Promissory Note Clause Checklist In Britain

Created:

This checklist helps you understand key clauses commonly included in promissory notes and why they matter. It is useful for reviewing terms clearly before drafting or signing an AI Generated British Promissory Note.

Clause Category | Importance Level | Purpose | Typical Content | Main Party Affected |

|---|---|---|---|---|

Title and Instrument Description | ||||

Administrative term | Recommended | States that the document is intended to be a promissory note. | Heading such as "Promissory Note" and a short statement of promise to pay. | Both parties |

Borrower Details | ||||

Core repayment term | Essential | Identifies who must repay the debt. | Full legal name, address, company number if applicable, and contact details. | Borrower |

Lender Details | ||||

Core repayment term | Essential | Identifies who is entitled to repayment. | Full legal name, address, company number if applicable, and payment contact details. | Lender |

Joint and Several Liability | ||||

Optional protection | Situational | Makes each borrower responsible for the whole debt. | Each borrower is liable jointly and individually for all sums due. | Borrower |

Principal Amount | ||||

Core repayment term | Essential | Records the amount borrowed and to be repaid. | A specific sterling amount written in numbers and words. | Both parties |

Currency | ||||

Core repayment term | Recommended | Avoids doubt about the currency of repayment. | All payments must be made in pounds sterling unless agreed otherwise. | Both parties |

Unconditional Promise To Pay | ||||

Core repayment term | Essential | Creates a clear repayment obligation. | Borrower unconditionally promises to pay the lender the principal and any agreed interest. | Borrower |

Issue Date | ||||

Administrative term | Essential | Shows when obligations start. | Date of signing or date funds are advanced. | Both parties |

Maturity Date | ||||

Core repayment term | Essential | Sets the final date for repayment. | A fixed calendar date or a defined number of days after demand or issue. | Both parties |

Repayment Schedule | ||||

Core repayment term | Situational | Sets when and how instalments are paid. | Payment dates, instalment amounts, final balloon payment, and allocation of payments. | Both parties |

Repayment On Demand | ||||

Core repayment term | Situational | Allows the lender to require repayment after a demand. | Payment due immediately or within a stated period after written demand. | Lender |

Voluntary Prepayment | ||||

Optional protection | Recommended | States whether early repayment is allowed. | Borrower may prepay all or part of the debt with or without notice or fee. | Borrower |

Mandatory Prepayment | ||||

Optional protection | Situational | Requires repayment if specified events occur. | Repayment on asset sale, refinancing, change of control, or receipt of insurance proceeds. | Borrower |

Payment Method | ||||

Administrative term | Recommended | Gives practical instructions for payment. | Bank transfer details, reference wording, cleared funds, and no cash unless agreed. | Both parties |

Place Of Payment | ||||

Administrative term | Optional | Specifies where payment must be made if relevant. | Payment to lender address or nominated bank account. | Both parties |

Cleared Funds | ||||

Administrative term | Recommended | Confirms payment counts only when funds are available. | Payment is made only when received in cleared funds in the lender account. | Lender |

Business Day Adjustment | ||||

Administrative term | Recommended | Explains what happens if a due date is not a business day. | Payment due on the next business day, or previous business day if specified. | Both parties |

Interest Rate | ||||

Interest and charges | Situational | States whether interest is charged and at what rate. | Fixed annual percentage, variable rate, or express statement that no interest applies. | Both parties |

Interest Accrual Period | ||||

Interest and charges | Recommended | Shows when interest starts and stops accruing. | Interest accrues from advance date until actual repayment or maturity. | Both parties |

Interest Calculation Method | ||||

Interest and charges | Recommended | Avoids disputes about how interest is calculated. | Daily accrual, actual days elapsed, 365-day year, simple or compound interest. | Both parties |

Compounding | ||||

Interest and charges | Situational | States whether unpaid interest earns further interest. | Interest compounds monthly, annually, on default, or does not compound. | Borrower |

