Financial Matters Checklist For UK Separation Agreements

Financial Topic | Priority Level | What To Consider | Useful Evidence | Common Issues |

|---|---|---|---|---|

Income and maintenance | ||||

Interim Spousal Maintenance | Essential | Whether one person will make regular support payments, amount, start date, review date and end date. | Payslips, bank statements, budgets, benefit letters and monthly expense schedules. | Unclear payments can cause arrears, dependence, pressure to return home or disputes about affordability. |

Child Maintenance Payments | Essential | Amount, payment frequency, receiving parent, annual review and whether CMS calculation will be followed. | CMS calculator results, income evidence, care pattern and Child Benefit records. | Informal amounts may become unfair if income or overnight care changes. |

Statutory Child Maintenance Rules | Essential | Whether the agreement should refer to statutory child maintenance rights and CMS jurisdiction. | Child Support Act 1991, CMS guidance and gross income information. | Private child maintenance clauses may not prevent a later CMS application where the law allows it. |

School Fees And Education Costs | Recommended | Who pays school fees, uniforms, trips, tutoring, equipment, exam fees and university support. | School invoices, fee schedules, trip letters, childcare invoices and education savings statements. | Parents may disagree whether extras are included in maintenance or paid separately. |

Childcare And Nursery Costs | Recommended | How nursery, childminder, after-school club and holiday club costs will be divided. | Invoices, childcare account records, Tax-Free Childcare statements and work schedules. | Costs can rise quickly if work patterns or care arrangements change. |

Income Disclosure | Essential | Whether both people will exchange accurate income information before setting support payments. | Payslips, P60s, tax returns, dividend vouchers, accounts and benefit statements. | Hidden or misunderstood income can make payments unrealistic or unfair. |

Bonuses, Commission And Overtime | Recommended | Whether variable income is shared, averaged, excluded or reviewed annually. | Employment contract, bonus letters, payslips, P60s and historic earnings records. | A fixed payment may be unfair where earnings fluctuate significantly. |

Self-Employed Or Company Director Income | Essential | How profits, drawings, dividends, retained earnings and tax liabilities affect support. | SA302s, company accounts, management accounts, dividend records and accountant letters. | Salary alone may understate available resources for maintenance. |

Income and maintenance, Tax and benefits | ||||

Benefits And Tax Credits As Income | Recommended | Whether benefits are included in budgets and whether separation changes entitlement. | Universal Credit journal, award letters, Child Benefit records and benefit calculator results. | New household status can change entitlement and cashflow quickly. |

Income and maintenance | ||||

Maintenance Review Triggers | Recommended | Review on job loss, illness, retirement, cohabitation, remarriage, house sale or child turning 18. | Redundancy letters, medical evidence, new payslips, tenancy or cohabitation evidence. | Without review triggers, old terms may become unworkable or disputed. |

Income and maintenance, Bank accounts and savings | ||||

Payment Method And Record Keeping | Recommended | Use standing orders, reference payments clearly and avoid cash unless receipts are kept. | Bank statements, standing order confirmations, receipts and payment schedules. | Cash or vague transfers can cause arguments about whether payments were made. |

Bank accounts and savings | ||||

Joint Current Accounts | Essential | Whether to freeze, close, convert or keep accounts for bills during transition. | Recent statements, direct debit list, overdraft terms and bank correspondence. | Either account holder may withdraw funds or increase overdraft if no limits are agreed. |

Joint Savings Accounts | Essential | How balances are divided, when transfers occur and whether funds are held for shared costs. | Statements, account terms, passbooks and evidence of contributions. | One person may withdraw savings before division is documented. |

Emergency Fund During Separation | Optional depending on circumstances | Whether joint savings will cover urgent child, home, car or medical expenses. | Savings statements, budget forecasts and expected repair or childcare costs. | No agreed reserve can leave urgent costs unpaid or paid unequally. |

Cash Held At Home | Optional depending on circumstances | Record amount, location, ownership and how cash will be divided or used. | Written inventory, photographs, withdrawal records and witness notes. | Cash is hard to trace and can lead to allegations of concealment. |

