Common Postnuptial Agreement Clauses In The UK

Clause name | Purpose | Typical importance | Drafting considerations | Supporting information |

|---|---|---|---|---|

Financial disclosure | ||||

Full financial disclosure clause | Confirms that both spouses have exchanged full details of assets, debts, income and pensions before signing. | Central inadequate disclosure can weaken the agreement. | Define the disclosure date, level of detail, valuation basis and whether updates are required before signature. | Asset schedule, bank statements, mortgage statements, pension statements, payslips, tax returns and company accounts. |

Accuracy of disclosure warranty | Requires each spouse to confirm that their financial disclosure is accurate and not misleading. | Central where the agreement relies on disclosed figures. | Avoid absolute wording if figures are estimates identify known omissions or pending valuations. | Signed disclosure schedules, valuation reports and written explanations of estimates. |

Later-discovered assets clause | Sets out what happens if a material asset, income source or debt was not disclosed before signing. | Important where finances are complex or fast-changing. | Define materiality and whether non-disclosure triggers review, variation or a specific adjustment. | Updated asset schedules, correspondence and evidence of discovery date. |

Acknowledgement of financial understanding | Records that each spouse understands the broad financial effect of the agreement. | Central for informed consent. | Use plain English and avoid suggesting legal advice was unnecessary. | Disclosure schedule, advice letters and signed certificate of independent advice. |

Updated disclosure before completion clause | Requires updated financial information if there is a delay between drafting and signing. | Useful where assets are volatile or negotiations take time. | Set a cut-off date and specify which changes must be reported. | Latest statements, updated valuations and revised liability balances. |

Property ownership | ||||

Pre-marital assets clause | Identifies property owned before marriage and states whether it should be kept separate. | Central where one spouse entered the marriage with significant assets. | Describe assets precisely and address growth, substitutions, mingling and use for family purposes. | Title registers, completion statements, portfolio statements and historic valuations. |

Family home ownership clause | Sets out how the matrimonial home is owned, occupied, sold or transferred on separation. | Central in most agreements involving a home. | Consider children's housing needs, mortgage affordability, sale timing and beneficial ownership. | Land Registry title, mortgage offer, trust deed, valuation and occupation costs. |

Joint property division clause | Explains how jointly owned properties should be divided, sold or transferred if the spouses separate. | Central where there is jointly owned real estate. | Specify shares, valuation method, sale process, transfer mechanics and responsibility for tax and costs. | Title documents, declarations of trust, mortgage balances, estate agent appraisals and rental statements. |

Sole property retention clause | States whether a property in one spouse's name is to remain that spouse's separate property. | Important where title ownership differs from family use. | Address mortgage contributions, renovations, occupation rights and any beneficial interest claim. | Title register, mortgage statements, contribution records and renovation invoices. |

Mortgage responsibility clause | Allocates responsibility for mortgage payments, secured loans and refinancing obligations. | Central where property is mortgaged. | Check lender consent, affordability and whether indemnities are realistic. | Mortgage statements, loan agreements, redemption figures and lender correspondence. |

Property valuation mechanism clause | Provides a method for valuing property if sale, transfer or buyout is required. | Important where property may be retained by one spouse. | Specify market value, valuation date, valuer qualifications and how disputes are resolved. | RICS valuation, estate agent appraisals and comparable sale evidence. |

Occupation pending sale clause | Sets out who may live in the home while sale, transfer or divorce proceedings are ongoing. | Important where separation living arrangements may be disputed. | Must not override statutory occupation or domestic abuse protections. | Housing needs assessment, mortgage costs and children's school or care arrangements. |

Personal belongings and contents clause | Allocates furniture, jewellery, vehicles, art and personal items if the spouses separate. | Useful to avoid disputes over valuable or sentimental items. | List high-value items separately and address insurance, storage and valuation. | Inventory, purchase receipts, photographs, insurance schedules and valuations. |

Foreign property clause | Deals with non-UK property and how it should be valued, used or transferred. | Situational important for international families. | Take local law advice on enforceability, tax, title and transfer restrictions. | Foreign title deeds, local valuations, tax advice and translated documents. |

