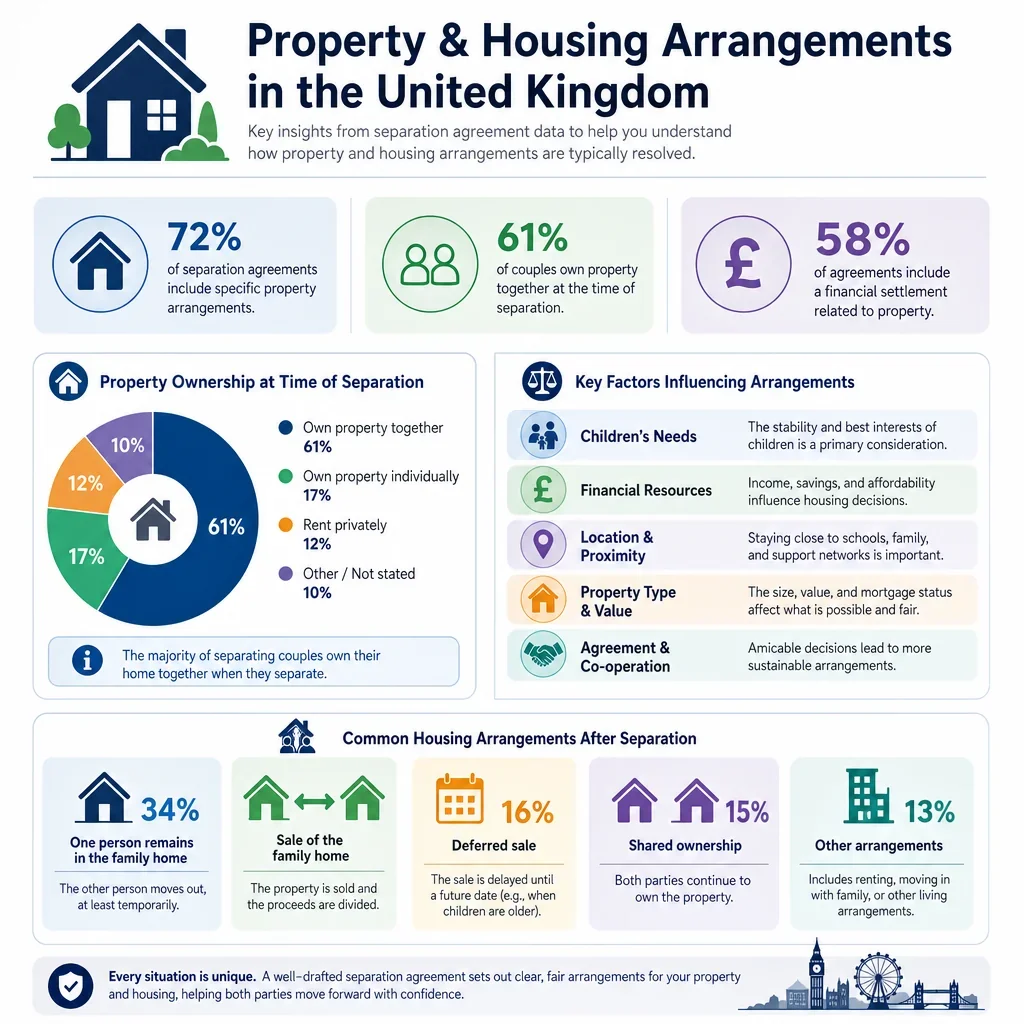

Property And Housing Arrangements Dataset In The United Kingdom

Housing Issue | Arrangement Timeframe | Key Decisions | Relevant Documents | Agreement Notes |

|---|---|---|---|---|

Family home | ||||

Interim occupation of the family home | Immediate arrangement Short-term arrangement | Who stays, who moves out, access for belongings, privacy, children’s routine. | Title register, tenancy, mortgage statement, child arrangements, utility bills. | Record occupation without implying permanent ownership or tenancy changes. |

Family home, Jointly owned property | ||||

Sale of the family home | Long-term arrangement Contingent on future event | Agent, valuation, asking price, sale timing, repairs, net proceeds split. | Title register, mortgage redemption figure, valuations, estate agent terms. | Set deadlocks for price reductions, offers, delays and sale costs. |

