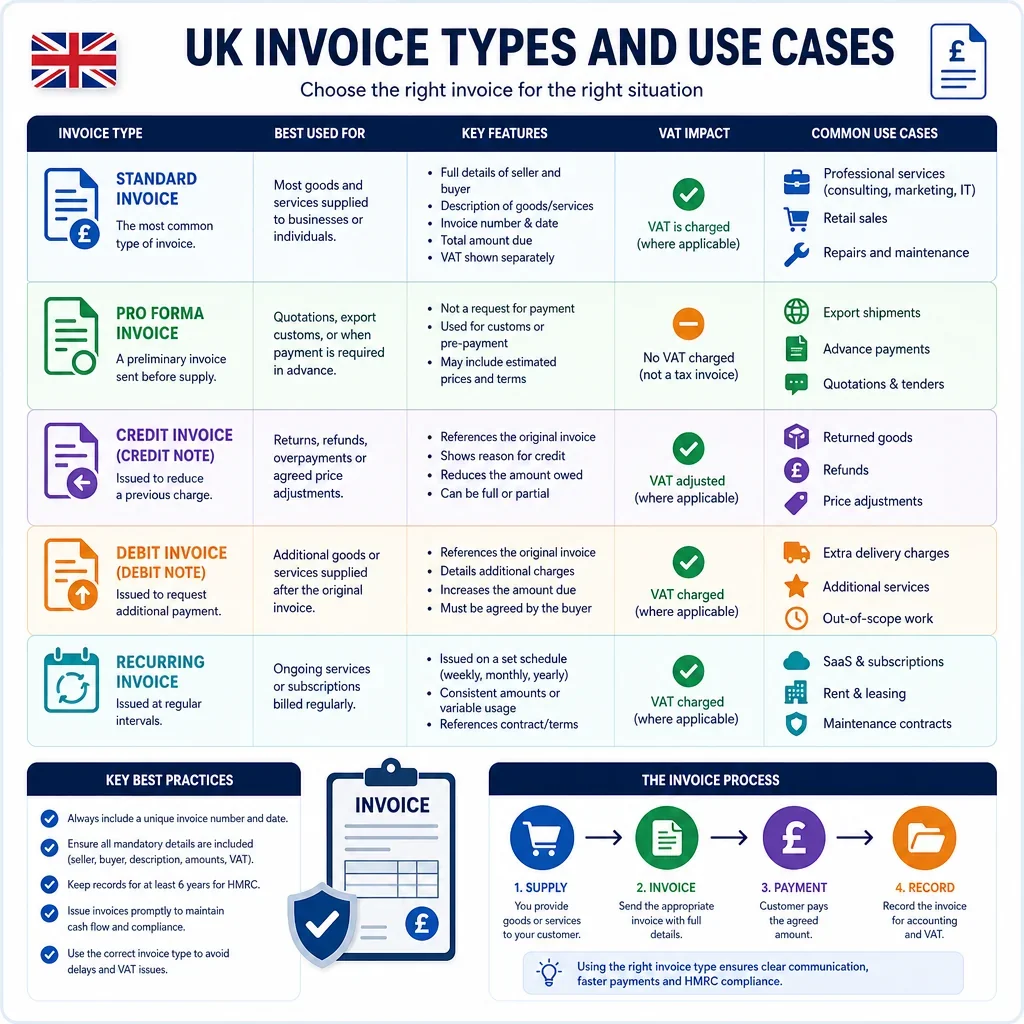

UK Invoice Types And Use Cases

Invoice Type | Purpose | Transaction Context | Requires Invoice Number | UK Drafting Notes |

|---|---|---|---|---|

After supply | ||||

Standard invoice | Requests payment for completed goods or services supplied on credit terms. | Goods and services | true | Include supplier and customer details, clear description, invoice date, unique invoice number, amount due, payment terms and VAT details if VAT registered. |

VAT invoice | Provides VAT evidence for a taxable supply between VAT-registered parties. | Goods and services | true | Show unique sequential number, tax point, VAT registration number, VAT rate, VAT amount, net amount and gross total. |

Simplified VAT invoice | Records lower-value retail VAT sales using reduced invoice details. | Goods and services | true | Generally used for supplies not exceeding £250 including VAT include supplier details, VAT number, tax point, description and VAT-inclusive total. |

Modified VAT invoice | Shows VAT details for retail supplies above simplified invoice limits. | Goods and services | true | May show VAT-inclusive values but must include enough VAT information for input tax claims when requested. |

Before supply | ||||

Pro forma invoice | States intended charges before supply or final invoicing not usually a tax invoice. | Goods and services | false | Mark clearly as pro forma and not a VAT invoice replace with a valid invoice once the tax point arises. |

Quotation invoice | Sets out proposed prices before acceptance, often formatted like an invoice. | Goods and services | false | Label as quotation, include validity period, exclusions and VAT position avoid wording that implies immediate payment is due. |

