Common Clauses In UK Personal Guarantee Documents

Clause Category | Clause Purpose | Inclusion Level | Importance for Guarantor | Importance for Beneficiary | Risk Impact |

|---|---|---|---|---|---|

Operative Guarantee | |||||

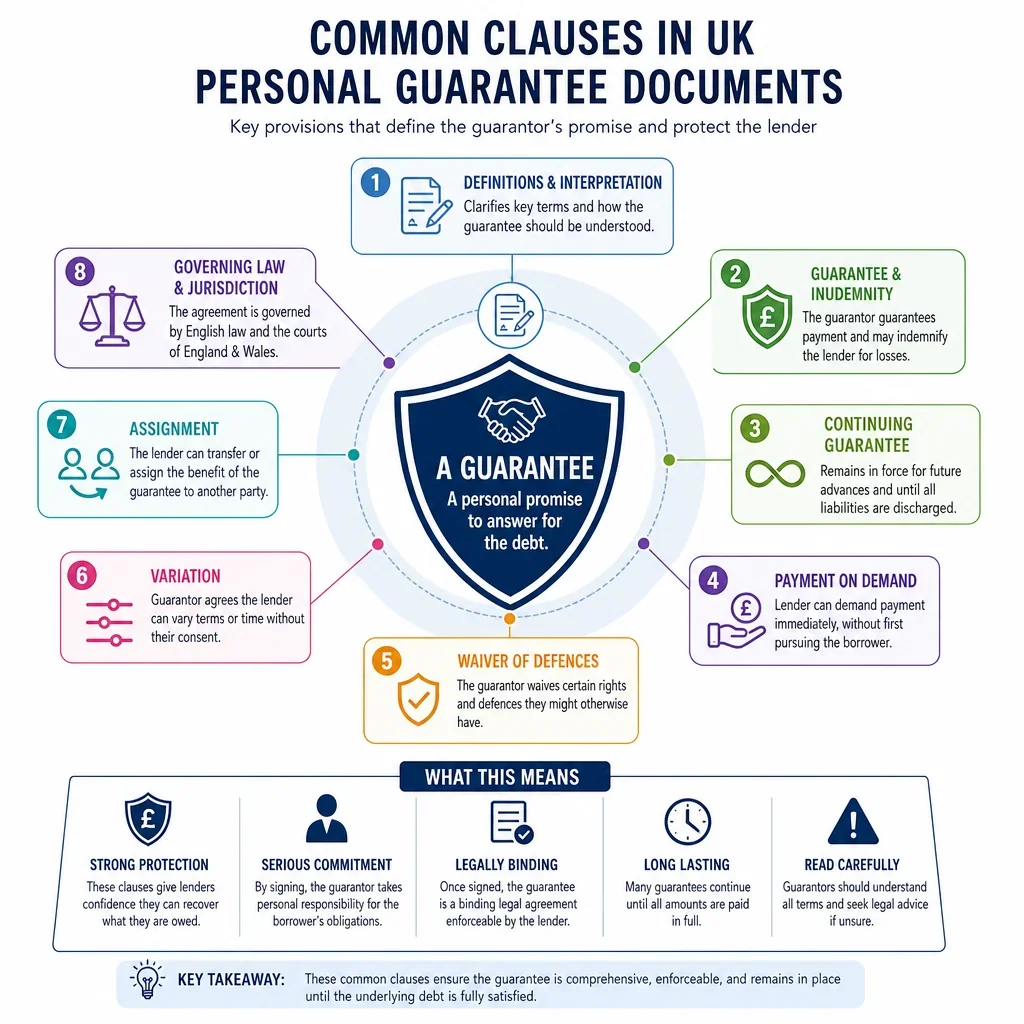

Core guarantee obligation | Creates the guarantor's promise to answer for the debtor's obligations. | Usually essential | Defines the basic personal liability being accepted. | Forms the main contractual right to claim against the guarantor. | High |

