UK ESG Reporting Frameworks And Standards

Created:

Understand key UK ESG reporting frameworks and standards and how they support transparent, consistent disclosures. This dataset is useful for comparing requirements, identifying relevant guidance, and preparing stronger ESG reports. For broader context, explore the AI Generated ESG Report for use in the United Kingdom category page.

Framework Name | Scope | Purpose | Application Status | Applicable Organisations | Key ESG Themes | Reporting Frequency | Effective Date |

|---|---|---|---|---|---|---|---|

Regulation | |||||||

Companies Act 2006 Strategic Report Requirements | United Kingdom | Requires strategic reporting on business model, risks, KPIs and non-financial matters. | Mandatory | UK companies required to prepare a strategic report. | Business model, principal risks, KPIs, employees, environment, social matters. | Annual. | 2013-10-01 |

Non-Financial and Sustainability Information Statement | United Kingdom | Requires large public-interest entities to report environmental, employee, social, human rights and anti-corruption matters. | Mandatory | Large traded companies, banks, insurers and other public-interest entities meeting thresholds. | Environment, employees, social matters, human rights, anti-bribery, diversity. | Annual. | 2017-01-01 |

Companies Climate-Related Financial Disclosure Regulations 2022 | United Kingdom | Requires TCFD-aligned climate governance, risk, strategy, metrics and targets disclosures. | Mandatory | Large UK companies and LLPs meeting turnover and employee thresholds. | Climate governance, transition risk, physical risk, metrics, targets. | Annual. | 2022-04-06 |

Streamlined Energy and Carbon Reporting | United Kingdom | Requires energy use, greenhouse gas emissions and efficiency action disclosures. | Mandatory | Quoted companies, large unquoted companies and large LLPs. | Energy use, greenhouse gas emissions, intensity ratios, efficiency measures. | Annual. | 2019-04-01 |

Mandatory Greenhouse Gas Emissions Reporting for Quoted Companies | United Kingdom | Requires quoted companies to disclose annual greenhouse gas emissions in directorsu0027 reports. | Mandatory | UK quoted companies. | Greenhouse gas emissions, methodology, intensity ratio. | Annual. | 2013-10-01 |

FCA Listing Rules TCFD-Aligned Climate Disclosures | United Kingdom | Requires listed issuers to state consistency with TCFD recommendations and explain gaps. | Comply or Explain | UK premium and standard listed commercial companies. | Climate governance, strategy, risk management, metrics and targets. | Annual. | 2021-01-01 |

FCA ESG Sourcebook Climate-Related Disclosures | United Kingdom | Requires entity and product-level TCFD-aligned disclosures by in-scope financial firms. | Mandatory | Asset managers, life insurers and FCA-regulated pension providers. | Climate risk, financed emissions, portfolio metrics, products. | Annual. | 2022-01-01 |

UK Sustainability Disclosure Requirements and Investment Labels | United Kingdom | Creates sustainability labels, naming, marketing and disclosure rules for investment products. | Mandatory | UK asset managers and distributors of sustainability-related investment products. | Fund labels, sustainability objectives, consumer disclosures, anti-greenwashing. | Pre-contractual, ongoing and annual product reports. | 2024-07-31 |

FCA Anti-Greenwashing Rule | United Kingdom | Requires sustainability claims by FCA-authorised firms to be fair, clear and not misleading. | Mandatory | FCA-authorised firms communicating sustainability claims. | Green claims, evidence, clarity, fair presentation. | Applies to communications on an ongoing basis. | 2024-05-31 |

Governance Code | |||||||

UK Corporate Governance Code | United Kingdom | Sets board leadership, controls, remuneration and accountability principles for listed companies. | Comply or Explain | Premium listed companies and other adopters. | Board leadership, controls, stakeholder engagement, remuneration, audit. | Annual. | 2025-01-01 |

Wates Corporate Governance Principles for Large Private Companies | United Kingdom | Provides governance principles for large private companies reporting governance arrangements. | Market Expected | Large private companies subject to corporate governance statement requirements. | Purpose, board composition, responsibilities, opportunity, risk, remuneration, stakeholders. | Annual. | 2019-01-01 |

Regulation | |||||||

Large Company Corporate Governance Statement Requirements | United Kingdom | Requires qualifying large companies to report corporate governance arrangements. | Mandatory | Very large UK companies meeting employee and financial thresholds. | Governance arrangements, board oversight, stakeholder engagement. | Annual. | 2019-01-01 |