Estimate invoice | Gives an approximate expected charge before the final scope or quantity is known. | Goods and services | false | State that figures are estimates, identify assumptions, VAT treatment and when a final invoice will be issued. |

At payment request | ||||

Interim invoice | Requests part payment during a project before final completion. | Services | true | Refer to milestone, period or valuation, show previous amounts invoiced, VAT treatment and balance remaining. |

After supply | ||||

Final invoice | Requests the final balance once work or supply is complete. | Goods and services | true | Deduct deposits, interim invoices, credits and retention state final amount payable and VAT correctly. |

Before supply | ||||

Deposit invoice | Requests an upfront part payment before full supply is completed. | Goods and services | true | For VAT, advance payment can create a tax point state deposit amount, VAT, balance due and refund terms. |

Advance payment invoice | Requests full or partial payment before goods or services are delivered. | Goods and services | true | Make clear whether payment creates a VAT tax point describe later supply and how any balance will be invoiced. |

Prepayment invoice | Collects payment in advance for future supply, often for services or licences. | Services | true | State covered period, VAT treatment, refund terms and whether further invoices will follow after performance. |

At recurring interval | ||||

Recurring invoice | Bills the same customer repeatedly for ongoing goods or services. | Recurring billing | true | Use a unique number for each invoice specify billing period, renewal basis, VAT rate and payment method. |

Subscription invoice | Bills periodic access to software, membership, media or other subscriptions. | Recurring billing | true | State subscription term, auto-renewal, cancellation route, VAT treatment and whether charges are in advance or arrears. |

Retainer invoice | Requests payment for reserved professional capacity or ongoing advisory services. | Services | true | Identify covered period, scope, unused time rules, expenses, VAT and termination provisions. |

After supply | ||||

Timesheet invoice | Bills services by hours or days worked during a stated period. | Services | true | Attach or reference approved timesheets, day rates, expenses, VAT and payment terms. |

At payment request | ||||

Milestone invoice | Requests payment when a defined project milestone is reached. | Services | true | Identify contractual milestone, acceptance evidence, percentage or amount due, VAT and any holdbacks. |

Progress invoice | Bills staged work by percentage completion or measured progress. | Services | true | Show contract value, percentage complete, prior applications, current amount, retention, VAT and balance to completion. |

Construction interim invoice | Requests payment during construction works under staged contractual payment provisions. | Services | true | Align with contract payment dates, valuation rules, payment notice process, retention and construction VAT domestic reverse charge where relevant. |

Retention invoice | Requests release of retained sums after completion or defects period. | Services | true | Reference original contract, retention percentage, completion certificate or defects expiry, VAT treatment and remaining deductions. |

After supply | ||||

Domestic reverse charge invoice | Invoices specified construction services where the customer accounts for VAT. | Services | true | Do not charge VAT to the customer state that the VAT domestic reverse charge applies and show the VAT rate due. |

After correction | ||||

Credit note | Reduces or cancels an earlier invoice after an overcharge, return or allowance. | Credit adjustment | true | Reference original invoice, state reason, amounts credited and VAT adjustment keep a clear audit trail. |

VAT credit note | Adjusts VAT and taxable value down after a VAT invoice has been issued. | Credit adjustment | true | Include credit note number, date, original invoice reference, VAT rate, VAT amount reduced and reason for adjustment. |

Debit note | Increases the amount payable after an undercharge or extra supply. | Credit adjustment | true | Reference original invoice or supply, explain the additional charge and show VAT correctly where applicable. |

Corrected invoice | Replaces an invoice containing administrative or charging errors. | Goods and services | true | Avoid deleting the original record mark replacement clearly and preserve links to credit or debit adjustments. |

Cancellation invoice | Documents cancellation of a mistaken or no-longer-payable invoice. | Credit adjustment | true | Use a credit note where VAT or accounts have been affected retain the original invoice for audit purposes. |

Before supply | ||||

Commercial export invoice | Supports customs clearance and payment for goods exported from the UK. | Goods | true | Include seller, buyer, goods description, value, currency, origin, commodity codes, Incoterms and export VAT status. |

Customs pro forma invoice | Provides customs details for non-sale shipments such as samples, gifts or replacements. | Goods | false | State no sale if applicable, give realistic customs value, goods description, origin, commodity codes and reason for export. |

After supply | ||||

Export VAT invoice | Records exported goods and supports zero-rating where conditions are met. | Goods | true | Keep export evidence, state zero-rated VAT where applicable and include shipping, destination and customer details. |

Before supply | ||||

Import invoice | Documents goods bought from overseas for import valuation and accounting. | Goods | true | Ensure value, currency, seller, buyer, origin, commodity code and freight terms match customs declarations. |