Jointly owned property, Mortgage and secured lending | ||||

Transfer of one party’s share in the home | Long-term arrangement | Buyout sum, mortgage release, lender consent, completion date, legal costs. | Title register, mortgage offer, valuation, transfer deed, lender consent. | Do not promise release from mortgage unless lender approval is obtained. |

Family home, Jointly owned property, Mortgage and secured lending | ||||

Deferred sale until children reach a trigger point | Contingent on future event Long-term arrangement | Trigger date, who occupies, payments, repairs, sale process, equity split. | Title register, mortgage statement, school dates, insurance, maintenance records. | Define triggers clearly, such as youngest child reaching 18 or finishing education. |

Mortgage and secured lending, Ongoing housing costs | ||||

Responsibility for mortgage payments after separation | Immediate arrangement Short-term arrangement Long-term arrangement | Payment shares, direct debit account, arrears, reimbursement, review dates. | Mortgage statement, lender correspondence, bank statements, arrears notices. | Joint borrowers usually remain liable to the lender despite private payment terms. |

Existing mortgage arrears | Immediate arrangement | Arrears plan, contribution shares, lender contact, possession risk, credit impact. | Arrears statement, lender notices, payment plan, court papers if issued. | Prioritise lender engagement agreement cannot bind lender or stop possession alone. |

Mortgage and secured lending, Jointly owned property | ||||

Remortgage to remove one party from borrowing | Long-term arrangement | Affordability, lender consent, timing, buyout amount, fall-back sale. | Mortgage statement, redemption figure, affordability decision, valuation. | Include a sale fallback if remortgage or release is refused. |

Secured loan or second charge on the home | Immediate arrangement Long-term arrangement | Who pays, redemption on sale, indemnity, whether debt was joint benefit. | Loan agreement, charge register, redemption statement, purpose of borrowing. | Secured lenders’ rights continue unless debt is repaid or lender agrees changes. |

Jointly owned property, Solely owned property | ||||

Dispute over beneficial shares in property | Long-term arrangement | Ownership shares, deposit contributions, mortgage payments, trust declaration. | TR1, declaration of trust, title register, bank records, conveyancing file. | Clarify whether agreed division is compromise or reflects legal ownership. |

Jointly owned property, Family home | ||||

Joint tenancy or tenancy in common status | Immediate arrangement Long-term arrangement | Whether to sever joint tenancy, update wills, record shares. | Title register, Form A restriction, severance notice, wills. | Severance can affect survivorship take advice before relying on agreement alone. |

Family home, Solely owned property | ||||

Home rights in a spouse’s solely owned home | Immediate arrangement Short-term arrangement | Occupation, registration, sale restrictions, mortgage contact, review on divorce. | Title register, marriage certificate, HR1 application, lender details. | A spouse or civil partner may need separate Land Registry protection. |

Family home, Rented property, Solely owned property, Jointly owned property | ||||

Need for an occupation order due to safety or exclusion | Immediate arrangement Short-term arrangement | Exclusion, permitted access, children, safety measures, police or court involvement. | Incident records, court orders, tenancy or title, safeguarding records. | Do not use a private agreement instead of urgent protection where risk exists. |

Solely owned property, Mortgage and secured lending, Ongoing housing costs | ||||

Sole owner remains responsible for mortgage | Immediate arrangement Long-term arrangement | Occupation contribution, bills, repairs, sale timing, reimbursement. | Mortgage statement, title register, bills, bank statements. | Contributions should be labelled carefully to avoid unintended ownership claims. |

Rented property, Ongoing housing costs | ||||

Joint tenancy after separation | Immediate arrangement Short-term arrangement Long-term arrangement | Who stays, rent payments, landlord consent, surrender, new tenancy. | Tenancy agreement, rent account, deposit certificate, landlord correspondence. | Joint tenants may remain liable for rent unless tenancy is lawfully changed. |

Rented property, Family home | ||||

One party is sole tenant of the home | Immediate arrangement Short-term arrangement | Whether non-tenant leaves, licence to occupy, rent contribution, notice. | Tenancy agreement, rent account, landlord letters, council tax bill. | Non-tenant rights vary landlord consent may be needed for occupation changes. |