Section 172 Statement | United Kingdom | Requires directors to explain how they considered stakeholder and long-term factors. | Mandatory | Large UK companies preparing a strategic report. | Stakeholders, employees, suppliers, community, environment, long-term consequences. | Annual. | 2019-01-01 |

Governance Code | |||||||

UK Stewardship Code | United Kingdom | Sets investor stewardship reporting expectations across ESG and governance outcomes. | Voluntary | Asset owners, asset managers and service providers. | Stewardship, engagement, voting, climate, governance, outcomes. | Annual submission. | 2020-01-01 |

Regulation | |||||||

Occupational Pension Schemes Climate Governance and Reporting Regulations | United Kingdom | Requires trustees to govern and report climate-related risks and opportunities. | Mandatory | Large occupational pension schemes and authorised master trusts. | Climate governance, scenario analysis, risk management, metrics, targets. | Annual TCFD report. | 2021-10-01 |

Modern Slavery Act 2015 Transparency in Supply Chains Statement | United Kingdom | Requires annual statement on steps to address slavery and trafficking in supply chains. | Mandatory | Commercial organisations carrying on business in the UK with turnover of at least £36m. | Modern slavery, human rights, supply chain due diligence, training. | Annual. | 2015-10-29 |

Gender Pay Gap Reporting Regulations | United Kingdom | Requires employers to publish gender pay and bonus gap data. | Mandatory | UK employers with 250 or more employees, subject to specific rules. | Workforce equality, pay, bonus gaps, gender representation. | Annual. | 2017-04-06 |

Payment Practices and Performance Reporting | United Kingdom | Requires large companies and LLPs to report payment practices affecting suppliers. | Mandatory | Large UK companies and LLPs meeting size thresholds. | Supplier treatment, payment terms, supply chain fairness. | Twice yearly. | 2017-04-06 |

Voluntary Guidance | |||||||

Bribery Act 2010 Adequate Procedures Guidance | United Kingdom | Guides anti-bribery procedures relevant to governance and ethics disclosures. | Market Expected | Commercial organisations exposed to bribery risk in or connected with the UK. | Anti-bribery, corruption risk, ethics, controls, third parties. | Ongoing controls reported as relevant. | 2011-07-01 |

Disclosure Framework | |||||||

Task Force on Climate-related Financial Disclosures Recommendations | International | Framework for climate-related financial risk disclosures across governance, strategy, risk and metrics. | Market Expected | Companies, investors, banks, insurers and asset owners. | Climate risk, governance, strategy, scenario analysis, metrics, targets. | Annual or mainstream financial reporting cycle. | 2017-06-29 |

Reporting Standard | |||||||

IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information | International | Requires material sustainability-related financial information for investors across all ESG topics. | Market Expected | Companies preparing investor-focused sustainability disclosures. | Material sustainability risks, governance, strategy, risk management, metrics. | Annual, with financial statements. | 2024-01-01 |

IFRS S2 Climate-related Disclosures | International | Sets investor-focused climate disclosure requirements aligned with TCFD structure. | Market Expected | Companies reporting climate-related financial risks and opportunities. | Climate governance, transition plans, Scope 1-3 emissions, scenario analysis. | Annual, with financial statements. | 2024-01-01 |

UK Sustainability Reporting Standards | United Kingdom | Proposed UK-endorsed ISSB-based sustainability disclosure standards. | Market Expected | Potential future UK companies and financial market participants, subject to decisions. | Sustainability-related financial risks, climate, governance, metrics, targets. | Expected annual reporting if adopted. | 2025-06-25 |

Disclosure Framework | |||||||

UK Transition Plan Taskforce Disclosure Framework | United Kingdom | Framework for credible climate transition plans and implementation disclosures. | Market Expected | Companies and financial institutions preparing transition plans. | Net zero strategy, implementation, engagement, governance, metrics. | Periodic plan updates with annual progress reporting. | 2023-10-09 |

Reporting Standard | |||||||

GHG Protocol Corporate Accounting and Reporting Standard | International | Standard for measuring and reporting corporate Scope 1 and Scope 2 emissions. | Market Expected | Organisations calculating operational greenhouse gas emissions. | Greenhouse gas accounting, organisational boundaries, Scope 1 and 2 emissions. | Annual inventory cycle. | 2004-03-01 |