After supply | ||||

Self-billing invoice | Customer prepares the VAT invoice on behalf of the supplier. | Goods and services | true | Requires a self-billing agreement include supplier VAT details, customer-generated invoice number and VAT information. |

Purchase invoice | Records an invoice received from a supplier for business purchases. | Goods and services | true | For internal records, capture supplier invoice number, date, net, VAT, gross, tax point and evidence for VAT recovery. |

Supplier invoice | Supplier-issued document demanding payment for supplied goods or services. | Goods and services | true | Check legal name, VAT number, bank details, payment terms and purchase order reference before payment. |

Sales invoice | Seller-issued invoice recording revenue and requesting payment from a customer. | Goods and services | true | Use a unique invoice number show seller details, customer details, items supplied, price, VAT if applicable and due date. |

Service invoice | Bills professional, consultancy, trade or other services supplied. | Services | true | Describe service scope, period, rate or fixed fee, expenses, VAT treatment and payment terms. |

Goods invoice | Bills physical products supplied to a customer. | Goods | true | Include product description, quantities, unit prices, delivery details, VAT rate, discounts and title or risk terms if relevant. |

Mixed supply invoice | Bills goods and services with different descriptions, rates or VAT treatments. | Goods and services | true | Separate line items by VAT rate or liability avoid combining taxable, zero-rated and exempt items ambiguously. |

Zero-rated VAT invoice | Records taxable supplies charged at 0% VAT. | Goods and services | true | Show 0% VAT rate and keep evidence supporting zero-rating, such as export evidence or product liability basis. |

Exempt supply invoice | Records supplies outside VAT charging because they are exempt. | Goods and services | true | Do not charge VAT state exempt where helpful and consider partial exemption implications for input tax recovery. |

Non-VAT invoice | Bills customers where the supplier is not VAT registered or VAT is not charged. | Goods and services | true | Do not show VAT as charged avoid using a VAT registration number unless registered include ordinary invoice essentials. |

Sole trader invoice | Requests payment from a customer for work or goods supplied by a sole trader. | Goods and services | true | Include sole trader name and any business name, address, unique number, description, price and VAT details if registered. |

Limited company invoice | Requests payment using a UK companyu0027s registered corporate details. | Goods and services | true | Include full company name as on Companies House, registered office if required, company number where used, VAT number if registered and payment details. |

Purchase order invoice | Matches a customer purchase order for procurement approval and payment. | Goods and services | true | Quote the PO number, buyer entity, delivery or service reference, agreed prices and VAT treatment to avoid rejection. |

At payment request | ||||

Expense reimbursement invoice | Claims reimbursable costs incurred while providing services. | Services | true | Distinguish disbursements from recharged expenses attach receipts and apply VAT correctly to onward charges. |

Disbursement invoice | Passes on costs paid as agent for the customer rather than as supplier expenses. | Services | true | Only treat as disbursement if agency conditions are met list separately from taxable fees and retain third-party evidence. |

Late payment interest invoice | Claims statutory or contractual interest and compensation on overdue commercial debts. | Services | true | State original invoice, overdue period, interest rate, compensation, calculation basis and whether VAT applies to any separate charge. |

At recurring interval | ||||

Rent invoice | Requests rent or licence fees for occupation of property. | Recurring billing | true | State rent period, property, lease reference, VAT position, option to tax if applicable, service charge and payment date. |

Service charge invoice | Bills property service charges such as maintenance, insurance or shared facilities. | Recurring billing | true | Identify property, service period, apportionment, VAT treatment, reserve fund items and lease basis. |

Royalty invoice | Bills licence fees or royalties for use of intellectual property. | Services | true | Reference licence agreement, royalty period, calculation basis, sales reports, withholding tax issues and VAT treatment. |

After supply | ||||

Commission invoice | Claims commission earned on introductions, sales or agency activity. | Services | true | State commission period, transactions, rate, exclusions, VAT treatment and supporting sales schedule. |

Agency invoice | Bills agency fees or principal transactions handled through an agent. | Services | true | Clarify whether billing as agent or principal, separate commission, client money, VAT and third-party charges. |

Before supply | ||||

Consignment invoice | Documents goods sent to a consignee for sale, often before final sale proceeds are known. | Goods | false | State consignment status, ownership retained, quantities, expected prices, commission and when a final sales invoice is issued. |

After supply | ||||

Delivery invoice | Bills delivery, carriage or shipping charges separately from goods. | Services | true | Specify shipment reference, delivery date, address, carrier charges and VAT treatment linked to the underlying supply. |

At recurring interval | ||||

Consolidated invoice | Combines multiple deliveries, jobs or orders into one invoice for a period. | Goods and services | true | List each supply with dates, references and VAT treatment ensure tax points and records support the consolidated total. |

Statement invoice | Summarises invoices, credits and payments to show an account balance. | Recurring billing | false | Do not present as a VAT invoice unless it contains valid invoice details reference underlying invoice numbers and due balances. |