Bank accounts and savings, Pensions and investments | ||||

Individual Savings Accounts | Recommended | Identify ISA balances and whether each person keeps, transfers or offsets their own savings. | ISA statements, platform reports and historic contribution records. | Tax-free savings may be overlooked when comparing overall resources. |

Bank accounts and savings | ||||

Children's Savings And Junior ISAs | Recommended | Confirm funds belong to the child and who manages accounts until adulthood. | Junior ISA statements, child bank statements and trustee or registered contact details. | Child funds may be wrongly treated as parental assets. |

Personal Bank Accounts | Recommended | Whether balances are disclosed and whether any personal accounts are excluded or offset. | Statements for all current, savings and digital bank accounts. | Undisclosed accounts undermine trust and may affect later settlement discussions. |

Debts and liabilities, Bank accounts and savings | ||||

Joint Overdrafts | Essential | Who clears the overdraft, whether account use stops and how interest is paid. | Bank statements, overdraft facility letters and repayment proposals. | Both holders may remain liable to the bank regardless of private agreement. |

Debts and liabilities | ||||

Credit Card Debts | Essential | Identify cardholder, authorised users, balance origin and repayment responsibility. | Statements, credit agreements, transaction history and balance transfer records. | Main cardholder remains liable even if spending was by an additional cardholder. |

Personal Loans | Essential | Who borrowed, what the loan funded and who will make future repayments. | Loan agreement, statements, direct debit records and purpose evidence. | A private split does not release the named borrower from lender liability. |

Car Finance And Vehicle Loans | Recommended | Who keeps the vehicle, who pays finance, mileage limits and end-of-term charges. | Finance agreement, V5C, insurance certificate, MOT, valuation and settlement figure. | User and finance borrower may differ, causing liability for damage or missed payments. |

Hire Purchase Or Lease Agreements | Recommended | Whether agreements can be transferred, terminated or paid by the person using the item. | Hire purchase contracts, settlement figures, asset condition reports and invoices. | Ownership may not pass until final payment, limiting sale or transfer options. |

Debts and liabilities, Tax and benefits | ||||

HMRC Debts And Tax Arrears | Essential | Who is responsible for income tax, VAT, corporation tax, penalties or time-to-pay arrangements. | HMRC statements, self-assessment accounts, VAT returns and payment plans. | Tax debts may attract penalties and affect business cashflow if ignored. |

Debts and liabilities | ||||

Loans From Family Or Friends | Recommended | Whether the money was a gift or loan, repayment terms and who owes it. | Loan agreement, messages, bank transfers and repayment history. | Disputes often arise if family support was informal or undocumented. |

Guarantees And Personal Guarantees | Essential | Identify any guarantees for mortgages, leases, business borrowing or family loans. | Guarantee documents, lender letters, business loan agreements and lease paperwork. | A guarantor may remain exposed after separation unless the lender releases them. |

Indemnity For Agreed Debts | Recommended | Whether one person promises to reimburse the other if a shared debt is enforced. | Debt schedule, lender statements, repayment plan and proof of payments. | Indemnities help between the couple but do not bind banks or lenders. |

Debts and liabilities, Bank accounts and savings | ||||

Credit File Financial Associations | Optional depending on circumstances | Whether to close joint products and request disassociation from credit reference agencies. | Credit reports, account closure letters and notices of disassociation. | A former partner's credit conduct may affect borrowing if financial links remain. |

