Personal Guarantee Use Cases In The UK

Transaction Type | Frequency of Use | Typical Guarantor | Typical Beneficiary | Commercial Purpose | Typical Liability Cap | Guarantor Exposure Level |

|---|---|---|---|---|---|---|

SME company term loan | ||||||

Business loan | High | Director or majority shareholder | Bank or business lender | Reduces lender risk where borrower has limited assets. | Either | High |

Business overdraft facility | ||||||

Business loan | High | Company director or owner-manager | Bank | Supports flexible working capital borrowing. | Either | Medium |

Revolving credit facility for SME | ||||||

Business loan | Medium | Director or controlling shareholder | Bank or alternative lender | Backs repeat drawdowns and fluctuating debt. | Either | High |

Start-up or early-stage company borrowing | ||||||

Business loan | High | Founder or director | Bank or start-up lender | Compensates for limited credit history and assets. | Capped | Medium |

Emergency working capital loan | ||||||

Business loan | Medium | Director or business owner | Bank or specialist lender | Supports short-term liquidity during cash pressure. | Either | High |

Unsecured business loan to limited company | ||||||

Business loan | High | Director or shareholder | Unsecured business lender | Substitutes for absent business security. | Capped | Medium |

Secured loan with shortfall guarantee | ||||||

Business loan | Medium | Director or property owner | Secured lender | Covers debt exceeding asset recovery value. | Either | High |

Commercial mortgage for company premises | ||||||

Business loan | Medium | Director-shareholder | Mortgage lender | Strengthens repayment support beyond property security. | Either | High |

Property development finance | ||||||

Business loan | High | Developer principal or director | Development lender | Covers build-cost overruns and repayment shortfalls. | Either | High |

Bridging loan for business property purchase | ||||||

Business loan | Medium | Director or property investor | Bridging lender | Secures short-term funding pending refinance or sale. | Either | High |

Management buyout acquisition finance | ||||||

Business loan | Medium | Buying director or management team member | Acquisition lender | Aligns buyers with acquisition debt risk. | Capped | High |

Peer-to-peer business loan | ||||||

Business loan | Medium | Director or business owner | P2P platform investors or lender | Improves credit support for investor-funded loans. | Capped | Medium |

Commercial lease for limited company tenant | ||||||

Commercial lease | High | Director, shareholder or parent company principal | Commercial landlord | Protects rent, service charge and lease covenants. | Either | High |

Retail shop lease for new trading company | ||||||

Commercial lease | High | Shop owner or director | Retail landlord | Supports rent covenant for unproven tenant. | Either | High |

Restaurant or cafe premises lease | ||||||

Commercial lease | High | Operator, director or franchisee principal | Commercial landlord | Covers rent and dilapidations risk in hospitality. | Either | High |

Office lease for small company | ||||||

Commercial lease | Medium | Director or founder | Office landlord | Supports lease obligations for asset-light tenant. | Either | Medium |

Warehouse or industrial unit lease | ||||||

Commercial lease | Medium | Director or logistics business owner | Industrial landlord | Protects rent, repairs and reinstatement obligations. | Either | High |

Lease assignment with authorised guarantee agreement | ||||||

Commercial lease | Medium | Outgoing tenant director or existing guarantor | Landlord | Supports assignee performance after lease transfer. | Either | High |

Commercial lease guarantee affected by tenant covenant rules | ||||||

Commercial lease | Medium | Lease guarantor | Landlord | Addresses liability on assignment and release issues. | Either | High |

Supplier trade credit account | ||||||

Trade credit | High | Customer company director | Trade supplier | Secures invoices supplied on deferred payment terms. | Either | Medium |

Builders merchant credit account | ||||||

Trade credit | High | Construction company director | Builders merchant | Covers materials supplied before customer payment. | Either | Medium |

Fuel card credit account | ||||||

Trade credit | Medium | Fleet operator director | Fuel card provider | Secures recurring fuel purchases on account. | Capped | Medium |

