Long term | Medium | State balloon amount, maturity date, refinancing assumptions and default if final payment is not made. |

Mini-balloon repayments | ||||

Instalments | Borrower makes periodic instalments with one or more larger scheduled payments before final maturity. | Medium term | Medium | List each larger payment date and amount, and specify whether failure accelerates the whole loan. |

Interest-only with final principal repayment | ||||

Instalments Single repayment | Borrower pays interest periodically and repays all principal at the end of the term. | Medium term Long term | High | Define interest dates, final principal date, repayment strategy and lender monitoring rights. |

Interest-only with principal sweeps | ||||

Instalments | Borrower pays regular interest and makes principal repayments from defined surplus cash or receipts. | Medium term | Medium | Define surplus cash, sweep frequency, evidence, minimum liquidity and permitted exclusions. |

Fully amortising loan | ||||

Instalments | Scheduled instalments repay all principal and interest by the final repayment date. | Medium term Long term | Low | Include amortisation table, recalculation rules and final balancing payment wording. |

Partially amortising loan | ||||

Instalments | Instalments reduce part of the principal, with remaining balance due at maturity. | Medium term Long term | Medium | State amortised amount, residual balance, maturity repayment and refinancing assumptions. |

Negative amortisation | ||||

Instalments | Scheduled payments are less than accruing interest, so unpaid interest is added to principal. | Medium term Long term | High | Clearly permit capitalisation, cap the balance, disclose total cost and check regulated credit rules. |

Deferred repayment period | ||||

Instalments Single repayment | Repayments start only after an agreed deferral period, event or long-stop date. | Medium term Flexible | High | Define deferral period, interest accrual, capitalisation, long-stop date and payment schedule after deferral. |

Initial grace period then instalments | ||||

Instalments | Borrower makes no principal payments for a short initial period, then begins scheduled repayments. | Short term Medium term | High | State whether interest is payable during grace period and when missed grace conditions end. |

Seasonal repayments | ||||

Instalments | Repayments are concentrated in months when the borrower expects stronger seasonal cash flow. | Short term Medium term | High | Define seasonal payment dates, lower off-season payments and covenant testing periods. |

Irregular scheduled instalments | ||||

Instalments | Borrower pays different amounts on bespoke dates agreed in a repayment schedule. | Flexible | High | Attach a schedule with exact dates, amounts, final balance and order of allocation. |

Income-based repayments | ||||

Instalments Milestone-based | Borrower repays a percentage of defined income until a cap, term or balance is reached. | Flexible Long term | High | Define income, reporting, audit rights, minimum payments, cap and consequences of under-reporting. |

Revenue-based repayments | ||||

Instalments Milestone-based | Business borrower repays an agreed percentage of revenue until a repayment cap is met. | Flexible | High | Define gross revenue, exclusions, reporting frequency, verification rights and minimum monthly payment. |

Profit-linked repayments | ||||

Instalments Milestone-based | Repayment amount varies by reference to defined accounting profit or distributable cash. | Flexible Long term | High | Define profit measure, accounting standards, adjustments, audit rights and anti-avoidance protections. |

Excess cash sweep | ||||

Milestone-based Instalments | Borrower must apply agreed excess cash to repay the loan at set testing dates. | Medium term Long term | Medium | Define excess cash flow, permitted deductions, testing date, percentage sweep and certificate requirements. |

Asset sale proceeds sweep | ||||

Milestone-based | Borrower repays the loan from net proceeds of specified asset disposals. | Flexible | Medium | Define disposal, net proceeds, reinvestment rights, timing and mandatory prepayment amount. |

Insurance proceeds repayment | ||||

Milestone-based | Borrower repays from insurance proceeds unless permitted to reinstate or replace the insured asset. | Flexible | Medium | Define proceeds, reinstatement period, evidence, lender consent and mandatory prepayment trigger. |

Refinancing proceeds repayment | ||||

Milestone-based Single repayment | Borrower repays the loan when replacement debt or equity financing is completed. | Short term Flexible | Medium | Define qualifying refinancing, long-stop date, permitted deductions and release mechanics. |

Sale completion repayment | ||||

Milestone-based Single repayment | Borrower repays on completion of a property, business or asset sale. | Short term Flexible | Medium | Identify sale asset, completion trigger, solicitor undertaking if relevant and repayment waterfall. |

