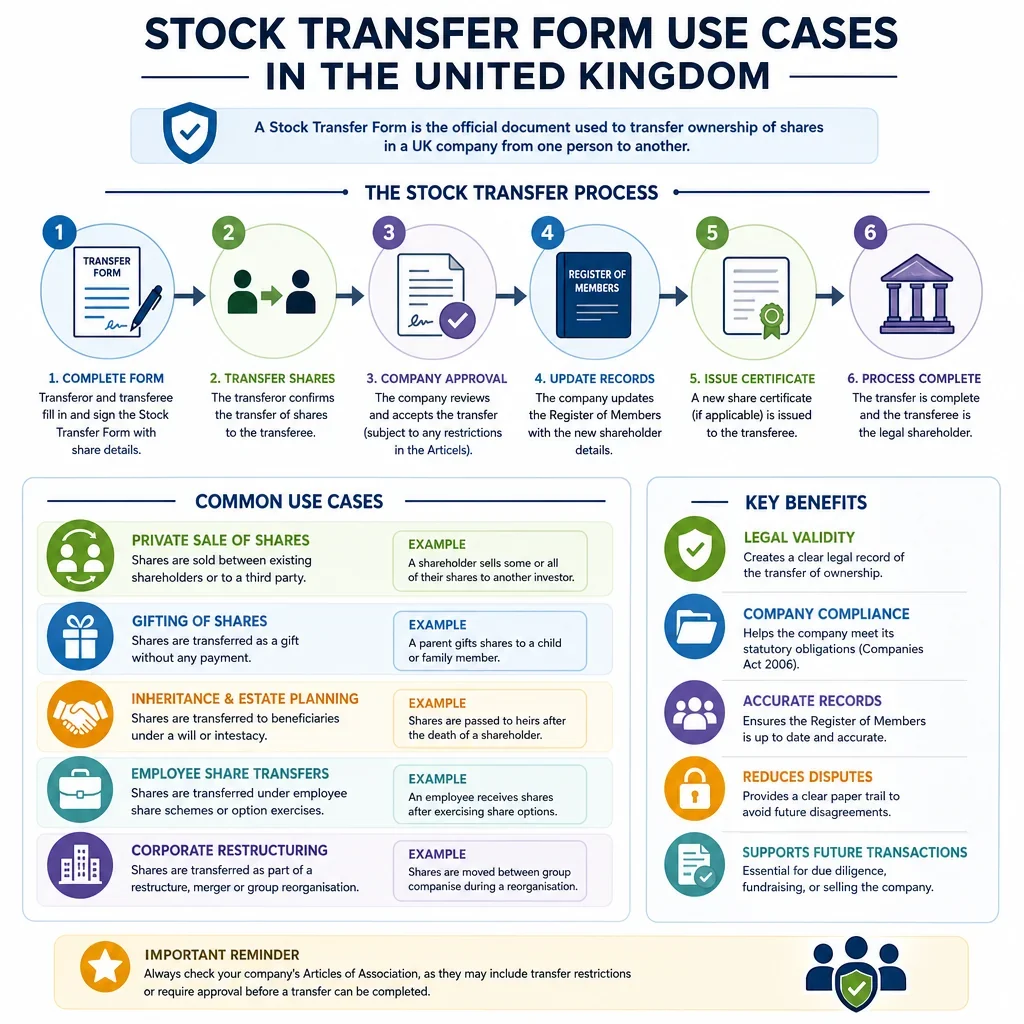

Stock Transfer Form Use Cases In The United Kingdom

Typical Use | Consideration Usually Paid | Stamp Duty Relevance | Common Supporting Documents | Practical Notes |

|---|---|---|---|---|

Sale of shares for cash | ||||

Used when a shareholder sells shares to a buyer for an agreed cash price. | Yes | Usually required | Share purchase agreement, board approval, old share certificate, Stamp Duty evidence. | Check pre-emption rights, articles, consideration, and whether HMRC stamping is needed. |