GHG Protocol Corporate Value Chain Scope 3 Standard | International | Standard for measuring indirect value chain greenhouse gas emissions. | Market Expected | Companies reporting supply chain and product-related emissions. | Scope 3 emissions, suppliers, use of sold products, value chain. | Annual inventory cycle. | 2011-10-01 |

GRI Standards | International | Impact-focused sustainability reporting standards covering economic, environmental and social topics. | Voluntary | Organisations reporting sustainability impacts to broad stakeholders. | Impacts, materiality, emissions, labour, human rights, governance, communities. | Annual or regular sustainability reporting cycle. | 2023-01-01 |

SASB Standards | International | Industry-specific sustainability disclosure topics and metrics for investors. | Market Expected | Companies seeking sector-specific financially material ESG metrics. | Sector metrics, financial materiality, climate, workforce, product governance. | Annual. | 2018-11-01 |

Disclosure Framework | |||||||

CDP Climate, Forests and Water Questionnaires | International | Investor and customer disclosure system for climate, forests and water impacts. | Market Expected | Companies responding to investor, lender or customer disclosure requests. | Climate, water security, deforestation, supply chains, targets. | Annual questionnaire cycle. | 2024-01-01 |

Voluntary Guidance | |||||||

Science Based Targets Initiative Corporate Net-Zero Standard | International | Guidance for setting validated near-term and net-zero emissions reduction targets. | Voluntary | Companies setting science-based climate targets. | Net zero, emissions reductions, target validation, Scope 1-3 emissions. | Annual progress disclosure target review at least every five years. | 2021-10-28 |

Disclosure Framework | |||||||

Taskforce on Nature-related Financial Disclosures Recommendations | International | Framework for nature-related dependencies, impacts, risks and opportunities disclosures. | Voluntary | Companies and financial institutions with nature-related exposures. | Biodiversity, nature risk, dependencies, impacts, locations, metrics. | Annual or mainstream reporting cycle. | 2023-09-18 |

Regulation | |||||||

Corporate Sustainability Reporting Directive | European Union | Expands EU sustainability reporting and assurance requirements using ESRS. | Mandatory | Large EU companies, listed SMEs and some non-EU groups with EU activity. | Double materiality, climate, workforce, value chain, governance, assurance. | Annual. | 2023-01-05 |

Reporting Standard | |||||||

European Sustainability Reporting Standards | European Union | Detailed mandatory sustainability standards under CSRD. | Mandatory | Companies in scope of CSRD reporting. | Climate, pollution, water, biodiversity, workforce, consumers, business conduct. | Annual. | 2024-01-01 |

Regulation | |||||||

EU Taxonomy Regulation | European Union | Classifies environmentally sustainable economic activities and related disclosures. | Mandatory | EU financial market participants and large companies subject to EU reporting. | Sustainable activities, climate mitigation, adaptation, environmental objectives. | Annual. | 2020-07-12 |

Sustainable Finance Disclosure Regulation | European Union | Requires sustainability disclosures by financial market participants and advisers. | Mandatory | EU financial market participants and financial advisers relevant to UK cross-border firms. | Product disclosures, principal adverse impacts, sustainability risks, taxonomy alignment. | Pre-contractual, website and periodic disclosures. | 2021-03-10 |

Corporate Sustainability Due Diligence Directive | European Union | Requires human rights and environmental due diligence across chains of activities. | Mandatory | Large EU companies and certain non-EU companies with EU turnover. | Human rights, environment, supply chain due diligence, transition plans. | Annual statement unless covered by CSRD reporting. | 2024-07-25 |

Disclosure Framework | |||||||

UN Global Compact Communication on Progress | International | Annual disclosure on implementation of UN Global Compact Ten Principles. | Voluntary | UN Global Compact participant companies and organisations. | Human rights, labour, environment, anti-corruption, SDGs. | Annual. | 2023-03-27 |

Voluntary Guidance | |||||||

OECD Guidelines for Multinational Enterprises on Responsible Business Conduct | International | Responsible business conduct guidance on due diligence and ESG impacts. | Voluntary | Multinational enterprises and companies with international value chains. | Due diligence, human rights, labour, environment, corruption, disclosure. | Ongoing due diligence reported as relevant. | 2023-06-08 |