Wholesale stock supplied on credit | ||||||

Trade credit | High | Retail company director | Wholesaler or distributor | Supports stock supply before resale revenue. | Either | Medium |

IT hardware reseller credit line | ||||||

Trade credit | Medium | Reseller director | Manufacturer or distributor | Covers high-value goods sold on credit terms. | Capped | Medium |

Haulage services paid on monthly account | ||||||

Trade credit | Medium | Customer company director | Haulage provider | Secures ongoing transport charges invoiced later. | Either | Medium |

Hire purchase for business vehicle | ||||||

Asset finance | High | Director or fleet business owner | Asset finance provider | Covers shortfall after repossession and sale. | Either | Medium |

Finance lease for machinery | ||||||

Asset finance | High | Manufacturing company director | Leasing company | Secures rentals and asset value risk. | Either | Medium |

Operating lease for business equipment | ||||||

Asset finance | Medium | Director or owner-manager | Equipment lessor | Covers unpaid rentals and asset return obligations. | Either | Medium |

Company vehicle leasing | ||||||

Asset finance | High | Company director | Vehicle finance company | Secures rentals, damage and early termination sums. | Either | Medium |

Plant and construction equipment hire | ||||||

Asset finance | Medium | Contractor director | Plant hire company | Protects against hire charges and equipment loss. | Either | High |

Invoice factoring facility | ||||||

Invoice finance | High | Director or shareholder | Invoice finance provider | Covers recourse debts and dilution risk. | Either | High |

Confidential invoice discounting facility | ||||||

Invoice finance | High | Company director | Invoice discounter | Supports advances against book debts. | Either | High |

Selective invoice finance | ||||||

Invoice finance | Medium | Director or founder | Invoice finance platform | Secures advances on selected customer invoices. | Capped | Medium |

Ongoing supply of goods to limited company | ||||||

Supply agreement | High | Buyer company director | Goods supplier | Secures payment under recurring purchase orders. | Either | Medium |

Long-term business services contract | ||||||

Supply agreement | Medium | Customer company director | Service provider | Protects fees under ongoing service commitments. | Capped | Medium |

Manufacturing supply agreement with credit terms | ||||||

Supply agreement | Medium | Customer director or group owner | Manufacturer | Covers bespoke stock and unpaid invoices. | Either | Medium |

SaaS subscription for small company | ||||||

Supply agreement | Low | Customer founder or director | Software vendor | Secures subscription fees for fixed contract term. | Capped | Low |

Recruitment agency supply fees | ||||||

Supply agreement | Low | Client company director | Recruitment agency | Secures placement fees where credit risk is high. | Capped | Low |

Franchise agreement for limited company franchisee | ||||||

Franchise agreement | High | Franchisee owner or director | Franchisor | Secures fees, royalties and brand obligations. | Either | High |

Master franchise development agreement | ||||||

Franchise agreement | Medium | Master franchisee principal | Franchisor | Supports territory development and payment obligations. | Either | High |

Multi-unit franchise rollout | ||||||

Franchise agreement | Medium | Franchise group owner | Franchisor | Secures obligations across several outlets. | Either | High |

Hotel franchise or management agreement | ||||||

Franchise agreement | Medium | Hotel company owner or investor | Hotel brand or operator | Secures fees, standards and termination sums. | Either | High |

Company credit card account | ||||||

Other | Medium | Director or business owner | Card issuer | Backs card balances and charges. | Capped | Medium |

Merchant cash advance | ||||||

Other | Medium | Retail or hospitality business owner | Merchant cash advance provider | Supports repayment from future card sales. | Capped | Medium |

Performance bond counter-indemnity | ||||||

Other | Medium | Contractor director or shareholder | Bond provider or surety | Reimburses surety for bond payouts. | Capped | High |

Advance payment bond indemnity | ||||||

Other | Medium | Contractor owner or director | Surety or bond issuer | Covers repayment if bond is called. | Capped | High |