Development exit repayment | ||||

Milestone-based Single repayment | Property developer repays from development sale proceeds or exit refinance at practical completion. | Short term Medium term | Medium | Define practical completion, sales proceeds, cost overruns, monitoring surveyor reports and long-stop date. |

Drawdown-by-drawdown repayment | ||||

Instalments Revolving | Each advance has its own repayment date or amortisation profile. | Flexible | High | Track each utilisation, interest period, repayment date and allocation of partial repayments. |

Tranche-specific repayment schedule | ||||

Instalments Milestone-based | Different loan tranches are repaid under separate schedules or priority rules. | Medium term Long term Flexible | Medium | Define tranche ranking, repayment order, cross-defaults and whether prepayments reduce tranches pro rata. |

Staggered bullet maturities | ||||

Single repayment Instalments | Separate portions of the loan mature on different dates and are each repaid in one amount. | Medium term Long term | Medium | List maturity dates, amounts, ranking and whether unpaid earlier bullets accelerate later bullets. |

Repayable on demand | ||||

On demand | Borrower must repay when the lender makes a valid demand for repayment. | Flexible Short term | Low | Specify demand form, service method, notice period, repayment deadline and accrued interest. |

Demand loan with notice period | ||||

On demand | Lender may demand repayment, but borrower has an agreed notice period before payment is due. | Flexible | Medium | State minimum notice, deemed receipt, demand contents and whether notice can be waived on default. |

Repayable on specified event | ||||

On demand Milestone-based | Borrower repays when a defined event occurs, such as sale, refinance, death or change of control. | Flexible | Medium | Define trigger events, evidence, repayment deadline and whether lender demand is also required. |

Callable fixed-term loan | ||||

On demand Single repayment | Loan has a maturity date, but lender may require earlier repayment under agreed call rights. | Medium term Flexible | Low | Define call events, notice period, repayment premium and limits on arbitrary lender calls. |

Overdraft-style repayable on demand | ||||

On demand Revolving | Borrower may draw and repay within a limit, with outstanding balance repayable on lender demand. | Flexible Short term | High | Set limit, interest calculation, review dates, demand rights and unauthorised overdraft consequences. |

Revolving credit repayments | ||||

Revolving | Borrower may repay and redraw amounts during the availability period, subject to the facility limit. | Short term Medium term Flexible | High | Define availability period, utilisation requests, repayment mechanics, redraw rights and final maturity. |

Reducing revolving facility | ||||

Revolving Instalments | Borrower may redraw within a facility limit that reduces on scheduled dates. | Medium term | Medium | Set reduction dates, reduced limits, excess repayment duty and redraw restrictions after reductions. |

Non-reducing revolving facility | ||||

Revolving | Repaid amounts can be redrawn up to a constant facility limit until the availability period ends. | Short term Medium term Flexible | High | Specify final repayment date, cancellation rights, fees and conditions to each redraw. |

Revolving facility with clean-down | ||||

Revolving | Borrower must reduce drawings to zero, or below a set level, for a specified period. | Medium term Flexible | Medium | Define clean-down period, permitted cash sources, testing evidence and breach consequences. |

Minimum payment line of credit | ||||

Revolving Instalments | Borrower may redraw but must make minimum periodic payments based on balance, interest or a fixed sum. | Flexible | High | Define minimum payment formula, payment hierarchy, credit limit and effect of over-limit balances. |

Credit card-style monthly minimum | ||||

Revolving Instalments | Borrower repays at least a minimum amount each month and may carry the remaining balance. | Flexible | High | Consumer agreements must address statements, APR, minimum payment, persistent debt and arrears rules. |

Card receivables split repayment | ||||

Milestone-based Instalments | Repayments are collected as a percentage of card takings until the agreed amount is repaid. | Short term Flexible | High | Clarify whether arrangement is loan or receivables purchase, collection method and reconciliation rights. |

Invoice proceeds repayment | ||||

Milestone-based | Borrower repays from specified customer invoice collections or assigned receivables. | Short term Flexible | Medium | Identify receivables, collection account, debtor notices, dilution risk and repayment waterfall. |