Savings and investments | ||||

Bank account ownership clause | States how sole and joint bank accounts should be treated during marriage and on separation. | Common and often central for liquid assets. | Distinguish pre-existing balances, salary deposits, joint spending and separation-date balances. | Bank statements, account mandates and balance schedules. |

Savings retention clause | Identifies savings that are to be retained separately or divided in agreed proportions. | Common where one or both spouses hold significant cash savings. | Address interest, withdrawals, substitutions and whether emergency funds are excluded. | Savings statements, ISA statements and source-of-funds evidence. |

Investment portfolio clause | Sets out how shares, funds, ISAs and investment accounts are owned and divided. | Important where investment assets are material. | Deal with gains, losses, dividends, tax wrappers and the valuation date. | Broker statements, tax reports, CGT calculations and portfolio valuations. |

Future savings allocation clause | Explains whether savings accumulated after signing are joint, separate or partly shared. | Useful where earnings or saving capacity differ significantly. | Define qualifying savings and avoid unfair outcomes if one spouse reduces work for family reasons. | Income records, savings statements and family budget evidence. |

Cryptocurrency and digital assets clause | Identifies cryptoassets, online accounts and digital investments and states how they are treated. | Situational important for volatile or hard-to-trace assets. | Specify valuation source, wallet control, tax position and evidence without exposing private keys. | Exchange statements, wallet addresses, tax reports and valuation screenshots. |

Life policy and investment bond clause | States ownership, beneficiaries and treatment of life policies or investment bonds. | Useful where policies have surrender value or protect maintenance obligations. | Check trust status, surrender value, beneficiary nominations and premium responsibility. | Policy schedules, trust deeds, surrender valuations and beneficiary forms. |

Pensions | ||||

Pension disclosure and valuation clause | Requires pension details and values to be disclosed before pension arrangements are agreed. | Central where either spouse has pension rights. | Use current cash equivalent values and consider actuarial advice for defined benefit schemes. | CETV statements, scheme booklets, state pension forecasts and actuarial reports. |

Pension sharing intention clause | Records whether the spouses intend pensions to be shared, offset or retained separately on divorce. | Central where pensions are a significant part of wealth. | A pension sharing order normally requires court process avoid wording that assumes automatic transfer. | Pension valuations, scheme rules, actuarial advice and draft financial order. |

Pension offsetting clause | Allows one spouse to keep pension rights while the other receives different assets instead. | Useful where pension division is impractical or unwanted. | Do not equate pension value directly with cash without actuarial or financial advice. | CETV, actuarial offset report, property valuations and liquidity analysis. |

Future pension accrual clause | States whether pension contributions and growth after signing are separate or shareable. | Important in longer marriages or where income is unequal. | Consider non-financial contributions, childcare, career breaks and retirement needs. | Contribution history, employment records and pension forecasts. |

State pension information clause | Requires each spouse to obtain and disclose their UK State Pension forecast. | Useful where retirement provision is limited or unequal. | Account for National Insurance gaps and differences between state and private pension rights. | State Pension forecast and National Insurance record. |

Debts and liabilities | ||||

Pre-existing debt clause | States that debts incurred before the agreement remain the responsibility of the original borrower. | Central where either spouse has significant debt. | Identify secured, unsecured, tax, student and business debts separately. | Credit reports, loan statements, HMRC statements and repayment plans. |

Future borrowing clause | Sets rules for responsibility for borrowing taken out after signing. | Important where either spouse may take on new credit. | Distinguish joint household borrowing from individual borrowing and require written consent for joint liability. | Loan agreements, credit card statements and written borrowing approvals. |

Credit card liability clause | Allocates responsibility for credit card balances and spending after separation. | Common where household spending uses credit cards. | Clarify authorised users, balance dates and whether family expenses are shared. | Card statements, account terms and spending records. |

Tax liability clause | Allocates responsibility for personal, business or property tax liabilities. | Important for self-employed spouses, landlords and business owners. | Address unknown assessments, penalties, interest and indemnities for tax caused by one spouse. | Tax returns, HMRC statements, accountant letters and company tax records. |