Public contract financial standing support | ||||||

Other | Medium | Parent owner or controlling director | Public authority or contracting body | Supports contractor capacity and performance risk. | Capped | High |

Business utilities supply account | ||||||

Supply agreement | Medium | Director or premises operator | Energy supplier | Secures ongoing energy charges for premises. | Capped | Medium |

Business telecoms or broadband account | ||||||

Supply agreement | Low | Company director | Telecoms provider | Backs recurring charges and early termination fees. | Capped | Low |

Commercial waste services account | ||||||

Supply agreement | Low | Business owner or director | Waste management contractor | Secures recurring service charges. | Capped | Low |

Nursery business lease or loan support | ||||||

Commercial lease, Business loan | Medium | Nursery owner or director | Landlord or lender | Supports premises and funding for regulated childcare. | Either | High |

Care home acquisition or premises finance | ||||||

Business loan, Commercial lease | Medium | Care business owner or director | Lender or landlord | Supports high-value premises and operating risk. | Either | High |

Dental practice acquisition finance | ||||||

Business loan | Medium | Practice buyer or dentist director | Bank or healthcare lender | Supports goodwill-heavy acquisition debt. | Either | High |

Pharmacy acquisition finance | ||||||

Business loan | Medium | Pharmacy owner or director | Bank or healthcare lender | Supports acquisition and regulated premises risk. | Either | High |

Farm input supply credit | ||||||

Trade credit | Medium | Farm company director or partner | Agricultural supplier | Covers seed, feed, fertiliser and chemicals on account. | Either | Medium |

Agricultural machinery hire purchase | ||||||

Asset finance | Medium | Farm owner or company director | Asset finance provider | Secures seasonal income-dependent repayments. | Either | Medium |

Professional services firm working capital facility | ||||||

Business loan | Medium | LLP member or director | Bank or lender | Supports fees-to-cash timing and overheads. | Either | Medium |

Law firm disbursement or WIP finance | ||||||

Business loan, Invoice finance | Low | Partner, LLP member or director | Specialist lender | Supports case funding and lock-up risk. | Either | Medium |

Accountancy practice acquisition finance | ||||||

Business loan | Medium | Purchasing partner or director | Bank or acquisition lender | Supports client-book acquisition funding. | Either | Medium |

New credit during turnaround or CVA | ||||||

Trade credit, Business loan | Medium | Director or shareholder | Supplier or rescue lender | Supports credit despite insolvency risk. | Capped | High |