Inventory sale proceeds repayment | ||||

Milestone-based | Borrower repays as financed stock or inventory is sold. | Short term Flexible | Medium | Define financed inventory, sale proceeds, reporting, retention of title and shortfall repayment. |

Project milestone repayment | ||||

Milestone-based | Borrower repays specified amounts when project milestones are achieved or certified. | Medium term Flexible | Medium | Use objective milestones, certification process, evidence requirements and long-stop dates. |

Completion certificate repayment | ||||

Milestone-based Single repayment | Repayment becomes due when an independent certificate confirms completion of works or project stage. | Short term Medium term | Medium | Name certifier, certificate standard, dispute process and payment deadline after certification. |

Milestone drawdown then amortisation | ||||

Milestone-based Instalments | Funds are advanced on milestones, then all drawn amounts amortise after the availability period. | Medium term Long term | High | Define drawdown milestones, availability cut-off, repayment start date and aggregate amortisation schedule. |

Bullet with voluntary prepayment option | ||||

Single repayment | Borrower may repay early before the full balance is due at maturity. | Short term Medium term Flexible | High | Set notice, minimum prepayment, allocation, break costs and whether amounts may be reborrowed. |

Instalments with optional overpayments | ||||

Instalments | Borrower makes scheduled instalments and may pay extra amounts to reduce principal faster. | Medium term Long term Flexible | High | State whether overpayments reduce term, reduce later instalments, incur charges or require notice. |

Mandatory prepayment on illegality | ||||

Milestone-based Single repayment | Borrower must repay if it becomes unlawful for the lender to maintain the loan. | Flexible | Low | Define illegality notice, cure period, replacement lender options and repayment timing. |

Mandatory prepayment on change of control | ||||

Milestone-based Single repayment | Borrower must repay, or offer to repay, if ownership or control changes. | Flexible | Low | Define control, permitted transfers, lender consent, notice timing and repayment price. |

Acceleration after event of default | ||||

On demand Single repayment | On default, lender may declare all outstanding principal and interest immediately due. | Flexible | Low | Link to defined events of default, cure periods, notice requirements and enforcement rights. |

Automatic acceleration on insolvency | ||||

Single repayment On demand | All sums become immediately due automatically if specified insolvency events occur. | Flexible | Low | Define insolvency events carefully and consider administration moratorium and enforcement restrictions. |

Consumer early settlement repayment | ||||

Single repayment Instalments | A regulated consumer borrower may discharge indebtedness early under the Consumer Credit Act 1974. | Flexible | High | Check early settlement rules, rebate calculation, notices and enforceability for regulated agreements. |

Early repayment with break costs | ||||

Single repayment Instalments | Borrower may repay early but must compensate lender for defined funding or hedging losses. | Medium term Long term | Medium | Define break costs, calculation certificate, notice, payment date and consumer-law limits if applicable. |

No voluntary prepayment | ||||

Single repayment Instalments | Borrower must follow the agreed schedule and cannot repay early without lender consent. | Medium term Long term | Low | State restriction clearly and check whether statutory early settlement rights override it. |

Repayment by set-off | ||||

Milestone-based Single repayment | Amounts owed by lender to borrower are applied against the borroweru0027s repayment obligation. | Flexible | Medium | Define eligible set-off amounts, timing, notice and whether set-off is excluded on default. |

Repayment in kind | ||||

Single repayment Milestone-based | Borrower repays by transferring agreed assets instead of cash. | Flexible | Medium | Specify asset valuation, title, delivery, taxes, shortfall payment and security release. |

Payment-in-kind interest with cash principal | ||||

Single repayment Instalments | Interest is capitalised into principal during the term borrower repays enlarged balance later. | Medium term Long term | High | Define PIK periods, compounding, capitalised interest, caps and tax treatment. |

Split cash and PIK repayments | ||||

Instalments Single repayment | Borrower pays part interest in cash and capitalises the rest for later repayment. | Medium term Long term | High | State cash margin, PIK margin, election rights, compounding and payment waterfall. |

Bullet with extension option | ||||

Single repayment | Borrower may extend maturity if agreed conditions are met, delaying final repayment. | Medium term Flexible | High | Define extension notice, fee, conditions, maximum term and revised interest rate. |

Rollover repayment | ||||

Single repayment Revolving | Maturing amount is refinanced into a new interest period instead of being repaid immediately. | Short term Flexible | High | Set rollover request process, conditions precedent, interest period limits and final maturity. |

