Patent Licence Royalty And Payment Models In The United Kingdom

Created:

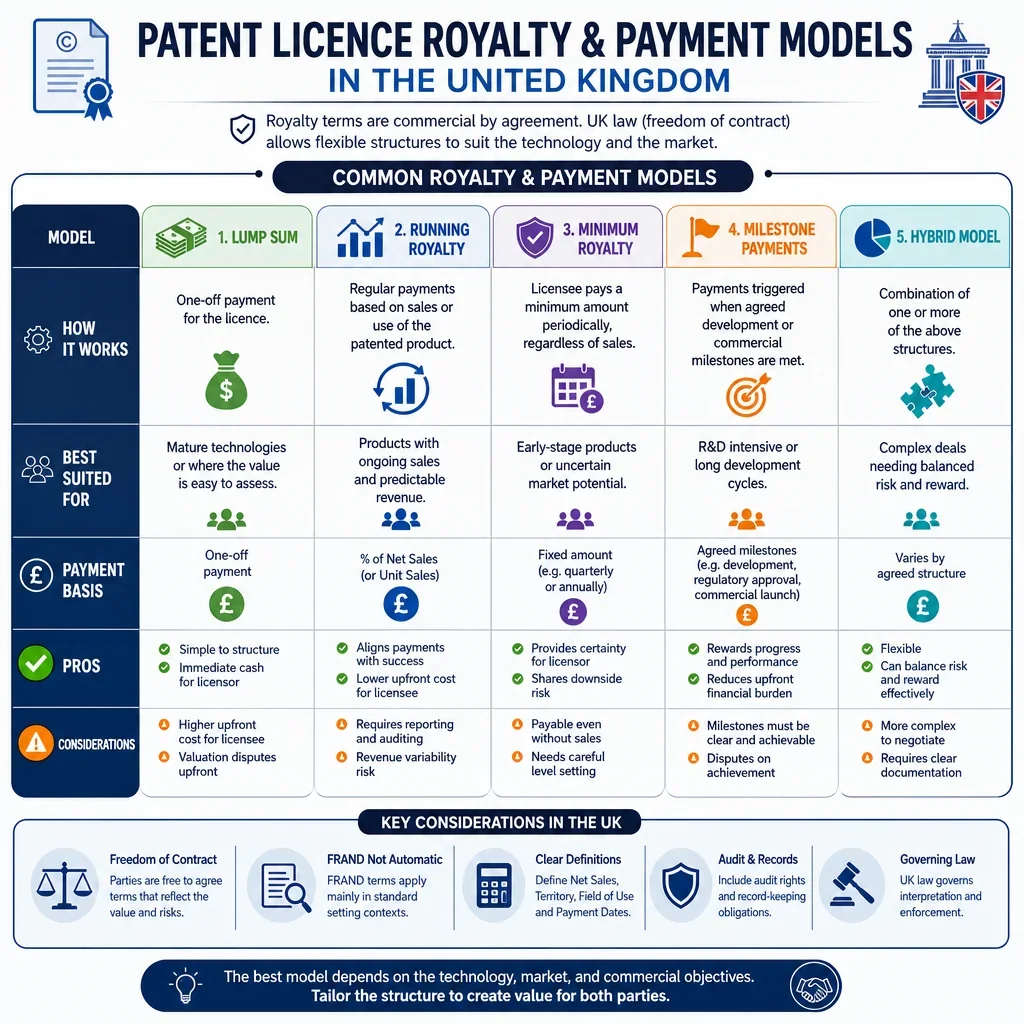

This guide explains common royalty structures and payment models used in patent licensing, helping readers compare practical options and draft clearer terms. It is especially relevant for anyone preparing an AI Generated British Patent Licence Agreement.