Balance forward invoice | Carries forward unpaid balances and adds new current charges. | Recurring billing | true | Separate new taxable supplies from previously invoiced arrears to avoid duplicating VAT or revenue. |

After supply | ||||

Electronic invoice | Issues an invoice digitally rather than on paper. | Goods and services | true | Ensure authenticity, integrity and readability retain digital records in line with VAT and accounting requirements. |

Public sector e-invoice | Allows electronic invoicing to public authorities under public procurement e-invoicing rules. | Goods and services | true | Use the required electronic standard or buyer portal format and include PO references, supplier identifiers and VAT data. |

At payment request | ||||

Payment request invoice | Requests payment where the document may not yet be a final VAT invoice. | Goods and services | false | Label carefully, state payment purpose and issue a valid VAT invoice when required by VAT rules. |

Application for payment | Requests valuation and payment under a construction contract before certification or invoice. | Services | false | Follow contract payment timetable identify valuation date, work measured, materials, variations, retention and VAT implications. |

After supply | ||||

Fee note | Requests professional fees, commonly used by advisers, consultants and experts. | Services | true | State professional services performed, matter reference, time or fixed fee, expenses, VAT and payment terms. |

Legal services invoice | Bills solicitorsu0027 fees, disbursements and expenses for legal work. | Services | true | Separate profit costs, VAT and disbursements include client or matter reference and comply with client money rules where relevant. |

Healthcare invoice | Bills private healthcare, clinical reports or related medical services. | Services | true | Check whether the service is VAT exempt healthcare or taxable administrative work protect patient data in descriptions. |

Charity invoice | Bills charity trading, services, grants or reimbursed costs with charity-specific VAT considerations. | Goods and services | true | Identify whether payment is consideration for a supply, donation, grant or exempt activity apply charity VAT reliefs only where valid. |

Reverse charge services invoice | Invoices cross-border B2B services where the customer accounts for VAT. | Services | true | State reverse charge applies, identify customer VAT details where relevant and do not charge UK VAT if outside UK place of supply. |

VAT margin scheme invoice | Invoices eligible second-hand goods, art, antiques or collectorsu0027 items under a margin scheme. | Goods | true | Do not show VAT separately include required margin scheme wording and maintain purchase and stock records. |

Second-hand vehicle margin invoice | Bills eligible used vehicles sold under the VAT margin scheme. | Goods | true | Do not disclose VAT separately include vehicle details, mileage, registration, margin scheme wording and sale price. |

CIS subcontractor invoice | Bills construction work where Construction Industry Scheme deductions may apply. | Services | true | Separate labour and materials, show VAT correctly, state UTR or CIS details if agreed and do not deduct CIS from materials. |

Receipt invoice | Confirms payment received and may also evidence the sale where invoice details are present. | Goods and services | false | Do not rely on a basic receipt for VAT recovery unless it contains required VAT invoice information. |

Retail receipt invoice | Provides point-of-sale evidence for retail purchases, often as a simplified VAT invoice. | Goods and services | false | For VAT claims, ensure receipt shows supplier VAT number, tax point, description and VAT rate or VAT-inclusive amount as required. |

At recurring interval | ||||

Instalment invoice | Requests one scheduled instalment under a payment plan or contract. | Recurring billing | true | State instalment number, total contract price, previous payments, remaining balance, VAT tax point and default consequences. |

At payment request | ||||

Hire purchase invoice | Bills goods supplied under hire purchase or conditional sale arrangements. | Goods | true | Separate goods price, finance charges, VAT and payment schedule consumer credit rules may apply. |

At recurring interval | ||||

Hire invoice | Bills temporary hire of equipment, vehicles or assets. | Goods | true | State hire period, asset ID, rates, deposit, damage charges, insurance, VAT and return obligations. |

Before supply | ||||

Warranty invoice | Bills extended warranty, repair cover or warranty-related charges. | Services | true | Identify covered item, term, exclusions, insurance element, VAT or insurance premium tax treatment and cancellation rights if consumer-facing. |

After supply | ||||

Repair invoice | Bills labour, parts and call-out charges for repair work. | Goods and services | true | Separate labour, parts, diagnostic fees, warranty work, VAT and customer authorisation for extra charges. |

Before supply | ||||

Insurance premium invoice | Requests payment of insurance premium and related taxes or fees. | Services | true | Show policy period, premium, Insurance Premium Tax, broker fees and insurer or intermediary details VAT is generally not charged on insurance. |

At payment request | ||||

Grant claim invoice | Requests grant drawdown or reimbursement under a funding agreement. | Services | false | State funding agreement, eligible costs, evidence, milestones and whether payment is outside VAT or consideration for a supply. |

Donation request invoice | Requests or acknowledges voluntary donations rather than payment for a supply. | Services | false | Avoid describing voluntary donations as consideration separate any taxable benefits, sponsorship or advertising charges. |