Disclosure Framework | |||||||

UN Guiding Principles Reporting Framework | International | Framework for reporting human rights governance, policies and due diligence. | Voluntary | Companies reporting human rights risks and impacts. | Human rights, salient risks, due diligence, grievance mechanisms. | Annual or regular sustainability reporting cycle. | 2015-02-24 |

Reporting Standard | |||||||

ISO 14001 Environmental Management Systems | International | Management system standard supporting environmental performance evidence in ESG reports. | Voluntary | Organisations operating environmental management systems or seeking certification. | Environmental management, compliance, objectives, lifecycle impacts, improvement. | Certification cycle with periodic surveillance audits. | 2015-09-15 |

Voluntary Guidance | |||||||

ISO 26000 Social Responsibility Guidance | International | Guidance on integrating social responsibility into governance and operations. | Voluntary | Organisations seeking broad social responsibility guidance. | Governance, human rights, labour, environment, fair operating practices, consumers, communities. | No fixed reporting frequency. | 2010-11-01 |

B Corp Certification Standards | International | Certification framework assessing governance, workers, community, environment and customers. | Voluntary | Companies seeking independent social and environmental performance certification. | Governance, workers, community, environment, customers, impact management. | Recertification every three years. | 2025-04-08 |

CMA Green Claims Code | United Kingdom | Guidance on making truthful, clear and substantiated environmental claims. | Market Expected | UK businesses making environmental claims to consumers or customers. | Green claims, substantiation, lifecycle impacts, consumer protection. | Applies whenever environmental claims are made. | 2021-09-20 |

CAP and ASA Environmental Claims Guidance | United Kingdom | Advertising guidance on environmental claims under UK advertising codes. | Market Expected | Businesses making ESG or environmental claims in UK advertising. | Advertising, green claims, evidence, omissions, qualifications. | Applies to marketing communications on an ongoing basis. | 2023-06-23 |

PRA Supervisory Statement SS3/19 Enhancing Banksu0027 and Insurersu0027 Approaches to Climate-related Financial Risks | United Kingdom | Sets supervisory expectations for managing climate-related financial risks. | Market Expected | PRA-regulated banks, building societies and insurers. | Climate financial risk, governance, risk management, scenario analysis, disclosure. | Ongoing supervisory review. | 2019-04-15 |

Disclosure Framework | |||||||

NHS Evergreen Sustainable Supplier Assessment | Sector Specific | Assessment tool for supplier sustainability maturity in NHS procurement. | Market Expected | Suppliers to NHS organisations and healthcare procurement teams. | Net zero, carbon reduction, supply chain, social value, sustainability governance. | Updated as part of supplier assessment and procurement cycles. | 2023-06-05 |

Voluntary Guidance | |||||||

UK Public Procurement Social Value Model | United Kingdom | Model for evaluating social value in central government procurement. | Market Expected | Central government contracting authorities and bidders for public contracts. | Social value, jobs, skills, climate, equal opportunity, wellbeing. | Applied during procurement and contract management. | 2021-01-01 |

PPN 06/21 Carbon Reduction Plans | United Kingdom | Requires suppliers bidding for major central government contracts to publish carbon reduction plans. | Market Expected | Suppliers bidding for central government contracts above £5 million per year. | Carbon reduction, net zero, Scope 1-3 emissions, procurement. | Updated at least annually. | 2021-09-30 |

Reporting Standard | |||||||

BREEAM Building Sustainability Assessment | Sector Specific | Sustainability assessment method for buildings and infrastructure assets. | Voluntary | Property developers, owners, occupiers and construction projects. | Buildings, energy, materials, water, health, land use, pollution. | Project assessment and certification cycle. | 1990-01-01 |

Disclosure Framework | |||||||

GRESB Real Estate Assessment | Sector Specific | Investor benchmark for ESG performance of real estate portfolios and assets. | Market Expected | Real estate companies, funds, developers and asset managers. | Real estate, energy, emissions, water, waste, tenants, governance. | Annual assessment. | 2024-04-01 |

Voluntary Guidance | |||||||

Equator Principles | International | Risk management framework for environmental and social risks in project finance. | Voluntary | Financial institutions financing projects and infrastructure. | Project finance, environmental and social risk, communities, biodiversity, human rights. | Annual implementation reporting by adopters. | 2020-10-01 |