Indemnity | |||||

Core guarantee obligation | Requires the guarantor to compensate the beneficiary for losses if the debtor fails to pay or perform. | Often included | May create primary liability wider than a pure guarantee. | Helps preserve recovery if the guarantee obligation is challenged. | High |

Payment On Demand | |||||

Payment and demand | Requires payment by the guarantor after a demand from the beneficiary. | Usually essential | Can trigger immediate payment pressure after written demand. | Provides a clear mechanism for enforcing payment. | High |

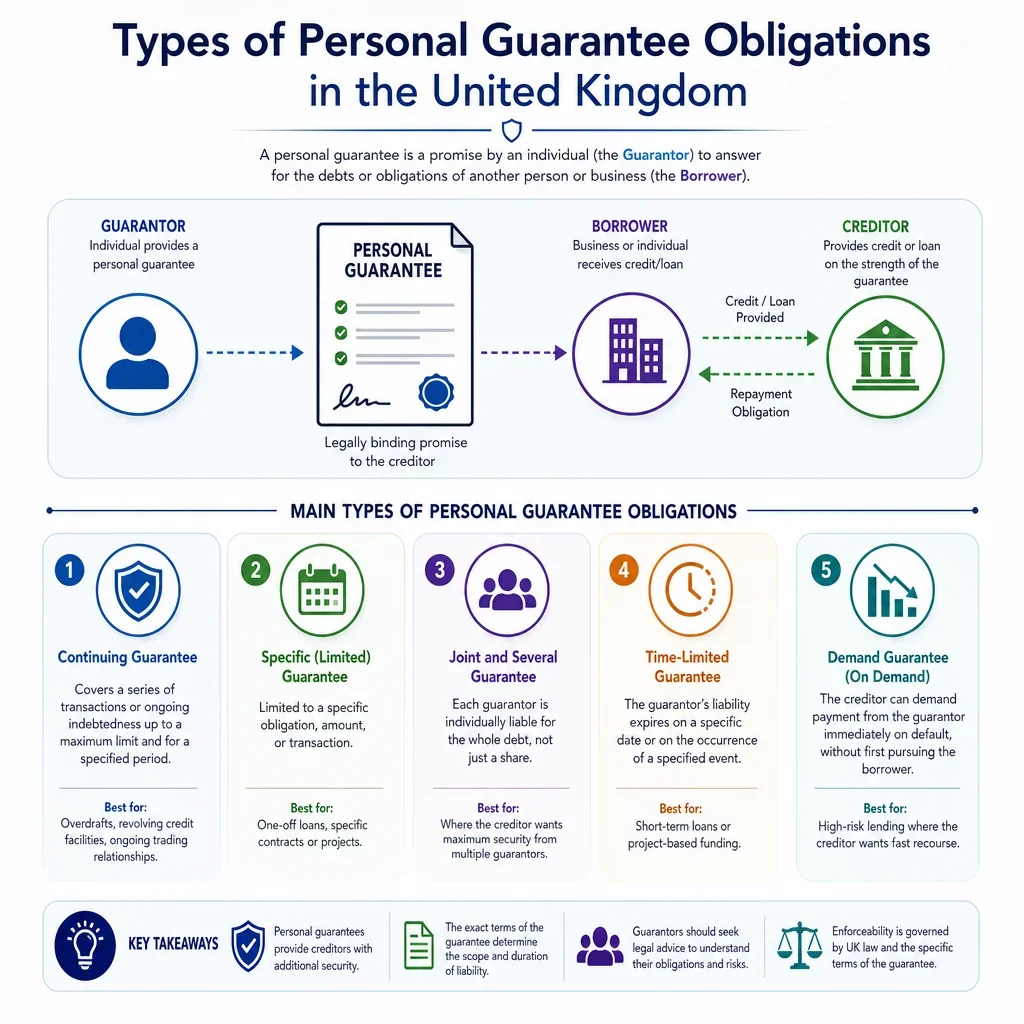

Continuing Guarantee | |||||

Core guarantee obligation | Keeps the guarantee in force for ongoing or future obligations until discharged. | Often included | Can extend liability beyond a single transaction or invoice. | Supports revolving credit, rolling trade accounts and ongoing facilities. | High |