Rented property | ||||

Ending a tenancy following separation | Short-term arrangement | Notice date, surrender terms, move-out date, deposit deductions, final rent. | Tenancy agreement, break clause, inventory, deposit protection details. | Check notice rules one tenant’s notice may end some periodic tenancies. |

Tenancy deposit return and deductions | Short-term arrangement Contingent on future event | Deposit ownership, deductions, cleaning, damage, repayment account. | Deposit certificate, prescribed information, inventory, check-out report, photos. | State how returned deposit and deductions will be divided. |

Rented property, Ongoing housing costs | ||||

Rent arrears at separation | Immediate arrangement Short-term arrangement | Arrears split, repayment plan, landlord contact, eviction risk. | Rent statement, tenancy agreement, landlord notices, court papers. | Private responsibility split may not stop landlord claiming against liable tenants. |

Rented property, Family home | ||||

Social housing tenancy and separation | Immediate arrangement Long-term arrangement | Who remains, housing provider consent, assignment, transfer, bedroom need. | Tenancy agreement, housing provider policy, rent account, child arrangements. | Assignment or transfer may need landlord agreement or a court order. |

Ongoing housing costs, Family home, Rented property | ||||

Council tax after one party moves out | Immediate arrangement Short-term arrangement | Liable person, single person discount, payment split, account update. | Council tax bill, occupancy date, local authority correspondence. | Update council promptly discount depends on actual adult occupancy. |

Gas, electricity and water accounts | Immediate arrangement | Meter readings, account holder, payment split, arrears, closing accounts. | Bills, meter readings, supplier account numbers, direct debit records. | Take dated meter readings when one party leaves or account changes. |

Ongoing housing costs, Household contents | ||||

Broadband, TV and media subscriptions | Immediate arrangement Short-term arrangement | Account holder, cancellation charges, equipment return, password changes. | Contracts, bills, router or equipment list, cancellation terms. | Allocate early termination fees and remove access to shared accounts. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Buildings insurance for owned home | Immediate arrangement Long-term arrangement | Policyholder, premium payment, lender requirements, vacancy notification. | Insurance policy, mortgage conditions, renewal notice, occupancy details. | Tell insurer about occupancy changes to avoid cover problems. |

Household contents, Ongoing housing costs | ||||

Contents insurance and belongings cover | Immediate arrangement Short-term arrangement | Who insures items, high-value items, removals cover, cancellation. | Policy schedule, valuations, receipts, contents inventory, photos. | Match insurance to the agreed contents split and storage arrangements. |

Household contents, Family home | ||||

Division of household furniture and appliances | Short-term arrangement | Item allocation, collection dates, condition, replacement value, delivery costs. | Inventory, photographs, receipts, warranties, valuation list. | Attach a schedule to avoid disputes over essential and sentimental items. |

Children’s bedroom furniture and essential items | Immediate arrangement Short-term arrangement | Beds, clothing, school equipment, toys, duplicates, transfer between homes. | Inventory, child arrangements, school equipment list, receipts. | Prioritise continuity for children and practical use at each home. |

Household contents, Family home, Ongoing housing costs | ||||

Pet housing and care after separation | Immediate arrangement Long-term arrangement | Primary carer, costs, insurance, vet decisions, handovers, microchip update. | Microchip record, insurance policy, vet records, purchase or adoption papers. | Pets are usually treated as property, so record care and costs clearly. |

Household contents, Family home, Rented property | ||||

Car, parking and garage use | Immediate arrangement Short-term arrangement | Vehicle keeper, finance, insurance, parking permit, garage contents. | V5C, finance agreement, insurance, parking permit, MOT records. | Update keeper, insurance and parking rights if vehicle use changes. |

Family home, Jointly owned property, Solely owned property, Rented property, Ongoing housing costs | ||||

Repairs and maintenance before sale or transfer | Short-term arrangement Long-term arrangement | Necessary repairs, approval limits, contractor choice, cost sharing, records. | Quotes, invoices, survey, landlord repair reports, photos. | Separate routine occupancy costs from capital repairs improving sale value. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Home improvements after separation | Long-term arrangement Contingent on future event | Consent, budget, funding source, equity credit, planning approval. | Quotes, planning documents, building control, invoices, before photos. | Avoid unilateral improvements unless reimbursement and consent are agreed. |