Sale for £1,000 or less | ||||

Used for a low value share sale where chargeable consideration does not exceed £1,000. | Yes | Usually not required | Sale agreement, board approval, share certificate, consideration evidence. | Confirm the total consideration and that no linked transaction changes the duty position. |

Gift of shares | ||||

Used when shares are transferred voluntarily without payment. | No | Usually not required | Gift letter, board approval, old share certificate, identity records. | Record nil consideration clearly and consider tax advice on capital gains and inheritance tax. |

Transfer to spouse or civil partner | ||||

Used for family or tax planning transfers between spouses or civil partners. | No | Usually not required | Gift letter, marriage or civil partnership evidence, board approval, share certificate. | Confirm the transfer is not part of a wider sale or consideration-bearing arrangement. |

Transfer on divorce or dissolution settlement | ||||

Used when shares move between former partners under a financial settlement. | Sometimes | May be required | Court order, settlement agreement, board approval, share certificate. | Check whether any monetary consideration or assumption of liabilities is involved. |

Transfer to family member | ||||

Used to pass shares to children, parents, siblings, or other relatives. | Sometimes | May be required | Gift letter or sale agreement, board approval, valuation, share certificate. | Identify whether the transfer is a true gift or a sale at undervalue. |

Transfer to minor child | ||||

Used when shares are intended for a child, often held by an adult nominee or trustee. | No | Usually not required | Gift letter, trust or nominee declaration, board approval, share certificate. | Check whether the company permits minors as registered members. |

Transfer into a trust | ||||

Used when shares are settled on trustees for beneficiaries. | No | Usually not required | Trust deed, trustee acceptance, board approval, share certificate. | Ensure trustees are correctly named and any trust tax reporting is considered. |

Transfer from trustees to beneficiary | ||||

Used when trustees distribute shares to a beneficiary. | No | Usually not required | Trust deed, trustee resolution, beneficiary details, board approval, share certificate. | Check trustee powers and whether all trustees must sign the transfer. |

Change of trustee | ||||

Used to move legal title from retiring trustees to continuing or new trustees. | No | Usually not required | Deed of appointment or retirement, trust deed, board approval, share certificate. | Use trustee names consistently with the trust instrument and company register. |

Nominee to beneficial owner | ||||

Used when a nominee transfers registered title to the underlying beneficial owner. | No | Usually not required | Nominee agreement, beneficiary instruction, board approval, share certificate. | Keep evidence that beneficial ownership has not changed for value. |

Beneficial owner to nominee | ||||

Used when shares are registered in a nominee's name for holding convenience. | No | Usually not required | Nominee agreement, owner instruction, board approval, share certificate. | Confirm the nominee arrangement and PSC register implications, if any. |

Transfer by personal representatives | ||||

Used where executors or administrators transfer deceased shareholder's shares to a beneficiary or buyer. | Sometimes | May be required | Grant of probate or letters of administration, death certificate, board approval, share certificate. | Distinguish transmission on death from any later sale by the estate. |

Transmission on death to beneficiary | ||||

Used to register inherited shares in the name of the beneficiary. | No | Usually not required | Grant of probate, will or estate instruction, board approval, share certificate. | Check articles for transmission procedures before using a transfer form. |

Founder share allocation transfer | ||||

Used to move existing founder shares between founders after incorporation. | Sometimes | May be required | Founder agreement, board approval, shareholders' agreement, share certificate. | Check vesting, leaver, and pre-emption provisions before transfer. |

Employee share acquisition | ||||

Used when an employee buys or receives existing shares from a shareholder. | Sometimes | May be required | Employee share agreement, valuation, board approval, share certificate. | Consider employment tax and section 431 election advice where relevant. |

Leaver transfer to company founders | ||||

Used when a departing employee or founder must transfer shares under leaver provisions. | Sometimes | May be required | Shareholders' agreement, leaver notice, valuation, board approval, share certificate. | Apply the good leaver or bad leaver price mechanism carefully. |

