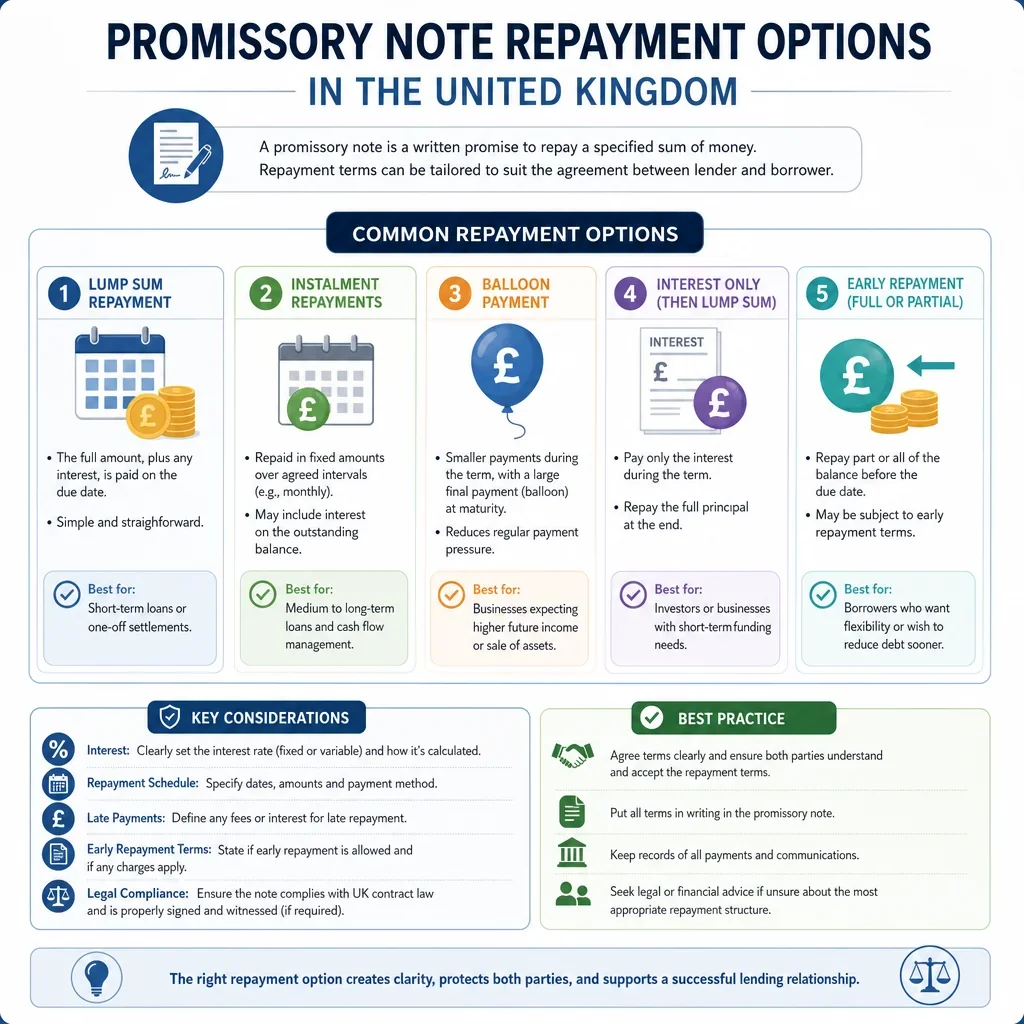

Promissory Note Repayment Options In The United Kingdom

Timing Model | Drafting Detail Required | Typical Party Benefit | Advantages | Potential Drawbacks | Information to Include |

|---|---|---|---|---|---|

Single lump sum on a fixed maturity date | |||||

Fixed date | Simple | Balanced | Clear, easy to administer and simple to evidence. | Borrower must find the full amount at once. | Maturity date, principal, interest, payment method and consequences of non-payment. |

Repayable on demand | |||||

On demand | Moderate | Lender | Gives lender strong control over repayment timing. | Creates uncertainty for borrower and possible liquidity pressure. | How demand is served, notice period, payment deadline and default interest. |

Repayable after written demand with notice period | |||||

On demand | Moderate | Balanced | Balances lender flexibility with borrower time to arrange funds. | Disputes may arise over valid service of demand. | Notice length, permitted service methods, deemed receipt and final due date. |