How it works | Complexity level | Accounting requirements | Key considerations |

|---|---|---|---|

Fixed fee | |||

Licensee pays a set amount for defined patent rights, regardless of sales volume. | Simple | Invoice records, payment receipts, VAT records, and any staged due dates. | Useful where future sales are uncertain may underprice a highly successful product. |

Upfront fee | |||

Licensee pays an initial fee when the patent licence is signed or becomes effective. | Simple | Signed agreement, invoice, receipt, VAT treatment, and allocation against later royalties if applicable. | Improves licensor cash flow should state whether refundable, creditable, or separate from royalties. |

Running royalty | |||

Licensee pays a percentage of sales revenue for licensed products during each royalty period. | Moderate | Royalty statements, net sales calculations, deductions, returns, credits, and audit trail. | Define Net Sales precisely, including discounts, rebates, tax, carriage, related-party sales, and bundled products. |

Royalty is calculated on gross invoiced sales before agreed deductions. | Moderate | Invoices, credit notes, sales ledger, VAT records, and reconciliation to royalty reports. | Simpler than net sales but may overstate value where returns, rebates, or distributor margins are material. |

Royalty applies to revenue after permitted deductions from sales of licensed products. | Complex | Detailed deduction schedules, sales reports, returns, rebates, taxes, and product-level ledgers. | Deductions should be capped or tightly defined to avoid royalty erosion. |

Per-unit royalty | |||

Licensee pays a fixed amount for each licensed product made, sold, supplied, or imported. | Moderate | Unit counts, SKU records, manufacturing logs, shipment data, returns, and inventory reconciliations. | Avoids price manipulation but needs clear trigger events and treatment of samples, replacements, and scrap. |

Royalty accrues when the licensee manufactures each patented product, whether or not sold. | Moderate | Production logs, batch records, stock write-offs, quality rejects, and reconciliation to finished goods. | Protects licensor from unsold stock strategies but may burden licensee before revenue is received. |

Royalty accrues only when a licensed unit is sold or supplied to a customer. | Moderate | Sales invoices, dispatch records, return records, credit notes, and unit-level royalty reports. | Aligns payment with revenue needs rules for free samples, warranty replacements, and internal use. |

Minimum annual royalty | |||

Licensee must pay at least a stated annual amount, even if earned royalties are lower. | Moderate | Annual royalty reconciliation, shortfall invoices, payment calendar, and carry-forward records if allowed. | Supports active exploitation should state whether shortfalls are creditable against future royalties. |

Exclusive licensee keeps exclusivity only if minimum annual royalty targets are met. | Moderate | Annual sales reports, royalty reconciliation, shortfall notices, and exclusivity status records. | Useful for exclusive licences include remedy such as conversion to non-exclusive rather than automatic termination. |

Milestone payment | |||

Payments become due when specified technical, regulatory, commercial, or funding events occur. | Moderate | Milestone evidence, acceptance records, regulatory correspondence, board approvals, and payment notices. | Milestones must be objective, dated where possible, and linked to events the licensee can evidence. |

Payment is due when a licensed product obtains specified marketing authorisation or regulatory clearance. | Complex | Regulatory submissions, approval letters, territory records, and product authorisation evidence. | Define each regulator, territory, indication, and whether conditional or provisional approvals trigger payment. |

Payments are triggered by trial commencement, patient dosing, endpoint achievement, or trial completion. | Complex | Clinical trial approvals, protocol records, dosing logs, trial reports, and milestone certificates. | Use precise trial definitions and decide whether partial, failed, repeated, or abandoned trials trigger payment. |

Payment is due when cumulative sales or annual sales exceed a specified threshold. | Moderate | Cumulative sales ledger, threshold calculations, sales statements, and supporting invoices. | Should align with Net Sales definition and prevent manipulation through affiliates or delayed invoicing. |

Revenue share | |||

Parties split revenue generated from licensed patent exploitation under agreed percentages. | Complex | Revenue ledger, cost allocations if any, partner reports, deductions, and reconciliation statements. | Clearly define shared revenue, allowable costs, timing, sublicensing income, and audit rights. |