Growth share transfer | ||||

Used to transfer existing growth shares to employees, founders, or investors. | Sometimes | May be required | Growth share terms, valuation, board approval, share certificate. | Check class rights, hurdle value, and employment-related securities issues. |

Option exercise over existing shares | ||||

Used when an option holder acquires existing shares from a shareholder. | Yes | May be required | Option agreement, exercise notice, board approval, share certificate, valuation. | Confirm exercise price, vesting, and whether new issue paperwork is needed instead. |

EMI option exercise over existing shares | ||||

Used where EMI options are satisfied by transferring existing shares. | Yes | May be required | EMI agreement, exercise notice, board approval, share certificate, HMRC records. | Check EMI terms, notification requirements, and whether shares are existing or newly issued. |

Transfer to employee benefit trust | ||||

Used when shares are transferred to trustees for employee incentive arrangements. | Sometimes | May be required | EBT trust deed, trustee resolution, board approval, valuation, share certificate. | Consider employment tax, disguised remuneration, and funding arrangements. |

Transfer from employee benefit trust | ||||

Used when trustees transfer shares to employees or option holders. | Sometimes | May be required | Trustee resolution, award documents, exercise notice, board approval, share certificate. | Check award terms and PAYE or NIC reporting duties before registration. |

Investor purchase from existing shareholder | ||||

Used when an angel, VC, or strategic investor buys existing shares. | Yes | Usually required | Share purchase agreement, investment agreement, board approval, share certificate, Stamp Duty evidence. | Do not confuse transfer of existing shares with subscription for new shares. |

Secondary sale in funding round | ||||

Used when existing shareholders sell shares alongside a new investment round. | Yes | Usually required | Investment agreement, transfer forms, board approval, investor consents, share certificates. | Separate documents for share transfers from subscription documents for new shares. |

Transfer under pre-emption offer | ||||

Used after existing shareholders accept an offer under transfer pre-emption provisions. | Yes | May be required | Pre-emption notice, acceptance, valuation, board approval, share certificate. | Follow notice, timing, pricing, and allocation rules exactly. |

Drag-along sale | ||||

Used when majority sellers require minority shareholders to sell to a buyer. | Yes | Usually required | Share purchase agreement, drag notice, shareholder consents, board approval, certificates. | Check drag thresholds, notice formalities, and power of attorney provisions. |

Tag-along sale | ||||

Used when minority shareholders join a majority shareholder sale. | Yes | Usually required | Sale agreement, tag notice, acceptances, board approval, share certificates. | Confirm the buyer acquires all tagged shares on matching terms. |

Management buyout share transfer | ||||

Used when managers buy shares from existing owners. | Yes | Usually required | Share purchase agreement, finance documents, board approval, share certificates, Stamp Duty evidence. | Coordinate completion mechanics, funding, warranties, and director conflicts. |

Company share buyback | ||||

Used when a company purchases its own shares from a shareholder. | Yes | May be required | Buyback contract, shareholder resolution, solvency documents, board minutes, SH03. | Buybacks have specific Companies Act rules and Companies House filings. |

Sale of treasury shares | ||||

Used when a company sells shares it previously held in treasury. | Yes | May be required | Board approval, treasury share records, sale agreement, share certificate. | Check treasury share rules and whether the transaction is treated as an issue or transfer. |

Intra-group transfer | ||||

Used to move shares between group companies for restructuring or holding company changes. | Sometimes | May be required | Group reorganisation steps plan, board approvals, relief claim, share certificate. | Consider whether Stamp Duty group relief is available and properly claimed. |

Holding company insertion | ||||

Used when shareholders transfer operating company shares to a new holding company. | Sometimes | May be required | Share-for-share agreement, board approvals, tax clearance, new share certificates. | Check reconstruction relief, share-for-share terms, and HMRC clearance needs. |

