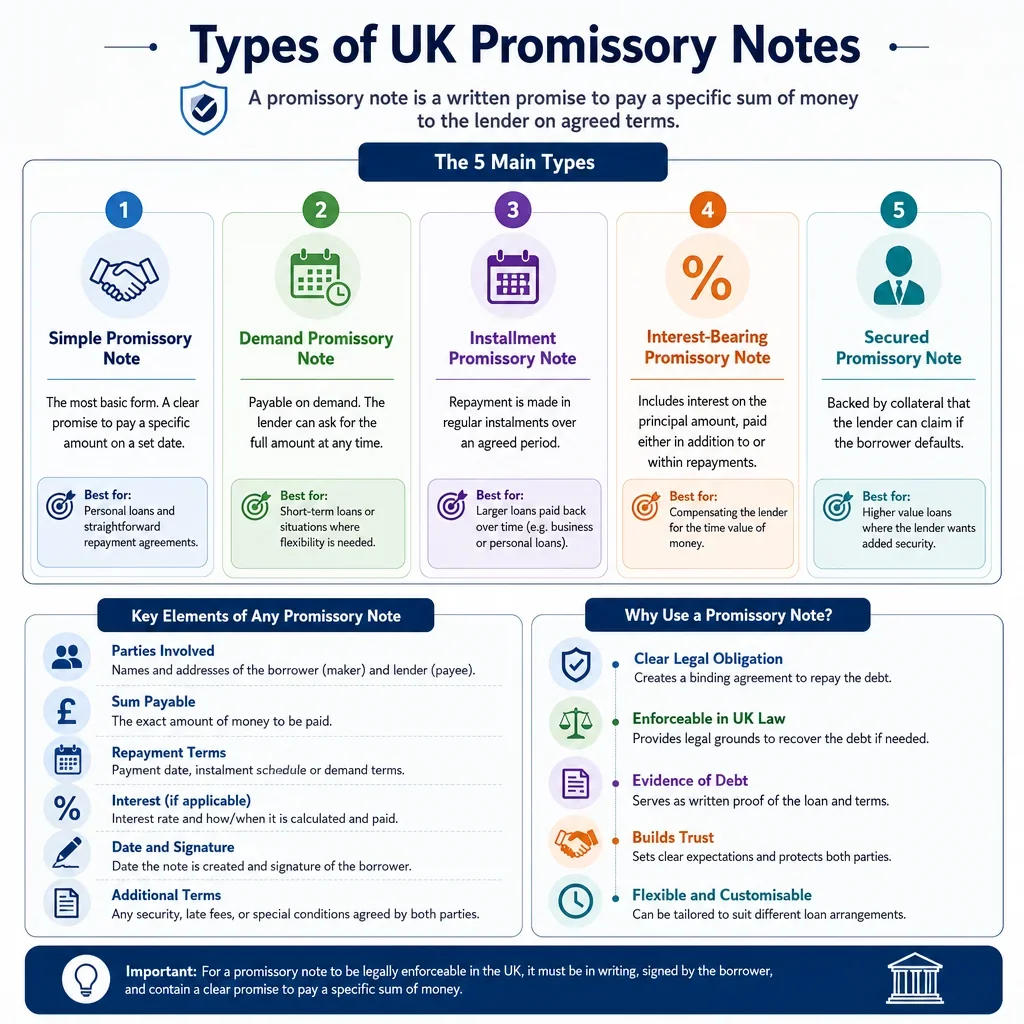

Types Of UK Promissory Notes

Typical Use Case | Repayment Structure | Interest Commonly Included | Typical Complexity | Common Clauses | Practical Considerations |

|---|---|---|---|---|---|

Fixed-Date Promissory Note | |||||

Personal loan Business loan Family or friends loan | Single lump sum | Sometimes | Low | Principal, fixed repayment date, interest, default, notices, governing law. | Best for a clear one-off debt where repayment date is certain. |

On-Demand Promissory Note | |||||

Personal loan Business loan Family or friends loan Short-term bridging arrangement | On demand | Sometimes | Medium | Demand procedure, repayment deadline after demand, interest, default, notices. | Borrower should understand repayment may be required at short notice. |

Instalment Promissory Note | |||||

Personal loan Business loan Asset purchase Family or friends loan | Instalments | Usually | Medium | Payment schedule, interest, late payment, default, acceleration, prepayment. | Needs a precise schedule and consequences for missed instalments. |