No Interest Statement | ||||

Interest and charges | Situational | Confirms the loan is interest-free. | No interest is payable unless the borrower defaults or parties agree otherwise in writing. | Both parties |

Default Interest | ||||

Interest and charges | Recommended | Increases interest after late payment or default. | A higher rate applies to overdue sums from due date until payment. | Borrower |

Statutory Late Payment Interest | ||||

Interest and charges | Situational | Refers to statutory interest for qualifying commercial debts. | Interest and compensation may apply to qualifying business debts under UK late payment rules. | Lender |

Arrangement Fee | ||||

Interest and charges | Situational | Records any upfront fee for making the loan. | Amount, due date, deduction from advance, or separate payment obligation. | Borrower |

Late Payment Fee | ||||

Interest and charges | Optional | Charges a fixed fee for missed or late payments. | A proportionate fixed fee payable after a missed instalment or overdue final payment. | Borrower |

Costs And Expenses | ||||

Interest and charges | Recommended | Requires the borrower to pay reasonable recovery costs. | Reasonable legal, collection, tracing, and enforcement costs caused by default. | Borrower |

Tax Gross-Up And Withholding | ||||

Interest and charges | Situational | Allocates risk of tax deductions from interest payments. | Payments made without deduction unless required by law gross-up if agreed. | Both parties |

Events Of Default | ||||

Default and enforcement | Essential | Lists events that allow enforcement action. | Non-payment, insolvency, breach, misrepresentation, unlawfulness, or security failure. | Both parties |

Non-Payment Default | ||||

Default and enforcement | Essential | Confirms failure to pay is a default. | Default occurs if any amount is not paid when due. | Borrower |

Grace Period | ||||

Default and enforcement | Situational | Gives the borrower time to fix specified breaches. | Non-payment cured within a stated number of days other breaches cured if capable of remedy. | Borrower |

Acceleration | ||||

Default and enforcement | Recommended | Allows the lender to demand the full balance after default. | All principal, interest, and costs become immediately due after an event of default. | Lender |

Default Notice | ||||

Default and enforcement | Situational | Sets notice steps before enforcement or acceleration. | Written notice describing the default, required remedy, deadline, and consequences. | Both parties |

No Waiver | ||||

Default and enforcement | Recommended | Prevents delay or partial action from giving up rights. | Failure or delay in exercising rights is not a waiver rights are cumulative. | Lender |

Application Of Payments | ||||

Default and enforcement | Recommended | Sets the order in which payments reduce the debt. | Payments applied to costs, default interest, ordinary interest, then principal. | Both parties |

No Set-Off Or Deduction | ||||

Optional protection | Recommended | Requires payment without withholding unrelated claims. | Borrower pays in full without set-off, counterclaim, deduction, or withholding except required by law. | Borrower |

Lender Set-Off | ||||

Optional protection | Situational | Lets lender apply money it owes borrower against the debt. | Lender may set off matured obligations after notice or default. | Lender |

Unsecured Note Statement | ||||

Optional protection | Situational | States that no asset secures the debt. | The note is unsecured and no security interest is granted. | Lender |

Security Interest | ||||

Optional protection | Situational | Links the note to collateral securing repayment. | Description of secured assets, separate security document, registration duties, and enforcement rights. | Lender |

Company Charge Registration | ||||

Execution and formalities | Situational | Flags registration when a UK company grants security. | Charge must be registered at Companies House within the applicable period if required. | Borrower |

Guarantee | ||||

Optional protection | Situational | Makes another person responsible if the borrower does not pay. | Guarantor guarantees payment, indemnifies lender, and signs in writing. | Both parties |

Borrower Representations | ||||

Optional protection | Recommended | Records key statements the lender relies on. | Capacity, authority, solvency, no conflict, accuracy of information, and lawful purpose. | Borrower |

Borrower Covenants | ||||

Optional protection | Situational | Controls borrower conduct until repayment. | Maintain status, pay taxes, keep records, provide information, and avoid prejudicing repayment. | Borrower |