Parties share net profit after agreed costs from exploitation of the licensed patent rights. | Complex | Revenue, direct costs, allocated overheads, tax assumptions, and periodic profit calculations. | Can be disputed unless costs, overheads, and transfer prices are tightly controlled. |

Licensee pays the licensor a percentage of fees or royalties received from authorised sublicensees. | Complex | Sublicence agreements, sublicensing income statements, deductions, royalty reports, and audit records. | Define gross sublicensing income, non-cash consideration, pass-through costs, and approval rights. |

Audit-adjusted royalty | |||

Reported royalties may be corrected after inspection of licensee books and records. | Complex | Royalty records, invoices, ledgers, stock data, audit access logs, and adjustment calculations. | Audit clause should cover notice, frequency, confidentiality, underpayment interest, and audit cost shifting. |

If an audit finds underpayment above a threshold, licensee pays the shortfall and audit costs. | Complex | Independent audit report, variance analysis, shortfall invoice, interest calculation, and remedial records. | Thresholds commonly incentivise accurate reporting ensure audit rights survive termination for past periods. |

Royalty-free licence | |||

Licensee receives patent rights without ongoing royalty payments, often for strategic or reciprocal value. | Simple | Licence records, consideration analysis, tax support, and compliance records for any non-payment obligations. | Consider tax, competition, exclusivity, sublicensing, termination, and whether non-monetary consideration is sufficient. |

Each party grants patent rights to the other without monetary royalties. | Moderate | Patent schedules, field-of-use records, product mappings, and records of reciprocal rights. | Balance patent value, scope, improvements, defensive termination, and freedom-to-operate objectives. |

Upfront fee, Running royalty | |||

Licensee pays an initial fee plus ongoing royalties based on sales or units. | Moderate | Upfront invoice, royalty statements, sales records, deductions, and periodic reconciliation. | Balances immediate value and upside state whether upfront payment is creditable against royalties. |

Fixed fee, Milestone payment | |||

A base fee is payable, with extra sums due when agreed development or commercial events occur. | Moderate | Payment schedule, milestone evidence, invoices, acceptance certificates, and notice records. | Useful where value depends on later success milestone wording must avoid subjective disputes. |

Running royalty, Minimum annual royalty | |||

Sales royalties accrue normally, but the licensee pays a top-up if annual royalties fall short. | Moderate | Periodic royalty reports, annual reconciliation, shortfall calculations, and credit carry-forward records. | Encourages exploitation while preserving upside set realistic minimums by territory and field. |

Running royalty | |||

Royalty percentage changes when sales volumes or revenue bands are reached. | Complex | Band calculations, cumulative sales records, period resets, product-level revenue, and reconciliations. | Can reward scale or protect margins specify whether tiers are marginal or retrospective. |

Royalty rate decreases as sales volumes increase or manufacturing economies improve. | Complex | Cumulative unit or revenue records, tier calculations, margin data, and royalty reconciliations. | May incentivise scaling ensure lower rates do not conflict with minimum revenue expectations. |

Royalty rate increases over time or after sales thresholds are met. | Complex | Time-based rate tables, sales thresholds, royalty calculations, and change-date records. | Useful to support launch margins should not create unintended price or competition-law pressure. |

Different royalty rates apply by territory covered by the licensed patent rights. | Complex | Territory-coded sales data, patent coverage schedules, currency conversion, and local tax records. | Match rates to patent coverage, market value, exchange rates, withholding tax, and local enforcement risk. |

Different royalties apply depending on the licensed field, application, or market segment. | Complex | Field-coded sales records, product classification, customer use data, and audit evidence. | Field definitions must be commercially clear and enforceable without excessive monitoring burden. |

Running royalty, Minimum annual royalty | |||

Exclusive licensee pays higher royalties or minimums in return for sole exploitation rights. | Moderate | Exclusivity territory records, sales reports, minimum royalty reconciliation, and compliance certificates. | Exclusivity should be tied to performance obligations, diligence duties, and loss-of-exclusivity remedies. |