Share-for-share exchange | ||||

Used where sellers transfer shares in exchange for shares in another company. | Sometimes | May be required | Share exchange agreement, valuation, board approvals, relief claim, certificates. | Non-cash consideration may still be chargeable and needs valuation. |

Demerger share transfer | ||||

Used as part of separating businesses or assets into different ownership structures. | Sometimes | May be required | Demerger steps plan, board approvals, shareholder resolutions, tax clearances. | Specialist tax and company law advice is usually needed before transfer forms are signed. |

Distribution in specie of shares | ||||

Used when a company distributes shares it owns to shareholders without cash sale. | No | May be required | Board minutes, distribution resolution, solvency records, valuation, share certificate. | Check distributable reserves and whether any liabilities are assumed. |

Transfer by liquidator | ||||

Used when a liquidator transfers shares held by an insolvent or solvent company. | Sometimes | May be required | Liquidator authority, sale agreement or distribution record, board or insolvency records. | Confirm the liquidator's authority and whether the transfer is a sale or distribution. |

Transfer in satisfaction of debt | ||||

Used when shares are transferred to a creditor to settle money owed. | Yes | Usually required | Debt settlement agreement, valuation, board approval, share certificate. | Debt release is consideration and should be valued for Stamp Duty purposes. |

Transfer on enforcement of share security | ||||

Used when a lender or secured party enforces security over shares. | Sometimes | May be required | Share charge, enforcement notice, power of attorney, board approval, certificates. | Check enforcement rights and any restrictions in articles or shareholders' agreement. |

Return of charged shares to owner | ||||

Used when shares held by a lender or nominee as security are returned after repayment. | No | Usually not required | Release deed, discharge letter, board approval, share certificate. | Keep evidence that the transfer reverses security holding rather than a sale. |

Broker nominee transfer | ||||

Used to move certificated shares into or out of a broker nominee account. | No | Usually not required | Broker instruction, nominee details, share certificate, identity checks. | Confirm whether legal title only is changing and broker forms are also needed. |

CREST withdrawal to certificate | ||||

Used when uncertificated shares are moved into certificated registered form. | No | Usually not required | CREST instruction, registrar forms, identity checks, new certificate request. | Registrar or CREST procedures may replace a standard paper stock transfer form. |

Deposit of certificated shares into CREST | ||||

Used to move paper share certificate holdings into CREST. | No | Usually not required | CREST transfer form, share certificate, broker or sponsor instruction. | Use the registrar or CREST participant process for dematerialisation. |

Certificated listed company share sale | ||||

Used where listed shares are sold in paper certificated form outside CREST settlement. | Yes | Usually required | Stock transfer form, share certificate, broker instruction, Stamp Duty evidence. | Registrar requirements and market settlement rules may be stricter than private company practice. |

Private company share transfer | ||||

Used for transfers of shares in a UK private limited company. | Sometimes | May be required | Board minutes, articles, shareholders' agreement, share certificate, register update. | Directors usually register the transfer only after checking restrictions and approvals. |

Transfer of partly paid shares | ||||

Used where shares have unpaid amounts that may affect the transferee's liability. | Sometimes | May be required | Sale agreement, share certificate, unpaid amount records, board approval. | The transferee should understand liability for unpaid share capital. |

Transfer of preference shares | ||||

Used when preference shares are sold, gifted, or transferred to another holder. | Sometimes | May be required | Articles, class rights documents, board approval, valuation, share certificate. | Check class rights, dividend arrears, redemption rights, and transfer restrictions. |

Transfer of alphabet shares | ||||

Used when a specific class of ordinary shares is transferred in an owner-managed company. | Sometimes | May be required | Articles, class rights schedule, board approval, valuation, share certificate. | Ensure the correct share class, rights, and certificate numbers are stated. |

Transfer of nil paid shares | ||||

Used where shares have been issued but no subscription amount has yet been paid. | Sometimes | May be required | Allotment records, unpaid capital records, board approval, share certificate. | Confirm unpaid capital liability and whether the transfer is permitted. |