Restriction On Further Debt | ||||

Optional protection | Situational | Limits borrower taking on more debt. | No new financial indebtedness above a threshold without lender consent. | Borrower |

Restriction On Asset Sales | ||||

Optional protection | Situational | Protects repayment prospects by limiting asset sales. | No material asset disposal outside ordinary course without lender consent. | Borrower |

Change Of Control | ||||

Optional protection | Situational | Protects lender if ownership or control changes. | Change in control triggers consent requirement, default, or mandatory repayment. | Lender |

Subordination | ||||

Optional protection | Situational | Sets payment priority against other creditors. | Debt ranks behind or ahead of specified debts, often in a separate intercreditor agreement. | Both parties |

Assignment And Transfer | ||||

Administrative term | Recommended | States whether rights or obligations can be transferred. | Lender may assign rights with notice borrower cannot transfer obligations without consent. | Both parties |

Negotiability | ||||

Administrative term | Situational | Clarifies whether the note can circulate by endorsement or delivery. | Payable to named lender only, to order, or to bearer if intended and lawful. | Both parties |

Lost Note Replacement | ||||

Administrative term | Optional | Deals with loss or destruction of the original note. | Borrower issues replacement against evidence of loss and indemnity if appropriate. | Both parties |

Cancellation On Repayment | ||||

Administrative term | Recommended | Shows the note is discharged after full payment. | Lender marks the note paid, returns it, or confirms discharge in writing. | Borrower |

Loan Account Records | ||||

Administrative term | Optional | Keeps evidence of balance, interest, and payments. | Lender records are evidence of amounts due unless obvious error is shown. | Both parties |

Notices | ||||

Administrative term | Recommended | Sets how formal communications are sent. | Permitted methods, addresses, email use, deemed receipt, and address updates. | Both parties |

Electronic Notices | ||||

Administrative term | Optional | Allows notices by email or electronic platform. | Approved email addresses, delivery rules, and exclusions for formal court documents. | Both parties |

Governing Law | ||||

Administrative term | Essential | Identifies which UK legal system governs the note. | Governed by the law of England and Wales, Scotland, or Northern Ireland. | Both parties |

Jurisdiction | ||||

Default and enforcement | Recommended | States which courts may hear disputes. | Courts of England and Wales, Scotland, or Northern Ireland have exclusive or non-exclusive jurisdiction. | Both parties |

Dispute Resolution | ||||

Default and enforcement | Optional | Encourages structured handling of disputes before court. | Negotiation, mediation, escalation, and ability to seek urgent relief. | Both parties |

Limitation Period Acknowledgment | ||||

Default and enforcement | Optional | Records awareness that debt claims have time limits. | Acknowledgment of debt and repayment dates, without trying to override statutory limitation rules. | Lender |

Entire Agreement | ||||

Administrative term | Recommended | Limits reliance on earlier informal statements. | The note and related security documents contain the whole agreement on the loan. | Both parties |

Variation | ||||

Administrative term | Recommended | Controls how terms can be changed. | Changes must be in writing and signed by the parties. | Both parties |

Severability | ||||

Administrative term | Recommended | Keeps the rest of the note effective if one term is invalid. | Invalid terms are modified or removed without affecting the remaining provisions. | Both parties |

Third Party Rights | ||||

Administrative term | Recommended | Controls whether non-parties can enforce terms. | No person other than the parties may enforce the note unless expressly stated. | Not party-specific |

Confidentiality | ||||

Optional protection | Optional | Restricts disclosure of the note and loan terms. | Disclosure allowed to advisers, funders, auditors, regulators, courts, or as required by law. | Both parties |

Data Protection | ||||

Administrative term | Situational | Addresses personal data shared for loan administration. | Use of personal data for identity checks, payment processing, enforcement, and record keeping. | Both parties |