All Monies Guarantee | |||||

Core guarantee obligation | Covers all sums owed by the debtor to the beneficiary, not only named liabilities. | Context specific | May greatly widen exposure to unrelated or future debts. | Maximises coverage across accounts, facilities and obligations. | High |

Specific Obligations Covered | |||||

Liability limitation | Limits the guarantee to identified debts, agreements or facilities. | Often included | Prevents liability spreading to unknown or future debts. | Reduces ambiguity about what is secured. | High |

Maximum Liability Cap | |||||

Liability limitation | Caps the total amount recoverable from the guarantor. | Often included | Provides a financial ceiling on personal exposure. | Clarifies recoverable amount and may make the guarantee more acceptable. | High |

Interest On Guaranteed Amounts | |||||

Payment and demand | Applies interest to unpaid guaranteed sums after default or demand. | Often included | Can increase the debt rapidly after default. | Compensates for delay in receiving payment. | Medium |

Costs And Expenses | |||||

Payment and demand | Makes the guarantor liable for enforcement, recovery and legal costs. | Often included | Adds enforcement costs to the underlying debt. | Improves recovery of collection and legal expenditure. | Medium |

Tax Gross-Up | |||||

Payment and demand | Requires payments to be increased if withholding or deductions apply. | Context specific | Can increase the amount payable beyond the headline debt. | Ensures receipt of the intended net amount. | Medium |

No Set-Off Or Deductions | |||||

Payment and demand | Requires payment without set-off, counterclaim, withholding or deduction. | Often included | Limits ability to reduce payment using cross-claims. | Supports prompt gross recovery after demand. | High |

Demand Notice Requirements | |||||

Payment and demand | Specifies how a demand must be made and what it must contain. | Often included | Creates procedural safeguards before payment is due. | Reduces disputes about whether a valid demand was served. | Medium |

Payment Currency | |||||

Payment and demand | States the currency in which guaranteed sums must be paid. | Context specific | Can expose the guarantor to exchange-rate risk. | Protects against currency mismatch and shortfall. | Medium |

Payment Method And Account | |||||

Payment and demand | Identifies how and where the guarantor must make payment. | Optional | Reduces risk of failed or misdirected payment. | Supports efficient collection of demanded sums. | Low |

Time Limit Or Expiry Date | |||||

Liability limitation | Limits the period during which the guarantee applies or demands may be made. | Context specific | Prevents indefinite personal exposure if drafted clearly. | May define enforcement deadlines and monitoring needs. | High |

Termination By Guarantor | |||||

Guarantor protection | Allows the guarantor to end liability for future obligations by notice. | Context specific | Gives a route to stop future liability building up. | Preserves liability for existing debts while ending future cover. | High |

Several Liability | |||||

Liability limitation | Limits each guarantor to their own stated share of liability. | Context specific | Avoids responsibility for other guarantors' shares. | May reduce flexibility compared with joint and several liability. | High |

Joint And Several Liability | |||||

Core guarantee obligation | Makes each guarantor liable for the whole guaranteed amount as well as collectively. | Context specific | The beneficiary may pursue one guarantor for all sums. | Improves recovery options where multiple guarantors exist. | High |

Proportionate Guarantee | |||||

Liability limitation | Restricts liability to a fixed percentage or stated proportion of the debt. | Context specific | Controls exposure where several owners or directors give guarantees. | May be acceptable if aligned with ownership or risk allocation. | High |

Principal Debtor Liability | |||||

Creditor protection | Treats the guarantor as primarily liable if the guarantee is ineffective as a secondary obligation. | Often included | May reduce protections normally linked to secondary liability. | Strengthens enforceability if the underlying obligation is defective. | High |