Transfer after share reorganisation | ||||

Used after shares have been subdivided, consolidated, or reclassified. | Sometimes | May be required | Shareholder resolution, updated articles, board minutes, new share certificate. | Use current share numbers, nominal value, and class descriptions. |

Transfer after company name change | ||||

Used when shares are transferred after the company has changed its registered name. | Sometimes | May be required | Certificate of name change, board approval, share certificate, register records. | Use the current company name and keep evidence linking older certificates. |

Corrective transfer | ||||

Used to correct shares registered in the wrong name or proportions. | No | Usually not required | Error evidence, board minutes, indemnity, old and new share certificates. | Document the mistake clearly and avoid disguising a later value transfer. |

Transfer where certificate is lost | ||||

Used when shares are transferred but the original certificate cannot be produced. | Sometimes | May be required | Indemnity for lost certificate, board approval, identity checks, transfer form. | The company or registrar may require an indemnity before registering the transfer. |

Adding a joint shareholder | ||||

Used to add another person as joint legal owner of existing shares. | No | Usually not required | Gift letter, joint holder instruction, board approval, share certificate. | Check joint holder limits and survivorship rules in the articles. |

Removing a joint shareholder | ||||

Used to transfer jointly held shares into the name of one remaining holder. | Sometimes | May be required | Joint holder instruction, settlement agreement if relevant, board approval, certificate. | Confirm whether the outgoing holder receives value or is making a gift. |

Transfer to pension scheme trustee | ||||

Used when shares are transferred to trustees of a pension scheme or SIPP. | Sometimes | May be required | Pension trustee instruction, scheme documents, valuation, board approval, certificate. | Check pension scheme investment rules and connected party valuation requirements. |

Gift of shares to charity | ||||

Used when a shareholder donates shares to a UK charity. | No | Usually not required | Donation letter, charity details, board approval, share certificate, valuation. | Confirm charity registration details and whether donor tax relief evidence is needed. |

Sale to corporate buyer | ||||

Used when a company buys shares from an individual or another company. | Yes | Usually required | Share purchase agreement, buyer board approval, seller authority, certificates, Stamp Duty evidence. | Check corporate authority, execution formalities, and PSC register effects. |

Transfer by corporate shareholder | ||||

Used when a company transfers shares it holds in another company. | Sometimes | May be required | Seller board approval, authorised signatory evidence, agreement, share certificate. | Ensure the corporate seller has approved the transfer and signs correctly. |

Transfer to overseas buyer | ||||

Used when UK company shares are transferred to a non-UK resident buyer. | Yes | Usually required | Sale agreement, identity checks, board approval, share certificate, Stamp Duty evidence. | UK Stamp Duty can still apply to UK shares despite overseas residence. |

Transfer signed by attorney | ||||

Used when an attorney signs the stock transfer form for the transferor. | Sometimes | May be required | Power of attorney, identity checks, board approval, share certificate. | Provide the power of attorney and check it authorises share transfers. |

Transfer under court order | ||||

Used when a court directs shares to be transferred or registered. | Sometimes | May be required | Sealed court order, board minutes, share certificate, identity evidence. | Follow the court order exactly and check whether any consideration is specified. |

Transfer after register rectification | ||||

Used after the register of members is corrected by agreement or court order. | No | Usually not required | Rectification agreement or order, board minutes, register entries, certificates. | Align the transfer form, register, and certificate history. |

Transfer to custodian | ||||

Used when shares are registered with a custodian for safekeeping or administration. | No | Usually not required | Custody agreement, transfer instruction, board approval, share certificate. | Confirm no beneficial ownership sale occurs and review PSC implications. |

Custodian to beneficial owner | ||||

Used when shares held by a custodian are re-registered to the underlying owner. | No | Usually not required | Custody release instruction, beneficial ownership evidence, board approval, certificate. | Keep a paper trail showing the transfer is administrative only. |