Running royalty | |||

Multiple licensees may use the patent and each pays a lower ongoing royalty. | Moderate | Separate licensee reports, royalty ledgers, product scopes, and confidentiality controls. | Licensor retains market flexibility manage confidentiality and most-favoured-licensee expectations carefully. |

Audit-adjusted royalty, Running royalty | |||

Royalty may adjust if the licensor grants more favourable comparable terms to another licensee. | Complex | Comparable licence records, confidential term summaries, adjustment notices, and reconciliation calculations. | Define comparable transactions, exclusions, confidentiality, and whether changes are automatic or prospective. |

Running royalty | |||

Running royalties stop or reduce once aggregate payments reach a specified cap. | Moderate | Cumulative royalty ledger, cap calculations, payment history, and confirmation of cap exhaustion. | May help investment modelling licensor should assess upside given patent life and market size. |

Running royalty, Minimum annual royalty | |||

Annual royalties are subject to a minimum floor and maximum cap. | Complex | Annual royalty calculations, floor top-ups, cap tracking, and payment reconciliations. | Gives budget certainty but can weaken incentives if caps are reached early. |

Upfront fee, Running royalty | |||

Licensee pays royalties in advance, later credited against earned running royalties. | Moderate | Advance payment ledger, earned royalty statements, credit balance, and expiry of unused credits. | Clarify whether advances are refundable, time-limited, transferable, or lost on termination. |

Minimum annual royalty, Upfront fee | |||

Licensee guarantees a minimum payment, often paid upfront or annually, regardless of sales. | Moderate | Guarantee schedule, invoices, payment records, royalty credit tracking if applicable. | Protects licensor downside licensee should model launch delays and market-entry risks. |

Fixed fee | |||

One payment buys a fully paid-up licence for the agreed term, territory, and field. | Simple | Payment receipt, licence scope records, tax records, and patent schedule maintenance. | Reduces administration licensor loses future upside unless new patents or improvements are excluded. |

Running royalty | |||

Royalty rate reduces as licensed patents expire, lapse, are revoked, or cease to cover products. | Complex | Patent status reports, product claim charts, expiry dates, territory coverage, and rate adjustments. | Important for portfolios specify effect of supplementary protection certificates and pending applications. |

Royalties are owed only for products covered by at least one valid licensed patent claim. | Complex | Claim coverage analysis, patent status checks, product technical records, and legal opinions if disputed. | Reduces overpayment risk but may create technical disputes and require patent counsel input. |

Royalty covers both patent rights and associated know-how, sometimes continuing after patent expiry for know-how value. | Complex | Allocation between patent and know-how value, sales records, expiry tracking, and rate-step records. | Separate patent and know-how consideration to reduce enforceability and competition-law risk. |

Royalties on overseas sales are converted into pounds sterling using an agreed exchange-rate method. | Moderate | Foreign sales ledgers, exchange-rate source, conversion date, bank charges, and payment records. | Specify currency, exchange-rate source, conversion date, bank fees, and who bears exchange risk. |

Fixed fee | |||

Fixed periodic payments increase by CPI, RPI, or another agreed index. | Moderate | Index data, adjustment calculations, updated invoices, and payment schedule records. | Preserves real value define index, base month, rounding, caps, floors, and replacement index. |

Fixed licence fee is paid later, often after launch, funding, or first commercial sale. | Simple | Due-date trigger evidence, invoice records, payment timetable, and late payment tracking. | Helps early-stage licensees licensor may need security, interest, or termination rights for non-payment. |

Milestone payment | |||

Payment is due only if the licensed technology reaches a defined success outcome. | Moderate | Objective success evidence, test results, approval records, and milestone notice records. | Reduces licensee risk licensor should include diligence obligations and anti-avoidance wording. |