Waiver Of Guarantor Defences | |||||

Creditor protection | Prevents reliance on common defences arising from dealings with the debtor or security. | Often included | Can remove arguments that might otherwise reduce or discharge liability. | Reduces enforcement risk caused by technical discharge arguments. | High |

Consent To Variations | |||||

Creditor protection | Keeps the guarantee effective despite amendments to the underlying obligation. | Often included | May bind the guarantor to changed debtor arrangements. | Allows commercial flexibility without losing guarantee support. | High |

Extension Of Time For Debtor | |||||

Creditor protection | Preserves liability if the beneficiary gives the debtor extra time to pay or perform. | Often included | Prevents discharge merely because the debtor receives indulgence. | Allows forbearance or restructuring without releasing the guarantor. | High |

Release Or Compromise Of Debtor | |||||

Creditor protection | Preserves guarantor liability despite settlement, compromise or release involving the debtor. | Context specific | May leave liability even after debtor arrangements change. | Supports settlement with the debtor without losing claims against the guarantor. | High |

Invalidity Of Underlying Obligation | |||||

Creditor protection | Keeps the indemnity or payment obligation alive if the debtor obligation is void or unenforceable. | Often included | May create liability even where the debtor could resist payment. | Protects against defects in the primary contract or debt. | High |

Preservation Of Rights | |||||

Creditor protection | States that rights against the guarantor continue despite acts, omissions or delays. | Often included | Narrows arguments based on beneficiary conduct. | Maintains enforcement rights despite practical administration changes. | High |

No Need To Proceed Against Debtor First | |||||

Enforcement | Allows the beneficiary to claim against the guarantor without first suing the debtor or enforcing security. | Often included | The guarantor may be pursued before the debtor is exhausted. | Speeds recovery and avoids procedural hurdles. | High |

Beneficiary Discretion Over Security | |||||

Enforcement | Lets the beneficiary decide whether and when to enforce other security. | Context specific | May prevent complaints that other security should have been used first. | Preserves strategic control over recovery routes. | Medium |

Continuing Security Despite Payments | |||||

Creditor protection | Keeps the guarantee in force despite interim payments or account reductions. | Often included | Payment by the debtor may not automatically end exposure. | Protects revolving accounts and future advances. | Medium |

Reinstatement After Clawback | |||||

Creditor protection | Revives liability if a payment is later set aside, refunded or clawed back in insolvency. | Often included | Liability can return after an apparent discharge. | Protects against insolvency clawback and similar repayment risks. | High |

Postponement Of Guarantor Claims | |||||

Creditor protection | Subordinates guarantor recovery claims against the debtor until the beneficiary is paid in full. | Often included | Delays reimbursement, contribution or subrogation claims. | Prevents the guarantor competing for debtor assets. | High |

Subrogation Rights Waiver | |||||

Creditor protection | Restricts the guarantor from taking over the beneficiary's rights until full repayment. | Often included | Limits routes to recover from the debtor after paying. | Protects priority and control of enforcement rights. | Medium |

Contribution Between Guarantors | |||||

Guarantor protection | Addresses recovery between co-guarantors after one pays more than their share. | Context specific | Supports fair sharing of loss between co-guarantors. | May be neutral if it does not restrict beneficiary claims. | Medium |

Debtor Insolvency | |||||

Enforcement | Confirms liability may be enforced if the debtor enters insolvency or similar proceedings. | Often included | A borrower insolvency may trigger a claim against personal assets. | Provides an alternative recovery route when debtor recovery is uncertain. | High |

Guarantor Bankruptcy Event | |||||

Enforcement | Addresses consequences if an individual guarantor becomes bankrupt or subject to insolvency proceedings. | Context specific | May accelerate enforcement or affect credit and personal assets. | Helps preserve rights to prove or claim in insolvency. | High |

Guarantor Representations | |||||

Creditor protection | Records statements about authority, solvency, understanding and ability to give the guarantee. | Often included | False statements may create extra breach or misrepresentation risk. | Provides evidential support for enforceability and reliance. | Medium |