Equal monthly instalments | |||||

Instalment schedule | Detailed | Borrower | Predictable cash flow and affordable staged repayment. | More administration and missed payment tracking. | Instalment amount, dates, interest allocation, late fees and final balancing payment. |

Equal weekly instalments | |||||

Instalment schedule | Detailed | Borrower | Matches weekly income or trading receipts. | High administrative burden and frequent default risk. | Payment weekday, amount, start date, end date and missed payment procedure. |

Quarterly instalments | |||||

Instalment schedule | Moderate | Balanced | Useful for business borrowers with quarterly cash flow. | Larger individual payments than monthly schedules. | Quarter dates, instalment amount, interest calculation and business day adjustment. |

Fully amortising repayments | |||||

Instalment schedule | Detailed | Balanced | Reduces principal over time and avoids final lump sum. | Requires accurate interest and amortisation calculations. | Repayment table, rate, calculation basis, instalment dates and rounding method. |

Interest-only payments with principal at maturity | |||||

Balloon payment | Detailed | Borrower | Low periodic payments while preserving lender interest return. | Large final principal payment may be unaffordable. | Interest dates, principal maturity date, rate, accrual basis and default terms. |

Small instalments with final balloon payment | |||||

Balloon payment | Detailed | Depends on terms | Improves short-term affordability while setting a clear final balance. | Final payment risk is concentrated at maturity. | Instalment schedule, balloon amount, maturity date and refinancing assumptions if any. |

Bullet repayment of principal and accrued interest | |||||

Fixed date | Moderate | Borrower | No interim payments and simple cash flow for borrower. | Lender waits for all return and bears greater credit risk. | Maturity date, accrued interest formula, total payoff method and default consequences. |

Repayment from sale proceeds | |||||

Event-based | Detailed | Depends on terms | Aligns repayment with expected asset disposal. | Delay or failed sale may postpone repayment. | Asset, sale deadline, proceeds waterfall, shortfall liability and longstop date. |

Repayment on completion of property sale | |||||

Event-based | Detailed | Depends on terms | Useful where repayment source is known property equity. | Completion may be delayed, fall through or produce insufficient funds. | Property details, completion trigger, solicitor undertaking if any, longstop and shortfall payment. |

Repayment on refinancing | |||||

Event-based | Detailed | Depends on terms | Matches repayment to replacement funding. | Refinancing may not be available or may be delayed. | Qualifying refinancing event, deadline, mandatory prepayment amount and fallback date. |

Repayment on funding round or investment receipt | |||||

Event-based | Detailed | Borrower | Useful for start-ups expecting equity or grant funding. | Funding may never occur without a robust longstop date. | Funding threshold, repayment percentage, longstop date and evidence of receipt. |

Percentage of revenue repayments | |||||

Flexible schedule | Detailed | Borrower | Repayments rise and fall with business performance. | Needs reporting rights and may create calculation disputes. | Revenue definition, percentage, reporting dates, audit rights, cap and maturity longstop. |

Percentage of profit repayments | |||||

Flexible schedule | Detailed | Depends on terms | Repayment tracks available profit rather than gross sales. | Profit is accounting-sensitive and easier to dispute. | Profit definition, accounting standard, deductions, reporting obligations and dispute process. |

Cash sweep from surplus cash | |||||

Flexible schedule | Detailed | Lender | Accelerates repayment when borrower has excess cash. | May restrict borrower working capital. | Surplus cash definition, testing dates, minimum cash buffer and payment priority. |

Seasonal repayment schedule | |||||

Flexible schedule | Detailed | Borrower | Matches repayments to seasonal income peaks. | Off-season arrears risk if dates are unrealistic. | High-season dates, payment amounts, skipped months and annual catch-up mechanism. |

Graduated increasing instalments | |||||

Instalment schedule | Detailed | Borrower | Supports borrower where income is expected to grow. | Later payments may become unaffordable if growth underperforms. | Step-up dates, payment amounts, interest treatment and final balance calculation. |

Graduated decreasing instalments | |||||

Instalment schedule | Detailed | Lender | Front-loads repayment and reduces lender exposure faster. | Higher early payments may strain borrower cash flow. | Step-down dates, amount table, principal allocation and missed payment effect. |