Property and mortgage | ||||

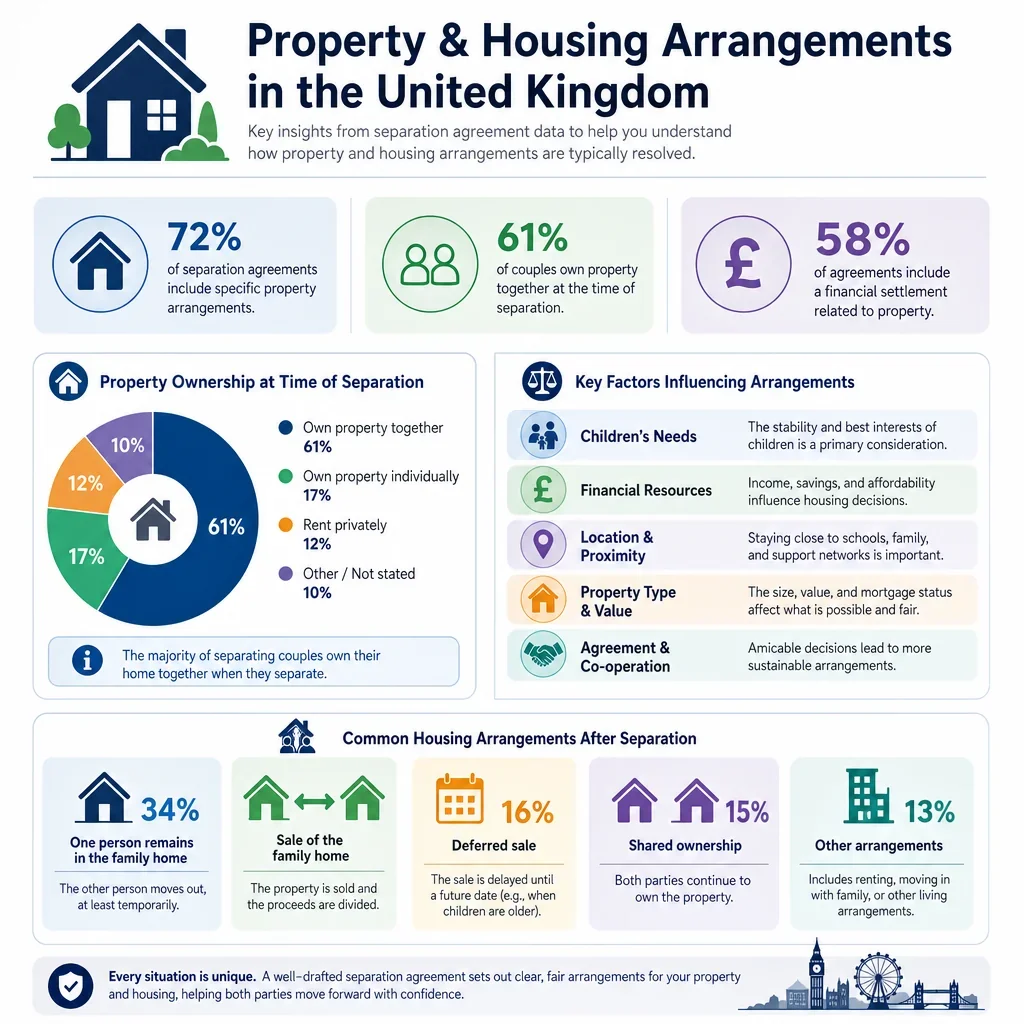

Occupation Of The Family Home | Essential | Who lives in the home, for how long and who pays mortgage, rent and bills. | Mortgage statement, tenancy agreement, bills, budgets and property valuation. | Occupation without payment terms can create arrears and resentment. |

Mortgage Payments | Essential | Who pays capital, interest, arrears, insurance-linked payments and overpayments. | Mortgage statements, lender correspondence, direct debit records and arrears letters. | Joint borrowers usually remain liable to the lender even if one moves out. |

Mortgage Lender Consent | Essential | Whether lender consent is needed for transfer, remortgage, payment holiday or release. | Mortgage offer, lender criteria, affordability assessment and consent letters. | Private agreement cannot force a lender to release a borrower. |

Sale Of The Family Home | Essential | Sale timing, agent choice, asking price, reductions, costs and division of net proceeds. | Valuations, estate agent terms, mortgage redemption figure and conveyancing estimates. | No sale mechanism can lead to stalemate over price or timing. |

Transfer Of Equity | Recommended | Whether one owner buys out the other and how release from mortgage is handled. | Title register, valuation, mortgage offer, redemption statement and conveyancer advice. | Legal ownership can remain unchanged if Land Registry and lender steps are not completed. |

Property Valuation Method | Essential | Agree market appraisal, surveyor valuation, valuation date and how disagreements are resolved. | Estate agent appraisals, RICS valuation, comparable sales and mortgage valuation. | Different values can significantly alter buyout sums or sale expectations. |

Beneficial Interests In Property | Essential | Record legal ownership, beneficial shares and whether a declaration of trust exists. | Title register, TR1, declaration of trust, mortgage deed and contribution records. | Legal title and beneficial ownership may differ, especially for unmarried couples. |