Family home, Jointly owned property, Solely owned property | ||||

Valuing the home for settlement purposes | Short-term arrangement Long-term arrangement | Valuer choice, valuation date, number of appraisals, dispute process. | Estate agent appraisals, RICS valuation, mortgage balance, title plan. | Use a clear valuation method to avoid later buyout or equity disputes. |

Sale costs and conveyancing fees | Contingent on future event Short-term arrangement | Agent fee, solicitor fee, EPC, removal costs, deductions before split. | Agent contract, conveyancing quote, EPC, completion statement. | Define net proceeds and deductions before stating percentage shares. |

Mortgage and secured lending, Jointly owned property, Solely owned property | ||||

Mortgage early repayment charge on sale or remortgage | Contingent on future event Short-term arrangement | Whether to delay, who bears charge, redemption timing, porting option. | Mortgage offer, redemption statement, lender tariff, fixed-rate end date. | Factor charges into equity calculations and sale timing. |

Jointly owned property, Mortgage and secured lending, Family home | ||||

Negative equity in the home | Long-term arrangement Contingent on future event | Sale delay, debt split, lender consent, shortfall payment, insolvency risk. | Valuation, mortgage statement, redemption figure, secured loan balances. | Address who pays any shortfall if sale proceeds do not clear secured debts. |

Family home, Jointly owned property, Solely owned property, Ongoing housing costs | ||||

Property left empty after separation | Immediate arrangement Short-term arrangement | Security, insurance notification, utilities, inspections, council tax premium. | Insurance policy, council tax bill, keys list, inspection log. | Vacancy can affect insurance cover and council tax costs. |

Family home, Rented property, Jointly owned property, Solely owned property | ||||

Keys, locks and home security | Immediate arrangement | Key return, alarm codes, lock changes, access notice, emergency access. | Tenancy terms, insurance policy, key list, alarm contract. | Avoid unlawful exclusion consider safety and landlord consent for locks. |

Family home, Rented property, Household contents | ||||

Access to collect personal belongings | Immediate arrangement Short-term arrangement | Date, supervision, item list, removals, disputed items, no-contact needs. | Inventory, photos, court orders, police reference if relevant. | Use a written list and neutral handover where conflict or safety risk exists. |

Household contents, Ongoing housing costs | ||||

Storage of furniture or personal items | Short-term arrangement | Storage provider, payment, insurance, access, disposal deadline. | Storage contract, inventory, insurance, receipts. | Set a review date to avoid indefinite storage liabilities. |

Household contents | ||||

Disposal or sale of unwanted household items | Short-term arrangement | Items to sell, minimum prices, charity donation, disposal costs, proceeds split. | Inventory, photos, sale receipts, waste collection receipts. | Do not dispose of disputed items without written consent. |

Family home, Jointly owned property, Solely owned property, Ongoing housing costs | ||||

Service charges and ground rent for leasehold property | Immediate arrangement Long-term arrangement | Payment shares, arrears, major works, reserve fund, sale apportionment. | Lease, service charge demands, ground rent demands, managing agent letters. | Major works can materially affect equity and should be allocated expressly. |

Jointly owned property, Solely owned property, Family home | ||||

Lease extension needed before sale or transfer | Contingent on future event Long-term arrangement | Whether to extend, premium, costs, timing, impact on sale price. | Lease, title register, valuation, freeholder correspondence, notices. | Short leases can affect mortgageability and valuation, so agree strategy early. |

Family home, Jointly owned property, Mortgage and secured lending, Ongoing housing costs | ||||

Shared ownership home after separation | Long-term arrangement Contingent on future event | Staircasing, rent, mortgage, resale restrictions, housing association consent. | Lease, mortgage statement, rent statement, housing association resale policy. | Check lease restrictions before agreeing sale, transfer or buyout terms. |

Family home, Jointly owned property, Solely owned property | ||||

Right to Buy discount and ownership issues | Long-term arrangement Contingent on future event | Discount repayment, sale timing, contribution shares, transfer restrictions. | Right to Buy offer, title register, discount terms, mortgage statement. | Sale within discount repayment period can reduce net equity. |

