Types Of Personal Guarantee Obligations In The United Kingdom

Obligation Category | Description | Typical Scenario | Scope of Liability | Complexity Level | Continuing Effect |

|---|---|---|---|---|---|

Pure guarantee | |||||

Guarantee | A secondary promise to answer for another party's default. | Director guarantees a company's payment obligations. | Moderate | Medium | Sometimes |

Standalone indemnity | |||||

Indemnity | A primary promise to compensate for specified loss. | Parent covers losses from a subsidiary's breach. | Broad | Medium | Sometimes |

Guarantee and indemnity | |||||

Guarantee and indemnity | Combines secondary guarantee liability with primary indemnity protection. | Lender seeks robust protection for corporate borrowing. | Broad | High | Yes |

All monies guarantee | |||||

All monies guarantee | Covers all present and future debts owed to the beneficiary. | Bank guarantees covering overdrafts, loans and future facilities. | Broad | High | Yes |

Specific debt guarantee | |||||

Specific obligation guarantee | Guarantees one identified debt or facility only. | Guarantee of a named term loan. | Narrow | Low | No |

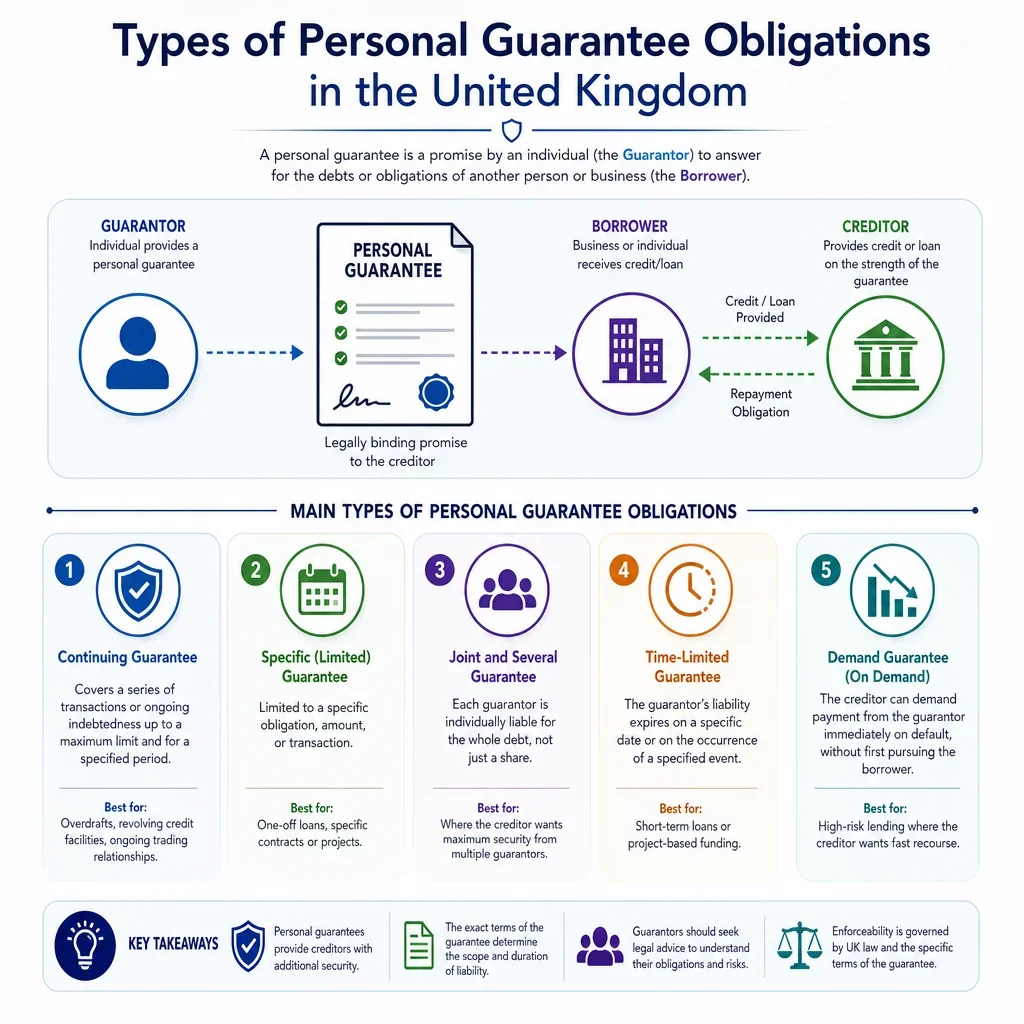

Continuing guarantee | |||||

Continuing guarantee | Continues across transactions until released or terminated. | Supplier credit account with repeated orders. | Broad | Medium | Yes |