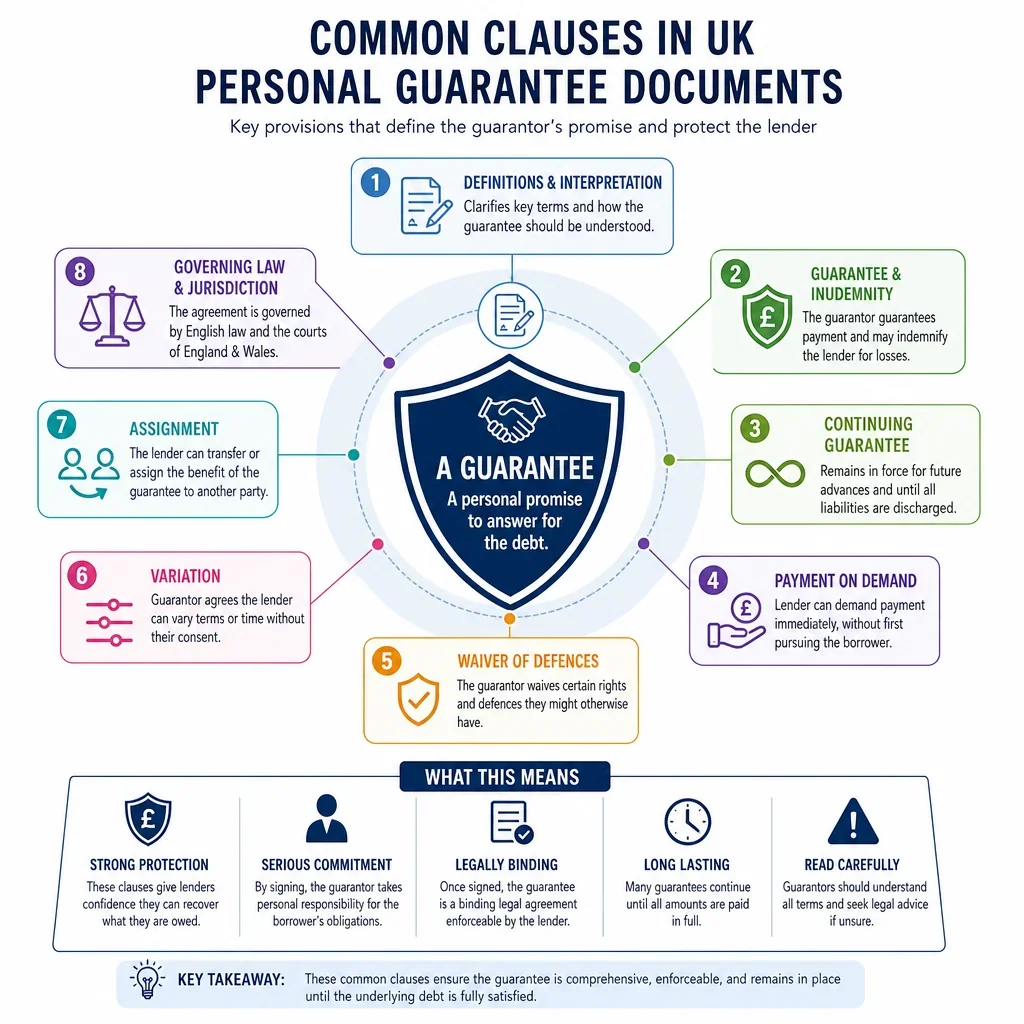

Guarantee evidenced in writing | ||||||

Other | High | Any individual guarantor | Any creditor | Provides enforceable written evidence of promise. | Either | Medium |

Individual guarantee with consumer element | ||||||

Other | Low | Individual connected to debtor | Trader, lender or supplier | Raises fairness scrutiny for individual guarantor terms. | Either | Medium |

When Are Personal Guarantees Most Common In The UK?