Bridging loan exit repayment | ||||

Single repayment Milestone-based | Short-term loan is repaid from a defined exit source, usually sale or refinance. | Short term | Medium | Identify exit route, long-stop date, security, default interest and regulated mortgage status if relevant. |

Rental income sweep | ||||

Instalments Milestone-based | Borrower applies rental income, or surplus rental income, to interest and principal repayments. | Medium term Long term | Medium | Define rent account, permitted property costs, void periods, reserve requirements and arrears treatment. |

Salary deduction repayments | ||||

Instalments | Repayments are deducted from salary under an agreed payroll or employer arrangement. | Short term Medium term | Low | Obtain clear authority, address employment termination, data protection and consumer credit status. |

Director loan account repayment | ||||

Single repayment Instalments On demand | Company or director repays an outstanding director loan account by agreed dates or on demand. | Flexible | Medium | Address board approval, Companies Act duties, tax charges and written demand mechanics. |

Shareholder loan repayment | ||||

Single repayment Instalments On demand | Company repays shareholder debt under a fixed schedule, at maturity or when demanded. | Flexible Long term | Medium | Consider subordination, solvency, conflicts, tax, connected-party pricing and distribution restrictions. |

Intercompany loan repayment | ||||

Single repayment Instalments On demand | Group company borrower repays another group company on agreed terms or on demand. | Flexible | High | Document armu0027s length terms, transfer pricing, subordination, withholding tax and year-end balances. |

Subordinated loan repayment | ||||

Single repayment Instalments | Borrower repays only when senior debt terms allow, often after senior lender consent. | Long term Flexible | Medium | Include subordination, payment blockage, turnover provisions and intercreditor consent rules. |

Waterfall repayment structure | ||||

Instalments Milestone-based | Cash is applied in a fixed order, usually costs, interest, principal, fees and subordinated amounts. | Flexible Long term | Medium | Set priority order, blocked payments, reserve accounts and treatment after default or enforcement. |

Escrow-funded repayment | ||||

Single repayment Milestone-based | Repayment is made from money held in an escrow or designated account when release conditions are met. | Short term Flexible | Low | Define escrow agent, release conditions, account control, interest on funds and dispute process. |

Sinking fund repayment | ||||

Instalments Single repayment | Borrower makes regular deposits into a reserve used to repay principal at set dates or maturity. | Long term | Low | Specify deposit amounts, reserve account control, permitted withdrawals and shortfall remedies. |

Cash trap repayment | ||||

Milestone-based Instalments | Cash is trapped in a controlled account after a trigger and applied to debt service or prepayment. | Medium term Long term Flexible | Low | Define trigger, cure, trapped amounts, account control and release conditions. |

Debt service reserve repayment | ||||

Instalments Milestone-based | A reserve account is used to pay scheduled debt service if borrower cash flow is insufficient. | Medium term Long term | Medium | Set required balance, replenishment duty, permitted drawings and default if reserve is not topped up. |

Secured asset realisation repayment | ||||

Milestone-based Single repayment | Loan is repaid from enforcement or sale proceeds of secured assets, with borrower liable for shortfall. | Flexible | Low | Ensure valid security, enforcement powers, valuation, proceeds waterfall and shortfall clause. |

Guarantor demand repayment | ||||

On demand Single repayment | If borrower does not pay, lender demands payment from guarantor under the guarantee. | Flexible | Low | Guarantee should cover principal, interest, costs, demand process and continuing liability. |

Joint and several borrower repayment | ||||

Single repayment Instalments On demand | Each borrower is liable for all repayments, not just its share of the loan. | Flexible | Low | State joint and several liability, contribution rights, notices and release of one borrower. |

Several liability repayment | ||||

Instalments Single repayment | Each borrower repays only its allocated share of principal, interest and costs. | Flexible | Medium | Define each borroweru0027s share, payment account, default effect and cross-default position. |

Standstill then catch-up repayments | ||||

Instalments Single repayment | Repayments are paused during a standstill, then arrears are caught up by lump sum or revised schedule. | Flexible | High | Document waiver scope, reserved rights, revised dates, default status and interest during standstill. |