Independent Legal Advice Confirmation | |||||

Guarantor protection | Confirms the guarantor had, or was advised to take, independent legal advice. | Context specific | Helps ensure the personal and financial consequences are understood. | Reduces undue influence and non est factum challenge risk. | High |

Undue Influence Warning | |||||

Guarantor protection | Records that the guarantor signs freely and understands the risk of guaranteeing another's debt. | Context specific | Highlights pressure and relationship risk before signing. | Helps address enforceability concerns in non-commercial relationship cases. | High |

Financial Information Acknowledgement | |||||

Guarantor protection | Acknowledges what debtor, facility or financial information the guarantor has reviewed. | Optional | Encourages assessment of the debtor's real repayment risk. | Creates evidence that the guarantor knew the commercial context. | Medium |

Capacity And Authority | |||||

Execution | Confirms the guarantor has legal capacity and authority to enter the guarantee. | Often included | Raises issues for trustees, partners, attorneys and corporate signatories. | Supports validity and reduces authority challenges. | High |

Execution As A Deed | |||||

Execution | Provides formal deed execution to support enforceability and limitation treatment. | Often included | A deed can be enforceable without consideration and for longer limitation periods. | Avoids consideration issues and supports stronger formal enforceability. | High |

Witness Attestation | |||||

Execution | Provides for an individual guarantor's deed signature to be witnessed. | Usually essential | Improper witnessing may create execution disputes. | Helps prove valid execution of a deed by an individual. | High |

Delivery Of Deed | |||||

Execution | States when the deed becomes delivered and legally effective. | Often included | Controls when binding liability starts. | Reduces uncertainty about commencement of enforceability. | Medium |

Company Execution Block | |||||

Execution | Sets out how a corporate guarantor signs under the Companies Act execution rules. | Context specific | Corporate signatories must have authority to bind the company. | Supports valid execution by a corporate guarantor. | High |

Counterparts | |||||

Execution | Allows separate signed copies to together form one binding document. | Optional | Useful where parties sign in different locations. | Facilitates practical completion of multi-party guarantees. | Low |

Electronic Signature | |||||

Execution | Allows signature by electronic means where legally acceptable and properly evidenced. | Optional | Requires care over identity, consent, witnessing and delivery. | Supports remote signing and evidential admissibility of e-signatures. | Medium |

Governing Law | |||||

Boilerplate | States which law governs the guarantee, commonly England and Wales, Scotland or Northern Ireland. | Usually essential | Determines the legal rules used to interpret liability. | Reduces uncertainty over applicable law and enforcement basis. | High |

Jurisdiction | |||||

Boilerplate | Identifies which courts may hear disputes about the guarantee. | Usually essential | Affects where the guarantor may have to defend proceedings. | Provides a predictable forum for enforcement proceedings. | High |

Service Of Process | |||||

Enforcement | Specifies how legal proceedings or court documents may be served. | Context specific | Important if the guarantor lives outside the chosen jurisdiction. | Simplifies enforcement against overseas or hard-to-reach guarantors. | Medium |

Notices | |||||

Boilerplate | Sets rules for giving formal notices, including demands and termination notices. | Usually essential | Controls whether notices are deemed received even if not actually read. | Provides a reliable method for demands and enforcement communications. | Medium |

Change Of Address Notification | |||||

Boilerplate | Requires parties to notify changes to their contact details. | Optional | Failure to update details may mean missing a demand. | Keeps service and demand details current. | Low |

Assignment By Beneficiary | |||||

Creditor protection | Allows the beneficiary to transfer guarantee rights to another lender, buyer or assignee. | Often included | The guarantor may owe obligations to a new creditor. | Supports refinancing, debt sale and business transfer transactions. | Medium |

No Assignment By Guarantor | |||||

Creditor protection | Prevents the guarantor transferring obligations without consent. | Often included | Personal obligations usually cannot be shifted to someone else. | Keeps recourse against the assessed guarantor. | Low |