Mortgage and secured lending, Family home, Jointly owned property, Solely owned property | ||||

Help to Buy equity loan repayment on sale or transfer | Contingent on future event Long-term arrangement | Redemption, valuation, authority consent, equity split after loan repayment. | Equity loan statement, Help to Buy documents, RICS valuation, mortgage statement. | Equity loan repayment is percentage-based and affects net proceeds. |

Family home, Solely owned property, Jointly owned property, Ongoing housing costs | ||||

Lodger or licensee living in the home | Immediate arrangement Short-term arrangement | Rent income, notice, consent, tax, mortgage or tenancy restrictions. | Lodger agreement, payment records, mortgage terms, insurance policy. | Account for rent income and check lender, landlord and insurer consent. |

Jointly owned property, Mortgage and secured lending, Ongoing housing costs | ||||

Rental income from jointly owned investment property | Long-term arrangement | Rent split, management, repairs, mortgage, tax, sale or retention. | Tenancy agreement, rent statements, mortgage statement, tax returns, invoices. | Separate property income, costs and tax from family home arrangements. |

Family home, Mortgage and secured lending, Ongoing housing costs | ||||

Letting out the former family home | Long-term arrangement Contingent on future event | Lender consent, landlord duties, rent split, agent, insurance, tax. | Mortgage terms, consent to let, insurance, tenancy agreement, gas safety record. | Do not let without checking mortgage, lease and insurance restrictions. |

Family home, Jointly owned property, Solely owned property, Ongoing housing costs | ||||

Safety duties when renting out the property | Immediate arrangement Long-term arrangement | Gas safety, electrical checks, deposit protection, repairs, agent duties. | Gas safety certificate, EICR, EPC, deposit certificate, tenancy agreement. | If retaining and letting property, allocate landlord compliance duties clearly. |

Family home, Jointly owned property, Solely owned property | ||||

Tax position on sale of former home | Contingent on future event Long-term arrangement | Sale timing, occupation history, tax advice, reporting, proceeds retention. | Purchase records, improvement invoices, completion statements, tax advice. | Tax may affect net proceeds where the property is no longer main residence. |

Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Stamp Duty Land Tax on property transfer | Long-term arrangement | Chargeable consideration, mortgage debt assumed, relief, filing responsibility. | Transfer deed, mortgage statement, consent order if any, SDLT advice. | Tax treatment can differ for separation, divorce and court-approved transfers. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Insolvency risk affecting the home | Immediate arrangement Long-term arrangement | Debt disclosure, creditor risk, equity protection, timing, specialist advice. | Credit reports, debt statements, charging orders, bankruptcy notices. | Property transfers may be vulnerable if made to avoid creditors. |

Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Charging order or judgment debt secured on property | Immediate arrangement Contingent on future event | Debt payer, redemption on sale, priority, indemnity, creditor contact. | Title register, court order, creditor statement, redemption figure. | Secured judgment debts may reduce sale proceeds before party division. |

Jointly owned property, Solely owned property, Family home | ||||

Restrictions or notices on the property title | Immediate arrangement Long-term arrangement | Purpose, removal, consent for sale, trust protection, lender requirements. | Official copy register, restriction entries, notices, Land Registry correspondence. | Check title early restrictions can delay sale or transfer completion. |

Jointly owned property, Solely owned property, Ongoing housing costs | ||||

Property outside the United Kingdom | Long-term arrangement Contingent on future event | Valuation, local law, sale, tax, currency, management costs. | Foreign title documents, mortgage statement, tax records, valuations. | UK agreement may need local legal steps for overseas property transfer. |

Jointly owned property, Solely owned property, Mortgage and secured lending, Ongoing housing costs | ||||

Second home or holiday property | Long-term arrangement Contingent on future event | Use, bookings, costs, sale, rent income, council tax, insurance. | Title register, mortgage statement, booking records, insurance, council tax bill. | Address occupancy, income and higher council tax charges separately from main home. |