Personal guarantee clause | Identifies guarantees given for business, property or family borrowing and allocates risk. | Situational but high importance if guarantees exist. | Check whether a lender will release a guarantor private indemnities do not bind lenders. | Guarantee deeds, facility letters, lender correspondence and indemnity documents. |

Debt indemnity clause | Requires one spouse to reimburse the other if they have to pay a debt allocated to that spouse. | Important where liabilities cannot be immediately transferred or discharged. | Ensure the indemnifying spouse has realistic means to pay and specify enforcement costs. | Debt schedules, repayment evidence and correspondence with creditors. |

Bankruptcy and insolvency risk clause | Addresses the effect of bankruptcy, insolvency or creditor claims on agreed financial arrangements. | Situational important if either spouse is financially exposed. | Do not draft arrangements intended to defeat creditors insolvency law may override private agreements. | Credit reports, insolvency searches, creditor schedules and business accounts. |

Inheritance and gifts | ||||

Existing inheritance clause | States whether inherited assets already received should remain separate property. | Central where inherited wealth is significant. | Address mingling, use for family needs, income generated and replacement assets. | Grant of probate, estate accounts, transfer records and asset valuations. |

Future inheritance clause | States how inheritances received after signing should be treated if the marriage ends. | Common where family wealth is expected. | Avoid assuming inheritance will be received address separate accounts and use for family expenses. | Will extracts, trust letters, estate planning documents and inheritance records. |

Family gift clause | Clarifies whether gifts from relatives are individual property or shared marital property. | Important where parents contribute to homes, businesses or savings. | Distinguish gifts from loans and record the donor's intention clearly. | Gift letters, bank transfers, donor correspondence and loan agreements if applicable. |

Trust interest clause | Identifies beneficial interests, discretionary interests or expectations under family trusts. | Situational but important for family wealth planning. | Do not overstate control of discretionary trusts consider trustee and tax advice. | Trust deed, letters of wishes, accounts, distribution history and trustee correspondence. |

Will and estate planning consistency clause | Confirms that wills and estate planning should be reviewed to avoid conflict with the agreement. | Important where death and divorce planning overlap. | Marriage may affect wills take estate planning advice and avoid contradictory beneficiary provisions. | Current wills, codicils, life policy nominations and estate planning letters. |

Family loan clause | Records whether money from relatives is a repayable loan and who is responsible for repayment. | Important where family money funds property or business assets. | Use a written loan agreement with repayment terms, interest and security if intended as debt. | Loan agreement, bank transfers, repayment records and donor or lender statements. |

Business interests | ||||

Business ownership clause | Identifies business interests and states whether ownership or value should be shared or retained. | Central for business owners and shareholders. | Address shares, control, valuation, liquidity, dividends and pre-marital value. | Company accounts, Companies House records, shareholder agreements and valuations. |

Business valuation mechanism clause | Sets the process for valuing a company, partnership or sole trader business. | Important where business value may affect settlement terms. | Specify valuer expertise, valuation date, minority discounts, goodwill and tax treatment. | Management accounts, tax returns, valuations, forecasts and shareholder documents. |

Business growth and retained earnings clause | Explains whether future growth, retained profits and reinvested earnings are separate or shareable. | Important where one spouse expects a business to grow materially. | Separate passive growth from active marital effort and unpaid spousal contributions. | Historic accounts, salary records, dividend records and business plans. |

Spousal business contribution clause | Records whether a spouse's work, advice or unpaid support creates any claim to business value. | Useful where one spouse works in the other spouse's business. | Deal with salary, dividends, share options, directorships and unpaid labour fairly. | Employment contracts, payroll records, board minutes and role descriptions. |

Professional practice clause | Deals with interests in medical, legal, accountancy or other professional practices. | Situational important for partners and members of LLPs. | Review partnership or LLP restrictions on transfer, valuation, retirement and capital accounts. | Partnership agreement, LLP agreement, accounts and capital account statements. |

Share options and incentive awards clause | States how share options, RSUs, carried interest or bonus-linked awards are treated. | Important for executives, founders and finance professionals. | Address vesting dates, performance conditions, tax, liquidity and whether awards reward past or future work. | Award letters, scheme rules, vesting schedules and tax advice. |