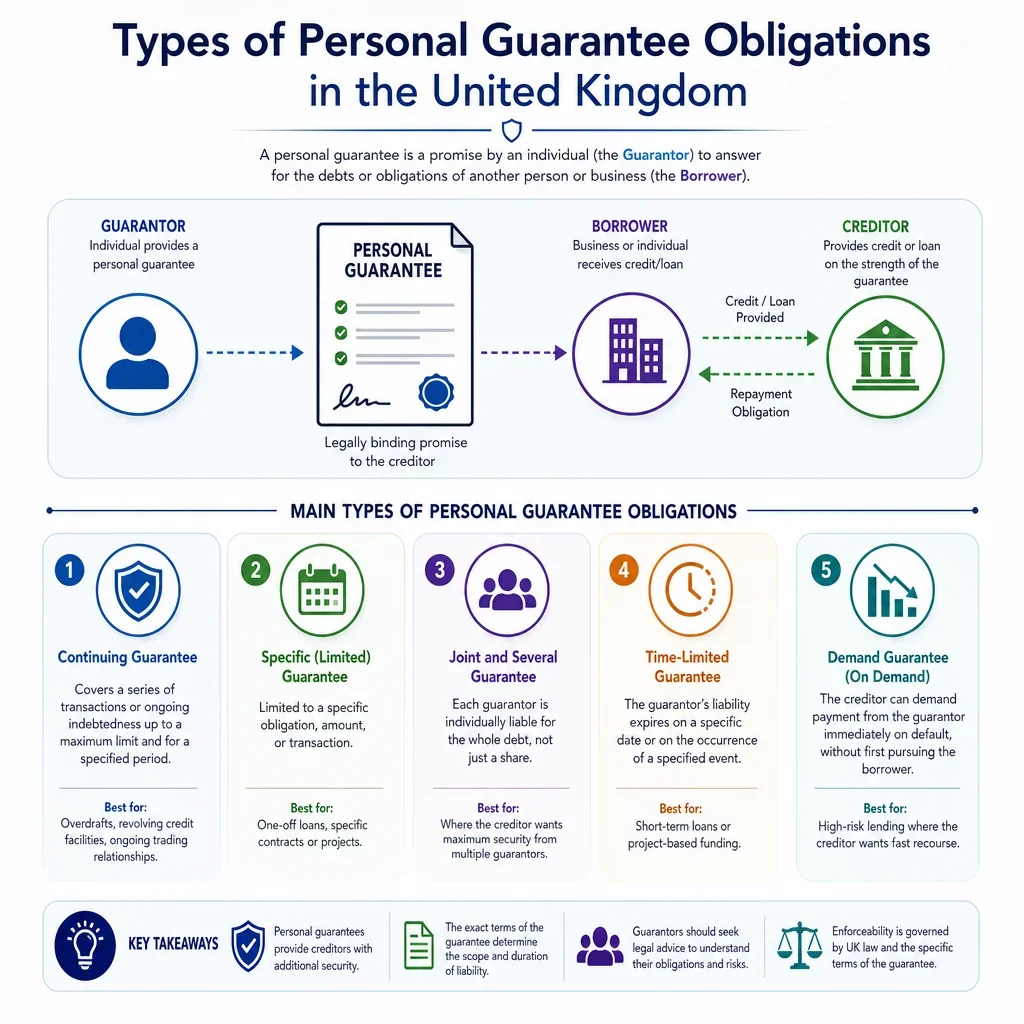

Personal guarantees are most common where a company has limited trading history, limited assets, or depends heavily on owner-managers. The highest-frequency UK use cases are SME lending, overdrafts, trade credit accounts, commercial leases, asset finance, invoice finance and franchise arrangements.

Which Personal Guarantee Use Cases Usually Create The Highest Exposure?

High exposure is most likely where the guarantee is uncapped or linked to long-term or fluctuating obligations. This is common in commercial leases, bank facilities, supplier credit accounts, invoice finance, development finance and franchise agreements. A guarantor should check whether liability covers only principal sums or also interest, rent, service charge, costs, indemnities and enforcement expenses.

When Should A UK Guarantor Ask For A Liability Cap?

A liability cap is especially important for trade credit, asset finance, overdrafts, invoice finance and supply agreements because the amount owed can change over time. Caps may be expressed as a fixed sum, a percentage of the facility, a rent deposit equivalent, or a limit covering specified invoices or contracts.

Who Usually Gives A Personal Guarantee?

The typical guarantor is a director, majority shareholder, LLP member, sole business owner, franchisee principal, or property developer. Lenders, landlords and suppliers often request guarantees from people who control the business and benefit from the transaction.

What UK Legal Points Should Users Check Before Signing?

- Independent legal advice: UK lenders commonly require it, particularly where the guarantor may not receive a direct commercial benefit.

- Written terms: guarantees must generally be evidenced in writing to be enforceable under section 4 of the Statute of Frauds 1677.

- Consumer and unfair terms risk: where the guarantor is an individual and the arrangement has a consumer element, enforceability and fairness may be affected by the Consumer Rights Act 2015.

- Insolvency context: guarantees are often called on when the principal debtor enters administration, liquidation or default, so the guarantor should treat the guarantee as a real contingent debt rather than a formality.

FAQs

You Might Also Be Interested In