Household contents, Family home, Ongoing housing costs | ||||

Home office, tools and business equipment kept at home | Immediate arrangement Short-term arrangement | Ownership, access, data, insurance, replacement, business continuity. | Asset list, invoices, business accounts, insurance, finance agreements. | Separate personal contents from business assets and financed equipment. |

Household contents, Ongoing housing costs | ||||

Furniture or appliances bought on finance | Immediate arrangement Short-term arrangement | Who keeps item, who pays finance, early settlement, default risk. | Finance agreement, statements, receipts, warranty documents. | Keeping an item does not automatically transfer finance liability. |

Family home, Rented property, Ongoing housing costs | ||||

Post, address updates and document access | Immediate arrangement Short-term arrangement | Mail forwarding, document collection, lender and council updates, privacy. | Royal Mail redirection, account update confirmations, key document list. | Protect confidential financial, medical and legal correspondence after moving out. |

Ongoing housing costs, Family home, Rented property | ||||

Temporary alternative accommodation costs | Immediate arrangement Short-term arrangement | Who pays, duration, deposit, overlap with home costs, reimbursement. | Short let agreement, hotel invoices, deposit receipt, bank statements. | Make clear whether support is temporary, repayable or part of maintenance. |

Rented property, Ongoing housing costs | ||||

Benefits and housing support after moving | Immediate arrangement Short-term arrangement | Claim update, rent liability, children, income change, overpayment risk. | Tenancy, rent statement, benefit award, separation date, income records. | Report household and rent changes promptly to avoid overpayments. |

Rented property, Ongoing housing costs, Family home | ||||

Applying for council housing after separation | Short-term arrangement Long-term arrangement | Local connection, children’s housing needs, evidence, homelessness risk. | Separation evidence, child arrangements, income records, notice or court papers. | Agreement should not undermine truthful evidence of housing need or residence. |

Family home, Rented property, Ongoing housing costs | ||||

Risk of homelessness after separation | Immediate arrangement | Safe accommodation, notice, local authority contact, children, belongings. | Notice, court order, tenancy, proof of children, income evidence. | Urgent housing advice may be needed before agreeing move-out dates. |

Family home, Ongoing housing costs | ||||

Housing arrangements linked to children’s schooling | Long-term arrangement Contingent on future event | School catchment, travel, bedrooms, sale delay, costs, review points. | School letters, child arrangements, mortgage or rent costs, travel costs. | Housing terms should align with realistic child arrangements and affordability. |

Jointly owned property, Solely owned property, Family home | ||||

Holding disputed sale proceeds pending agreement | Contingent on future event Short-term arrangement | Amount retained, stakeholder, release conditions, interest, dispute process. | Completion statement, solicitor undertaking, correspondence, draft settlement. | Useful where sale can proceed but equity division is unresolved. |

Mortgage and secured lending, Ongoing housing costs, Rented property, Jointly owned property | ||||

Indemnity for housing liabilities paid by one party | Immediate arrangement Long-term arrangement | Covered liabilities, payment evidence, reimbursement deadline, enforcement. | Bills, mortgage statement, rent account, bank statements. | Indemnity helps between parties but does not bind external creditors. |

Jointly owned property, Family home, Ongoing housing costs | ||||

Occupation charge where one co-owner remains in the home | Long-term arrangement Contingent on future event | Whether charge applies, amount, offset against mortgage, review date. | Valuation, local rent evidence, mortgage payments, occupation dates. | State whether sole occupation is rent-free or financially credited later. |

Ongoing housing costs, Mortgage and secured lending, Rented property | ||||

Set-off for missed housing contributions | Short-term arrangement Contingent on future event | Missed payments, evidence, interest, deduction from equity or deposit. | Bank statements, bills, rent or mortgage account, payment schedule. | Use a schedule so later deductions are transparent and verifiable. |

Solely owned property, Family home | ||||

Unmarried partner claim to share in sole-owned home | Long-term arrangement | Contributions, common intention, compromise amount, release of claims. | Bank records, title register, messages, renovation invoices, mortgage records. | Unmarried partners should be explicit about settlement of property claims. |