Capped guarantee | |||||

Guarantee | Limits guarantor liability to a stated maximum amount. | SME director agrees a fixed exposure cap. | Narrow | Low | Sometimes |

Uncapped guarantee | |||||

Guarantee | No fixed monetary limit on guarantor exposure. | Creditor requires full support for business liabilities. | Broad | Medium | Sometimes |

Limited guarantee | |||||

Specific obligation guarantee | Restricts liability by amount, time, obligation or assets. | Guarantor supports only rent arrears under one lease. | Narrow | Medium | Sometimes |

Unlimited guarantee | |||||

Guarantee and indemnity | Covers all guaranteed liabilities without a stated cap. | Owner-manager guarantees company banking liabilities. | Broad | High | Yes |

Joint guarantee | |||||

Guarantee | Guarantors are liable together as one collective party. | Two shareholders jointly guarantee one company debt. | Moderate | Medium | Sometimes |

Joint and several guarantee | |||||

Guarantee and indemnity | Each guarantor may be pursued for the whole liability. | Multiple directors guarantee the same borrowing. | Broad | Medium | Yes |

Several-only guarantee | |||||

Guarantee | Each guarantor is liable only for an agreed share. | Investors guarantee debt pro rata to shareholding. | Narrow | Medium | Sometimes |

Several capped guarantee | |||||

Guarantee | Each guarantor has an individual maximum liability cap. | Minority shareholders accept different exposure caps. | Narrow | Medium | Sometimes |

Pro rata guarantee | |||||

Guarantee | Liability is divided by agreed percentages or shares. | Consortium owners guarantee obligations by ownership share. | Narrow | Medium | Sometimes |

Secured personal guarantee | |||||

Guarantee and indemnity | Guarantee backed by security over guarantor assets. | Lender takes a charge over guarantor property. | Broad | High | Yes |

Unsecured personal guarantee | |||||

Guarantee | Guarantee not supported by specific collateral. | Trade supplier obtains a director's signed guarantee. | Moderate | Low | Sometimes |

Director's personal guarantee | |||||

Guarantee and indemnity | A director personally supports company obligations. | Company loan or supplier credit for an SME. | Broad | Medium | Sometimes |

Shareholder guarantee | |||||

Guarantee | A shareholder guarantees company or joint venture liabilities. | Investor supports borrowing by a portfolio company. | Moderate | Medium | Sometimes |

Parent company guarantee | |||||

Guarantee and indemnity | Parent supports a subsidiary's contractual performance or debts. | Public-sector customer requires group support for supplier obligations. | Broad | High | Yes |

Performance guarantee | |||||

Specific obligation guarantee | Guarantees performance of contractual duties, not just payment. | Parent guarantees contractor delivery obligations. | Moderate | High | Sometimes |

Payment guarantee | |||||

Specific obligation guarantee | Guarantees payment of money due by the principal debtor. | Guarantor covers unpaid invoices or loan instalments. | Moderate | Low | Sometimes |

Rent guarantee | |||||

Specific obligation guarantee | Guarantees tenant rent and sometimes lease covenants. | Landlord requires a guarantor for a commercial tenant. | Moderate | Medium | Sometimes |

Authorised guarantee agreement | |||||

Specific obligation guarantee | Outgoing tenant guarantees assignee's lease covenant performance. | Commercial lease assignment requires an AGA. | Moderate | High | Sometimes |

Lease covenant guarantee | |||||

Guarantee | Guarantees tenant compliance with lease covenants. | Guarantor supports repair, rent and service charge duties. | Broad | High | Sometimes |

Loan repayment guarantee | |||||

Specific obligation guarantee | Guarantees repayment of a specified loan facility. | Director guarantees company term loan repayments. | Moderate | Medium | Sometimes |

Overdraft guarantee | |||||

Continuing guarantee | Covers fluctuating overdraft indebtedness within agreed terms. | Bank requires owner support for business overdraft. | Broad | Medium | Yes |