Matrimonial Home Rights | Recommended | Whether a spouse needs to protect occupation rights by registration. | Title register, marriage certificate and Land Registry home rights application. | A non-owning spouse may need protection if the property is in the other's sole name. |

Tenancy And Rent Liability | Essential | Who stays, who pays rent, deposit arrangements and whether landlord consent is needed. | Tenancy agreement, deposit certificate, landlord letters and rent statements. | Joint tenants may remain liable for rent after moving out. |

Property and mortgage, Tax and benefits | ||||

Second Homes And Holiday Properties | Optional depending on circumstances | Valuation, use, mortgage, tax, sale timing and division of proceeds. | Title documents, mortgage statements, valuations, rental records and tax returns. | Capital gains tax and running costs may be underestimated. |

Property and mortgage, Tax and benefits, Pensions and investments | ||||

Buy-To-Let Properties | Recommended | Rental income, mortgage, management costs, tax, sale or transfer and tenant obligations. | Tenancy agreements, rental accounts, mortgage statements, valuations and tax returns. | Rental income and tax liabilities may be overlooked when calculating resources. |

Property and mortgage, Insurance and household costs | ||||

Repairs And Maintenance Of Property | Recommended | Who pays urgent repairs, routine maintenance, improvements and pre-sale works. | Quotes, invoices, survey reports, photographs and service records. | Disagreements arise over whether works are necessary or an improvement. |

Property and mortgage | ||||

Household Contents And Furniture | Recommended | Which items each person keeps and whether any replacement payment is made. | Inventory, photos, receipts, valuations and removal quotes. | Sentimental or high-value items can cause disproportionate conflict. |

Pensions and investments | ||||

Pension Disclosure | Essential | Identify all workplace, personal, public sector and overseas pensions. | Cash equivalent values, annual statements, scheme booklets and State Pension forecasts. | Pensions are often valuable and may be missed if only cash assets are compared. |

Pension Sharing On Divorce | Recommended | Record whether pension sharing is intended later through a court order, not just private agreement. | Pension valuations, actuarial report, scheme rules and draft financial order advice. | A separation agreement alone cannot implement a pension sharing order. |

Pension Offsetting | Recommended | Whether one person keeps more non-pension assets in return for pension claims being reduced. | Pension CEVs, property equity, savings balances and actuarial advice. | Cash equivalent values may not reflect true retirement income value. |

State Pension Forecasts | Recommended | Check expected State Pension and National Insurance record gaps for retirement planning. | State Pension forecast and National Insurance contribution record. | A career break for childcare may reduce future retirement income. |

Stocks, Shares And Investment Accounts | Recommended | Identify holdings, value date, transferability, tax position and who keeps market risk. | Platform statements, share certificates, valuations and capital gains records. | Market movements between agreement and transfer can change values. |

Pensions and investments, Tax and benefits | ||||

Cryptocurrency And Digital Assets | Optional depending on circumstances | Disclose wallets, exchanges, value date, tax history and transfer method. | Exchange statements, wallet addresses, transaction history and tax reports. | Volatility, poor records and hidden wallets can cause disputes. |

Pensions and investments, Income and maintenance | ||||

Business Interests And Shares | Essential | Value shares, dividends, director loans, retained profits and control of business assets. | Company accounts, Companies House filings, shareholder agreements and valuation reports. | Business value and income may be confused or double counted. |

Pensions and investments, Debts and liabilities, Tax and benefits | ||||

Director Loan Accounts | Recommended | Identify money owed to or by the company and any tax consequences. | Company accounts, loan account ledgers, board minutes and accountant advice. | Withdrawals may be mistaken for income or ignored as a liability. |

Pensions and investments | ||||

Trust Interests | Optional depending on circumstances | Disclose beneficiary interests, distributions, trustees' discretion and expected income. | Trust deed, accounts, letters of wishes and distribution history. | Future or discretionary interests can be hard to value and easy to overlook. |

Inheritance And Expected Inheritance | Optional depending on circumstances | Whether received inheritance is shared, excluded, ring-fenced or used for housing needs. | Will, grant of probate, estate accounts and bank transfer records. | Mixing inheritance with joint funds can make ownership harder to evidence. |