Deferred first payment after grace period | |||||

Instalment schedule | Moderate | Borrower | Allows time before repayments begin. | Interest may accumulate and increase total debt. | Grace period length, first payment date, interest accrual and revised schedule. |

Payment moratorium with capitalised interest | |||||

Flexible schedule | Detailed | Borrower | Temporary relief without writing off accrued interest. | Debt increases and compound interest issues may arise. | Moratorium dates, capitalisation method, revised principal and repayment restart date. |

Optional early repayment without penalty | |||||

Flexible schedule | Moderate | Borrower | Lets borrower reduce interest and clear debt early. | Lender may lose expected interest return. | Notice required, minimum amount, accrued interest and application to principal. |

Optional early repayment with premium | |||||

Flexible schedule | Detailed | Lender | Compensates lender for early exit. | May deter refinancing or early settlement. | Premium formula, notice period, settlement date and accrued interest treatment. |

Mandatory prepayment on asset sale | |||||

Event-based | Detailed | Lender | Protects lender when borrower converts assets into cash. | May restrict borrower asset management. | Covered assets, disposal threshold, proceeds percentage, timing and permitted reinvestment. |

Mandatory repayment on change of control | |||||

Event-based | Detailed | Lender | Lets lender exit if borrower ownership changes. | Can complicate investment, sale or restructuring plans. | Change of control definition, notification duty, repayment deadline and waiver process. |

Acceleration after event of default | |||||

Event-based | Detailed | Lender | Allows lender to demand all outstanding sums after serious breach. | Harsh if defaults are minor or easily cured. | Default events, cure periods, acceleration notice and sums immediately due. |

Acceleration only after cure period | |||||

Event-based | Detailed | Balanced | Prevents immediate acceleration for curable breaches. | Delays lender enforcement. | Cure period length, eligible defaults, notice requirements and acceleration process. |

Fixed repayments by standing order | |||||

Instalment schedule | Moderate | Balanced | Automates regular payments and reduces missed dates. | Failed payments still need default handling. | Payment account, reference, dates, amount and failed payment consequences. |

Repayments by direct debit | |||||

Instalment schedule | Moderate | Balanced | Convenient for recurring repayments where collection authority exists. | Requires mandate and may be cancelled by payer. | Mandate details, collection dates, advance notice and failed collection process. |

Repayment by payroll deduction | |||||

Instalment schedule | Detailed | Lender | Can provide reliable deductions where legally authorised. | Employment law and consent issues require care. | Employee consent, deduction amount, payroll dates and cessation on employment end. |

Permitted partial prepayments | |||||

Flexible schedule | Moderate | Borrower | Allows borrower to reduce debt whenever surplus funds arise. | Can complicate recalculation of remaining instalments. | Minimum partial amount, notice, allocation order and revised schedule method. |

Borrower payment holiday | |||||

Flexible schedule | Detailed | Borrower | Provides temporary cash-flow relief during agreed periods. | May extend term or increase final balance. | Eligibility, maximum holidays, notice, interest accrual and repayment recalculation. |

Lender-approved maturity extension | |||||

Flexible schedule | Moderate | Depends on terms | Avoids immediate default if repayment is delayed. | May require renegotiation fees or higher interest. | Extension request process, approval form, new date, fees and interest change. |

Automatic extension if conditions met | |||||

Event-based | Detailed | Borrower | Gives certainty if agreed objective conditions are satisfied. | Ambiguous conditions can cause disputes. | Extension conditions, evidence required, maximum extension and revised maturity date. |

Repayment from insurance proceeds | |||||

Event-based | Detailed | Lender | Protects lender if insured asset is lost or damaged. | Insurance proceeds may be needed to repair or replace the asset. | Relevant policy, claim trigger, repayment amount, reinstatement exception and timing. |

Repayment from litigation or settlement proceeds | |||||

Event-based | Detailed | Depends on terms | Links repayment to a specific expected recovery. | Outcome, timing and net recovery are uncertain. | Claim details, net proceeds definition, legal costs priority and longstop date. |

Repayment by contractual set-off | |||||

Event-based | Detailed | Depends on terms | Can simplify mutual debts between the same parties. | Set-off rights may be disputed or affected by insolvency. | Eligible obligations, valuation date, notice, netting method and exclusions. |

