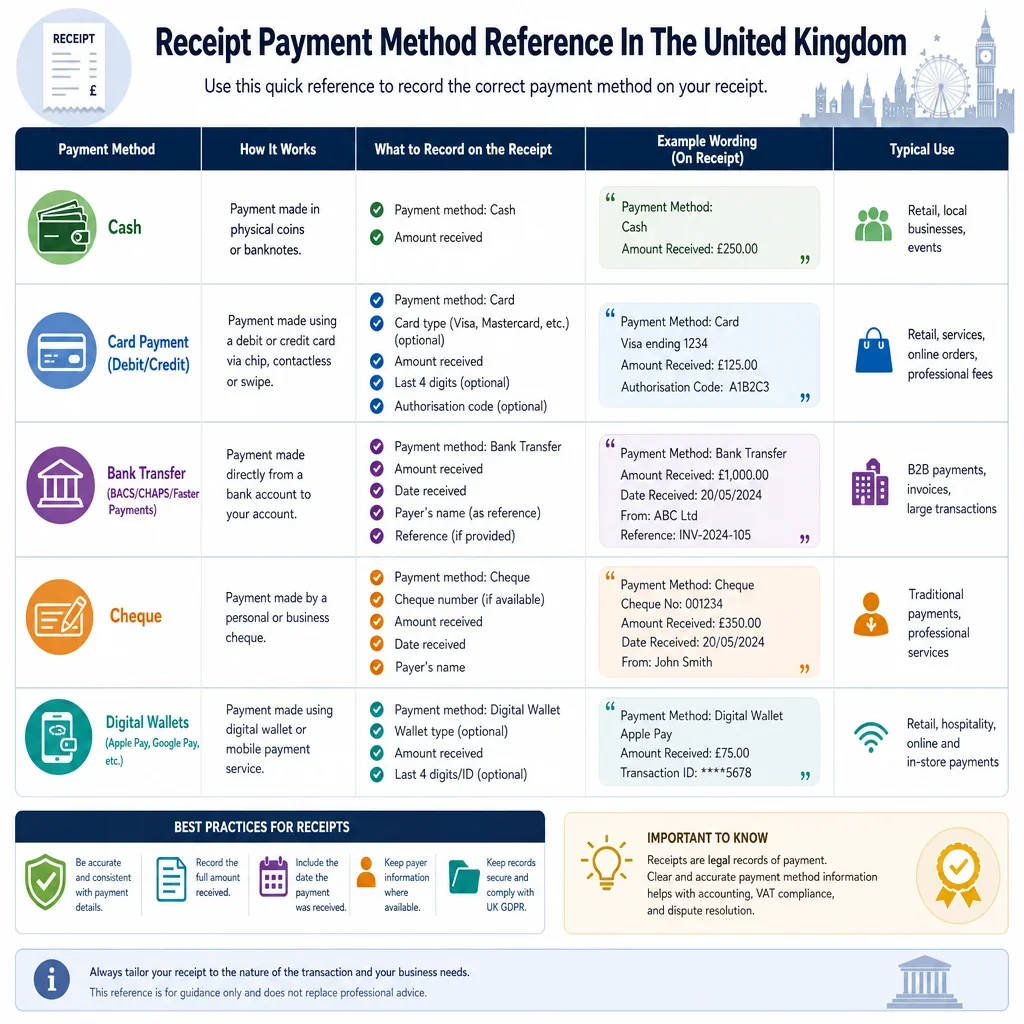

Receipt Payment Method Reference In The United Kingdom

Receipt Wording Guidance | Reference Details | Payment Confirmation Timing | Clearance Note Needed | Practical Notes |

|---|---|---|---|---|

Cash | ||||

State payment received in cash and show the amount, date, payer, and invoice or account number. | Cash receipt number, till number, cashier initials, branch or location, and invoice number. | Usually immediate | No | Count cash before issuing the receipt and keep a duplicate or audit copy for reconciliation. |

Debit Card | ||||

Record as debit card payment received, with card brand and masked card details if available. | Authorisation code, merchant receipt ID, terminal ID, masked PAN, and card scheme reference. | Usually immediate | No | Do not record full card numbers or CVV codes retain only masked and provider references. |