Tax and benefits, Property and mortgage, Pensions and investments | ||||

Capital Gains Tax On Transfers Or Sales | Essential | Check CGT on property, shares or business transfers between separating spouses or partners. | Purchase records, valuations, sale statements, residence history and tax advice. | Unexpected CGT can reduce net sale proceeds or make a transfer unaffordable. |

Tax and benefits, Property and mortgage | ||||

Stamp Duty Land Tax | Recommended | Whether SDLT applies to property transfer, buyout, new purchase or additional dwelling surcharge. | Transfer terms, mortgage debt assumed, property values and conveyancer tax advice. | Assuming mortgage debt may create SDLT exposure even without a cash payment. |

Land Transaction Tax In Wales | Optional depending on circumstances | Check LTT if Welsh property is transferred or bought as part of separation. | Welsh property value, transfer terms, mortgage details and solicitor advice. | Using English SDLT assumptions for Welsh property may be wrong. |

Land And Buildings Transaction Tax In Scotland | Optional depending on circumstances | Check LBTT if Scottish property is transferred or bought as part of separation. | Scottish property value, transfer terms, mortgage details and solicitor advice. | Scottish property taxes and family law procedures differ from England and Wales. |

Tax and benefits, Insurance and household costs | ||||

Council Tax And Single Person Discount | Recommended | Who pays council tax and whether single person discount or exemptions apply. | Council tax bill, occupancy dates, student status and local authority correspondence. | Outdated occupancy details can lead to overpayment, arrears or incorrect discounts. |

Tax and benefits, Income and maintenance | ||||

Child Benefit Recipient | Recommended | Who claims Child Benefit and how this affects child maintenance and National Insurance credits. | Child Benefit award letter, HMRC account and care arrangement record. | Only one person can receive Child Benefit for a child at a time. |

Universal Credit Household Status | Essential | Report separation, housing costs, children, childcare and maintenance accurately. | Universal Credit journal, tenancy or mortgage evidence, childcare invoices and bank statements. | Incorrect household reporting can cause overpayments, underpayments or benefit fraud concerns. |

Tax and benefits | ||||

Tax Credits And Legacy Benefits | Optional depending on circumstances | Check whether separation changes tax credits, Housing Benefit or managed migration position. | Award notices, change of circumstances records and benefit adviser calculations. | A change may end legacy benefit entitlement and require Universal Credit advice. |

High Income Child Benefit Charge | Optional depending on circumstances | Check whether either household is affected by the Child Benefit tax charge. | Income records, Child Benefit claims, self-assessment returns and HMRC calculations. | The charge may be missed where Child Benefit is paid to the other parent. |

Tax Returns After Separation | Recommended | Who files returns, declares rental income, claims expenses and reports disposals. | SA302s, tax returns, P60s, rental statements and accountant letters. | Unreported income or gains can create later HMRC penalties. |

Marriage Allowance | Optional depending on circumstances | Check whether Marriage Allowance still applies and whether HMRC should be updated. | HMRC tax code notices, income records and marriage allowance claim records. | Tax codes may be wrong if relationship or income changes are not reported. |

Insurance and household costs | ||||

Utilities And Household Bills | Essential | Who pays gas, electricity, water, broadband, TV licence and service contracts. | Bills, account numbers, direct debits, meter readings and supplier correspondence. | Accounts in one name may build arrears for costs used by both households. |

Insurance and household costs, Property and mortgage | ||||

Buildings Insurance | Essential | Maintain cover, disclose occupancy changes and agree who pays premiums. | Policy schedule, mortgage conditions, renewal notice and insurer correspondence. | Insurance may be invalid if occupancy or ownership changes are not disclosed. |

Insurance and household costs | ||||

Contents Insurance | Recommended | Which address and contents are covered after one person moves out. | Policy schedule, inventory, receipts, valuations and change of address records. | Items moved to a new home may not be covered under the old policy. |

Life Insurance | Recommended | Whether policies secure mortgage, maintenance or child support obligations. | Policy schedule, trust documents, beneficiaries, premiums and mortgage balance. | A support obligation may be unsecured if the payer dies. |