Interest-Free Promissory Note | |||||

Family or friends loan Personal loan | Single lump sum Instalments On demand | Rarely | Low | Principal, repayment date or schedule, no-interest wording, default, notices. | State expressly that no interest accrues to avoid later disputes. |

Interest-Bearing Promissory Note | |||||

Business loan Personal loan Asset purchase | Single lump sum Instalments Balloon payment | Usually | Medium | Interest rate, accrual method, payment dates, default interest, tax gross-up if needed. | Interest method and compounding should be clear and commercially realistic. |

Balloon Payment Promissory Note | |||||

Business loan Asset purchase Short-term bridging arrangement | Balloon payment | Usually | Medium | Interim payments, final balloon amount, interest, default, acceleration, prepayment. | Borrower needs a credible plan to fund the final large payment. |

Secured Promissory Note | |||||

Business loan Asset purchase Short-term bridging arrangement Personal loan | Single lump sum Instalments On demand Balloon payment | Usually | High | Security description, enforcement triggers, covenants, default, acceleration, release. | Company security may require Companies House registration to preserve priority. |

Unsecured Promissory Note | |||||

Personal loan Business loan Family or friends loan | Single lump sum Instalments On demand | Sometimes | Low | Principal, repayment terms, interest, default, costs, governing law. | Lender relies mainly on borrower creditworthiness and contractual remedies. |

Family Loan Promissory Note | |||||

Family or friends loan Personal loan | Single lump sum Instalments Flexible repayment | Rarely | Low | Amount, repayment expectations, interest position, forgiveness, default, informal notices. | Clear written terms help distinguish a loan from a gift. |

Friends Loan Promissory Note | |||||

Family or friends loan Personal loan | Single lump sum Instalments Flexible repayment | Rarely | Low | Loan amount, repayment date, no-gift wording, interest, default, evidence of payment. | Record bank transfers and communications to reduce evidential disputes. |

Business Loan Promissory Note | |||||

Business loan | Single lump sum Instalments On demand Balloon payment | Usually | Medium | Purpose, interest, repayment, default, financial covenants, costs, governing law. | Check company authority, board approval, and any existing debt restrictions. |

Director Loan Promissory Note | |||||

Business loan Other | Single lump sum Instalments On demand Flexible repayment | Sometimes | Medium | Account balance, repayment, interest, set-off, board approval, tax responsibility. | Director loans can create UK tax and company approval issues. |

Shareholder Loan Promissory Note | |||||

Business loan | Single lump sum Instalments On demand Flexible repayment | Sometimes | Medium | Subordination, repayment priority, interest, conversion option, default, transfer. | Align terms with shareholder agreements and existing lender restrictions. |

Convertible Promissory Note | |||||

Business loan Other | Single lump sum Balloon payment | Usually | High | Conversion trigger, valuation cap, discount, interest, maturity, investor rights. | Company articles, pre-emption rights, and securities law should be checked. |

Bridging Finance Promissory Note | |||||

Short-term bridging arrangement Business loan Asset purchase | Single lump sum Balloon payment On demand | Usually | High | Short maturity, interest, arrangement fees, default, exit source, security. | Should identify the repayment exit, such as sale proceeds or refinancing. |

Asset Purchase Promissory Note | |||||

Asset purchase Business loan Personal loan | Single lump sum Instalments Balloon payment | Usually | Medium | Purchase price balance, instalments, title, security, default, repossession rights. | Coordinate note terms with the sale contract and ownership transfer. |

Vehicle Purchase Promissory Note | |||||

Asset purchase Personal loan | Instalments Balloon payment Single lump sum | Sometimes | Medium | Vehicle details, price balance, instalments, insurance, default, title/security. | Vehicle ownership, registration, insurance, and security should be consistent. |

Equipment Purchase Promissory Note | |||||

Asset purchase Business loan | Instalments Balloon payment Single lump sum | Usually | Medium | Equipment description, repayment schedule, maintenance, insurance, default, security. | Identify equipment precisely and confirm any retention or security rights. |

Property Deposit Promissory Note | |||||

Personal loan Family or friends loan Short-term bridging arrangement | Single lump sum On demand Balloon payment | Sometimes | Medium | Purpose, repayment trigger, interest, source of repayment, default, evidence of funds. | Mortgage lenders may require disclosure of borrowed deposit funds. |