Amendments In Writing | |||||

Boilerplate | Requires changes to the guarantee to be made formally in writing. | Often included | Helps prevent informal increases or changes to liability. | Reduces disputes about oral variations. | Medium |

Entire Agreement | |||||

Boilerplate | States that the written guarantee contains the complete agreement between the parties. | Often included | May limit reliance on side statements or assurances. | Reduces disputes based on alleged prior statements. | Medium |

Severance | |||||

Boilerplate | Keeps the rest of the guarantee effective if one provision is invalid or unenforceable. | Often included | Invalid wording may be removed while other liabilities remain. | Protects the document from total failure due to one bad clause. | Medium |

No Waiver | |||||

Creditor protection | Prevents delay or partial enforcement from being treated as loss of rights. | Often included | Creditor delay may not release or reduce liability. | Preserves rights while negotiating or delaying enforcement. | Medium |

Cumulative Rights | |||||

Creditor protection | States that contractual rights are additional to other legal rights and remedies. | Optional | The beneficiary may rely on several remedies at once. | Avoids arguments that one remedy excludes another. | Low |

Third Party Rights Exclusion | |||||

Boilerplate | Excludes or controls rights of non-parties under the Contracts (Rights of Third Parties) Act 1999. | Often included | Clarifies who can enforce the guarantee. | Prevents unintended enforcement by third parties. | Low |

Data Protection Consent | |||||

Boilerplate | Explains or supports processing of guarantor personal data for credit and enforcement purposes. | Context specific | Personal and credit information may be checked and shared. | Supports lawful administration, credit assessment and recovery records. | Medium |

Confidentiality | |||||

Boilerplate | Restricts disclosure of the guarantee and related financial information. | Optional | May restrict sharing the document except with advisers. | Protects commercial and financial information. | Low |

Consumer Credit Compliance | |||||

Guarantor protection | Addresses regulated consumer credit issues where the guarantee supports a consumer credit agreement. | Context specific | Regulated credit may give statutory protections and formal requirements. | Non-compliance can create enforcement problems in regulated cases. | High |

Fairness And Transparency Acknowledgement | |||||

Guarantor protection | Supports clear drafting and awareness of potentially onerous guarantee terms. | Context specific | Important where the guarantor may be treated as a consumer. | Transparent wording reduces unfairness and enforceability challenges. | High |

Limitation Period Awareness | |||||

Enforcement | Highlights when claims may become time-barred, especially under simple contract or deed limitation rules. | Optional | Time limits may affect whether old guarantee claims can be pursued. | Helps manage enforcement deadlines and document retention. | Medium |

Conclusive Evidence Certificate | |||||

Enforcement | Allows a creditor certificate of debt to be evidence, or conclusive evidence, of amounts due. | Context specific | May make it harder to dispute the amount claimed. | Simplifies proof of debt in enforcement. | High |

Statement Of Account Evidence | |||||

Enforcement | Treats the beneficiary's account records as evidence of the debtor's liability. | Optional | Requires checking creditor statements carefully and promptly. | Creates evidential support for the amount demanded. | Medium |

Material Adverse Change | |||||

Enforcement | Allows action if the guarantor's financial position materially worsens. | Context specific | Financial deterioration may trigger review or enforcement rights. | Provides early warning and protection against guarantor credit decline. | Medium |

Negative Pledge By Guarantor | |||||

Creditor protection | Restricts the guarantor from granting competing security over assets. | Context specific | Limits ability to borrow against personal or business assets. | Helps preserve asset value available for recovery. | Medium |

Restriction On Asset Disposals | |||||

Creditor protection | Limits significant disposals of guarantor assets while the guarantee is outstanding. | Context specific | Can restrict personal financial planning or business transactions. | Reduces risk of asset stripping before enforcement. | Medium |

Information Undertakings | |||||

Creditor protection | Requires the guarantor to provide financial information or updates when requested. | Context specific | Creates ongoing disclosure duties beyond signing. | Helps monitor guarantor creditworthiness and enforcement prospects. | Medium |