Record as contactless debit card payment and include the merchant or terminal receipt reference. | Contactless transaction ID, terminal ID, merchant receipt number, authorisation code, and masked card digits. | Usually immediate | No | Issue a VAT or sales receipt separately if the card slip lacks required transaction details. |

Show payment by debit card through the named payment gateway or checkout provider. | Gateway transaction ID, order ID, authorisation code, settlement batch, and masked card digits. | Usually immediate | Sometimes | If authorisation is pending, state that the receipt confirms authorisation rather than settled funds. |

Credit Card | ||||

Record as credit card payment received, with card brand and payment processor reference. | Authorisation code, acquirer reference, merchant receipt ID, terminal ID, and masked PAN. | Usually immediate | Sometimes | Keep processor references for refund, dispute, and chargeback tracing never record the CVV. |

State payment made by credit card remotely or online through the named processor. | Payment gateway ID, order reference, authorisation code, fraud check result, and masked card digits. | Varies | Sometimes | Consider wording as authorised or captured if funds have not yet settled to the merchant account. |

Bank Transfer | ||||

Show payment by bank transfer or Faster Payment and include the payer reference used. | Bank statement reference, payer name, Faster Payment reference, sort code tail, and invoice number. | Usually immediate | Sometimes | Issue final receipt after the funds appear in the recipient account or banking feed. |

Record as Bacs bank transfer and show the payer reference and expected value date. | Bacs reference, payer name, remittance advice number, invoice number, and bank statement narrative. | Usually delayed | Yes | Avoid stating cleared funds until the Bacs credit is visible in the bank account. |

State payment received by CHAPS transfer and include the bank reference. | CHAPS reference, payer bank, remittance reference, payment time, and invoice number. | Usually immediate | Sometimes | Confirm receipt in the bank account before issuing an unconditional receipt for large sums. |

Record as international bank transfer and show currency, amount received, and bank reference. | SWIFT UETR, sender name, remittance reference, exchange rate, fees deducted, and invoice number. | Usually delayed | Yes | State the net amount and currency actually received, especially where bank fees are deducted. |

Cheque | ||||

State payment by cheque and note that receipt is subject to clearance unless already cleared. | Cheque number, drawer name, bank, amount, date on cheque, and invoice number. | Usually delayed | Yes | Use wording such as subject to cheque clearance until the cheque has cleared through the bank. |

Record as bankeru0027s draft or bank draft and identify the issuing bank. | Draft number, issuing bank, purchaser name, date, amount, and invoice or contract reference. | Varies | Sometimes | Verify authenticity and bank clearance before treating the draft as final payment. |

Direct Debit | ||||

Record as Direct Debit collection and identify the mandate or service user reference. | Mandate reference, service user number, collection date, payer account name, and invoice number. | Usually delayed | Yes | Allow for unpaid collections and indemnity claims under the Direct Debit Guarantee. |

Credit Card | ||||

State recurring card payment received and identify the subscription or customer reference. | Recurring payment ID, authorisation code, subscription ID, masked card digits, and payment period. | Varies | Sometimes | Show the period covered so the receipt does not look like a one-off payment. |

Standing Order | ||||

Record as standing order payment and show the payeru0027s bank reference. | Standing order reference, payer name, bank statement reference, payment date, and account number or invoice. | Varies | Sometimes | Confirm each instalment separately a standing order can be changed or cancelled by the payer. |

Online Payment Service | ||||

State payment received through PayPal and include the PayPal transaction ID. | PayPal transaction ID, payer email, order ID, invoice number, gross amount, fees, and net amount. | Varies | Sometimes | Check whether the payment is completed, pending, held, refunded, or disputed before final wording. |

Record as online payment through Stripe and include the Stripe payment reference. | PaymentIntent ID, charge ID, checkout session ID, customer ID, order ID, and receipt URL. | Varies | Sometimes | Distinguish successful authorisation from payout settlement to the business bank account. |

State online card payment via the named merchant gateway and include the gateway reference. | Gateway transaction ID, merchant code, authorisation code, order ID, settlement batch, and masked card details. | Varies | Sometimes | Use the provideru0027s unique transaction reference for reconciliation and customer support. |

Mobile Payment | ||||

Record as Apple Pay payment and include the card processor or terminal reference. | Device account number tail, authorisation code, terminal ID, merchant receipt ID, and processor reference. | Usually immediate | No | Use tokenised or masked details only do not request the underlying card number. |