Conversion into shares instead of cash repayment | |||||

Event-based | Detailed | Depends on terms | Avoids cash repayment and may reward lender upside. | Needs company law, valuation and shareholder approval checks. | Conversion trigger, valuation, share class, approvals, allotment mechanics and residual debt. |

Lender election to convert or require cash repayment | |||||

Event-based | Detailed | Lender | Gives lender choice between liquidity and equity upside. | Can create uncertainty for borrower and investors. | Election window, conversion price, cash repayment fallback and notice requirements. |

Borrower election between permitted repayment methods | |||||

Flexible schedule | Detailed | Borrower | Allows borrower to choose cash, instalments or other agreed method. | Lender may receive less predictable repayment. | Permitted methods, election deadline, lender consent if required and default method. |

Fixed maturity with extension fee | |||||

Fixed date | Moderate | Depends on terms | Sets firm due date while allowing priced flexibility. | Fee may be challenged if excessive or unclear. | Original date, extension period, fee, payment timing and maximum extensions. |

Milestone-based repayment tranches | |||||

Event-based | Detailed | Balanced | Matches repayment to measurable project milestones. | Milestone satisfaction may be subjective or disputed. | Milestones, evidence, tranche amounts, due dates and dispute resolution process. |

Repayment on completion of works or project | |||||

Event-based | Detailed | Borrower | Allows project to generate value before repayment is due. | Completion delays can defer repayment indefinitely without a longstop. | Project description, completion certificate, longstop date and fallback repayment schedule. |

Repayment from specified invoice receipts | |||||

Event-based | Detailed | Balanced | Links repayment to identifiable receivables. | Customers may pay late, dispute invoices or not pay. | Invoice details, debtor, receipt account, repayment percentage and fallback date. |

Part instalment and part lump sum repayment | |||||

Instalment schedule, Balloon payment | Detailed | Depends on terms | Combines affordability with a defined final payoff. | Needs clear allocation between instalments and final balance. | Instalment schedule, lump sum amount, due date and interest allocation. |

Irregular agreed payment dates | |||||

Flexible schedule | Detailed | Borrower | Can reflect expected non-standard cash inflows. | Easy to misunderstand without a full payment table. | Each date, amount, interest treatment and final reconciliation method. |

Minimum monthly payment plus surplus sweep | |||||

Instalment schedule, Flexible schedule | Detailed | Balanced | Ensures regular repayment while capturing upside cash flow. | Surplus calculation can be contentious. | Minimum amount, sweep formula, testing period, cash buffer and cap. |

Repayments capped by monthly affordability limit | |||||

Flexible schedule | Detailed | Borrower | Reduces borrower hardship by limiting monthly outflow. | Can extend repayment period significantly. | Cap amount, affordability evidence, review dates, longstop date and unpaid balance treatment. |

Instalments with final balancing payment | |||||

Instalment schedule | Moderate | Balanced | Corrects rounding and variable interest differences at the end. | Final amount may be higher than expected. | How final balance is calculated, statement date and payment deadline. |

Fixed principal instalments plus accrued interest | |||||

Instalment schedule | Detailed | Lender | Principal reduces steadily and interest declines over time. | Initial payments may be higher than level-payment structures. | Principal portion, interest calculation, payment dates and outstanding balance schedule. |

Fixed total payment instalments | |||||

Instalment schedule | Detailed | Borrower | Same payment amount each period aids budgeting. | Requires amortisation schedule and interest accuracy. | Payment amount, interest rate, amortisation table, term and final adjustment. |

Repayment on death from estate | |||||

Event-based | Detailed | Depends on terms | Can suit family loans where repayment is expected from estate assets. | Estate solvency, probate delays and priority issues may affect recovery. | Trigger event, evidence, interest after death, estate claim process and longstop. |

Repayment on receipt of divorce settlement funds | |||||

Event-based | Detailed | Borrower | Aligns repayment with expected matrimonial finance receipt. | Settlement amount and timing may be uncertain. | Relevant settlement, receipt trigger, repayment amount, evidence and fallback date. |