Before supply | ||||

Sponsorship invoice | Bills sponsorship benefits such as advertising, branding or event rights. | Services | true | Describe benefits supplied, event or campaign dates, VAT treatment and distinguish sponsorship from pure donation. |

After supply | ||||

Factored invoice | Invoice assigned to a factor or finance provider for collection or funding. | Goods and services | true | Include assignment or payment notice, correct remittance account, original invoice details and VAT treatment unchanged. |

At payment request | ||||

Finance charge invoice | Bills interest, finance fees or credit charges linked to payment terms. | Services | true | Specify contractual basis and calculation check whether the charge is exempt finance, compensation or taxable fee. |

After correction | ||||

Cancellation fee invoice | Claims a fee payable when a booking, contract or service is cancelled. | Services | true | Reference cancellation terms, calculation, VAT treatment and whether any advance payment is retained or credited. |

At recurring interval | ||||

Minimum charge invoice | Bills a contractual minimum amount where usage or work is below threshold. | Recurring billing | true | State minimum commitment, actual usage, shortfall, billing period, VAT and contract clause. |

Usage-based invoice | Bills metered consumption such as utilities, telecoms, storage or API usage. | Recurring billing | true | Show billing period, meter or usage data, unit rates, thresholds, VAT and dispute process for readings. |

Utility invoice | Bills electricity, gas, water or similar utilities by period and usage. | Recurring billing | true | State supply address, billing period, readings or estimates, standing charges, VAT rate and climate or regulatory charges where applicable. |

Telecoms invoice | Bills phone, broadband, data or communications services. | Recurring billing | true | Show service numbers, billing period, usage, recurring charges, VAT and any early termination or roaming charges. |

Before supply | ||||

Software licence invoice | Bills software licences, SaaS access or digital services. | Services | true | State licence term, users, renewal, VAT place-of-supply treatment and customer VAT details for B2B cross-border supplies. |

Training invoice | Bills training courses, workshops or education services. | Services | true | State course date, attendee, cancellation terms, VAT status and whether the provider qualifies for education exemption. |

Event invoice | Bills event tickets, venue hire, catering, sponsorship or exhibitor fees. | Goods and services | true | State event date, location, ticket or package, VAT treatment, cancellation terms and any deposit applied. |

After supply | ||||

Hospitality invoice | Bills accommodation, catering, venue or hospitality services. | Goods and services | true | Itemise room, food, drink, service charges and VAT rates identify business guest or booking reference where needed. |

Before supply | ||||

Travel invoice | Bills transport, accommodation or travel agency services. | Services | true | State itinerary, traveller, ticket references, VAT or TOMS treatment where relevant and cancellation terms. |

After supply | ||||

Passenger transport invoice | Bills passenger transport fares or charter transport services. | Services | true | Check zero-rating or standard-rating by vehicle capacity and service type show route, date and passenger details if needed. |

Freight invoice | Bills freight transport, forwarding or associated logistics services. | Services | true | Identify shipment, route, consignor, consignee, freight terms and VAT treatment for UK, export or international transport. |

At recurring interval | ||||

Storage invoice | Bills warehousing, storage units or inventory holding charges. | Recurring billing | true | State storage period, location, goods reference, space used, insurance, access charges and VAT treatment. |

Warehouse handling invoice | Bills picking, packing, handling, fulfilment or warehousing services. | Services | true | Show service period, order volumes, unit rates, storage charges, materials, VAT and service-level adjustments. |

After supply | ||||

Manufacturing invoice | Bills made-to-order goods, materials, labour and production charges. | Goods and services | true | Reference order, specification, batch, delivery, tooling, materials, VAT and retention of title if relevant. |

Wholesale invoice | Bills bulk goods supplied to trade customers or retailers. | Goods | true | Include SKU, quantities, unit prices, discounts, delivery note references, VAT rates and payment terms. |

Drop-shipping invoice | Bills goods fulfilled by a third party directly to the customer. | Goods | true | Clarify seller of record, delivery details, VAT liability, import position and separate supplier invoices. |

Marketplace invoice | Bills sales made through an online marketplace or platform. | Goods and services | true | Identify seller, platform fees, VAT responsibility, order ID and whether marketplace deemed supplier rules apply. |

At recurring interval | ||||

Platform fee invoice | Bills fees charged by a platform, marketplace or payment processor. | Services | true | State gross sales, fees, VAT on fees, refunds, chargebacks, payout period and platform VAT registration details. |

After correction | ||||

Refund invoice | Documents money returned to a customer after payment. | Credit adjustment | true | Usually issue a credit note linked to the original invoice show refund method, VAT reduction and reason. |

Bad debt relief adjustment | Supports VAT bad debt relief where an invoice remains unpaid. | Credit adjustment | false | Keep original invoice and records claim only when statutory conditions and timing for VAT bad debt relief are met. |