Arrears capitalisation and reschedule | ||||

Instalments | Missed amounts are added to the balance and repaid over a revised schedule. | Flexible Medium term | High | Record arrears, capitalised amount, revised schedule, waiver limits and credit reporting treatment. |

Split amortising and bullet portions | ||||

Instalments Single repayment | Part of the loan amortises by instalments while the remainder is repaid at maturity. | Medium term Long term | Medium | Define amortising portion, bullet portion, payment allocation and prepayment application. |

Index-linked repayment | ||||

Instalments Single repayment | Repayment amounts are adjusted by reference to an agreed index, such as CPI or RPI. | Long term | Low | Define index, base date, adjustment formula, replacement index and caps or floors. |

Foreign currency repayment | ||||

Single repayment Instalments | Borrower repays in a currency different from sterling or from its income currency. | Flexible | Medium | Specify payment currency, exchange rate source, currency indemnity and conversion costs. |

Sterling equivalent repayment | ||||

Single repayment Instalments | Repayment is calculated by converting a foreign currency amount into sterling at an agreed rate. | Flexible | Medium | State conversion date, rate source, who bears FX movement and rounding method. |

Murabaha deferred price instalments | ||||

Instalments Single repayment | Customer pays a deferred sale price by instalments or at maturity instead of conventional interest. | Short term Medium term Long term | Medium | Document asset sale, deferred price, payment dates, late payment treatment and tax consequences. |

Commodity murabaha bullet payment | ||||

Single repayment | Customer pays the marked-up deferred price in one amount at maturity. | Short term Medium term | Medium | Ensure commodity trades, agency terms, deferred price and payment default provisions are clear. |

Hire purchase instalments | ||||

Instalments | Customer pays instalments for use of goods and usually acquires title after final payment. | Medium term | Low | Address title retention, option to purchase fee, termination rights and regulated credit rules. |

Conditional sale instalments | ||||

Instalments | Buyer pays instalments and ownership transfers automatically after all conditions and payments are satisfied. | Medium term | Low | Define title transfer, default repossession, payment schedule and consumer credit compliance. |

Personal contract purchase final balloon | ||||

Instalments Single repayment | Customer pays instalments and may pay a final optional balloon to acquire the vehicle. | Medium term | Medium | State optional final payment, mileage terms, return condition and regulated motor finance duties. |

Income-contingent student loan repayment | ||||

Instalments | Repayments are based on income thresholds and collected through PAYE or self-assessment where applicable. | Long term Flexible | High | Usually statutory rather than bespoke private drafting do not copy into ordinary private loans without advice. |

Capital repayment mortgage | ||||

Instalments | Borrower pays interest and capital each month so the mortgage is repaid by term end. | Long term | Low | Regulated mortgage contracts need FCA-compliant disclosures, affordability assessment and arrears handling. |

Interest-only mortgage repayment | ||||

Instalments Single repayment | Borrower pays monthly interest and repays capital from a separate repayment strategy at term end. | Long term | High | Identify repayment strategy, review duties, maturity risk and FCA mortgage conduct requirements. |

Lifetime mortgage roll-up repayment | ||||

Single repayment Milestone-based | Interest rolls up and loan is usually repaid from property sale after death or permanent care move. | Long term Flexible | High | Check regulated lifetime mortgage rules, advice requirements, no-negative-equity terms and trigger events. |

Roll-up interest with optional payments | ||||

Single repayment Instalments | Borrower may pay some interest voluntarily unpaid interest is added to the balance. | Long term Flexible | High | Define optional payment rights, interest roll-up, compounding, caps and final repayment trigger. |

Drawdown lifetime mortgage repayment | ||||

Revolving Single repayment Milestone-based | Borrower draws amounts over time rolled-up balance is repaid on sale after trigger event. | Long term Flexible | High | Define drawdown reserve, trigger events, advice process, interest roll-up and property sale mechanics. |

Peer-to-peer platform instalments | ||||

Instalments | Borrower repays through a platform which distributes payments to lenders or investors. | Short term Medium term | Medium | Address platform role, payment agency, investor allocation, defaults and FCA crowdfunding rules. |

Buy-now-pay-later deferred instalments | ||||

Instalments | Customer pays purchase price later in short instalments, often interest-free if paid on time. | Short term | Medium | Check exemption or regulation status, disclosures, late fees, cancellations and affordability processes. |