Repayment from employment bonus | |||||

Event-based | Moderate | Borrower | Uses exceptional income rather than regular salary. | Bonus may be discretionary, reduced or not paid. | Bonus type, percentage payable, payment deadline, tax/net amount treatment and fallback. |

Repayment from tax refund | |||||

Event-based | Moderate | Borrower | Links repayment to an identifiable one-off receipt. | Refund may be smaller than expected or not due. | Refund type, amount or percentage, evidence, payment deadline and fallback schedule. |

Repayment in goods or assets by agreement | |||||

Event-based | Detailed | Depends on terms | Useful where borrower has valuable assets but limited cash. | Valuation, title, tax and delivery issues may arise. | Asset description, valuation, transfer date, warranties, VAT and shortfall treatment. |

Repayment from enforcement of security | |||||

Event-based | Detailed | Lender | Provides lender with a defined recovery source after default. | Security validity, registration and priority must be checked. | Security document, charged assets, enforcement trigger, proceeds waterfall and shortfall liability. |

Repayment by guarantor after borrower default | |||||

Event-based | Detailed | Lender | Gives lender secondary recovery source. | Guarantee enforceability and notice requirements must be clear. | Guarantor details, trigger, demand procedure, liability cap and continuing guarantee wording. |

Repayment by any joint borrower on joint and several basis | |||||

Fixed date | Moderate | Lender | Lender can seek full repayment from any liable borrower. | Co-borrowers may dispute internal contribution. | Borrower names, joint and several liability, due date and contribution arrangements if any. |

Pro rata repayment by multiple borrowers | |||||

Instalment schedule | Detailed | Borrower | Reflects agreed shares of liability between borrowers. | Lender recovery may be weaker if one borrower defaults. | Each borrower share, payment dates, default by one borrower and lender rights. |

Repayment in specified foreign currency | |||||

Fixed date | Detailed | Depends on terms | Matches currency of funding or income. | Exchange rate and payment system risks. | Currency, exchange rate source, conversion date, bank charges and shortfall rule. |

Sterling repayment converted from foreign currency amount | |||||

Fixed date | Detailed | Depends on terms | Allows UK payment while referencing foreign currency value. | Conversion disputes if rate source or timing is unclear. | Reference currency, GBP conversion source, rate date, charges and rounding. |

Repayment on next business day if due date is not a business day | |||||

Fixed date | Simple | Balanced | Avoids technical default when banks are closed. | Minor delay may affect interest calculations. | Business day definition, adjusted date rule and extra interest treatment. |

Immediate repayment on insolvency event | |||||

Event-based | Detailed | Lender | Protects lender if borrower solvency deteriorates. | Enforcement may be stayed or affected by insolvency rules. | Insolvency events, acceleration mechanism, notice and rights against security or guarantors. |

Repayment on breach of financial covenant | |||||

Event-based | Detailed | Lender | Gives early warning and remedy if borrower finances weaken. | Complex covenant testing may be unsuitable for simple notes. | Covenant formula, test dates, financial information, cure rights and repayment trigger. |

Lender call option after no-call period | |||||

On demand | Detailed | Lender | Gives borrower initial certainty and lender later flexibility. | Borrower faces refinancing risk after call date. | No-call period, call notice, repayment date, premium and accrued interest. |

Borrower put right to repay after lock-in | |||||

Flexible schedule | Detailed | Borrower | Lets borrower exit once agreed lock-in expires. | Lender return may be shortened unexpectedly. | Lock-in period, exercise notice, settlement amount and repayment date. |

Limited recourse repayment from specified asset only | |||||

Event-based | Detailed | Borrower | Limits borrower liability to agreed asset or proceeds. | Lender may not recover full debt if asset value falls. | Recourse limit, asset description, enforcement rights, shortfall release and risk allocation. |

Non-recourse repayment from collateral only | |||||

Event-based | Detailed | Borrower | Borrower has no personal liability beyond collateral. | Lender depends entirely on collateral value and enforceability. | Collateral, exclusive remedy wording, enforcement process and deficiency waiver. |

Repayment from inheritance receipt | |||||

Event-based | Detailed | Borrower | Aligns repayment with expected estate distribution. | Inheritance may be delayed, disputed or reduced. | Expected estate, receipt trigger, repayment percentage, evidence and fallback date. |