Revolving credit guarantee | |||||

Continuing guarantee | Supports borrowings that can be drawn, repaid and redrawn. | Company working-capital facility backed by directors. | Broad | High | Yes |

Trade credit guarantee | |||||

Continuing guarantee | Guarantees debts arising on a supplier credit account. | Wholesaler requires director guarantee for goods supplied. | Broad | Medium | Yes |

Invoice-specific guarantee | |||||

Specific obligation guarantee | Guarantees payment of one or more identified invoices. | Supplier extends credit for a single large order. | Narrow | Low | No |

Hire purchase guarantee | |||||

Specific obligation guarantee | Guarantees instalments and liabilities under hire purchase terms. | Business equipment finance backed by a director. | Moderate | Medium | Sometimes |

Equipment lease finance guarantee | |||||

Specific obligation guarantee | Guarantees rental and default sums under equipment leasing. | Company leases machinery with director support. | Moderate | Medium | Sometimes |

Factoring facility guarantee | |||||

Continuing guarantee | Guarantees client liabilities to an invoice finance provider. | Director supports recourse factoring obligations. | Broad | High | Yes |

Invoice discounting guarantee | |||||

Continuing guarantee | Supports liabilities under invoice discounting arrangements. | SME invoice finance facility backed by directors. | Broad | High | Yes |

Bond counter-indemnity | |||||

Indemnity | Indemnifies a bond issuer for payments made under a bond. | Contractor indemnifies surety issuing a performance bond. | Broad | High | Yes |

Performance bond | |||||

Indemnity | Bond provider pays on contractor default or stated trigger. | Construction employer requires bond for project completion risk. | Moderate | High | Sometimes |

On-demand guarantee | |||||

Indemnity | Requires payment on compliant demand, often without proving default first. | Bank or parent issues security for contract obligations. | Broad | High | Yes |

Conditional guarantee | |||||

Guarantee | Liability arises only after specified conditions are met. | Creditor must first demand payment from principal debtor. | Narrow | Medium | Sometimes |

Demand guarantee | |||||

Guarantee and indemnity | Guarantor must pay after a valid contractual demand. | Lender serves demand after borrower event of default. | Broad | High | Yes |

See-to-it guarantee | |||||

Guarantee | Guarantor undertakes that the principal debtor will perform. | Parent promises subsidiary will meet contractual obligations. | Moderate | High | Sometimes |

Responsible obligor covenant | |||||

Indemnity | Promisor assumes responsibility for another party's performance outcome. | Group company accepts liability if subsidiary fails to perform. | Broad | High | Sometimes |

Time-limited guarantee | |||||

Specific obligation guarantee | Liability applies only during a defined period. | Guarantee expires after initial lease term or project phase. | Narrow | Low | No |

Single transaction guarantee | |||||

Specific obligation guarantee | Covers obligations from one defined transaction only. | Guarantee for a one-off equipment purchase. | Narrow | Low | No |

Facility-specific continuing guarantee | |||||

Continuing guarantee | Continues for all liabilities under one named facility. | Guarantee covers all drawings under a revolving facility. | Moderate | Medium | Yes |

Future advances guarantee | |||||

All monies guarantee | Covers advances or credit provided after signature. | Bank may increase or renew facilities later. | Broad | High | Yes |

Fixed sum guarantee | |||||

Specific obligation guarantee | Guarantees a defined sum rather than fluctuating liabilities. | Guarantee of a deposit balance or settlement sum. | Narrow | Low | No |

Principal, interest and costs guarantee | |||||

Guarantee and indemnity | Covers debt plus interest, default interest and enforcement costs. | Lender wants recovery beyond unpaid principal. | Broad | Medium | Sometimes |

Net loss guarantee | |||||

Indemnity | Covers loss remaining after recoveries and mitigation. | Commercial indemnity after asset realisation or insurance recovery. | Moderate | High | Sometimes |

First-loss guarantee | |||||

Indemnity | Guarantor absorbs initial losses up to an agreed layer. | Credit support for a portfolio or receivables facility. | Moderate | High | Sometimes |

Shortfall guarantee | |||||

Guarantee and indemnity | Covers any deficit after collateral or debtor payments. | Property loan where sale proceeds may not repay debt. | Moderate | Medium | Sometimes |

Deficiency guarantee | |||||

Guarantee and indemnity | Covers remaining debt after enforcement against primary assets. | Lender enforces property security before claiming balance. | Moderate | Medium | Sometimes |