Fixed fee | |||

Licensee pays fixed monthly, quarterly, or annual fees for continued access to patent rights. | Simple | Payment calendar, invoices, receipts, renewal records, and termination notices. | Predictable income define suspension or termination if periodic fees are missed. |

Royalty-free licence | |||

Licensee pays no royalties but grants back rights to improvements or related patents. | Complex | Improvement invention records, patent filings, grant-back notices, and scope tracking. | Grant-back clauses need careful competition-law review, especially if exclusive or innovation-restricting. |

Patent rights are licensed without royalties for specified public-interest, research, or humanitarian uses. | Moderate | Use restrictions, eligibility records, territory records, compliance reports, and sublicence controls. | Define permitted purpose tightly and reserve commercial uses for paid licences if needed. |

Audit-adjusted royalty | |||

Licensee pays estimated royalties during the year, then true-up is made after final accounts or audit. | Complex | Estimated royalty schedules, management accounts, final accounts, true-up calculations, and audit reports. | Useful where final sales data lags define timing, interest, overpayment credits, and audit standards. |

Running royalty, Minimum annual royalty, Milestone payment, Fixed fee | |||

Interest accrues if licence payments are not made by the contractual due date. | Moderate | Due dates, payment receipts, overdue balances, interest calculations, and demand letters. | For UK business debts, contractual wording should align with or expressly replace statutory late payment rights. |

Running royalty, Fixed fee, Milestone payment | |||

Licensee grosses up payments so the licensor receives the agreed net amount after withholding tax. | Complex | Tax residence documents, withholding certificates, treaty relief forms, gross-up calculations, and remittance evidence. | Cross-border royalty payments may need tax advice on withholding, treaty relief, and payment responsibility. |

Running royalty, Fixed fee | |||

Group companies set patent royalty charges by reference to armu2019s length transfer pricing principles. | Complex | Benchmarking studies, intercompany agreements, transfer pricing files, invoices, and tax adjustments. | Rates must be supportable for UK tax purposes, especially where IP ownership and exploitation are split. |

Fixed fee, Running royalty, Minimum annual royalty, Milestone payment, Upfront fee, Revenue share, Per-unit royalty | |||