Disclosure Framework | |||||||

Principles for Responsible Investment Reporting Framework | International | Responsible investment reporting and assessment framework for PRI signatories. | Voluntary | Asset owners, investment managers and service providers that are PRI signatories. | Responsible investment, stewardship, ESG integration, climate, human rights. | Annual reporting cycle for signatories. | 2023-01-01 |

Regulation | |||||||

FCA Consumer Duty | Sector Specific | Requires financial firms to deliver good consumer outcomes, relevant to social and governance reporting. | Mandatory | FCA-regulated firms serving retail customers. | Consumer outcomes, fair value, governance, vulnerable customers, communications. | Ongoing monitoring with at least annual board review. | 2023-07-31 |

Voluntary Guidance | |||||||

Living Wage Foundation Real Living Wage Accreditation | United Kingdom | Accreditation for employers paying the independently calculated real Living Wage. | Voluntary | UK employers seeking workforce pay accreditation. | Fair pay, workforce, contractors, social impact. | Annual rate update and accreditation maintenance. | 2011-01-01 |

Which ESG Reporting Frameworks Matter Most For UK Organisations?

UK ESG reporting is not governed by one single rulebook. A credible ESG Report usually needs to map together mandatory UK company law disclosures, FCA listing rules, governance codes and widely used international sustainability standards.

- Quoted and large UK companies should prioritise Companies Act strategic report requirements, Streamlined Energy and Carbon Reporting and mandatory climate-related financial disclosures.

- UK listed issuers should consider FCA climate disclosure rules, the UK Corporate Governance Code and the UK Stewardship Code where relevant to investors.

- Financial institutions and asset managers face additional ESG expectations under SDR, TCFD-aligned FCA sourcebook rules, PRA climate risk supervision and anti-greenwashing requirements.

- Groups with EU operations or value chains may also need to align UK reporting with CSRD, ESRS, EU Taxonomy and CSDDD requirements.

- Voluntary standards such as ISSB, GRI, SASB, TNFD, SBTi and GHG Protocol help make ESG Reports more comparable, investor-friendly and assurance-ready.

How Should A UK ESG Report Use These Frameworks?

A practical UK ESG Report should begin by identifying which disclosures are legally mandatory, then use recognised voluntary frameworks to fill gaps. Climate, energy, governance, workforce, human rights, supply chain due diligence and biodiversity are recurring themes across the dataset.

- Use legal requirements as the baseline: include mandatory UK narrative reporting, SECR and climate-related disclosures where applicable.

- Use international standards for structure: ISSB, GRI, GHG Protocol and TCFD terminology are commonly used to organise metrics, targets, risks and governance disclosures.

- Check investor-facing obligations: FCA rules, the UK Corporate Governance Code and stewardship expectations can affect listed companies and asset managers even where company law alone is not enough.

- Avoid unsupported green claims: the CMA Green Claims Code, FCA anti-greenwashing rule and ASA guidance mean ESG statements should be accurate, evidenced and not misleading.

Want to Generate Your own ESG Report?

Docaro AI can help you write your own ESG Report for use in the United Kingdom in minutes.

FAQs

The main ESG reporting frameworks relevant in the UK include TCFD-aligned climate disclosures, ISSB Standards, GRI Standards, SASB Standards, ESRS for EU-linked reporting, and the UK Companies Act strategic reporting requirements.