Completion guarantee | |||||

Specific obligation guarantee | Guarantees completion of a project, sale or works. | Developer guarantees practical completion of building works. | Moderate | High | Sometimes |

Construction contract guarantee | |||||

Guarantee and indemnity | Guarantees contractor payment, performance or defect obligations. | Parent company supports a building contractor's obligations. | Broad | High | Yes |

Defects liability guarantee | |||||

Specific obligation guarantee | Covers correction of defects after completion. | Contractor's parent guarantees snagging and defects obligations. | Moderate | Medium | Sometimes |

Retention release guarantee | |||||

Indemnity | Secures employer if retained construction money is released early. | Contractor gives bond to obtain retention release. | Narrow | Medium | No |

Advance payment guarantee | |||||

Indemnity | Secures repayment if advance funds are not properly earned. | Customer pays mobilisation money before works begin. | Moderate | Medium | No |

Warranty obligation guarantee | |||||

Specific obligation guarantee | Guarantees warranty, repair or replacement obligations. | Parent supports product warranty obligations of subsidiary seller. | Moderate | Medium | Sometimes |

Deferred consideration guarantee | |||||

Specific obligation guarantee | Guarantees payment of deferred purchase price. | Buyer's parent guarantees earn-out or deferred consideration. | Moderate | High | Sometimes |

Share purchase agreement guarantee | |||||

Guarantee and indemnity | Guarantees buyer or seller obligations under an SPA. | Parent guarantees buyer payment and completion obligations. | Moderate | High | Sometimes |

Tax indemnity support | |||||

Indemnity | Supports liability for defined tax losses or claims. | Seller indemnifies buyer for pre-completion tax exposure. | Moderate | High | Sometimes |

Regulated consumer credit guarantee | |||||

Guarantee | Guarantee linked to regulated consumer credit obligations. | Individual guarantees another individual's regulated credit agreement. | Moderate | High | Sometimes |

Business loan personal guarantee | |||||

Guarantee and indemnity | Individual guarantees business borrowing, often for an SME. | Bank requires director guarantee for company finance. | Broad | High | Yes |

Supplier account personal guarantee | |||||

Continuing guarantee | Personal guarantee for a company's ongoing supplier account. | Builder's merchant gives company a monthly trade account. | Broad | Medium | Yes |

Settlement payment guarantee | |||||

Specific obligation guarantee | Guarantees payment obligations under a settlement agreement. | Third party guarantees staged settlement instalments. | Narrow | Low | No |

Adverse costs indemnity | |||||

Indemnity | Indemnifies against adverse litigation costs exposure. | Funder or insurer supports claimant's costs risk. | Moderate | High | Sometimes |

Cross-guarantee | |||||

Guarantee and indemnity | Two or more parties guarantee each other's liabilities. | Group companies support shared banking facilities. | Broad | High | Yes |

Upstream guarantee | |||||

Guarantee and indemnity | Subsidiary guarantees obligations of its parent company. | Group financing supported by operating subsidiaries. | Broad | High | Yes |

Downstream guarantee | |||||

Guarantee and indemnity | Parent guarantees obligations of its subsidiary. | Parent supports subsidiary loan, lease or supply contract. | Broad | Medium | Yes |

Sister company guarantee | |||||

Guarantee and indemnity | One group company guarantees another group company's obligations. | Trading subsidiary supports affiliate's supply obligations. | Broad | High | Yes |

Variation-proof guarantee | |||||

Continuing guarantee | Drafted to survive variations to underlying obligations. | Loan terms may be amended after guarantee signing. | Broad | High | Yes |

Strict secondary guarantee | |||||

Guarantee | May be discharged by material unauthorised variations. | Old-form guarantee lacks consent-to-variation wording. | Narrow | High | No |

Insolvency-proof indemnity | |||||

Indemnity | Covers loss if debtor obligations are void, avoided or unenforceable. | Lender protects against borrower insolvency arguments. | Broad | High | Yes |

Reinstatement guarantee | |||||

Continuing guarantee | Revives liability if payments are later clawed back. | Borrower payment is challenged as an insolvency preference. | Broad | High | Yes |

Principal debtor clause guarantee | |||||

Guarantee and indemnity | Makes guarantor liable as if primary debtor. | Creditor wants direct claim without procedural defences. | Broad | High | Yes |