Insurance Undertaking | |||||

Creditor protection | Requires relevant insurance to be maintained for assets or business risks affecting repayment. | Context specific | May add ongoing insurance cost and compliance duties. | Protects recovery prospects where asset value matters. | Low |

Guarantor Death Or Estate Liability | |||||

Enforcement | States whether obligations continue against the guarantor's estate after death. | Context specific | May affect estate planning and beneficiaries. | Preserves claims where the guarantor dies before discharge. | High |

Spouse Or Occupier Consent | |||||

Guarantor protection | Records consent or awareness from a spouse, occupier or co-owner where home assets may be affected. | Context specific | Highlights risk to family home or shared assets. | Reduces priority and undue influence complications involving home interests. | High |

Security For Guarantee | |||||

Creditor protection | Links the guarantee to collateral such as a legal charge, debenture or other security. | Context specific | Can put specific assets, including property, directly at risk. | Improves recovery prospects beyond an unsecured personal claim. | High |

Release Of Guarantor | |||||

Guarantor protection | States when the guarantor is discharged, such as full repayment or written release. | Often included | Confirms how personal liability ends. | Avoids accidental release before all secured liabilities are satisfied. | High |

Partial Release | |||||

Guarantor protection | Allows liability to reduce or release in stages as milestones or payments occur. | Optional | Can reduce exposure over time if conditions are met. | Can align security reduction with repayment progress. | Medium |

Survival Of Obligations | |||||

Creditor protection | Keeps selected obligations effective after termination, repayment or document expiry. | Optional | Some duties may continue after the main guarantee ends. | Preserves repayment, cost, confidentiality or clawback protections. | Medium |

Interpretation And Definitions | |||||

Boilerplate | Defines key terms such as debtor, liabilities, guaranteed obligations and beneficiary. | Usually essential | Definitions often determine the real width of liability. | Precise definitions reduce disputes about coverage. | High |

Business Day Convention | |||||

Boilerplate | Defines how deadlines move when they fall on weekends or bank holidays. | Optional | Affects demand response and payment deadlines. | Clarifies timing of notices, demands and payments. | Low |

Sanctions And AML Compliance | |||||

Creditor protection | Requires compliance with sanctions, anti-money laundering and financial crime requirements. | Context specific | May require identity checks and lawful source of funds evidence. | Supports compliance screening and lawful receipt of payments. | Medium |

What Clauses Matter Most In A UK Personal Guarantee?

The highest-risk clauses are usually the operative guarantee, indemnity, continuing security, all monies wording, payment on demand, and principal debtor clauses. Together, these can make the guarantor liable quickly, for a wide class of debts, and sometimes even where the underlying borrower obligation is disputed or unenforceable.

How Can A Guarantor Limit Personal Guarantee Risk?

A guarantor should focus on clauses that cap exposure: maximum liability cap, time limit, specific facility wording, termination rights, notice requirements, and exclusions for future variations. These provisions can materially reduce the risk of an open-ended or expanding guarantee.

Why Do Lenders Include Creditor Protection Clauses?

Beneficiaries commonly include waiver of defences, variation consent, preservation of rights, set-off restrictions, and postponement of guarantor claims to stop technical arguments delaying enforcement. These clauses are designed to keep the guarantee enforceable even if the underlying loan, lease, trade credit or other arrangement changes.

What Formalities Are Important For UK Personal Guarantees?

Execution matters. A guarantee is commonly executed as a deed to avoid consideration issues and to support a longer limitation period. UK users should pay close attention to signature blocks, witnessing, delivery, capacity, and, where a company is involved, authority and Companies Act execution requirements.

Can Consumer Or Small Business Guarantees Need Extra Care?

Where a personal guarantee is connected to consumer credit, regulated lending, unfair terms, or a vulnerable guarantor, additional legal issues may arise. Independent legal advice, clear warnings, readable drafting, and evidence that the guarantor understood the risk can be important in reducing later disputes.

FAQs

You Might Also Be Interested In