Show All FAQs

You Might Also Be Interested In

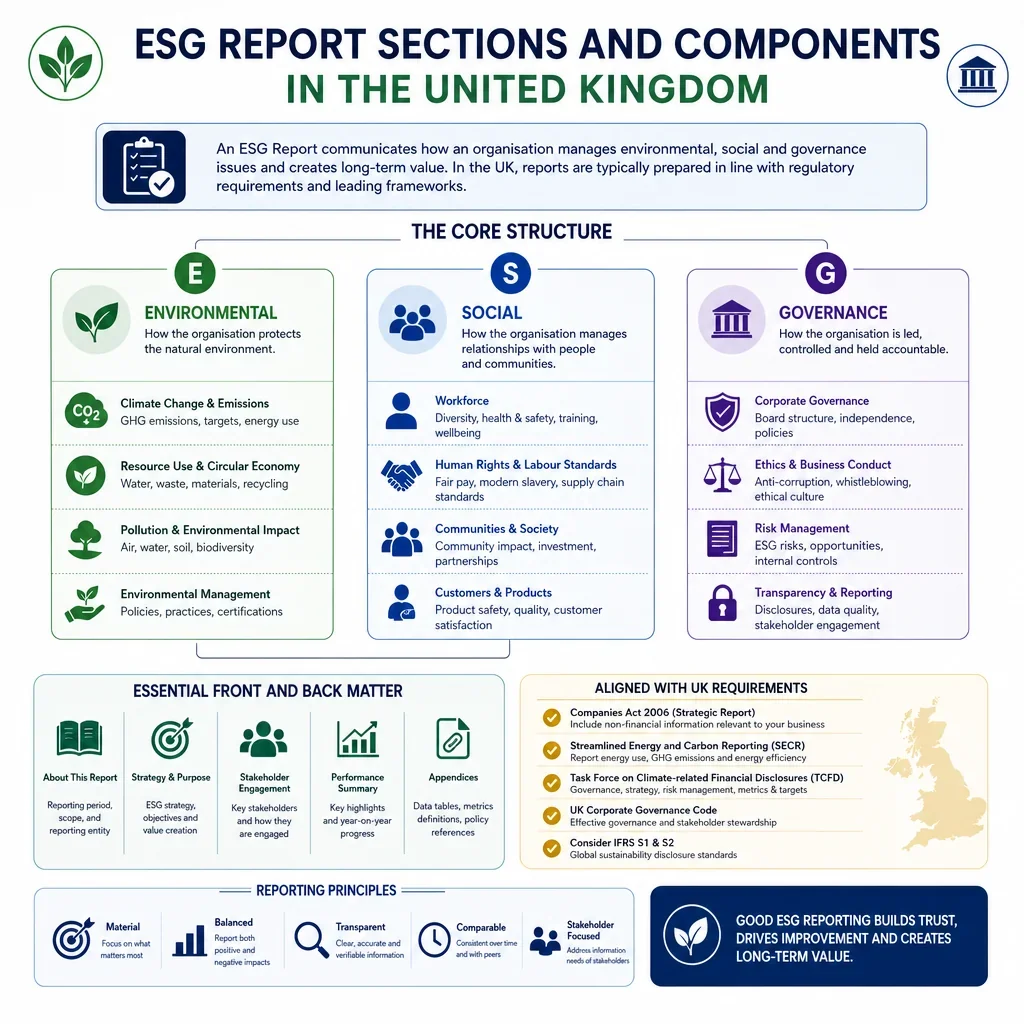

Explore ESG report sections and components in the United Kingdom, including key disclosures, structure, and reporting essentials.