Record as Google Pay payment and include the processor or merchant receipt reference. | Token or virtual account tail, authorisation code, terminal ID, gateway ID, and order reference. | Usually immediate | No | Record the wallet method and processor reference rather than the underlying full card data. |

State mobile wallet payment and name the wallet where known. | Wallet name, authorisation code, terminal ID, transaction ID, masked token digits, and invoice number. | Usually immediate | No | Treat like a card payment for receipt references and privacy of cardholder data. |

Bank Transfer | ||||

Record as Open Banking bank payment and include the payment initiation reference. | Open Banking payment ID, consent ID, bank reference, payer name, order ID, and invoice number. | Varies | Sometimes | Confirm whether the provider reports initiation only or confirmed receipt of funds. |

Online Payment Service | ||||

State payment made via payment link and name the processor if known. | Payment link ID, checkout session ID, order reference, authorisation code, and payer email. | Varies | Sometimes | Match the link payment to the correct invoice before issuing a paid receipt. |

Mobile Payment | ||||

Record as QR code payment and identify the app or provider used. | QR payment ID, provider transaction ID, payer name, order ID, timestamp, and invoice number. | Varies | Sometimes | Do not rely on the customeru0027s screen alone verify confirmation in the merchant app or account. |

Cash | ||||

State cash deposit received into bank account and include deposit reference where available. | Paying-in slip number, bank branch, deposit date, payer name, account reference, and invoice number. | Varies | Sometimes | Confirm the deposit appears in the business account before marking the invoice as paid. |

Other | ||||

Record as postal order payment and identify the postal order number. | Postal order number, payer name, issue date, amount, and invoice or account reference. | Varies | Sometimes | Check authenticity and whether the order has been cashed before treating funds as final. |

State payment by money order and include the issuer and instrument reference. | Money order number, issuer, payer name, issue date, amount, and invoice number. | Usually delayed | Yes | Use subject to clearance wording until the payment instrument has been verified and paid. |

Record as voucher or gift card redemption and show the value applied. | Voucher code, gift card number tail, redemption ID, balance remaining, and order reference. | Usually immediate | No | Show any part-payment balance separately if the voucher does not cover the full amount. |

State cryptoasset payment received and record sterling value, crypto amount, and transaction hash. | Transaction hash, wallet address tail, network, confirmation count, exchange rate, sterling value, and invoice number. | Varies | Sometimes | Use sterling accounting values and wait for sufficient network confirmations before final receipt wording. |

State split payment and list each method with its amount and reference. | Separate references for each method, total received, balance outstanding, and invoice number. | Varies | Sometimes | Do not mark the full invoice paid unless all parts have cleared or been confirmed. |

Record as credit note or account credit applied, not as new cash received. | Credit note number, original invoice number, allocation date, amount applied, and balance remaining. | Usually immediate | No | Make clear that the receipt records settlement by credit allocation rather than payment of money. |

What Payment Details Should A UK Receipt Include?

A formal UK receipt should identify the payment method clearly and include a usable audit reference. For card payments, record the card type, masked card digits if available, terminal or merchant receipt ID, and authorisation code. For bank transfers, record the payer name, bank reference, date received, and invoice or account number. For cheques, state that payment is subject to clearance unless the cheque has already cleared.

When Should A Receipt Say Payment Is Subject To Clearance?

Use a clearance note for cheques, Direct Debit collections, some bank transfers, online payment services, and any payment that can be reversed, recalled, disputed, or not yet settled. This avoids implying that cleared funds have been received before confirmation.

How Should Card And Cash Receipts Be Handled In The UK?

Cash and chip-and-PIN or contactless card payments are usually treated as immediate for receipt wording, but the receipt should still avoid storing unnecessary personal data. For card payments, do not record the full card number or security code; use masked details and the payment provider reference.

Why Do References Matter On A Formal Receipt?

Transaction references help match the receipt to bank statements, merchant statements, invoices, chargeback enquiries, and accounting records. The most reliable wording combines the method, date, amount, payer, and a method-specific reference such as an authorisation code, Faster Payment reference, cheque number, or provider transaction ID.

FAQs

You Might Also Be Interested In