United Kingdom Postnuptial Agreement Preparation Checklist

Checklist item | Reason needed | Typical relevance | Example evidence | Confidentiality level |

|---|---|---|---|---|

Personal details | ||||

Full legal names of both spouses | Identifies the contracting parties accurately. | Usually required | Passport, driving licence, deed poll | Medium |

Dates of birth | Supports identity checks and capacity context. | Usually required | Passport, birth certificate, driving licence | Medium |

Current residential addresses | Records residence and contact details. | Usually required | Utility bill, council tax bill, bank statement | Medium |

Nationality, domicile and immigration status | Helps identify jurisdiction and enforcement risks. | Often useful | Passport, visa, residence permit, domicile note | High |

Email addresses and phone numbers | Enables communication during preparation. | Usually required | Client information form | Medium |

Marriage and family details | ||||

Marriage certificate | Confirms the marriage and date. | Usually required | Certified marriage certificate | Medium |

Date and place of marriage | Shows marital timeline and jurisdictional links. | Usually required | Marriage certificate, ceremony records | Low |

Previous marriage or civil partnership documents | Identifies previous obligations and financial orders. | Circumstance dependent | Divorce order, final order, dissolution order | High |

Current separation or reconciliation status | May affect fairness and pressure concerns. | Often useful | Written chronology, correspondence, counselling notes | High |

Children names, ages and living arrangements | Children’s housing and care needs affect fairness. | Usually required | Birth certificates, parenting schedule, school letters | High |

Other dependants or stepchildren | Identifies wider financial responsibilities. | Circumstance dependent | Care agreements, benefit letters, support records | High |

Monthly household budget | Helps assess needs and affordability. | Often useful | Budget schedule, bills, bank statements | High |

Income | ||||

Employment status and job title | Shows income source and earning capacity. | Usually required | Employment contract, payslip, employer letter | Medium |

Salary, bonus and commission details | Assesses resources and future income. | Usually required | Payslips, P60, bonus letters | High |

Self-employed profits and drawings | Shows variable income and cash extraction. | Circumstance dependent | Tax returns, accounts, SA302, bank statements | High |

Dividends and director remuneration | Identifies company-derived income. | Circumstance dependent | Dividend vouchers, payslips, company accounts | High |

Rental income from property | Shows investment income and property returns. | Circumstance dependent | Tenancy agreement, rent statements, tax return | High |

Benefits, tax credits and child benefit | Records state support and dependants’ resources. | Circumstance dependent | Award letters, HMRC notices, bank entries | High |

Maintenance paid or received | Shows existing support obligations or income. | Circumstance dependent | Court order, CMS calculation, bank statements | High |

Expected income changes | Flags foreseeable changes in resources. | Often useful | Promotion letter, redundancy notice, retirement plan | High |

Property | ||||

Family home title details | Identifies ownership and legal title. | Usually required | Land Registry title register, title plan | High |

Family home market value | Assesses main housing asset value. | Usually required | Estate agent appraisals, RICS valuation | High |

Mortgage balance and repayment terms | Calculates equity and affordability. | Usually required | Mortgage statement, offer, redemption figure | High |

Declaration of trust for property | Shows beneficial shares and contributions. | Circumstance dependent | Declaration of trust, TR1, conveyancing file | High |

Pre-marital property owned by either spouse | Identifies assets to preserve or ring-fence. | Often useful | Old title registers, purchase completion statements | High |

Inherited or gifted property | Identifies non-matrimonial source arguments. | Often useful | Grant of probate, will, gift letter, title records | High |

Other UK properties | Captures additional real estate assets. | Circumstance dependent | Title registers, mortgage statements, valuations | High |

Overseas property interests | Flags foreign assets and enforcement issues. | Circumstance dependent | Foreign title deeds, valuations, tax records | High |

Property purchase and renovation contributions | Evidences source of funds and contributions. | Often useful | Completion statement, invoices, bank transfers | High |

Bank accounts | ||||

Current account balances | Shows liquid funds and cash flow. | Usually required | Recent bank statements, online balance screenshots | High |

Savings account balances | Identifies readily available capital. | Usually required | Savings statements, passbooks, online statements | High |

Joint account details | Shows shared funds and household arrangements. | Usually required | Joint bank statements, mandate details | High |

Foreign bank accounts | Captures overseas liquid assets. | Circumstance dependent | Foreign bank statements, tax disclosures | High |

Cash holdings above ordinary spending money | Completes disclosure of liquid assets. | Often useful | Cash schedule, safe deposit records | High |

Investments | ||||

ISAs and investment account balances | Identifies taxable and tax-free investments. | Usually required | Platform statements, ISA statements, portfolio reports | High |

Shares, bonds and funds | Shows capital assets and market exposure. | Usually required | Broker statements, share certificates, CREST records | High |

Cryptoassets and digital wallets | Captures volatile digital investments. | Circumstance dependent | Exchange statements, wallet records, tax reports | High |

Premium Bonds and fixed-term savings | Identifies low-risk savings assets. | Often useful | NS&I statements, savings certificates | High |