Repayment from grant or government payment | |||||

Event-based | Detailed | Borrower | Uses anticipated funding source without immediate cash pressure. | Grant eligibility, timing and permitted use may be restricted. | Grant scheme, qualifying receipt, permitted use, repayment amount and fallback terms. |

Consumer instalment repayments under regulated credit agreement | |||||

Instalment schedule | Detailed | Borrower | Structured consumer repayments with statutory protections where applicable. | May require regulatory compliance and prescribed information. | APR, total amount payable, instalments, default rights, notices and regulated status. |

Demand note intended to be enforceable without prior demand | |||||

On demand | Detailed | Lender | May allow immediate enforceability if validly drafted. | Limitation and demand wording can affect enforcement timing. | Express demand wording, issue date, limitation assumptions and payment deadline if demanded. |

Early settlement of consumer credit debt | |||||

Flexible schedule | Detailed | Borrower | Consumer borrower may have statutory early settlement protections if applicable. | Incorrect settlement wording may be non-compliant. | Regulated status, settlement calculation, notice process, rebate and statutory wording. |

Business debt repayment with statutory late payment interest after due date | |||||

Fixed date | Moderate | Lender | Can encourage prompt payment in qualifying business transactions. | Applies only where statutory conditions are met. | Commercial status, due date, contractual rate, statutory rate fallback and compensation wording. |

Same-day bank transfer repayment | |||||

Fixed date | Simple | Balanced | Fast settlement and clear payment evidence. | Limits, cut-off times or bank checks may delay payment. | Bank details, payment reference, currency, cut-off responsibility and receipt confirmation. |

Repayment through escrow account | |||||

Event-based | Detailed | Balanced | Protects parties where release depends on conditions. | Escrow fees and release disputes can arise. | Escrow agent, release conditions, fees, dispute process and fallback release date. |

Repayment via solicitor client account on completion | |||||

Event-based | Detailed | Balanced | Useful for property or transaction-linked repayment. | Requires solicitor cooperation and clear authority. | Solicitor details, client authority, undertaking if any, completion trigger and payment instructions. |

Gross-up repayment if tax withholding applies | |||||

Fixed date | Detailed | Lender | Preserves lender net receipt where withholding is required. | Tax analysis can be complex and fact-specific. | Tax deduction rule, gross-up formula, evidence, exemptions and cooperation obligations. |

Payment waterfall allocation | |||||

Flexible schedule | Detailed | Lender | Clarifies order of applying partial payments. | Borrower may prefer principal reduction first. | Order for costs, default interest, accrued interest, fees and principal. |

Pro rata repayment to multiple lenders | |||||

Instalment schedule | Detailed | Balanced | Treats lenders fairly in proportion to their note holdings. | Requires accurate lender register and payment administration. | Lender shares, payment agent, record date, rounding and shortfall allocation. |

Which Promissory Note Repayment Option Is Best In The UK?

Fixed-date repayment is usually the simplest structure, but it gives the borrower little flexibility and can create an immediate default risk if funds are not available on the due date. Instalment schedules are often better for affordability, but the note should state exact dates, amounts, interest allocation and what happens if one instalment is missed.

When Should A Promissory Note Use On-Demand Repayment?

On-demand repayment can strongly favour the lender because repayment can be required after notice, but the document should define how demand is made and how many days the borrower has to pay. In England and Wales, limitation periods can differ depending on whether a note is payable on demand or on a future date, so the repayment wording should be precise.

What Repayment Details Should Be Included?

- State the repayment trigger: date, demand, instalment dates, sale proceeds, refinancing, maturity or another event.

- State the amount payable: principal only, principal plus interest, fees, default interest and any early repayment discount or penalty.

- State the payment mechanics: bank details, currency, business day adjustment and whether partial payments are allowed.

- State the default consequences: acceleration, enforcement costs, security enforcement, guarantor demand or renegotiation rights.

Can A Borrower Repay Early?

Early repayment rights can be useful for borrowers, especially where interest accrues over time. However, if the lender expects a fixed return, the note should say whether early repayment is free, requires notice, includes accrued interest, or attracts a break cost. For consumer or regulated lending, UK rules and the Consumer Credit Act 1974 may affect enforceability and disclosure requirements.

FAQs

You Might Also Be Interested In