Transfer for non-cash consideration | ||||

Used when shares are exchanged for assets, services, debt release, or other non-cash value. | Yes | May be required | Asset transfer agreement, valuation, board approval, share certificate. | Value the non-cash consideration before deciding Stamp Duty treatment. |

Transfer for nominal consideration | ||||

Used when shares are transferred for a token amount, often within families or groups. | Sometimes | May be required | Transfer agreement, valuation, board approval, share certificate. | Nominal price may not reflect tax value consider connected party tax advice. |

Transfer under settlement agreement | ||||

Used to settle a commercial, shareholder, employment, or family dispute involving shares. | Sometimes | May be required | Settlement agreement, releases, board approval, share certificate, valuation. | Check whether mutual releases or payments amount to consideration. |

Shareholder exit transfer | ||||

Used when a shareholder exits following dispute, deadlock, or negotiated buyout. | Yes | Usually required | Exit agreement, valuation, settlement terms, board approval, share certificate. | Align price, release wording, restrictive covenants, and completion deliverables. |

Transfer to bare trustee | ||||

Used where legal title is held by a bare trustee for an absolute beneficiary. | No | Usually not required | Bare trust declaration, beneficiary instruction, board approval, share certificate. | Record beneficial ownership and consider PSC register consequences. |

Transfer to offshore trustee | ||||

Used when UK shares are settled on trustees outside the UK. | No | Usually not required | Trust deed, trustee KYC, tax advice, board approval, share certificate. | Offshore trust, inheritance tax, and reporting issues need specialist advice. |

Share transfer in asset sale consideration | ||||

Used when shares are transferred as part payment for business assets. | Yes | May be required | Asset purchase agreement, valuation, board approvals, share certificate. | Value the asset consideration and check VAT and Stamp Duty interaction. |

Transfer under earn-out arrangement | ||||

Used when shares are transferred as deferred or contingent consideration. | Yes | May be required | Sale agreement, earn-out calculation, valuation, board approval, certificates. | Contingent consideration can complicate Stamp Duty and valuation. |

Vendor rollover share transfer | ||||

Used when sellers roll part of their sale proceeds into buyer group shares. | Yes | May be required | SPA, rollover agreement, valuation, board approvals, share certificates. | Check whether shares are transferred, newly issued, or exchanged for relief purposes. |

Compulsory acquisition after takeover | ||||

Used when a bidder acquires remaining shares after reaching statutory thresholds. | Yes | Usually required | Takeover notices, acceptance records, board or registrar records, Stamp Duty evidence. | Follow the statutory squeeze-out process and registrar requirements. |

Transfer under scheme of arrangement | ||||

Used where a court-sanctioned scheme transfers shares to a bidder or new holding company. | Sometimes | May be required | Court order, scheme document, shareholder approvals, registrar records. | Scheme mechanics may use court order rather than individual stock transfer forms. |

Transfer after company restoration | ||||

Used after a company is restored and historic share ownership needs updating. | Sometimes | May be required | Restoration order or confirmation, register records, board approval, share certificate. | Confirm the company has been restored before registering any transfer. |

Transfer to meet regulatory ownership limits | ||||

Used where regulated businesses require changes in shareholder ownership or control. | Sometimes | May be required | Regulatory approval, sale agreement, board approval, share certificate. | Obtain any required change in control consent before completing the transfer. |

FCA change in control share transfer | ||||

Used when acquiring or disposing shares in an FCA-regulated firm triggers control thresholds. | Yes | Usually required | FCA approval, sale agreement, board approval, share certificate, Stamp Duty evidence. | Do not complete before required regulatory approval or statutory notice clearance. |

Transfer from dissolved corporate shareholder | ||||

Used where shares were held by a company that has been dissolved and title must be resolved. | No | Usually not required | Restoration documents, bona vacantia waiver or vesting evidence, board approval. | Resolve bona vacantia or restoration issues before attempting registration. |