Before supply | ||||

Payment on account invoice | Requests an account payment before final fees or costs are known. | Services | true | State that it is on account, explain later reconciliation, VAT tax point and refund or top-up process. |

After supply | ||||

Call-off invoice | Bills goods or services drawn down under a framework or call-off contract. | Goods and services | true | Reference framework, call-off order, delivery or service period, agreed rates, VAT and remaining contract allowance. |

At payment request | ||||

Staged supply invoice | Bills one stage of a longer supply contract as it becomes due. | Goods and services | true | Identify stage, tax point, previous stages, contract value, VAT and balance outstanding. |

At recurring interval | ||||

Continuous supply invoice | Bills ongoing services supplied continuously over time. | Recurring billing | true | State service period, payment date, VAT tax point, renewal terms and any arrears or advance element. |

After correction | ||||

Tax-only invoice | Charges VAT only where VAT was omitted or becomes due separately. | Credit adjustment | true | Reference original supply, explain VAT-only adjustment and ensure customer can identify the tax point and VAT rate. |

After supply | ||||

Contractor invoice | Bills independent contractor services under a contract for services. | Services | true | State contractor name, period, deliverables or days worked, expenses, VAT if registered and client reference. |

International services invoice | Bills services supplied to or from overseas customers. | Services | true | Determine place of supply, customer status, VAT number, reverse charge wording, currency and exchange rate if needed. |

Foreign currency invoice | Bills in a currency other than sterling. | Goods and services | true | Show currency, VAT in sterling where required, exchange rate basis, payment account and bank charges responsibility. |

Retention of title invoice | Bills goods while preserving seller ownership until payment under contract terms. | Goods | true | Reference retention of title terms, delivery note, goods description, VAT, payment deadline and repossession rights if contracted. |

After correction | ||||

Returns credit invoice | Credits goods returned by the customer after a sales invoice was issued. | Credit adjustment | true | Link to return authorisation and original invoice show quantities returned, restocking fees and VAT credit. |

Discount credit note | Applies a post-sale discount or rebate to a previous invoice. | Credit adjustment | true | State discount basis, original invoice, net reduction, VAT reduction and whether it is settlement discount or volume rebate. |

Debit memo invoice | Adds charges not included in an original invoice, often internal terminology for a debit note. | Credit adjustment | true | Use clear numbering, reason, original reference, VAT treatment and due date for the added amount. |

After supply | ||||

Tax receipt | Provides VAT evidence for a small purchase where a full invoice is not issued. | Goods and services | false | For VAT recovery, it must contain sufficient simplified VAT invoice details and be retained with purchase records. |

At payment request | ||||

Partial invoice | Bills part of an order or contract separately from the remaining balance. | Goods and services | true | State what proportion is invoiced, remaining balance, prior payments, VAT and related order or contract reference. |