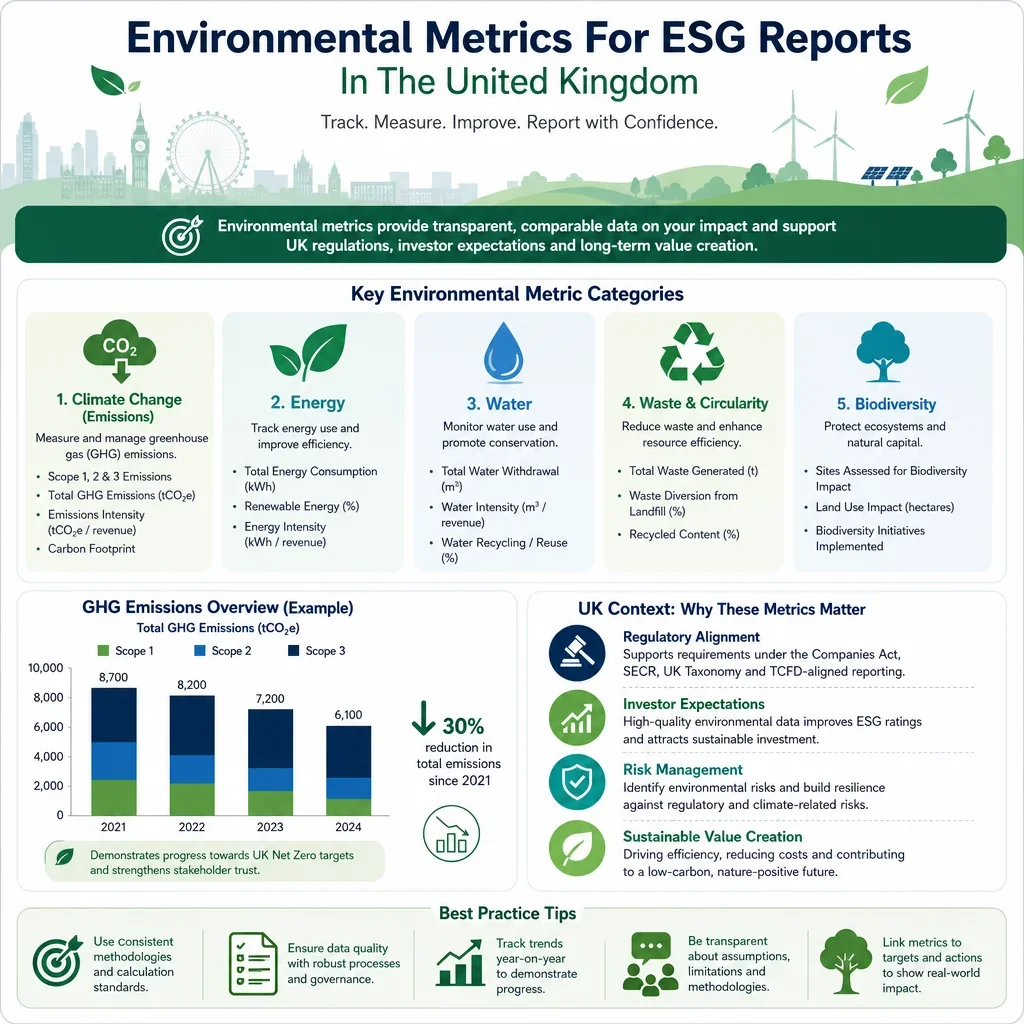

Environmental metrics for ESG reports in the United Kingdom, covering emissions, resource use, and sustainability insights.