Identity And AML Checks | ||||

Administrative term | Situational | Supports verification where regulated checks are needed. | Parties provide identification, beneficial ownership information, and source of funds evidence if requested. | Both parties |

Consumer Credit Compliance | ||||

Execution and formalities | Situational | Flags whether consumer credit rules may apply. | Statement that parties should check if the loan is regulated, exempt, or business lending. | Both parties |

Residential Security Warning | ||||

Execution and formalities | Situational | Warns that loans secured on a home may need specialist compliance. | Do not secure the note on residential property without checking mortgage regulation and advice needs. | Both parties |

Financial Promotion Compliance | ||||

Execution and formalities | Situational | Flags restrictions on promoting investment-like notes. | No offer, invitation, or circulation unless authorised or exempt. | Lender |

Corporate Authority | ||||

Execution and formalities | Situational | Confirms a company has power and approval to sign. | Board approval, authorised signatory, capacity confirmation, and no constitutional restriction. | Both parties |

Company Execution | ||||

Execution and formalities | Situational | Ensures proper signing by a company. | Signed by two authorised signatories or one director in the presence of a witness. | Witness or signatory |

Execution As A Deed | ||||

Execution and formalities | Situational | Used where deed formalities or longer limitation are desired. | Document states it is a deed, is validly executed, witnessed if needed, and delivered. | Witness or signatory |

Individual Signature Block | ||||

Execution and formalities | Essential | Provides evidence that the individual borrower signed. | Signature, printed name, date, address, and optional witness details. | Witness or signatory |

Witness Attestation | ||||

Execution and formalities | Situational | Supports deed execution or evidential certainty. | Witness signature, name, address, occupation, and confirmation of witnessing. | Witness or signatory |

Electronic Signature | ||||

Execution and formalities | Optional | Allows signing by electronic method where appropriate. | Electronic signatures are accepted if the method identifies the signer and shows intent. | Witness or signatory |

Counterparts | ||||

Execution and formalities | Optional | Allows parties to sign separate copies. | Each signed copy is an original and all copies form one document. | Witness or signatory |

Condition To Advance | ||||

Core repayment term | Situational | States conditions before the lender must release funds. | Signed note, identity checks, board approvals, security documents, and bank details delivered first. | Lender |

Acknowledgment Of Advance | ||||

Core repayment term | Recommended | Records that the borrower received the loan money. | Borrower acknowledges receipt of the principal or states when the advance will be made. | Both parties |

Purpose Of Loan | ||||

Core repayment term | Optional | Records the intended use of funds. | General working capital, personal loan, purchase funding, or no restriction on use. | Borrower |

Use Of Proceeds Restriction | ||||

Optional protection | Situational | Prevents use of funds for prohibited purposes. | Funds must not be used for unlawful purposes, sanctions breaches, gambling, or unauthorised investments. | Borrower |

Sanctions Compliance | ||||

Optional protection | Situational | Reduces risk of dealing with sanctioned persons or prohibited funds. | Parties are not sanctioned and will not use funds in breach of UK sanctions. | Both parties |

Illegality | ||||

Default and enforcement | Situational | Deals with repayment if continuing the loan becomes unlawful. | Loan becomes repayable if performance becomes unlawful for either party. | Both parties |

Insolvency Default | ||||

Default and enforcement | Recommended | Triggers default if borrower becomes insolvent. | Bankruptcy, liquidation, administration, CVA, IVA, moratorium, or inability to pay debts. | Borrower |

Material Adverse Change | ||||

Default and enforcement | Optional | Protects lender from serious deterioration in borrower position. | Default if an event materially affects ability to repay or validity of the note. | Lender |

Cross-Default | ||||

Default and enforcement | Situational | Links default under other debts to this note. | Default occurs if borrower defaults under other financial indebtedness above a threshold. | Borrower |

Misrepresentation Default | ||||

Default and enforcement | Recommended | Allows remedies if key statements are untrue. | Default if a representation is materially untrue or misleading when made or repeated. | Borrower |