Business liabilities and director loan clause | Allocates responsibility for business debts, director loans and overdrawn loan accounts. | Important where personal and business finances overlap. | Check company accounts, tax consequences and whether liabilities are personal or corporate. | Company accounts, director loan ledgers, facility agreements and guarantees. |

Review and variation | ||||

Scheduled review clause | Requires the spouses to review the agreement at set intervals. | Central for long-term fairness and relevance. | Set review dates and state whether non-review affects the agreement. | Calendar review dates, updated disclosure and legal advice records. |

Trigger event review clause | Requires review after major changes such as children, illness, relocation, inheritance or business sale. | Central where future circumstances may change significantly. | List clear triggers and deadlines for review discussions and fresh advice. | Birth certificates, medical evidence, relocation documents, inheritance records and sale agreements. |

Variation in writing clause | States that changes to the agreement must be written, signed and usually supported by advice. | Central to avoid informal uncertainty. | Specify execution requirements and whether fresh disclosure is needed for variations. | Deed of variation, updated schedules and advice certificates. |

Reconciliation clause | States whether the agreement continues if the spouses separate and later resume living together. | Situational but useful where separation has already occurred. | Define reconciliation and consider whether financial arrangements during separation alter the agreement. | Separation correspondence, living arrangements and updated financial disclosure. |

Sunset clause | Provides that some or all terms expire after a set period or event. | Situational useful where fairness changes over time. | State whether expiry is automatic and which clauses survive. | Timeline of marriage, review notes and updated financial projections. |

General legal terms | ||||

Independent legal advice clause | Records that each spouse had the opportunity to receive separate legal advice before signing. | Central lack of advice may reduce weight given to the agreement. | Each spouse should use a different adviser and have time to consider the advice. | Solicitor letters, advice certificates and attendance notes. |

Free will and no pressure clause | Records that both spouses sign voluntarily without duress, undue pressure or exploitation. | Central for the agreement's persuasive weight. | Avoid last-minute signing and record any negotiation history. | Negotiation correspondence, draft history and solicitor confirmation letters. |

Understanding of legal effect clause | Records that each spouse understands the agreement may influence financial outcomes on divorce. | Central for informed consent. | Avoid saying the court is bound explain the intended persuasive effect. | Legal advice letters and signed acknowledgements. |

Court discretion acknowledgement clause | Confirms that the agreement cannot remove the court's powers in financial remedy proceedings. | Central in England and Wales. | Draft consistently with the Matrimonial Causes Act 1973 and avoid absolute exclusion wording. | Legal advice notes and draft financial remedy order if divorce occurs. |

Children's needs safeguard clause | States that arrangements should not prejudice the welfare or financial needs of any children. | Central where there are or may be children. | Do not attempt to restrict child maintenance or housing needs unfairly. | Children's ages, care arrangements, school costs and housing needs evidence. |

Spousal maintenance clause | Sets expectations about ongoing financial support between spouses after separation or divorce. | Central where income or earning capacity differs. | Consider needs, childcare, disability, earning capacity, term, indexation and clean break aims. | Budgets, income evidence, childcare costs, medical evidence and earning capacity reports. |

Clean break intention clause | Records whether the spouses intend to achieve financial independence after divorce where fair. | Common but depends on needs and affordability. | Do not assume a clean break is fair if needs cannot be met. | Income forecasts, housing budgets, pension forecasts and needs analysis. |

Lump sum payment clause | Sets out any agreed lump sum payable on separation or divorce. | Useful where a simple balancing payment is intended. | Specify amount, timing, interest, funding source and tax consequences. | Liquidity evidence, bank statements, tax advice and payment schedule. |

Separation trigger clause | Defines when the agreement's separation-related provisions take effect. | Central for operational clarity. | Define separation by written notice, living apart or intention to end the relationship. | Written separation notice, correspondence and living arrangement evidence. |