Transfer involving LLP shareholder | ||||

Used when an LLP transfers or acquires shares in a company. | Sometimes | May be required | LLP member approval, agreement, authority evidence, board approval, certificate. | Check the LLP agreement and authority of signing members. |

Transfer from partnership to partner | ||||

Used when shares held for a partnership are distributed to a partner. | Sometimes | May be required | Partnership agreement, partner resolution, valuation, board approval, certificate. | Identify whether the partner gives value or receives a capital distribution. |

Transfer to joint venture company | ||||

Used when parties contribute shares to a joint venture vehicle. | Sometimes | May be required | JV agreement, contribution agreement, valuation, board approvals, certificates. | Contribution of shares may be consideration-bearing even without cash. |

Transfer out of joint venture company | ||||

Used when JV assets or shares are unwound or transferred to venture parties. | Sometimes | May be required | JV exit agreement, valuation, board approvals, share certificate. | Apply exit rights, reserved matters, and valuation rules before transfer. |

Transfer to ISA manager nominee | ||||

Used when eligible shares are placed with an ISA manager nominee. | No | Usually not required | ISA manager instruction, nominee details, share certificate, eligibility confirmation. | Confirm ISA eligibility and nominee process before completing transfer paperwork. |

Transfer to personal investment company | ||||

Used when an individual transfers shares to a company they own or control. | Sometimes | May be required | Transfer agreement, valuation, company board approval, tax advice, certificate. | Connected party tax, valuation, and Stamp Duty issues are common. |

Transfer from personal investment company | ||||

Used when a company transfers shares to its owner, another company, or a third party. | Sometimes | May be required | Board approval, distribution or sale agreement, valuation, certificate. | Determine whether the transfer is a sale, dividend in specie, or loan-related benefit. |

Transfer after warrant exercise | ||||

Used where a warrant is satisfied by transfer of existing shares rather than new issue. | Yes | May be required | Warrant instrument, exercise notice, board approval, share certificate, valuation. | Check whether the warrant requires allotment of new shares instead of transfer. |

Transfer on convertible loan settlement | ||||

Used where existing shares are transferred to settle or convert a loan arrangement. | Yes | Usually required | Convertible loan note, settlement agreement, valuation, board approval, certificate. | Loan release or conversion value is likely to be relevant consideration. |

Crowdfunding nominee transfer | ||||

Used when shares are moved between a crowdfunding nominee and investor or replacement nominee. | No | Usually not required | Nominee terms, platform instruction, beneficial owner records, board approval. | Check platform terms and maintain accurate beneficial owner records. |

Nominee migration transfer | ||||

Used when holdings are moved from one nominee company to another. | No | Usually not required | Migration instruction, nominee agreements, beneficial owner confirmation, certificates. | Evidence that beneficial ownership remains unchanged. |

Compulsory transfer under articles | ||||

Used where articles require transfer on death, insolvency, employment exit, or breach. | Sometimes | May be required | Articles, compulsory transfer notice, valuation, board approval, share certificate. | Follow the articles' trigger, valuation, notice, and default execution provisions. |

Transfer to multiple transferees | ||||

Used when one seller transfers shares to several buyers at completion. | Yes | Usually required | Sale agreement, allocation schedule, board approval, certificates, Stamp Duty evidence. | Use separate forms or clear allocations for each transferee and consideration amount. |

Transfers from multiple transferors | ||||

Used when a buyer acquires shares from several selling shareholders. | Yes | Usually required | SPA, seller schedules, board approval, certificates, Stamp Duty evidence. | Prepare separate transfer forms matching each seller's registered holding. |

Partial transfer of holding | ||||

Used when a shareholder transfers only some of their shares. | Sometimes | May be required | Transfer form, old certificate, balance certificate, board approval, agreement. | Cancel the old certificate and issue new certificates for transferred and retained shares. |