Valuable personal possessions | Captures high-value chattels and collections. | Circumstance dependent | Valuations, insurance schedules, purchase receipts | High |

Cars, boats and other vehicles | Identifies valuable movable assets and loans. | Often useful | V5C, finance agreement, valuation, receipt | Medium |

Pensions | ||||

All pension scheme details | Identifies retirement assets for disclosure. | Usually required | Annual pension statements, provider letters | High |

Pension cash equivalent values | Values pension rights for comparison. | Usually required | CETV statement, scheme valuation letter | High |

State Pension forecast | Shows expected state retirement income. | Often useful | State Pension forecast | High |

Pension contributions during marriage | Distinguishes marital and non-marital accrual. | Often useful | Payslips, pension statements, contribution history | High |

Pension tax protections and restrictions | Flags tax issues affecting pension division. | Circumstance dependent | HMRC protection certificates, scheme letters | High |

Business assets | ||||

Company shares or partnership interests | Identifies ownership, control and value. | Circumstance dependent | Companies House filings, share certificates, partnership deed | High |

Recent business accounts | Supports valuation and income assessment. | Circumstance dependent | Filed accounts, management accounts, tax computations | High |

Shareholder or partnership agreements | Shows transfer limits and valuation mechanisms. | Circumstance dependent | Shareholders’ agreement, articles, partnership deed | High |

Director loans and business debts | Shows liabilities linked to business ownership. | Circumstance dependent | Loan account, balance sheet, facility letters | High |

Intellectual property and royalties | Captures valuable rights and income streams. | Circumstance dependent | IP registrations, licence agreements, royalty statements | High |

Debts | ||||

Credit card balances | Shows unsecured liabilities and repayments. | Usually required | Credit card statements, credit report | High |

Personal loans and overdrafts | Identifies borrowing and monthly commitments. | Usually required | Loan agreements, overdraft statements, credit report | High |

Student loan balances | Shows income-linked liabilities. | Circumstance dependent | Student Loans Company statement, payslip deductions | High |

Family loans or informal borrowing | Clarifies whether advances are loans or gifts. | Often useful | Loan agreement, bank transfers, correspondence | High |

Outstanding tax liabilities | Identifies priority debts and net resources. | Often useful | HMRC statements, tax returns, payment plans | High |

Guarantees and contingent liabilities | Flags possible future liabilities. | Circumstance dependent | Guarantee deeds, facility letters, indemnities | High |

Insurance | ||||

Life insurance policies | Shows protection for spouse, children or debts. | Often useful | Policy schedule, trust form, beneficiary nomination | High |

Income protection and critical illness cover | Shows financial resilience if health changes. | Often useful | Policy documents, employer benefit summary | High |

Private medical insurance arrangements | May affect needs and benefit packages. | Circumstance dependent | Policy schedule, employer benefits statement | High |

Home and contents insurance schedule | Evidences valuable contents and insured property. | Often useful | Insurance schedule, high-value item list | Medium |

Estate planning | ||||

Current wills | Checks consistency with inheritance intentions. | Often useful | Signed will, codicil, solicitor storage letter | High |

Trust interests and beneficiary rights | Identifies trust assets, expectations and limits. | Circumstance dependent | Trust deed, letters of wishes, accounts | High |

Expected inheritances or family gifts | May explain future ring-fencing intentions. | Circumstance dependent | Gift letter, family correspondence, estate summary | High |

Lasting powers of attorney | Shows who can make decisions if capacity is lost. | Circumstance dependent | Registered LPA, OPG access code | High |

Pension death benefit nominations | Checks beneficiary intentions outside the will. | Often useful | Expression of wish form, scheme confirmation | High |

Other documents | ||||

Any pre-existing prenuptial or postnuptial agreement | Shows existing agreed terms or variations. | Circumstance dependent | Signed agreement, schedules, review correspondence | High |

Independent legal advice records | Supports informed and voluntary agreement. | Often useful | Advice certificate, solicitor letters, attendance notes | High |

Summary schedule of all assets and debts | Provides clear snapshot of net positions. | Usually required | Asset schedule, Form E-style summary, spreadsheet | High |

Relationship and financial chronology | Explains acquisition, contributions and timing. | Often useful | Chronology, key event timeline, supporting documents | High |

Reasons for making the postnuptial agreement | Clarifies aims such as protection or reconciliation. | Usually required | Instruction note, joint statement, correspondence | High |

Proposed terms for separation, divorce or death | Defines what the agreement should cover. | Usually required | Term sheet, heads of agreement, draft clauses | High |

Review dates and trigger events | Keeps terms current after major changes. | Often useful | Draft review clause, family planning note | Medium |

Evidence of voluntary agreement and timing | Helps address duress or pressure concerns. | Often useful | Email trail, meeting notes, signing timetable | High |

Matrimonial Causes Act 1973 section 25 factors | Court considers resources, needs, children and fairness. | Usually required | Needs schedule, disclosure bundle, legal advice note | Medium |