Breach Of Covenant Default | ||||

Default and enforcement | Recommended | Makes breach of non-payment terms enforceable. | Default if borrower breaches any obligation and fails to remedy within any cure period. | Borrower |

Information Undertaking | ||||

Optional protection | Optional | Lets lender monitor repayment risk. | Borrower provides accounts, bank details, address updates, and notice of defaults. | Borrower |

Change Of Address Notice | ||||

Administrative term | Optional | Keeps contact and notice details current. | Party must promptly notify the other of address, email, or bank detail changes. | Both parties |

Bank Details Verification | ||||

Administrative term | Optional | Reduces risk of payment diversion fraud. | Changes to payment details require independent verification before use. | Both parties |

Stamp Duty Responsibility | ||||

Execution and formalities | Situational | Allocates responsibility for any stamp duty issue. | Party responsible for any duty, stamping, penalties, or advice on negotiable instruments. | Both parties |

Independent Legal Advice Acknowledgment | ||||

Execution and formalities | Optional | Records that parties could seek advice before signing. | Each party has had opportunity to take independent legal and financial advice. | Both parties |

Undue Influence Safeguard | ||||

Execution and formalities | Situational | Reduces challenge risk where pressure or dependency may exist. | Signer confirms they sign freely, understand obligations, and had chance for independent advice. | Borrower |

No Partnership Or Agency | ||||

Administrative term | Optional | Clarifies the loan does not create a wider relationship. | Nothing creates partnership, joint venture, agency, employment, or fiduciary relationship. | Both parties |

Priority Of Documents | ||||

Administrative term | Situational | Resolves conflict between the note and related documents. | States whether the note, loan agreement, guarantee, or security document prevails. | Both parties |

Receipts And Statements | ||||

Administrative term | Optional | Helps prove payments and outstanding balance. | Lender provides receipts or periodic statements after request or payment. | Borrower |

Rounding Of Amounts | ||||

Interest and charges | Optional | Avoids small calculation disputes. | Interest and payment amounts rounded to the nearest penny or pound. | Both parties |

Interest Savings Clause | ||||

Interest and charges | Optional | Limits interest if a court finds part unenforceable. | Interest is reduced to the highest enforceable amount if required by applicable law. | Both parties |

Cumulative Remedies | ||||

Default and enforcement | Recommended | Confirms lender rights are additional, not exclusive. | Rights under the note are cumulative and do not exclude rights under law or security documents. | Lender |

Service Of Process Address | ||||

Default and enforcement | Situational | Gives a UK address for formal legal service. | Overseas party appoints a process agent or address for service in the chosen jurisdiction. | Both parties |

Death Or Incapacity | ||||

Default and enforcement | Situational | Deals with repayment if an individual borrower dies or loses capacity. | Debt remains payable by estate or representatives, subject to applicable probate and capacity rules. | Borrower |

Successors And Personal Representatives | ||||

Administrative term | Recommended | Ensures rights and obligations continue after death or transfer. | Note binds and benefits successors, permitted assigns, and personal representatives. | Both parties |

Definitions And Interpretation | ||||

Administrative term | Recommended | Defines key terms used in the note. | Definitions of business day, due date, default, outstanding amount, and parties. | Not party-specific |

Headings | ||||

Administrative term | Optional | Prevents headings from altering legal meaning. | Headings are for convenience only and do not affect interpretation. | Not party-specific |