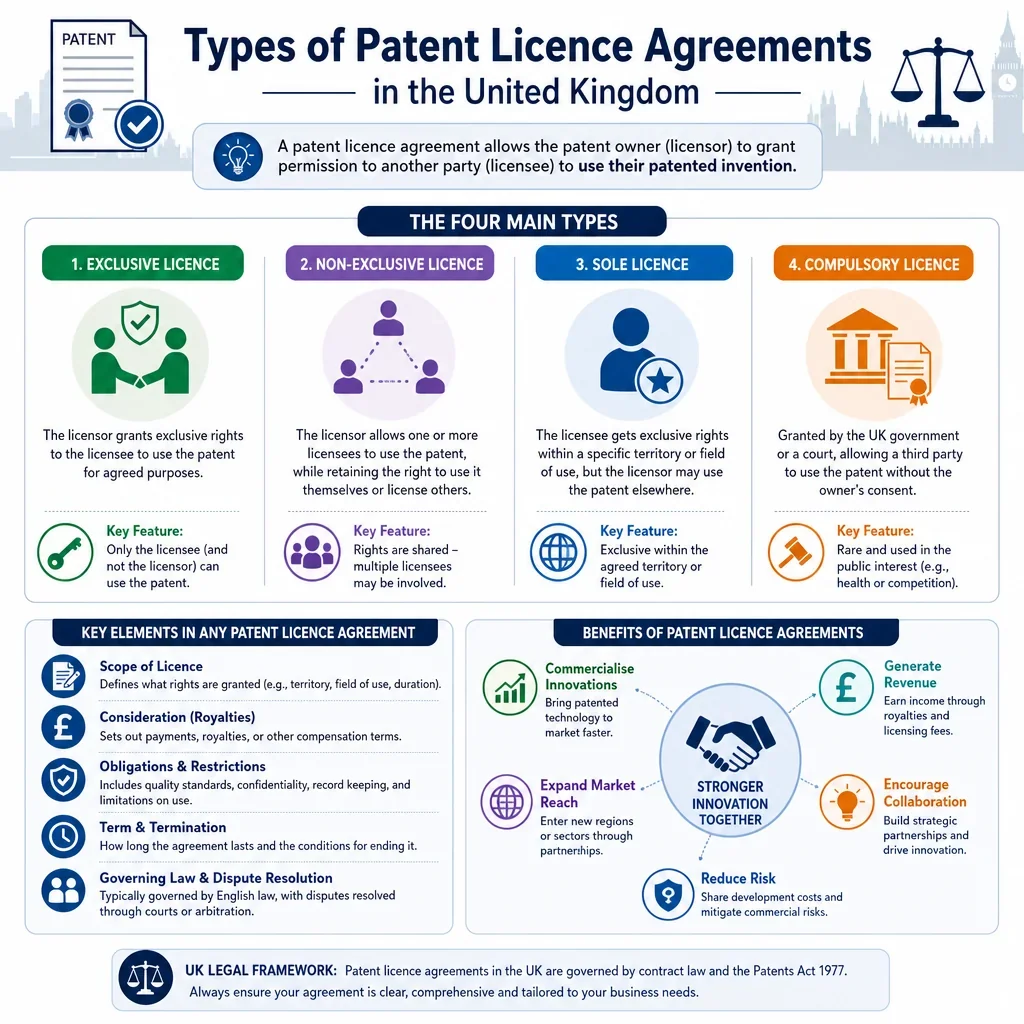

Payment obligations sit within a patent licence that may be registrable at the UK IPO. | Moderate | Executed licence, patent numbers, registration evidence, payment schedules, and royalty records. | UK patent licences should consider registration because registered interests affect priority and third-party notice. |

Fixed fee, Running royalty, Minimum annual royalty, Milestone payment, Upfront fee, Revenue share, Per-unit royalty, Royalty-free licence | |||