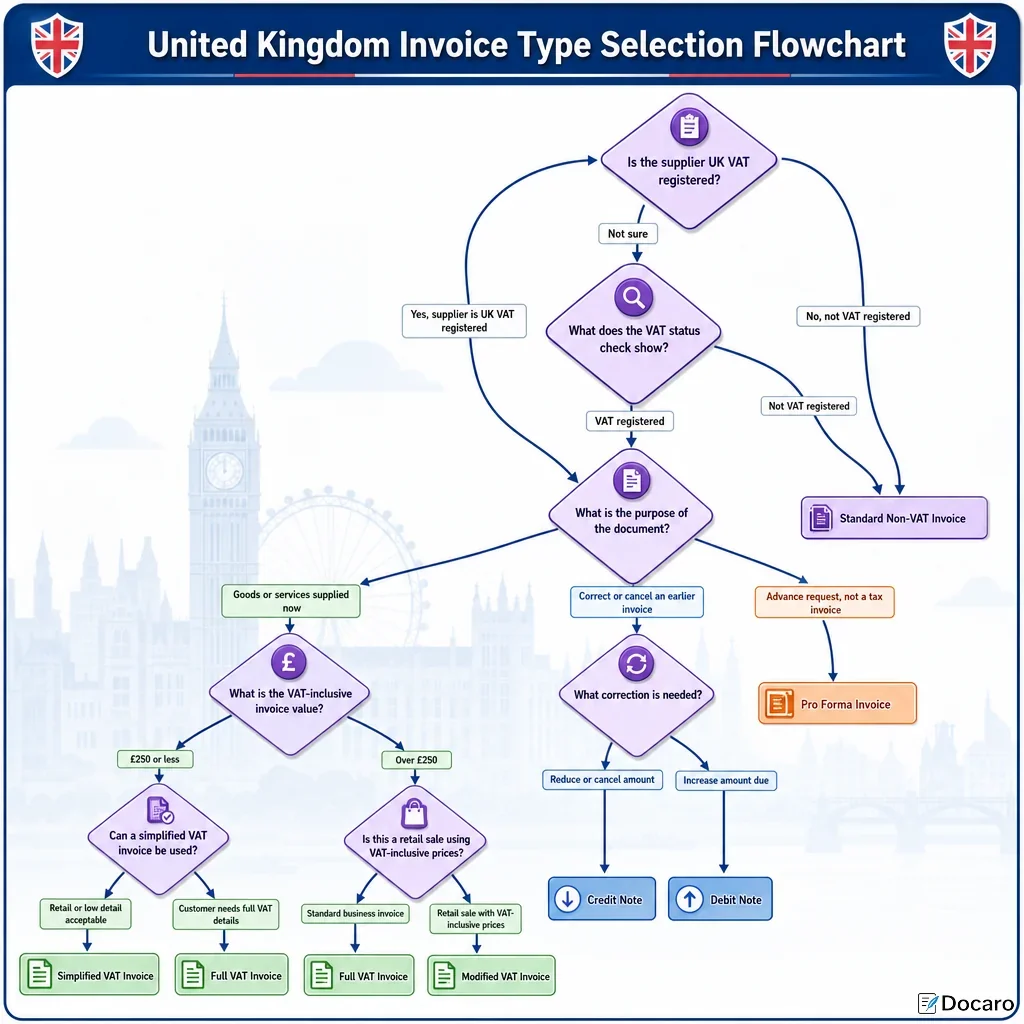

Which Invoice Type Should A UK Business Use?

Use a VAT invoice or modified VAT invoice where the supply is taxable and the customer needs VAT evidence. Use a simplified VAT invoice only for qualifying lower-value retail supplies, and use a VAT credit note or VAT debit note where the VAT position changes after invoicing.

When Is An Invoice Not A Demand For Payment?

A pro forma invoice is normally issued before supply or payment and should be clearly marked as not being a VAT invoice. It is commonly used for quotations, customs, or advance approval, but it should not be treated as the final tax invoice.

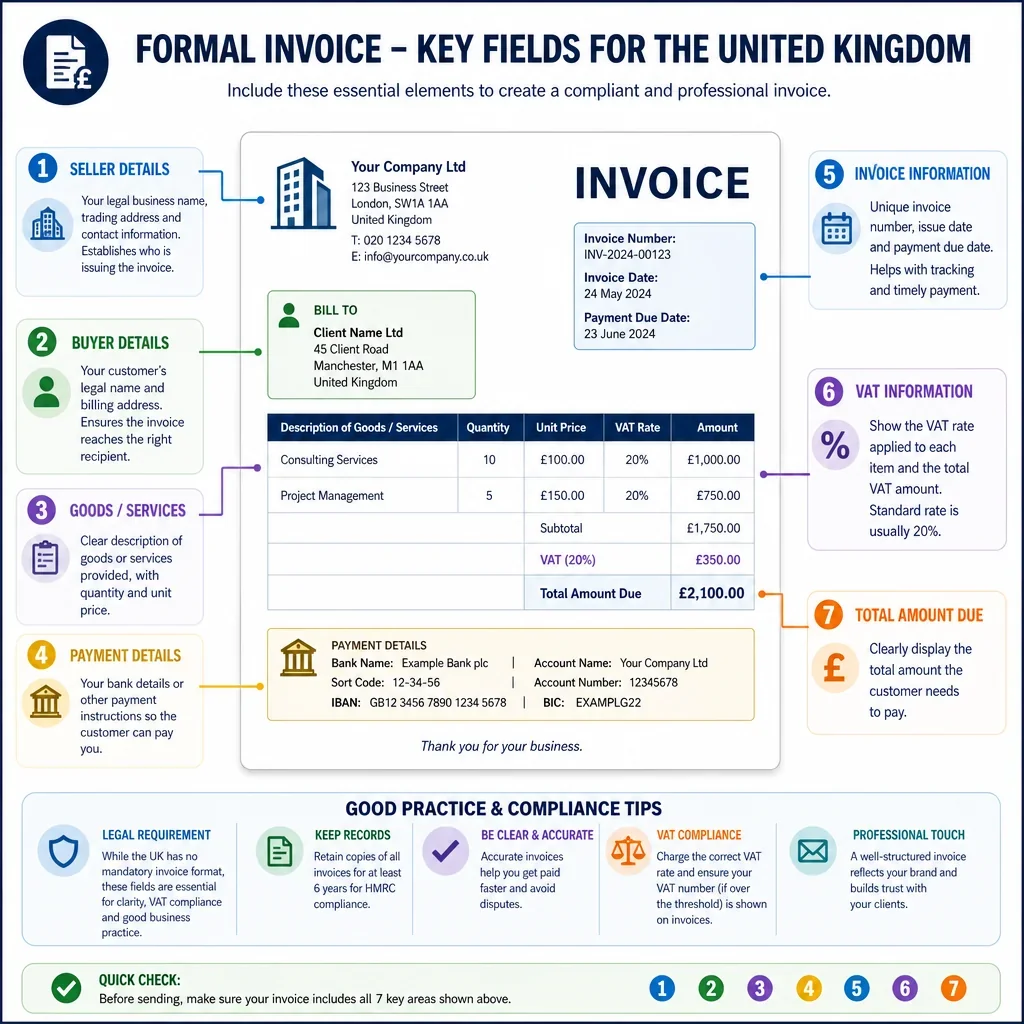

What Details Matter Most On UK Invoices?