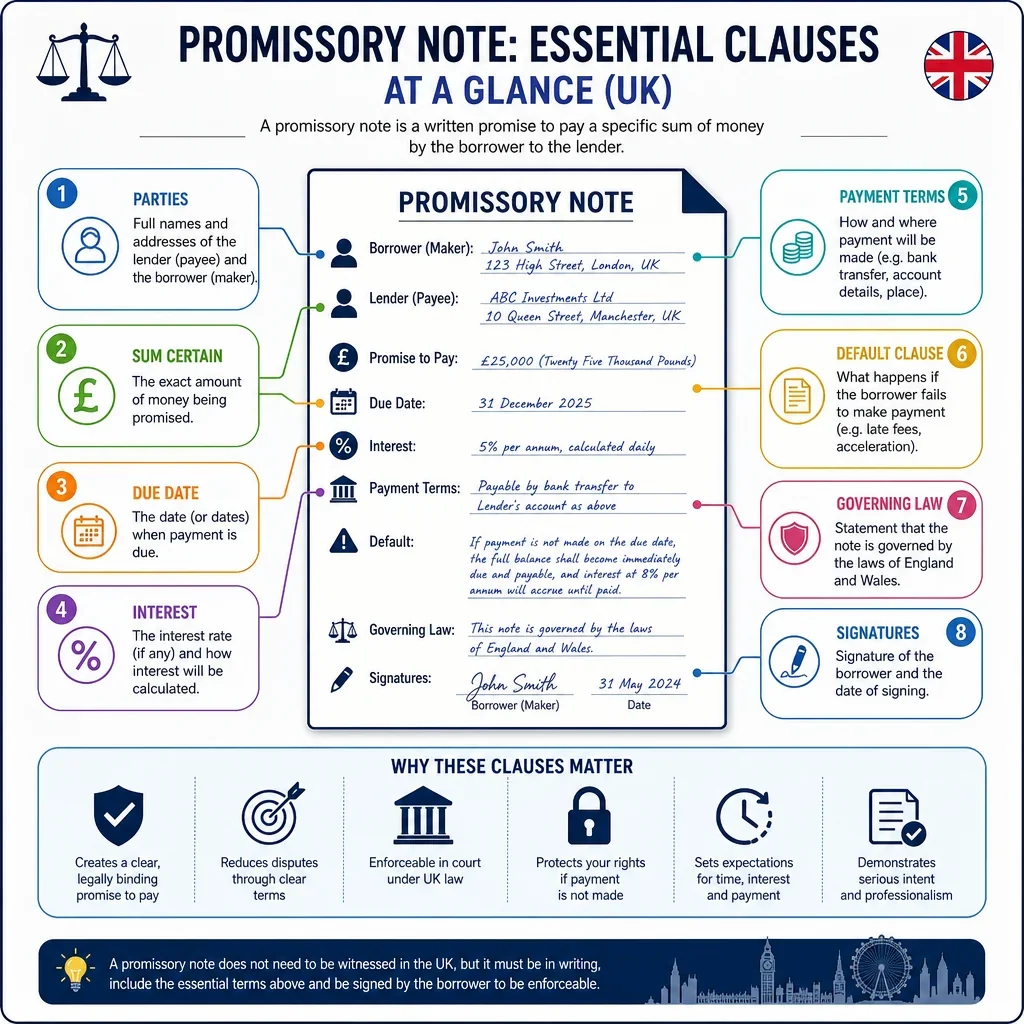

What Clauses Should A UK Promissory Note Include?

A useful UK promissory note should clearly identify the borrower, lender, principal amount, repayment obligation, due date or repayment schedule, interest position, payment method, governing law, and signatures. These clauses reduce uncertainty about whether the document is evidence of a debt, when payment is due, and what happens if the borrower does not pay.

When Is A Promissory Note More Than A Simple IOU?

A promissory note can become more complex where it includes interest, default interest, security, guarantees, transfer rights, set-off restrictions, or acceleration. In the UK, these additions may have regulatory, tax, enforcement, and consumer-credit implications depending on the parties and purpose of the loan.

Which UK Legal Issues Should Users Check Before Signing?

- Consumer credit: if the borrower is an individual and the loan is not exempt, the Consumer Credit Act 1974 and FCA regime may apply.

- Interest and late payment: business-to-business late payment interest may be affected by the Late Payment of Commercial Debts (Interest) Act 1998, but private loan interest should be expressly agreed.