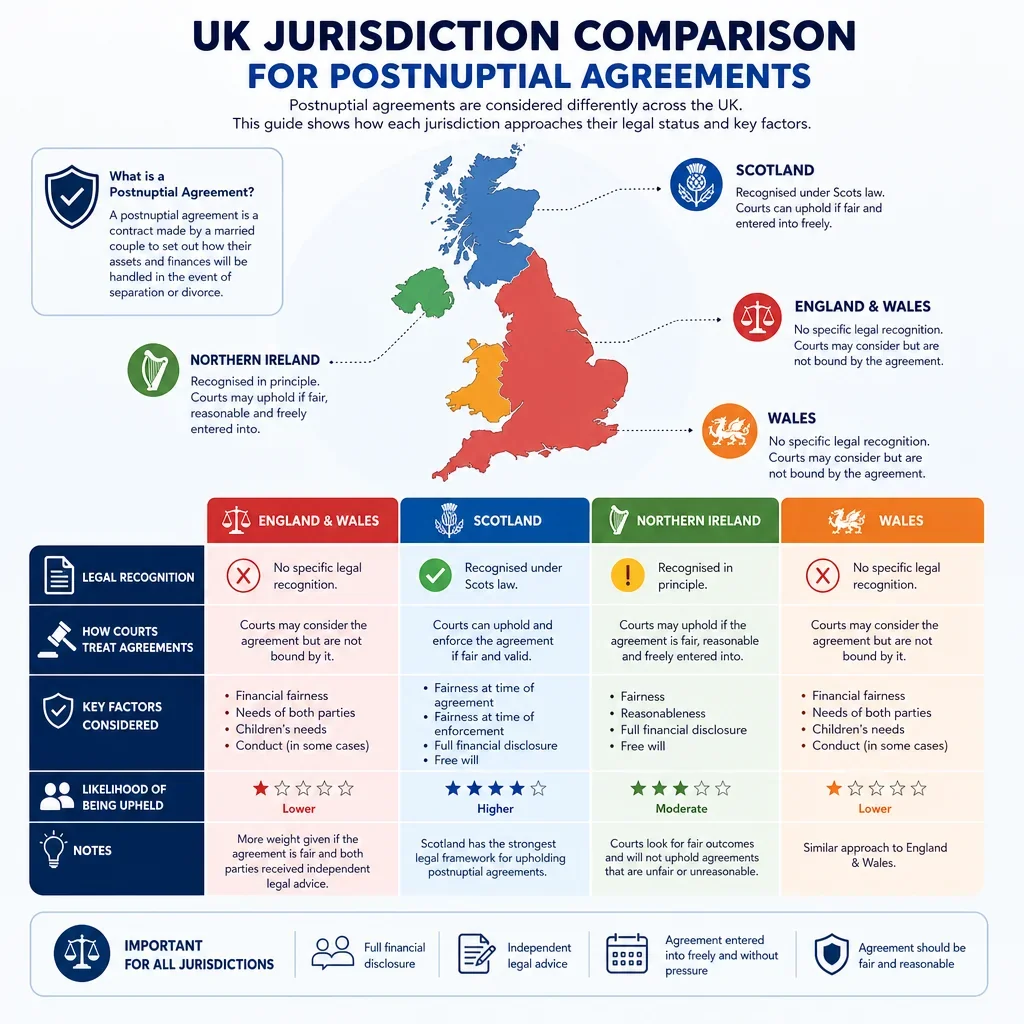

Governing law and jurisdiction clause | States which UK legal system is intended to govern interpretation and where disputes should be heard. | Important for couples with cross-border connections. | England and Wales, Scotland and Northern Ireland have distinct family law systems take local advice. | Residence evidence, nationality documents, property locations and foreign legal advice. |

Severability clause | Provides that invalid or ineffective terms should not necessarily undermine the whole agreement. | Standard supporting clause. | Avoid relying on severability to save fundamentally unfair arrangements. | Final agreement and legal advice notes. |

Entire agreement clause | States that the written agreement records the spouses' agreed financial intentions. | Standard supporting clause. | Do not use it to hide undisclosed side agreements or misrepresentations. | Draft history, side letters and written confirmations of no other agreements. |

Confidentiality clause | Limits disclosure of the agreement and related financial information to permitted people and processes. | Useful for privacy, especially with business or high-profile finances. | Allow disclosure to courts, advisers, tax authorities, lenders and as legally required. | Confidentiality undertakings and adviser engagement letters. |