Litigation funding contingent repayment | ||||

Milestone-based | Funder is repaid only from successful claim proceeds, usually by agreed multiple or percentage. | Flexible Long term | High | Clarify non-recourse status, priority, settlement control, adverse costs and damages-based agreement risks. |

Earn-out funded repayment | ||||

Milestone-based | Borrower repays when earn-out or deferred consideration from a business sale is received. | Medium term Flexible | Medium | Define relevant consideration, timing, evidence, disputes and whether non-receipt extends maturity. |

Grant receipt repayment | ||||

Milestone-based Single repayment | Bridge funding is repaid when expected grant, subsidy or public funding is received. | Short term Flexible | Medium | Identify funding source, eligibility conditions, long-stop date, non-receipt risk and repayment alternative. |

Tax refund repayment | ||||

Milestone-based Single repayment | Borrower repays when an expected tax refund or credit is received from HMRC. | Short term Flexible | Medium | Define refund, HMRC correspondence, receipt account, repayment deadline and non-receipt fallback. |

Completion monies repayment | ||||

Milestone-based Single repayment | Borrower repays from completion monies received under a sale, investment or financing transaction. | Short term Flexible | Medium | Define transaction, completion evidence, funds flow, solicitor undertakings and failed completion fallback. |

Interest reserve then bullet repayment | ||||

Single repayment Instalments | Interest is paid from a funded reserve during the term principal is repaid at maturity. | Short term Medium term | High | Set reserve amount, permitted use, top-up duty, shortfall events and final principal repayment. |

Covenant-ratchet repayment amount | ||||

Instalments Single repayment | Interest component of repayments changes when financial ratios or agreed thresholds change. | Medium term Long term | Medium | Define ratios, testing dates, information certificates, revised margin date and error correction. |

Inflation-adjusted instalments | ||||

Instalments | Instalment amounts increase or decrease periodically by reference to an inflation index. | Long term | Low | Specify index, adjustment date, base value, cap, floor and replacement index method. |

Fixed principal with variable interest | ||||

Instalments | Principal repayment is fixed, while interest element varies with the reference rate. | Medium term Long term | Medium | Define reference rate, fallback rate, interest periods, notification and payment recalculation. |

Rate-reset variable instalments | ||||

Instalments | Instalments are recalculated when the interest rate resets, keeping the term or balance target. | Medium term Long term | Medium | State reset dates, calculation formula, notice period and fallback if rate is unavailable. |

Base-rate linked repayment | ||||

Instalments Single repayment | Interest element varies by reference to Bank of England Bank Rate or another agreed base rate. | Flexible | Medium | Define rate source, change date, notification, negative rate treatment and payment recalculation. |

SONIA-linked repayment | ||||

Instalments Single repayment | Interest is calculated using SONIA, affecting periodic interest payments and final repayment amount. | Medium term Long term Flexible | Medium | Include compounding method, observation shift, lookback, fallback and interest determination provisions. |

Direct debit scheduled repayments | ||||

Instalments | Borrower authorises recurring collections from a bank account for scheduled repayments. | Short term Medium term Long term | Low | Obtain mandate, state collection dates, failed collection consequences and Direct Debit Guarantee rights. |

Continuous payment authority collections | ||||

Instalments On demand | Borrower permits lender to collect repayments from a debit or credit card under a CPA. | Short term Flexible | Low | Explain CPA authority, cancellation rights, retry limits, collection dates and FCA consumer credit rules. |