- Limitation: ordinary contract debt claims commonly have a six-year limitation period in England and Wales, while deeds may have a longer period.

- Execution: a simple promissory note usually requires signature, but deeds have stricter witnessing and delivery requirements under UK law.

- Stamp duty and negotiability: UK bills and notes law can be relevant if the document is intended to operate as a negotiable promissory note rather than a private loan acknowledgment.

Want to Generate Your own Promissory Note?

Docaro AI can help you write your own Promissory Note for use in the United Kingdom in minutes.

FAQs

A promissory note clause checklist helps ensure a UK promissory note includes key terms such as parties, loan amount, repayment date, interest, default, governing law, and signatures.

Show All FAQs

You Might Also Be Interested In

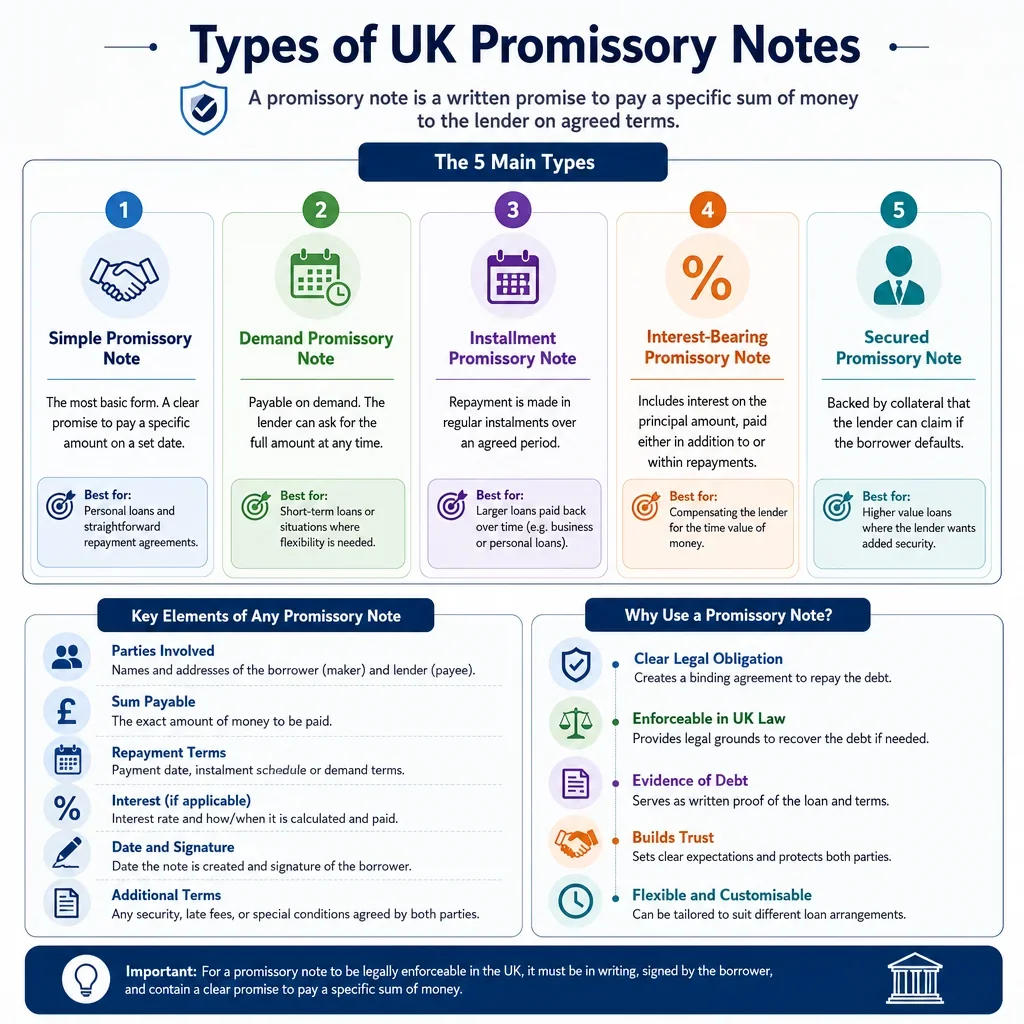

Explore types of UK promissory notes, their uses, and key differences to help choose the right note for your agreement.