Jointly owned property, Solely owned property, Family home | ||||

Potential court application about property ownership or sale | Contingent on future event Long-term arrangement | Sale, occupation, beneficial shares, mediation, costs, evidence. | Title, declaration of trust, contribution evidence, valuations, correspondence. | A negotiated agreement can reduce litigation risk if ownership terms are clear. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending, Ongoing housing costs | ||||

Interaction with divorce financial remedy orders | Long-term arrangement Contingent on future event | Whether terms need consent order, disclosure, pension and income links. | Separation agreement, financial disclosure, draft consent order, property valuations. | Married couples often need a court-approved consent order for finality. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Civil partnership financial order affecting housing | Long-term arrangement Contingent on future event | Transfer, sale, occupation, mortgage release, consent order. | Civil partnership certificate, financial disclosure, valuation, title register. | Civil partners should align separation terms with any final court order. |

Family home, Jointly owned property, Solely owned property | ||||

Updating wills and property succession plans | Immediate arrangement Long-term arrangement | Will changes, severance, beneficiaries, life insurance, guardianship links. | Existing wills, title register, severance notice, life policy documents. | Property ownership form and wills should be reviewed together after separation. |

Mortgage and secured lending, Ongoing housing costs, Family home | ||||

Life insurance linked to the mortgage | Immediate arrangement Long-term arrangement | Premium payer, beneficiary, trust, cover amount, cancellation risk. | Policy schedule, trust deed, mortgage statement, beneficiary nomination. | Maintain cover if mortgage or child housing security depends on it. |

Ongoing housing costs, Family home, Household contents | ||||

Boiler, alarm and home maintenance contracts | Immediate arrangement Short-term arrangement | Account transfer, cancellation, payment split, access for engineers. | Service contracts, warranties, boiler records, alarm agreement. | Keep essential cover active where property is retained or being sold. |

Family home, Jointly owned property, Solely owned property | ||||

Preparing property documents for sale | Short-term arrangement | EPC, title documents, guarantees, property information forms, keys. | EPC, title register, TA6, guarantees, planning and building certificates. | Allocate responsibility for gathering sale documents to prevent delays. |

Boundary or neighbour dispute affecting sale | Contingent on future event Short-term arrangement | Disclosure, settlement, legal costs, sale impact, evidence gathering. | Title plan, correspondence, survey, legal letters, property information forms. | Known disputes may need disclosure to buyers and affect value. |

Family home, Jointly owned property, Solely owned property, Ongoing housing costs | ||||

Building safety or cladding issue affecting flat | Long-term arrangement Contingent on future event | Remediation costs, sale delay, service charges, mortgageability, valuation. | EWS1 if available, managing agent letters, service charge demands, valuation. | Building safety issues can delay sale and require cost-sharing provisions. |

Jointly owned property, Family home | ||||

Unequal deposit contributions to jointly owned home | Long-term arrangement Contingent on future event | Return of deposits, equity percentages, growth sharing, loss sharing. | Declaration of trust, bank statements, completion statement, title documents. | State formula precisely, especially whether deposits are fixed sums or percentages. |

Family home, Jointly owned property, Solely owned property | ||||

Family loan or gift used for property purchase | Long-term arrangement Contingent on future event | Loan or gift status, repayment, equity deduction, evidence, family expectations. | Gift letter, loan agreement, bank statements, conveyancing file. | Unclear family contributions can cause disputes when dividing sale proceeds. |

Mortgage and secured lending, Solely owned property, Jointly owned property | ||||

Equity release or lifetime mortgage on home | Long-term arrangement Contingent on future event | Redemption, interest roll-up, occupation, sale timing, advice requirement. | Equity release offer, redemption statement, title register, advice certificate. | Rolled-up interest can significantly reduce future equity. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Implementing property terms in a consent order | Contingent on future event Long-term arrangement | Order wording, transfer deadline, sale mechanics, mortgage release, default clauses. | Approved order, title register, mortgage consent, conveyancing documents. | Ensure separation agreement terms do not conflict with later court order. |

Family home, Jointly owned property, Solely owned property | ||||

Right for one party to buy the other out before open-market sale | Contingent on future event Long-term arrangement | Offer period, valuation method, mortgage approval, deposit, fallback sale. | Valuation, mortgage decision, title register, transfer documents. | Use strict deadlines so buyout option cannot indefinitely block sale. |