Insurance and household costs, Income and maintenance | ||||

Income Protection And Critical Illness Cover | Optional depending on circumstances | Whether policies should continue to protect maintenance, mortgage or childcare payments. | Policy terms, benefit amount, waiting period, exclusions and premium records. | Illness or incapacity may stop agreed payments if no protection exists. |

Insurance and household costs | ||||

Private Medical Insurance | Optional depending on circumstances | Who remains covered, who pays premiums and whether children stay on the policy. | Policy schedule, employer benefits booklet, renewal quote and claims history. | Cover may end for a former partner when employment or marital status changes. |

Vehicle Insurance And Road Costs | Recommended | Named drivers, address, main user, premiums, tax, MOT and servicing costs. | Insurance certificate, V5C, MOT, service history and finance documents. | Wrong main driver or address can affect cover or claims. |

Subscriptions And Memberships | Optional depending on circumstances | Cancel, transfer or split streaming, gym, clubs, apps and family memberships. | Bank statements, app subscriptions, membership contracts and cancellation terms. | Small recurring costs can continue unnoticed on one person's account. |

Insurance and household costs, Property and mortgage | ||||

Moving And Set-Up Costs | Recommended | Who pays removals, deposits, furniture, appliance replacement and connection charges. | Removal quotes, tenancy deposit details, furniture receipts and budget estimates. | One person may be unable to rehouse without short-term financial support. |

Insurance and household costs | ||||

Pet Costs And Insurance | Optional depending on circumstances | Who keeps pets and pays food, vet bills, insurance and boarding. | Insurance policy, vet records, microchip details and regular cost records. | Unexpected vet bills can cause disputes if responsibility is not agreed. |

Pensions and investments, Insurance and household costs | ||||

Wills And Death Benefits | Recommended | Review wills, pension nominations, life policy beneficiaries and guardianship wishes. | Will, expression of wish forms, policy nominations and pension scheme records. | Old nominations may leave benefits to an unintended person after separation. |

Debts and liabilities, Income and maintenance | ||||

Legal, Mediation And Advice Costs | Recommended | How fees for solicitors, mediation, financial advice and valuations will be paid. | Fee estimates, mediation invoices, legal aid checks and savings balances. | Unequal access to advice may increase pressure or later challenge risk. |

Bank accounts and savings, Debts and liabilities, Property and mortgage, Pensions and investments | ||||

Schedule Of Assets And Liabilities | Essential | Attach a dated summary of assets, debts, income and pensions relied on when agreeing terms. | Bank statements, valuations, mortgage statements, pension CEVs, debt statements and payslips. | Without a disclosure schedule, later disputes may arise about what each person knew. |

Income and maintenance, Property and mortgage, Pensions and investments | ||||

Clean Break Intention | Recommended | State whether the couple intends final financial independence, subject to court order if divorcing. | Asset schedule, income budgets, legal advice notes and proposed consent order terms. | A separation agreement is not the same as a final divorce financial order. |

Income and maintenance, Property and mortgage, Pensions and investments, Tax and benefits | ||||

Financial Needs And Section 25 Factors | Essential | Consider income, earning capacity, needs, standard of living, age, disability and child welfare. | Budgets, medical evidence, childcare needs, housing needs, pensions and income records. | Terms ignoring needs or children may be harder to rely on later. |

Property and mortgage, Debts and liabilities, Bank accounts and savings | ||||

Cohabiting Partners' Property And Debt Position | Essential | Record ownership, contributions, debts and whether claims differ from divorce remedies. | Title register, declaration of trust, bank statements and contribution records. | Unmarried partners do not have the same financial claims as spouses or civil partners. |