- Sequential numbering is expected for formal sales invoices and VAT invoices; credit notes and debit notes should also be identifiable and link to the original invoice where relevant.

- VAT invoices must include required VAT details such as the supplier VAT number, tax point, VAT rate and amount, and sufficient description of the goods or services.

- Recurring and subscription invoices should state the billing period, payment terms, VAT treatment, and cancellation or contract reference where useful.

- Retention, interim, and final invoices used in construction and professional services should clearly state the valuation period, contract basis, previous payments, deductions, retention, and balance due.

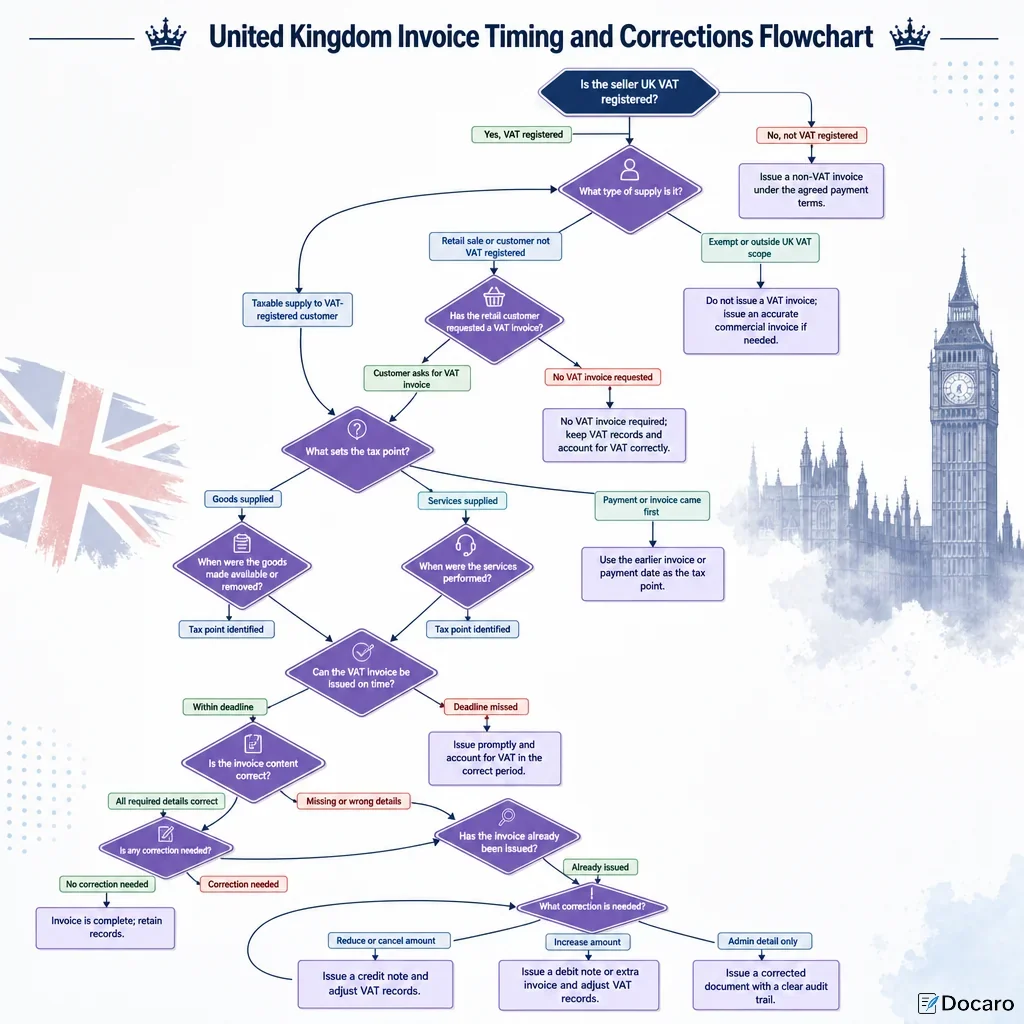

How Do Corrections Work For UK Invoices?

Do not usually delete or overwrite an issued invoice. If the amount is reduced, issue a credit note; if the amount is increased, issue a debit note or additional invoice. For VAT, correction documents should preserve an audit trail and refer back to the original invoice.

FAQs

You Might Also Be Interested In