Jointly owned property, Family home, Solely owned property | ||||

Non-cooperation with sale, transfer or documents | Contingent on future event | Signing deadlines, agent instructions, price changes, default mechanism, costs. | Sale contract, agent letters, conveyancer correspondence, court order if needed. | Include cooperation duties and fallbacks to reduce deadlock. |

Ongoing housing costs, Household contents, Family home, Rented property | ||||

Moving, removals and cleaning costs | Immediate arrangement Short-term arrangement | Removal company, cleaning standard, payment split, booking date, access. | Quotes, invoices, inventory, check-out report. | Allocate practical moving costs, especially where sale proceeds are delayed. |

Household contents, Family home | ||||

Garden equipment, outdoor furniture and sheds | Short-term arrangement | Item allocation, fixtures, safety, removal damage, sale inclusion. | Inventory, photos, purchase receipts, sale fixtures list. | Identify fixtures included in a property sale separately from movable items. |

Family home, Household contents, Jointly owned property, Solely owned property | ||||

Fixtures and fittings on sale of the home | Contingent on future event Short-term arrangement | Included items, excluded items, replacement, buyer negotiations, proceeds split. | TA10 fixtures form, inventory, photos, sale contract. | Avoid promising the same item to a party and a buyer. |

Mortgage and secured lending, Ongoing housing costs, Family home | ||||

Mortgage payment holiday or lender support | Immediate arrangement Short-term arrangement | Application consent, credit impact, arrears, future payment increase, review. | Lender support offer, mortgage statement, affordability budget. | Record whether deferred payments are shared or borne by the occupier. |

Rented property, Mortgage and secured lending, Ongoing housing costs | ||||

Guarantor liability for rent or mortgage-related obligations | Immediate arrangement Long-term arrangement | Release request, indemnity, payment responsibility, communication with guarantor. | Guarantee agreement, tenancy, mortgage documents, arrears statements. | A private agreement may not release a guarantor without creditor consent. |

Family home, Solely owned property, Jointly owned property, Ongoing housing costs | ||||

Houseboat, caravan or mobile home used as family home | Immediate arrangement Long-term arrangement | Ownership, pitch or mooring fees, licence, insurance, sale or occupation. | Purchase documents, pitch agreement, mooring licence, insurance, finance agreement. | Check licence terms because occupation rights may differ from land ownership. |

Family home, Jointly owned property, Solely owned property, Mortgage and secured lending | ||||

Farm, smallholding or mixed residential-business property | Long-term arrangement Contingent on future event | Home value, business value, occupation, livestock, finance, tax advice. | Title, business accounts, valuations, loan documents, tenancy or grazing agreements. | Separate residential needs from business continuity and secured borrowing. |

What Property And Housing Issues Should A UK Separation Agreement Cover?

A separation agreement should record who will live in the family home, who will pay the mortgage, rent, council tax, utilities and insurance, and what will happen if the home is sold, transferred or retained. Where children are involved, housing arrangements should also align with child arrangements and school stability.

Why Are Mortgage And Tenancy Details Important?

If both names remain on a mortgage or tenancy, both parties may remain liable to the lender or landlord even if only one person stays in the property. A separation agreement can set out reimbursement, indemnity and review arrangements, but it usually cannot remove lender or landlord rights without their consent.

What Should Happen To Jointly Owned Property?

For jointly owned property, the agreement should identify whether the home will be sold, transferred to one party, retained until a trigger event, or occupied by one party temporarily. The parties should check the Land Registry title, mortgage balance, equity, valuation, and whether they hold the property as joint tenants or tenants in common.

Can One Partner Stay In A Solely Owned Or Rented Home?

Occupation rights may depend on marriage, civil partnership, ownership, tenancy terms, children, and any court orders. A non-owning spouse or civil partner may be able to protect home rights by registration, and tenants should check whether assignment, surrender or a new tenancy is needed.

What Records Help Avoid Disputes Over Contents And Bills?

A short inventory of household contents, meter readings, service contracts, insurance documents and bill accounts can prevent later disputes. The agreement should state who keeps key items, who pays outstanding bills, and when accounts will be transferred or closed.

FAQs

You Might Also Be Interested In