Rent Arrears Promissory Note | |||||

Personal loan Other | Instalments Single lump sum | Rarely | Medium | Arrears amount, repayment plan, tenancy preservation, default, no waiver wording. | Should not conflict with tenancy rights or possession procedures. |

Settlement Promissory Note | |||||

Other Business loan Personal loan | Single lump sum Instalments | Sometimes | Medium | Settlement sum, payment dates, release link, confidentiality, default, costs. | Must align with any settlement agreement and release conditions. |

Trade Credit Promissory Note | |||||

Business loan Other | Single lump sum Instalments | Usually | Medium | Invoice references, repayment, statutory interest, costs, default, retention of rights. | Commercial debts may attract statutory late payment interest and recovery costs. |

Revolving Promissory Note | |||||

Business loan Personal loan Other | Flexible repayment On demand | Usually | High | Credit limit, drawdowns, repayments, interest, availability period, termination. | Needs accurate records of advances, repayments, and available balance. |

Line Of Credit Promissory Note | |||||

Business loan Other | Flexible repayment On demand | Usually | High | Facility limit, utilisation requests, interest periods, fees, repayment, cancellation. | Better for ongoing borrowing than a single fixed advance. |

Master Promissory Note | |||||

Business loan Other | Flexible repayment Instalments On demand | Usually | High | Framework terms, advance confirmations, interest, repayment, default, amendments. | Useful where repeated loans need consistent terms and separate drawdown records. |

Demand Loan Promissory Note With Interest | |||||

Business loan Short-term bridging arrangement Personal loan | On demand | Usually | Medium | Demand mechanics, daily interest, default interest, repayment deadline, notices. | Borrower should negotiate minimum notice before repayment becomes due. |

Promissory Note Payable To Order | |||||

Business loan Other | Single lump sum On demand | Sometimes | High | Payee order wording, amount certain, payment time, endorsement, governing law. | Transferability can affect who may enforce payment. |

Promissory Note Payable To Bearer | |||||

Other Business loan | Single lump sum On demand | Sometimes | High | Bearer payment wording, amount certain, maturity, presentation, replacement limits. | High loss and misuse risk because possession may support enforcement. |

Joint Borrower Promissory Note | |||||

Personal loan Business loan Family or friends loan | Single lump sum Instalments On demand | Sometimes | Medium | Joint and several liability, notices, repayments, default, borrower representations. | Clarify whether each borrower is liable for the whole debt. |

Guaranteed Promissory Note | |||||

Business loan Personal loan Asset purchase Family or friends loan | Single lump sum Instalments On demand Balloon payment | Usually | High | Guarantee, indemnity, demand on guarantor, continuing security, guarantor notices. | Guarantees usually need careful execution and independent advice is prudent. |

Subordinated Promissory Note | |||||

Business loan Other | Single lump sum Balloon payment Instalments | Usually | High | Payment subordination, turnover, standstill, senior debt consent, default. | Repayment may be blocked until senior creditors are paid or consent. |

Deferred Consideration Promissory Note | |||||

Asset purchase Business loan Other | Single lump sum Instalments Balloon payment | Sometimes | High | Deferred price, conditions, set-off, warranties link, interest, default. | Should match sale agreement conditions and any set-off rights. |

Employee Loan Promissory Note | |||||

Personal loan Other | Instalments Single lump sum Flexible repayment | Sometimes | Medium | Payroll deductions, interest, termination repayment, tax reporting, consent. | Low-interest employee loans can create taxable benefit reporting obligations. |

Private Education Loan Promissory Note | |||||

Personal loan Family or friends loan Other | Instalments Single lump sum Flexible repayment | Rarely | Low | Education purpose, repayment start date, grace period, interest, default. | Avoid confusion with statutory student loans and state repayment triggers. |

Debt Consolidation Promissory Note | |||||

Personal loan Business loan Other | Instalments Single lump sum | Usually | Medium | Existing debts, novation or replacement, interest, schedule, releases, default. | Specify whether old debts are discharged or merely rescheduled. |

Refinancing Promissory Note | |||||

Business loan Personal loan Short-term bridging arrangement | Single lump sum Instalments Balloon payment | Usually | Medium | Existing debt reference, payoff, new rate, maturity, security continuity, releases. | Confirm whether existing security continues, is released, or must be re-registered. |