Dispute resolution | ||||

Mediation before proceedings clause | Encourages spouses to try mediation before contested court proceedings where suitable. | Useful where cooperative resolution is intended. | Include exceptions for urgency, domestic abuse, safeguarding or risk of asset dissipation. | Mediator details, MIAM records and correspondence about dispute resolution. |

Family arbitration clause | Provides for financial disputes to be referred to family arbitration if both spouses proceed with it. | Situational useful for privacy and speed. | Clarify that court approval may still be needed for enforceable financial orders. | Arbitration agreement, arbitrator appointment and procedural directions. |

Expert determination clause | Allows a neutral expert to decide valuation or technical disputes such as property or business value. | Useful for valuation-heavy agreements. | Define expert qualifications, appointment process, information rights and cost sharing. | Expert letters, valuation instructions and source documents. |

Structured negotiation clause | Sets staged discussions, disclosure updates and deadlines before formal proceedings are started. | Useful for reducing conflict and delay. | Keep timelines realistic and preserve urgent court options. | Negotiation timetable, updated disclosure and solicitor correspondence. |

General legal terms | ||||

Legal costs clause | States how drafting, advice, review or dispute costs should be paid. | Common supporting clause. | Avoid cost arrangements that compromise independent advice or create pressure to sign. | Solicitor invoices, payment records and engagement letters. |

Execution as deed clause | Provides for the agreement to be signed with formal deed requirements. | Central for formal execution practice. | Ensure signature, witnessing and delivery wording comply with applicable formalities. | Signed deed, witness details and execution counterparts. |

Counterparts and electronic signature clause | Allows the spouses to sign separate copies or use electronic signatures where valid. | Useful for remote signing. | Check deed witnessing requirements, identity checks and secure audit trails. | Signing platform certificate, witness details and counterpart copies. |

Tax consequences of transfers clause | Records that tax advice should be taken before transfers, sales or settlements are implemented. | Important where assets may be sold or transferred. | Consider CGT, SDLT, income tax, IHT and timing of separation or divorce. | Tax advice, base cost records, transfer dates and HMRC guidance. |

Savings and investments | ||||

Insurance maintenance clause | Requires specified life, health, property or income protection insurance to be maintained. | Useful where one spouse or children depend on financial support. | Specify policy owner, premium payer, beneficiary, term and what happens if cover becomes unavailable. | Policy documents, premium schedule and beneficiary nomination forms. |

General legal terms | ||||

Education and childcare costs clause | Records expectations about school fees, nursery costs, childcare and child-related extras. | Important where children have private education or high childcare costs. | Do not conflict with child maintenance law or future child welfare needs. | School fee schedules, childcare invoices and child maintenance calculations. |

Review and variation | ||||

Relocation and international change clause | Requires review if either spouse moves country or the family's legal and tax position changes. | Important for internationally mobile families. | Consider jurisdiction, enforceability, tax residence, immigration and foreign property issues. | Residence evidence, visas, tax residence advice and foreign legal opinions. |

Inheritance and gifts | ||||

Death before divorce clause | Addresses the intended effect if one spouse dies before divorce or financial orders are made. | Important where estate planning is material. | Cannot safely exclude possible family provision claims align with wills and beneficiary nominations. | Wills, estate accounts, life policies and pension death benefit nominations. |