Whole holding transfer | ||||

Used when a shareholder transfers all shares held in a company. | Sometimes | May be required | Transfer form, share certificate, board approval, sale or gift record. | Ensure the number of shares matches the register and certificate exactly. |

Paper certificated share transfer | ||||

Used for most private company transfers where physical share certificates exist. | Sometimes | May be required | Stock transfer form, share certificate, board approval, register of members update. | Registration, not signing alone, updates legal membership in company records. |

Transfer needing director approval | ||||

Used where articles give directors discretion to approve or refuse registration. | Sometimes | May be required | Articles, board minutes, transfer form, share certificate, agreement. | If refusing registration, the company must comply with statutory notice rules. |

Transfer to overseas company | ||||

Used when a non-UK company acquires shares in a UK company. | Yes | Usually required | Corporate authority evidence, sale agreement, KYC, board approval, Stamp Duty evidence. | Obtain evidence of overseas corporate capacity and authorised signatories. |

Trustee sale of shares | ||||

Used where trustees sell shares held in trust to a third-party buyer. | Yes | Usually required | Trust deed, trustee resolution, sale agreement, board approval, certificate. | All required trustees should sign and apply trust powers of sale. |

Estate sale of shares | ||||

Used when executors sell inherited shares to raise cash or distribute estate value. | Yes | Usually required | Grant of probate, sale agreement, board approval, certificate, Stamp Duty evidence. | Confirm executors' authority and whether shares were first transmitted to the estate. |

Joint holder death transfer | ||||

Used when shares held jointly pass to surviving joint holder or are later transferred. | No | Usually not required | Death certificate, register evidence, board approval, share certificate. | Check articles for survivorship treatment and registrar evidence requirements. |

Restricted share transfer to beneficiary | ||||

Used where inherited or trust shares are subject to company transfer restrictions. | No | Usually not required | Will or trust deed, restriction consent, board approval, share certificate. | Beneficiary entitlement does not override valid article restrictions on registration. |

Pre-sale reorganisation transfer | ||||

Used before a business sale to tidy ownership, group structure, or share classes. | Sometimes | May be required | Steps paper, tax clearance, board and shareholder approvals, certificates. | Sequence transfers with tax clearances, buyer consents, and completion conditions. |

Transfer after share conversion | ||||

Used after shares have converted from one class into another before transfer. | Sometimes | May be required | Conversion notice, articles, board minutes, updated certificate, transfer form. | Ensure the transfer form reflects the post-conversion class and rights. |

Transfer of redeemable shares | ||||

Used when redeemable shares are transferred before redemption or buyback. | Sometimes | May be required | Articles, redemption terms, board approval, valuation, share certificate. | Check redemption date, price, and whether transfer is restricted before redemption. |

When Is Stamp Duty Likely To Matter For A UK Stock Transfer Form?

Stamp Duty is most likely to be relevant where shares are transferred for consideration, especially a sale, buyback, option exercise, debt settlement, or intra-group transfer that does not qualify for relief. For paper stock transfer forms, HMRC generally requires Stamp Duty where the chargeable consideration is over £1,000, subject to exemptions and reliefs.

Which Transfers Commonly Need Extra Company Checks?

Before completing a stock transfer form, check the company articles, any shareholders' agreement, pre-emption rights, and whether directors must approve registration of the transfer. Private companies often require board approval and cancellation or issue of share certificates before updating the register of members.

Which Stock Transfers Are Usually Not For Cash?

Gifts, transfers to a spouse or civil partner, probate-related transmissions, nominee changes, and transfers into some family trusts are commonly made without cash consideration. Even where no cash is paid, the form and company records should accurately show the nature of the transfer and keep evidence supporting any exemption.

What Records Should Be Kept With The Stock Transfer Form?

Common records include the signed stock transfer form, old share certificate, board minutes approving registration, any sale or gift agreement, valuation evidence, trust deed, probate documents, and proof of any Stamp Duty payment, exemption, adjudication, or relief claim.

FAQs

You Might Also Be Interested In