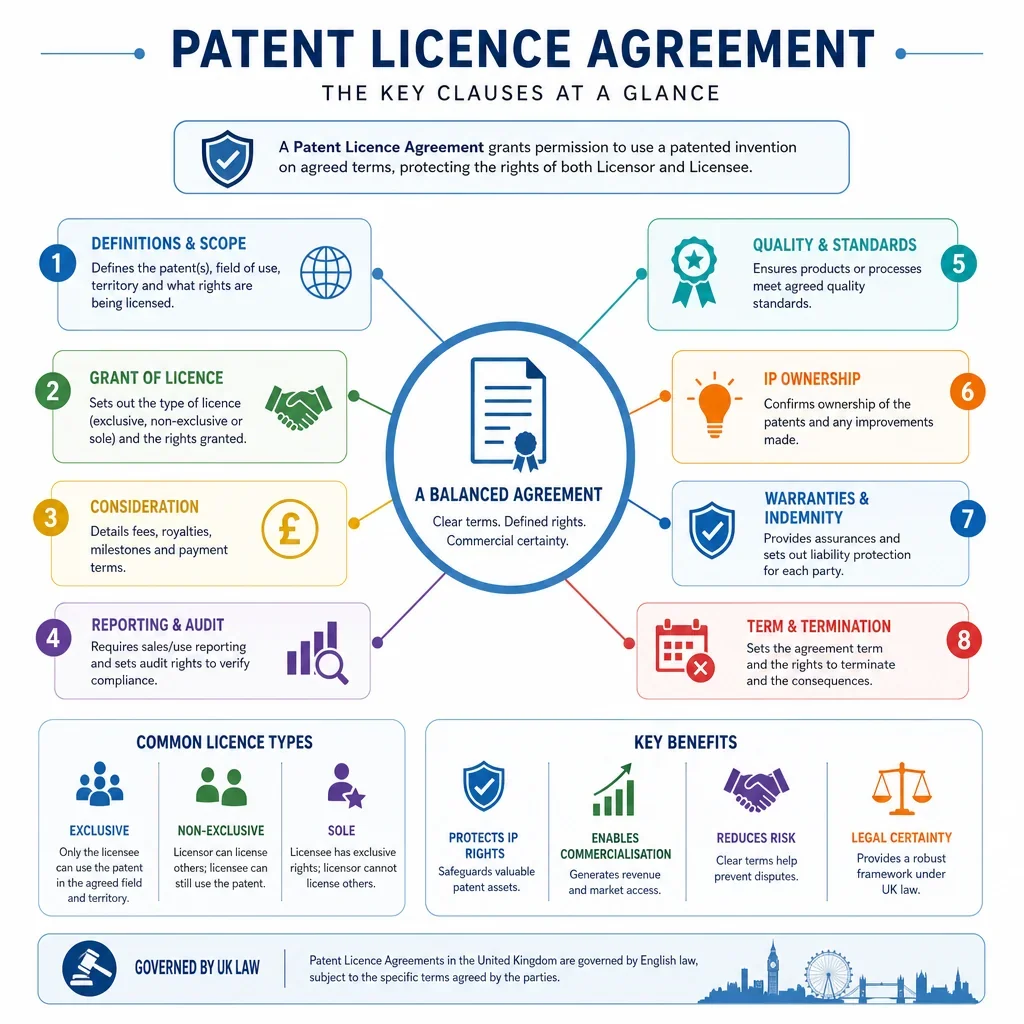

Payment and royalty terms are recorded in a written patent licence defining scope, parties, and consideration. | Simple | Signed licence, authorised signatories, payment terms, patent schedule, and amendments. | UK patent assignments and certain patent transactions require signed written instruments licences should be documented clearly. |

Running royalty, Revenue share, Royalty-free licence, Minimum annual royalty | |||

Royalty terms are combined with field, territory, exclusivity, grant-back, or output restrictions. | Complex | Licence restrictions, market data, exclusivity records, sublicence controls, and compliance reviews. | Avoid royalty or exclusivity terms that restrict competition beyond what is legally justifiable. |

How Should A UK Patent Licence Set Royalties?

UK patent licence royalties should be drafted around measurable triggers: sales, units, milestones, sublicensing income, or a fixed timetable. The licence should define Net Sales, reporting periods, VAT treatment, exchange rates, deductions, late payment interest, audit rights, and whether payments survive expiry, invalidity, termination, or patent challenge.

Which Patent Licence Payment Model Is Easiest To Administer?

Fixed fees, upfront fees, and royalty-free licences are usually simplest because they require limited sales tracking. Running royalties, revenue share, and audit-adjusted royalties need stronger accounting controls, especially where the licensee sells bundled products, grants sublicences, or operates across multiple territories.

What UK Legal Issues Affect Patent Royalty Clauses?

- Patent licences should normally be put in writing and signed if they grant or assign rights connected with UK patents; registration at the UK IPO can also affect enforceability against third parties. See the Patents Act 1977 section 30 and section 33.

- Royalty structures must be competition-law aware. Restrictions or royalties that distort competition may be assessed under the Competition Act 1998 Chapter I prohibition.

- Withholding tax, VAT, transfer pricing, and overseas payments can materially affect net receipts, so tax wording should be checked before finalising royalty rates.

Want to Generate Your own Patent Licence Agreement?

Docaro AI can help you write your own Patent Licence Agreement for use in the United Kingdom in minutes.

FAQs

Common models include fixed fees, running royalties based on sales or revenue, milestone payments, minimum annual royalties, lump-sum payments, and hybrid structures combining several methods.

Show All FAQs

You Might Also Be Interested In

Browse a United Kingdom patent licence clause library to compare drafting options, common terms, and agreement structures.

Explore types of patent licence agreements in the United Kingdom and choose the right option for your patent strategy.