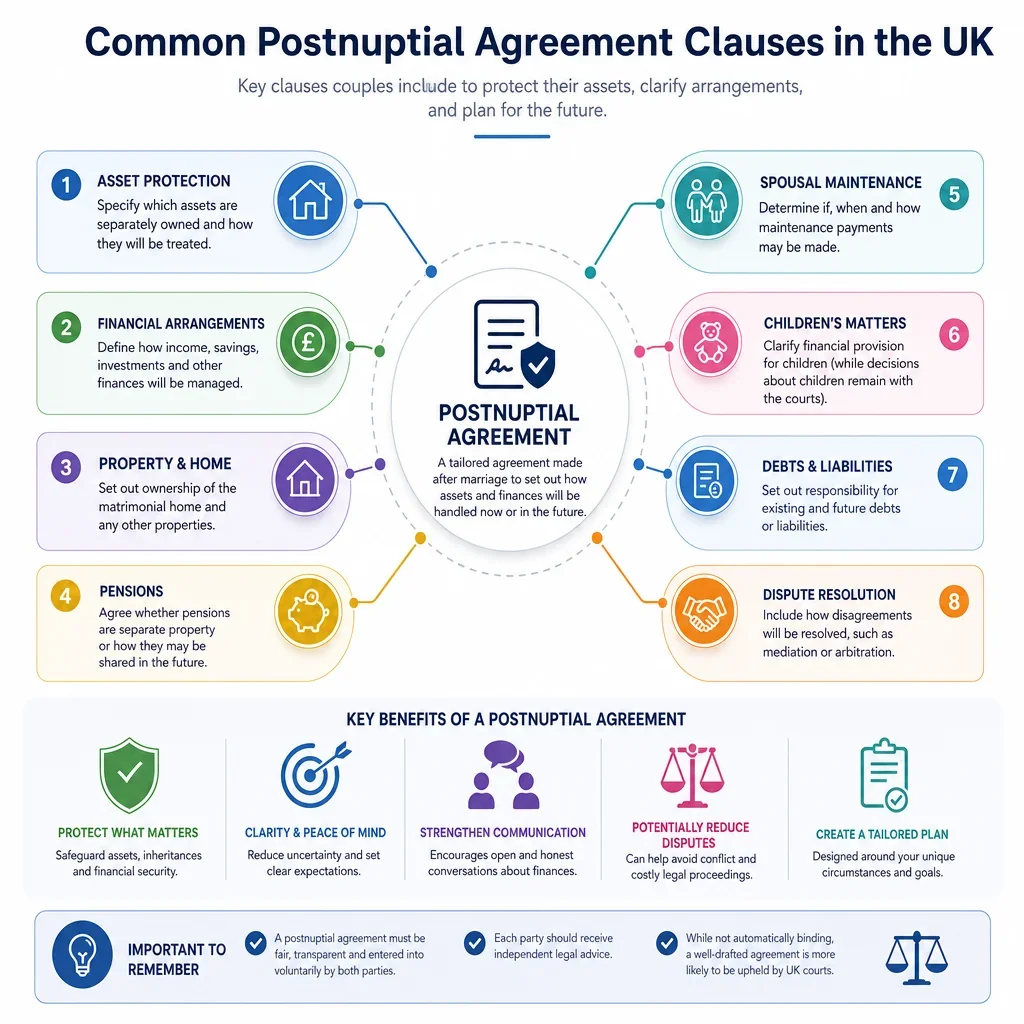

What Clauses Usually Matter Most In A UK Postnuptial Agreement?

Financial disclosure, property ownership, pensions, debts, inheritance and review clauses are usually the core clauses because they directly affect whether the agreement is fair and workable if the marriage later breaks down.

Why Is Full Financial Disclosure So Important?

A UK court is more likely to give weight to a postnuptial agreement where both spouses understood the other\'s financial position before signing. Schedules of assets, liabilities, income, pensions and business interests are therefore not just administrative; they support informed consent and help reduce later challenges.

Which Clauses Need The Most Careful Drafting?

- Family home clauses should deal with ownership, occupation, mortgage payments, sale triggers and any children\'s housing needs.

- Pension clauses should be based on accurate pension valuations and should not assume that a pension sharing order can be made without court involvement.

- Business clauses should distinguish pre-marital value, future growth, dividends and control, especially where third-party shareholders or company documents are involved.

- Inheritance and gift clauses should be consistent with wills, trusts and estate planning documents.

Can A Postnuptial Agreement Remove The Court\'s Powers?

No. In England and Wales, financial orders on divorce are ultimately governed by the court\'s discretion under the Matrimonial Causes Act 1973. A well-drafted postnuptial agreement can be highly persuasive, but it should avoid claiming to exclude the court\'s jurisdiction entirely.

When Should The Agreement Be Reviewed?

Review clauses are particularly useful after major life events such as the birth of a child, serious illness, a house purchase, receiving inheritance, starting or selling a business, moving country or a major change in income. These review triggers help keep the agreement fair and relevant over time.

FAQs

You Might Also Be Interested In