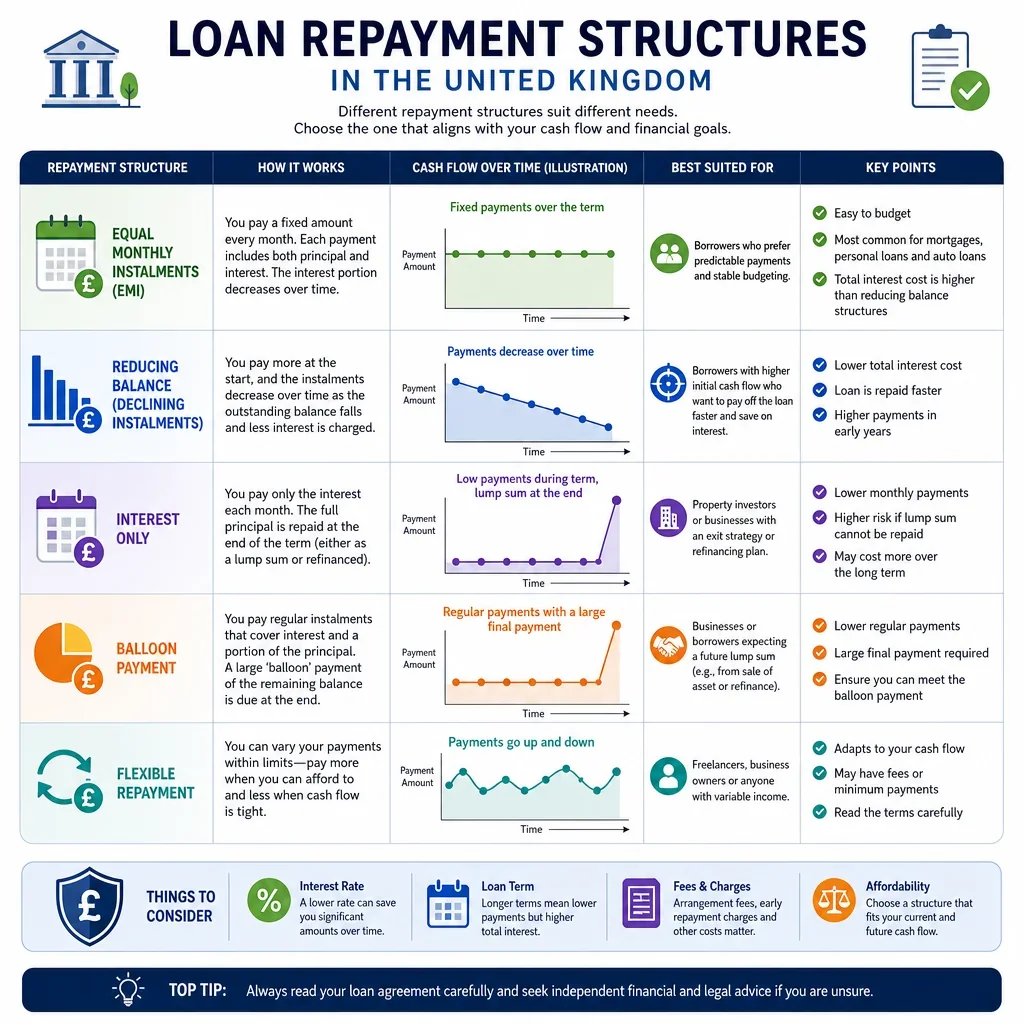

How Should A UK Loan Agreement Choose A Repayment Structure?

The repayment clause is one of the main risk-allocation clauses in a UK loan agreement. A single bullet repayment is simple but creates refinancing risk at maturity, while amortising instalments reduce outstanding principal over time and usually need a clear payment schedule. Demand loans are flexible for lenders, but should state how demand is made and any notice period to avoid uncertainty.

What Repayment Terms Need Extra Care In Drafting?

- Dates, amounts and calculation method: instalment, annuity, balloon and seasonal structures should specify the due dates, principal component, interest treatment, business day convention and rounding.

- Prepayment rights: if the borrower may repay early, the agreement should say whether lender consent, notice, break costs, minimum amounts or prepayment fees apply.

- Default consequences: missed repayment should tie into default interest, acceleration and enforcement clauses, with any consumer or regulated-credit rules checked where relevant.

- Revolving and overdraft-style facilities: these need separate rules for drawings, repayments, redraws, commitment reduction, availability periods and final clean-down or maturity repayment.

- Milestone-based lending: where repayment depends on sales, drawdown milestones or project completion, objective triggers and evidence requirements are essential.

When Do UK Consumer Credit Rules Matter?

If the borrower is an individual, sole trader or small partnership, the Consumer Credit Act 1974 and FCA consumer credit rules may affect repayment notices, early settlement, arrears notices and enforceability. Business loans, connected-company loans and high-net-worth arrangements may be treated differently, so the repayment structure should be checked against the regulatory status of the loan before the document is signed.

FAQs

You Might Also Be Interested In