Prepayable Promissory Note | |||||

Personal loan Business loan Asset purchase | Single lump sum Instalments Balloon payment | Sometimes | Medium | Voluntary prepayment, notice, break costs, interest adjustment, allocation of payments. | State whether early repayment fees or minimum interest apply. |

No-Prepayment Promissory Note | |||||

Business loan Asset purchase Other | Single lump sum Instalments Balloon payment | Usually | Medium | Prepayment prohibition, lender consent, interest protection, default, maturity. | Borrower loses flexibility if cheaper refinancing becomes available. |

Variable Rate Promissory Note | |||||

Business loan Personal loan Short-term bridging arrangement | Instalments Single lump sum Balloon payment | Usually | Medium | Reference rate, margin, rate changes, interest periods, fallback rate. | Use a clear reference rate such as Bank Rate and define changes. |

Fixed Rate Promissory Note | |||||

Personal loan Business loan Asset purchase Family or friends loan | Single lump sum Instalments Balloon payment | Usually | Low | Fixed rate, accrual basis, interest payment dates, default interest, maturity. | Gives certainty but may become unattractive if market rates change. |

Promissory Note With Default Interest | |||||

Business loan Asset purchase Short-term bridging arrangement Personal loan | Single lump sum Instalments Balloon payment | Usually | Medium | Default events, default rate, cure period, acceleration, enforcement costs. | Default rate should be justifiable and not drafted as a penalty. |

Promissory Note With Acceleration Clause | |||||

Business loan Asset purchase Personal loan Short-term bridging arrangement | Instalments Balloon payment Single lump sum | Usually | Medium | Default triggers, cure period, acceleration notice, full balance due, costs. | Acceleration should be tied to clear defaults and notice requirements. |

Assignable Promissory Note | |||||

Business loan Other | Single lump sum Instalments On demand | Usually | High | Assignment rights, notice to borrower, transfer restrictions, payment instructions. | Borrower should know whether payment recipient can change. |

Non-Transferable Promissory Note | |||||

Family or friends loan Personal loan Business loan | Single lump sum Instalments On demand | Sometimes | Low | No assignment, named lender, repayment terms, interest, default, notices. | Restricts lender liquidity but gives borrower certainty over creditor identity. |

Consumer Loan Promissory Note | |||||

Personal loan Family or friends loan Other | Single lump sum Instalments On demand Flexible repayment | Sometimes | High | Credit amount, repayment, interest, APR if applicable, notices, cancellation rights. | Non-exempt lending to individuals may require FCA authorisation and compliant terms. |

Regulated Credit Promissory Note | |||||

Personal loan Other | Instalments Single lump sum Flexible repayment | Usually | High | Prescribed information, interest, APR, repayments, arrears notices, rights. | Consumer Credit Act compliance may be essential for enforceability. |

Company Charge-Backed Promissory Note | |||||

Business loan Asset purchase Short-term bridging arrangement | Single lump sum Instalments Balloon payment On demand | Usually | High | Charged assets, restrictions, enforcement, registration, default, release. | Part 25 Companies Act 2006 governs registration of company charges. |

Cross-Border Promissory Note | |||||

Business loan Personal loan Other | Single lump sum Instalments On demand Balloon payment | Usually | High | Governing law, jurisdiction, currency, tax, sanctions, service of process. | Currency, tax withholding, enforcement location, and sanctions screening matter. |

Sterling Promissory Note | |||||

Personal loan Business loan Family or friends loan Asset purchase | Single lump sum Instalments On demand Balloon payment | Sometimes | Low | GBP amount, payment account, repayment date, interest, default, bank charges. | Avoids exchange-rate risk for UK-based parties paid in pounds sterling. |

Foreign Currency Promissory Note | |||||

Business loan Other Asset purchase | Single lump sum Instalments Balloon payment | Usually | High | Currency, exchange rate, conversion date, payment location, bank fees, tax. | Exchange-rate movements can materially change the real repayment cost. |

Promissory Note Executed As A Deed | |||||

Business loan Personal loan Family or friends loan Other | Single lump sum Instalments On demand | Sometimes | Medium | Deed execution, consideration wording, repayment, interest, default, governing law. | Special execution formalities apply and limitation periods may differ. |

Simple IOU Promissory Note | |||||

Personal loan Family or friends loan | Single lump sum On demand | Rarely | Low | Borrower, lender, amount owed, repayment date, signatures. | May be too sparse for interest, default, or instalment arrangements. |