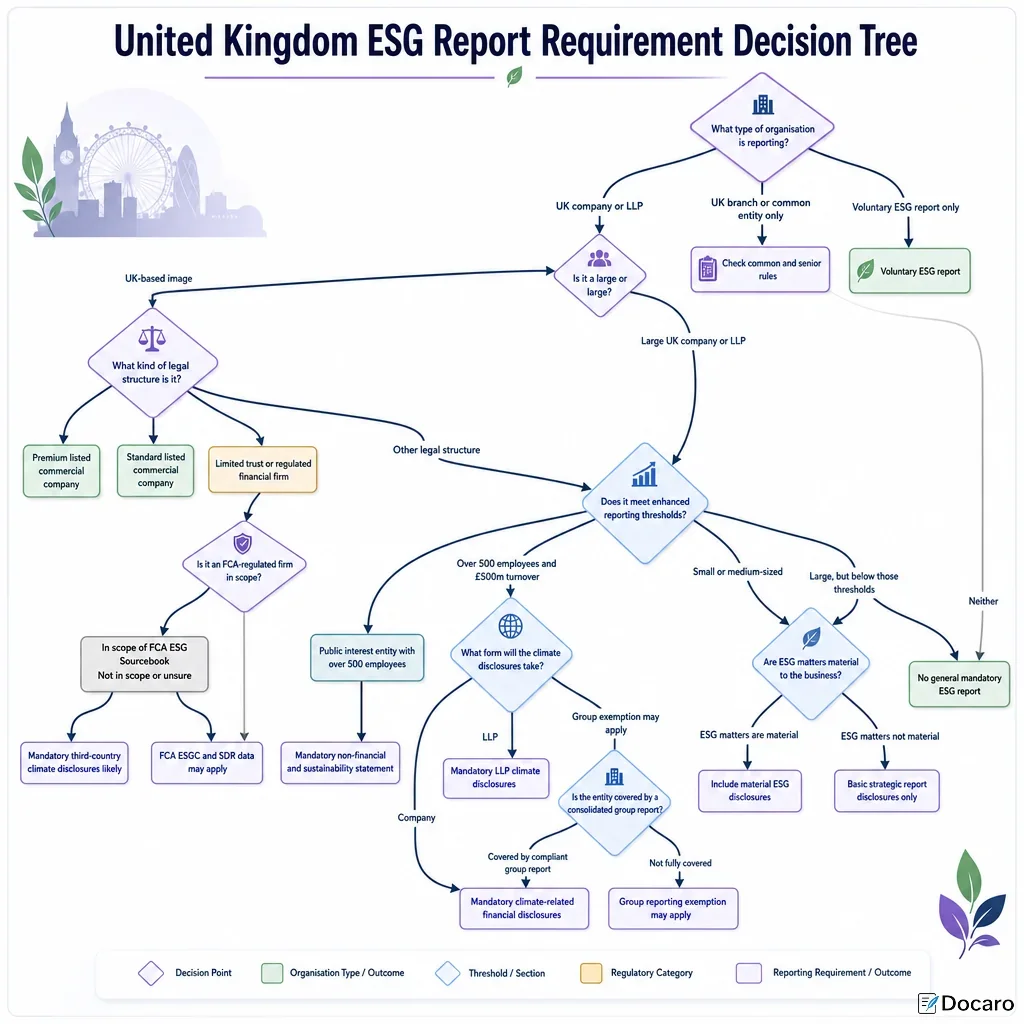

United Kingdom ESG report decision tree to help assess reporting requirements and support compliance planning.

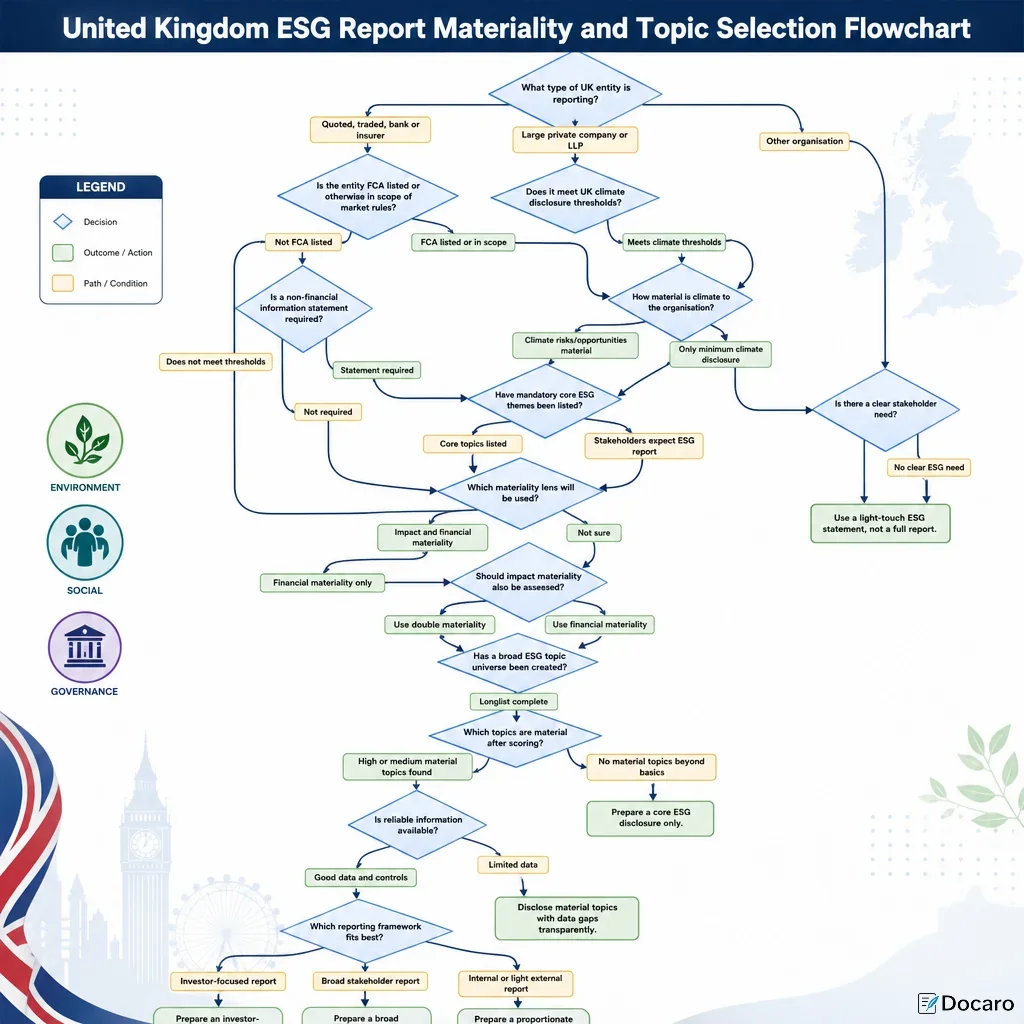

United Kingdom ESG report flowchart for materiality assessment and topic selection to support clearer, relevant sustainability reporting.