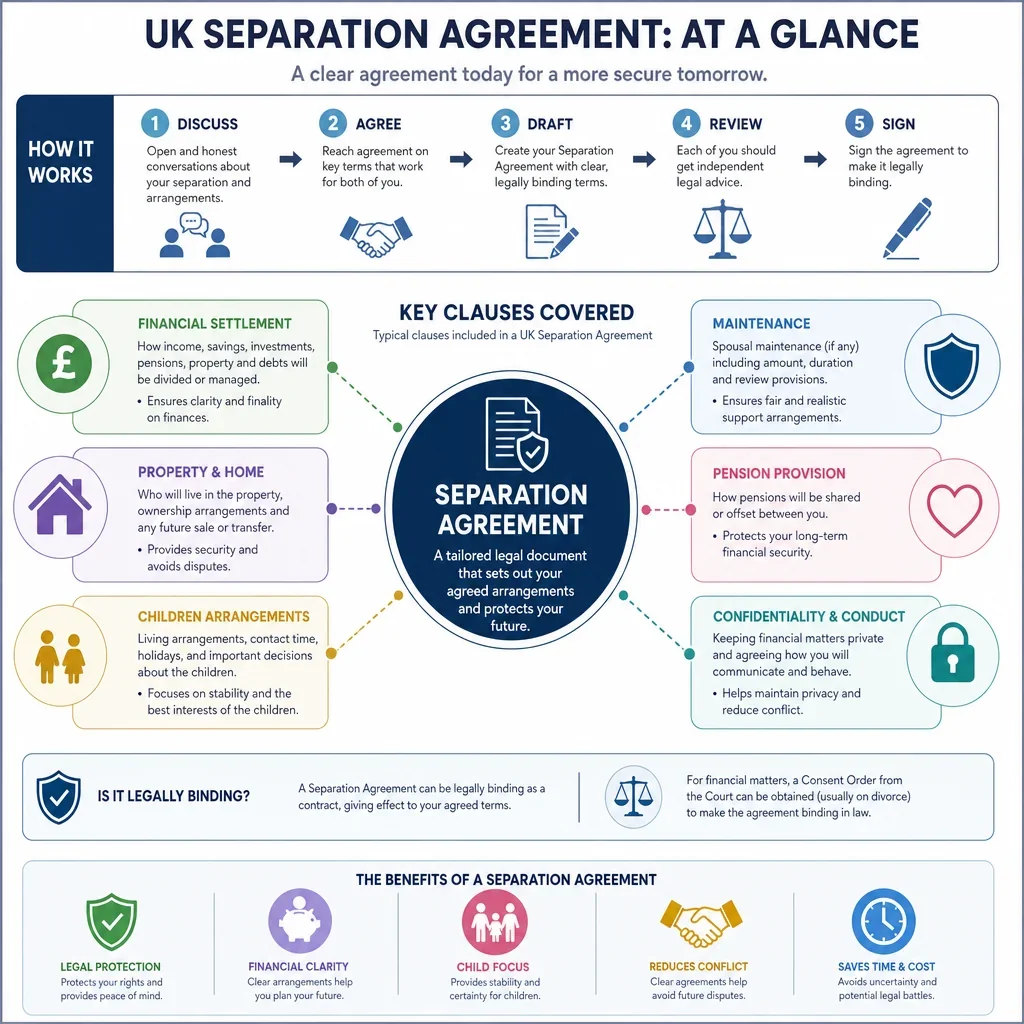

What Financial Issues Should A UK Separation Agreement Cover?

A strong separation agreement should record not only who pays what now, but also what happens if income, housing, mortgage payments, benefits, tax or debts change later. The most important items are usually maintenance, the family home, mortgage liability, joint debts, pensions and child-related costs.

Why Is Full Financial Disclosure Important?

Accurate disclosure helps each person understand the overall financial position before agreeing terms. Bank statements, mortgage statements, pension valuations, payslips, tax records and debt statements are particularly important where the agreement may later be considered by a court.

Which Financial Clauses Are Most Likely To Prevent Disputes?

- Mortgage and rent payments: state who pays, from what date, and what happens if payments are missed.

- Joint accounts and debts: decide whether accounts will be closed, frozen or divided, and who is responsible for overdrafts, loans and credit cards.

- Child maintenance and school costs: distinguish ordinary child maintenance from extras such as uniforms, trips, childcare and private school fees.

- Pensions: record whether pensions are excluded, shared later through divorce proceedings, or considered in return for other assets.

- Tax and benefits: check the effect of separation on council tax, Child Benefit, Universal Credit, capital gains tax and stamp duty land tax before signing.

When Should Legal Or Financial Advice Be Taken?

Independent advice is especially important where there is a home, pension, business, unequal income, large debt, inheritance, complex tax position or any pressure to sign quickly. A separation agreement is more likely to be useful if both parties understand the finances and have had a fair chance to take advice.

FAQs

You Might Also Be Interested In