Principal-only guarantee | |||||

Specific obligation guarantee | Covers principal debt but excludes interest and costs. | Guarantor negotiates limited loan support. | Narrow | Low | No |

Enforcement costs guarantee | |||||

Guarantee and indemnity | Includes legal and recovery costs incurred enforcing obligations. | Lender claims debt plus solicitors' fees after default. | Broad | Medium | Sometimes |

Subordinated recourse guarantee | |||||

Guarantee and indemnity | Restricts guarantor recourse until creditor is paid in full. | Bank prevents guarantor competing in borrower insolvency. | Broad | High | Yes |

Postponed contribution guarantee | |||||

Continuing guarantee | Delays guarantor contribution claims against co-guarantors. | Multiple guarantors sign a creditor-friendly facility guarantee. | Broad | High | Yes |

Security-preserving guarantee | |||||

Continuing guarantee | States liability survives release, exchange or loss of security. | Lender may vary collateral package over facility life. | Broad | High | Yes |

Asset-limited guarantee | |||||

Guarantee | Recovery is limited to specified assets or collateral. | Guarantor limits recourse to a charged property. | Narrow | High | Sometimes |

Non-recourse carve-out guarantee | |||||

Indemnity | Liability arises only for specified bad acts or carve-outs. | Property finance sponsor covers fraud or prohibited disposals. | Narrow | High | Sometimes |

Bad acts guarantee | |||||

Indemnity | Covers losses caused by fraud, misconduct or prohibited acts. | Sponsor indemnifies lender for borrower fraud or asset stripping. | Narrow | High | Sometimes |

Environmental indemnity | |||||

Indemnity | Covers contamination, clean-up or environmental liability losses. | Property buyer or lender seeks support for contamination risks. | Broad | High | Yes |

Data breach indemnity | |||||

Indemnity | Covers losses from data protection breaches or claims. | Processor indemnifies controller for breach-related costs. | Moderate | High | Sometimes |

Employment liabilities indemnity | |||||

Indemnity | Covers employment liabilities, often linked to staff transfers. | Outsourcing contract includes TUPE indemnity protection. | Moderate | High | Sometimes |

IP infringement indemnity | |||||

Indemnity | Covers losses from intellectual property infringement claims. | Software supplier indemnifies customer for third-party IP claims. | Moderate | High | Sometimes |

Title indemnity | |||||

Indemnity | Covers losses from title defects or ownership issues. | Seller indemnifies buyer for unresolved property title risk. | Moderate | High | Sometimes |

Undertaking-backed indemnity | |||||

Indemnity | Indemnity supports performance of a professional undertaking. | Completion undertaking backed by firm or client indemnity. | Moderate | High | Sometimes |

Deed of guarantee | |||||

Guarantee | Guarantee executed as a deed, often without consideration issues. | Commercial guarantee signed with deed formalities. | Moderate | Medium | Sometimes |

Simple contract guarantee | |||||

Guarantee | Written signed guarantee supported by contractual consideration. | Supplier guarantee signed as part of a credit application. | Moderate | Medium | Sometimes |

Oral guarantee risk | |||||

Guarantee | Promise to answer for another's debt without signed writing. | Informal assurance given to a creditor by phone or email. | Narrow | High | No |

Electronically signed guarantee | |||||

Guarantee | Guarantee signed using an electronic signature method. | Director signs a guarantee through an e-signing platform. | Moderate | Medium | Sometimes |

Which Type Of Personal Guarantee Is Riskiest In The UK?

All monies, continuing, and guarantee and indemnity structures are usually the broadest and most creditor-friendly forms. They may cover future advances, varied facilities, interest, costs, enforcement expenses and, where drafted as a primary indemnity, losses that might not be recoverable under a pure secondary guarantee.

Why Does The Difference Between A Guarantee And An Indemnity Matter?

A guarantee is usually a secondary obligation: the guarantor answers for another party\'s default. An indemnity is usually a primary obligation: the indemnifier promises to protect the beneficiary against specified loss. In practice, many UK commercial forms combine both to reduce arguments about invalidity, variation, release of the principal debtor, or discharge of the guarantee.

When Should A Guarantee Be Narrowly Drafted?

- Use a specific obligation guarantee where the intended risk is limited to one loan, lease, invoice, contract, milestone or payment obligation.

- Use a capped guarantee where the guarantor will accept liability only up to a stated amount, often plus interest and enforcement costs if expressly included.