Radmacher v Granatino fairness and autonomy principles | Explains weight given to nuptial agreements. | Usually required | Legal advice note, drafting checklist | Medium |

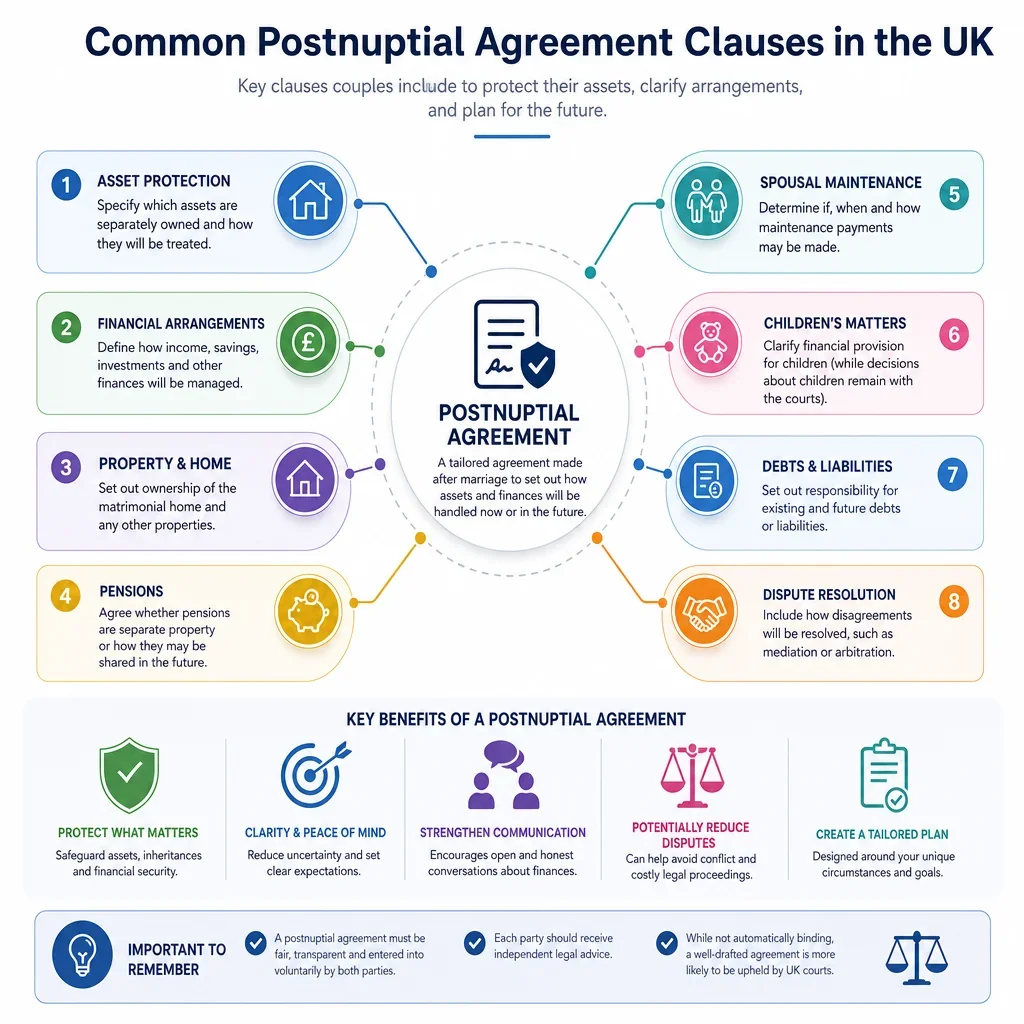

What Should You Gather Before Making A UK Postnuptial Agreement?

A useful postnuptial agreement checklist should start with full financial disclosure: identity details, family circumstances, income, property, bank accounts, investments, pensions, business interests, debts, insurance and estate planning documents. In England and Wales, a nuptial agreement is more likely to carry weight if each spouse entered it freely, with a full appreciation of its implications and if the outcome is fair.

Which Documents Are Most Sensitive In A Postnuptial Agreement?

The highest sensitivity items are usually bank statements, tax returns, pension valuations, business accounts, mortgage details, debts, trusts, wills and medical or life insurance information. These documents can reveal net worth, income sources, liabilities, beneficiaries and dependants, so they should be shared securely and only with the people preparing or advising on the agreement.

Why Are Pensions And Property Especially Important?

UK postnuptial agreements often need clear evidence of home ownership, mortgage liabilities, pension values and any pre-marital or inherited contributions. These assets can be among the most valuable matrimonial resources and may affect whether the agreement meets housing, income and retirement needs if the marriage later ends.

When Should Legal Advice Be Considered?

Independent legal advice is not a statutory formality, but it is highly relevant to weight and fairness. Each spouse should usually have time to review disclosure, understand the proposed terms and consider advice before signing, especially where there are children, unequal wealth, businesses, trusts, pensions, international assets or significant debts.

FAQs

You Might Also Be Interested In