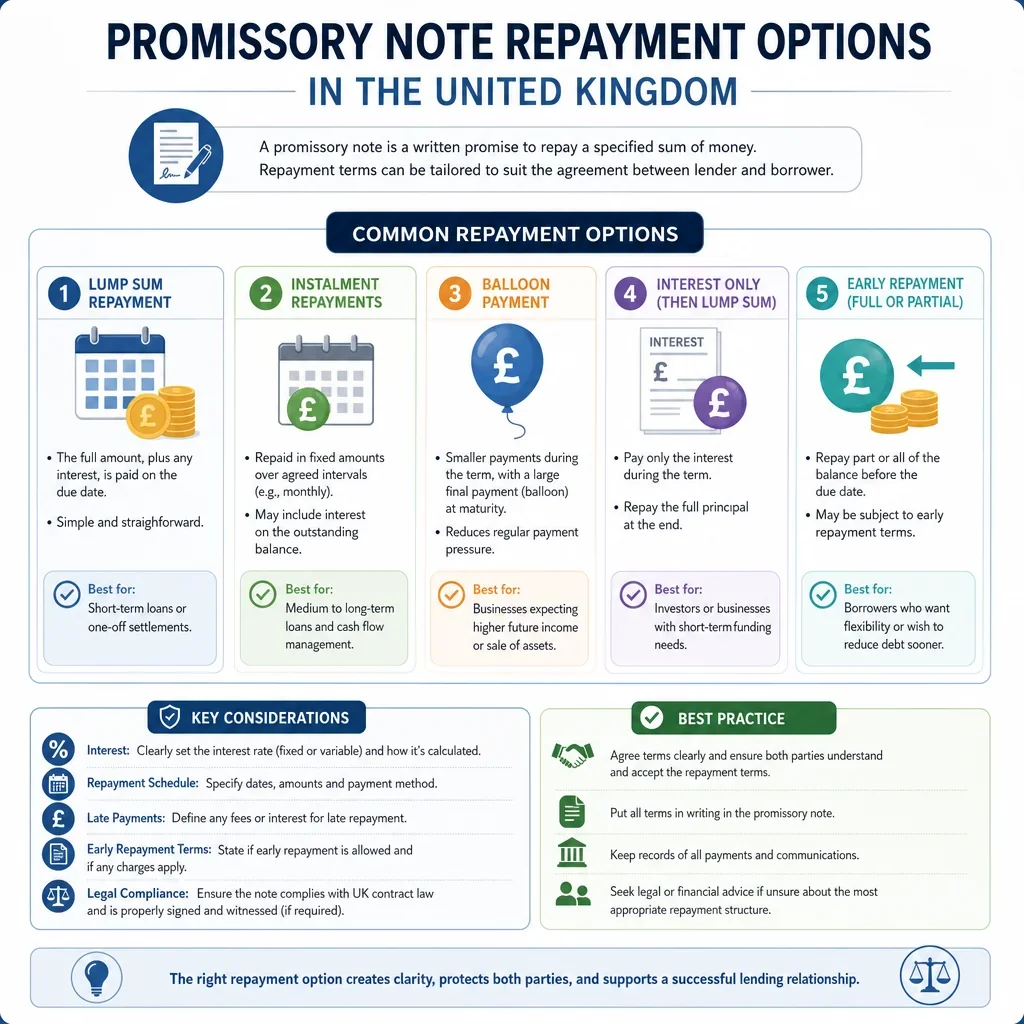

Explore promissory note repayment options in the United Kingdom, including schedules, interest, and flexible payment terms.