- Use a time-limited guarantee or single transaction guarantee where the commercial exposure should end on a clear date or after a defined deal.

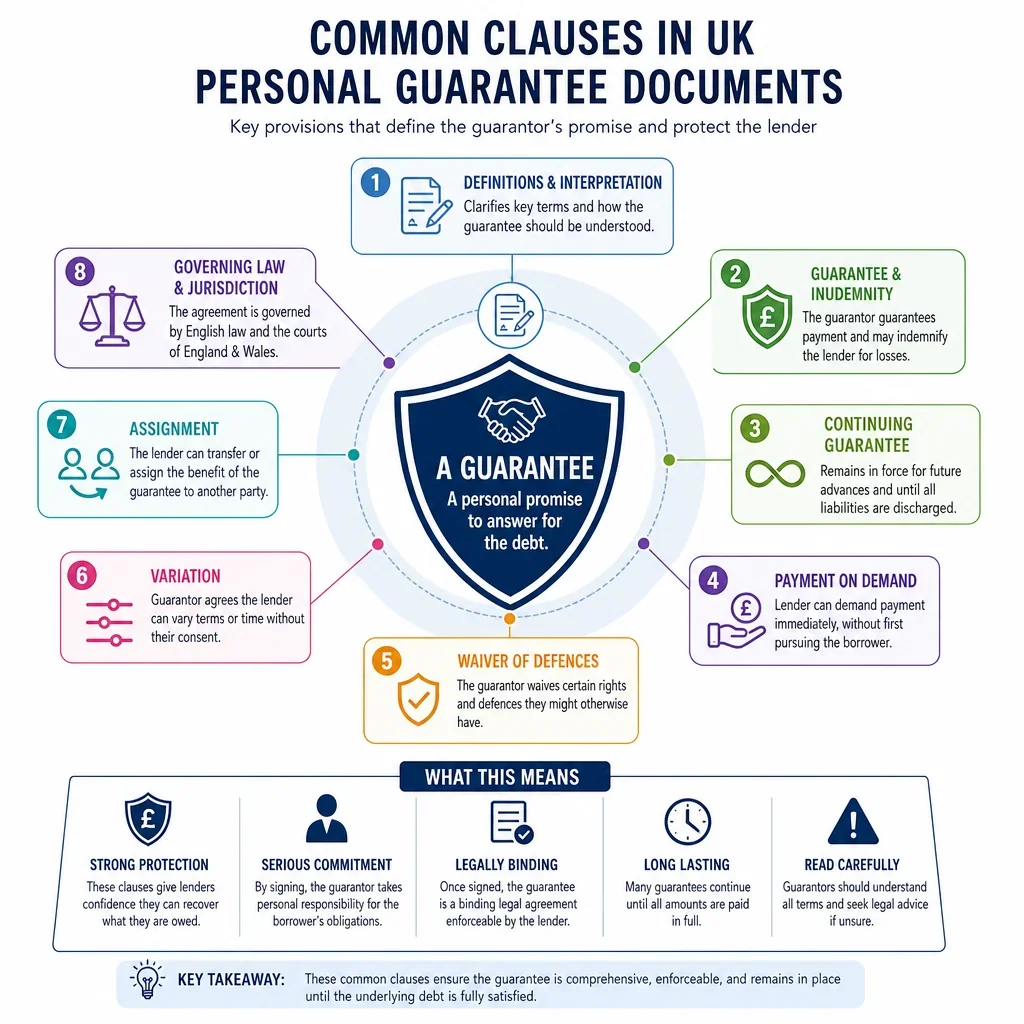

What Drafting Points Most Affect Enforceability?

For UK use, personal guarantees should normally be in writing and signed, because section 4 of the Statute of Frauds 1677 requires a signed written memorandum for a promise to answer for another\'s debt, default or miscarriage. Guarantees should also state whether liability is capped, continuing, all-monies, secured, joint and several, or supported by an indemnity.

What Should Individual Guarantors Check Before Signing?

- Whether the document is a simple guarantee or a broader guarantee and indemnity.

- Whether it is all monies and can catch future or replacement facilities.

- Whether it continues despite variations, renewals, extensions, insolvency or release of security.

- Whether liability is unlimited, capped, joint and several, or supported by security over the guarantor\'s home or other assets.

FAQs

You Might Also Be Interested In