Bills Of Exchange Act Promissory Note | |||||

Business loan Other | Single lump sum On demand | Sometimes | High | Unconditional promise, maker signature, certain sum, payee, time, delivery. | Section 83 defines promissory notes as unconditional written promises to pay. |

Short-Form Commercial Promissory Note | |||||

Business loan Other | Single lump sum Instalments | Usually | Low | Principal, commercial interest, due date, default, costs, governing law. | Suitable only where no security, covenants, or complex conditions are needed. |

Long-Form Commercial Promissory Note | |||||

Business loan Asset purchase Short-term bridging arrangement | Single lump sum Instalments Balloon payment On demand | Usually | High | Representations, covenants, information undertakings, default, security, transfer. | Appropriate where lender needs monitoring rights and detailed remedies. |

Maturity-Date Promissory Note | |||||

Business loan Personal loan Asset purchase | Single lump sum Balloon payment | Usually | Low | Maturity date, accrued interest, principal repayment, default, notices. | Works well where the borrower expects funds by a known date. |

Event-Triggered Promissory Note | |||||

Short-term bridging arrangement Business loan Asset purchase Other | Single lump sum Balloon payment Flexible repayment | Usually | High | Repayment trigger, longstop date, interest, information duties, default. | Include a longstop date if the triggering event never occurs. |

Promissory Note With Grace Period | |||||

Personal loan Family or friends loan Business loan | Instalments Single lump sum | Sometimes | Medium | Due dates, grace period, late charges, default timing, notices. | Define whether interest or default interest runs during the grace period. |

Promissory Note With Late Fees | |||||

Business loan Personal loan Asset purchase | Instalments Single lump sum | Usually | Medium | Late fee amount, trigger date, default interest, costs, payment allocation. | Late fees should reflect genuine costs and avoid penalty risk. |

Secured Personal Loan Promissory Note | |||||

Personal loan Family or friends loan Asset purchase | Instalments Single lump sum On demand | Sometimes | High | Collateral, repayment, interest, possession rights, default, consumer credit checks. | Security over consumer assets may raise regulated-credit and enforcement issues. |

Promissory Note With Personal Guarantee | |||||

Business loan Asset purchase Short-term bridging arrangement | Single lump sum Instalments Balloon payment On demand | Usually | High | Primary debt, guarantee, indemnity, guarantor waiver, demand, enforcement costs. | Guarantor may be personally liable even if the borrower is a company. |

Promissory Note With Waiver Rights | |||||

Family or friends loan Personal loan Business loan | Instalments Flexible repayment Single lump sum | Sometimes | Medium | Waiver process, no continuing waiver, revised dates, written consent, default. | Any waiver should be documented so rights are not accidentally lost. |

Which UK Promissory Note Type Is Best For Your Loan?

The most suitable promissory note depends mainly on when repayment is due, whether interest is charged, and whether the parties need flexibility. A simple fixed-date or lump-sum note is usually lower complexity, while secured, convertible, asset-purchase, or cross-border notes need more detailed drafting.

When Should A Promissory Note Include Interest?

Interest is commonly included for business loans, bridging arrangements, asset purchases, and longer-term instalment notes. For family or friends loans, interest is often omitted or kept simple, but the note should still state clearly whether interest is payable, the rate, when it accrues, and what happens after default. UK users should also consider tax and consumer-credit implications where lending is not purely private or informal.

When Is A Promissory Note More Than A Simple IOU?

A note becomes more complex where it is secured, guaranteed, convertible into shares, linked to an asset sale, repayable on demand, or used for business finance. These versions normally need clauses covering default, enforcement, security, notices, prepayment, transfer, governing law, and, where relevant, Companies House filings or Financial Conduct Authority regulated-credit issues.

What Should UK Borrowers And Lenders Check Before Signing?

- Repayment wording: choose a fixed date, instalments, on-demand repayment, a balloon payment, or flexible drawdown terms.

- Interest and default interest: state the rate, calculation method, payment dates, and whether interest changes after missed payment.

- Security: if assets secure the note, separate security documents and registration may be required.

- Consumer lending risk: loans to individuals can raise regulated credit issues under the Consumer Credit Act 1974 and FCA rules.

- Transferability: if the lender may sell or assign the note, include clear assignment or negotiation terms.

FAQs

You Might Also Be Interested In