Assets Commonly Covered By A Will In The UK

Asset Type | Common Ownership or Transfer Method | Usually Controlled by Will | Information to Gather | Practical Notes |

|---|---|---|---|---|

Property | ||||

Main home or residential property | Sole ownership Joint ownership | Depends on ownership structure | Address, title number, mortgage lender, ownership type. | Joint tenants usually pass by survivorship tenants in common can leave their share by Will. |

Buy-to-let or rental property | Sole ownership Joint ownership | Depends on ownership structure | Address, title number, tenancy details, managing agent, mortgage. | Executors need rental records, deposits, insurance and tax information. |

UK holiday home | Sole ownership Joint ownership | Depends on ownership structure | Address, title number, co-owners, loans, insurer, keys. | Check whether occupation agreements, loans or co-ownership restrictions apply. |

Overseas property | Varies | Depends on ownership structure | Country, address, title details, local adviser, ownership documents. | Local law may affect succession, tax and whether a separate local Will is needed. |

Land, fields or woodland | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Title number, plan, access rights, tenancies, restrictions. | Agricultural or business relief may be relevant for inheritance tax planning. |

Leasehold flat or house | Sole ownership Joint ownership | Depends on ownership structure | Title number, lease term, freeholder, service charge, mortgage. | Short leases, ground rent and service charges can affect value and administration. |

Share of freehold or residents' management company share | Sole ownership Joint ownership Trust or nominee ownership | Usually covered by a Will | Company name, share certificate, flat address, directors or managing agent. | Transfer may be governed by company articles or lease terms. |

Money and accounts | ||||

Current account | Sole ownership Joint ownership | Depends on ownership structure | Bank, sort code, account number, joint holders. | Sole accounts are usually frozen joint accounts may continue for the survivor. |

Savings account | Sole ownership Joint ownership | Depends on ownership structure | Bank or building society, account numbers, passbooks. | Interest to date of death may be needed for estate valuation. |

Cash ISA | Sole ownership | Usually covered by a Will | ISA provider, account number, balance, transfer history. | Spouses and civil partners may have an additional permitted subscription after death. |

Fixed-term deposit or savings bond | Sole ownership Joint ownership | Depends on ownership structure | Provider, bond number, maturity date, early-access terms. | Early withdrawal penalties or maturity rules may affect estate administration. |

NS&I savings products | Sole ownership | Usually covered by a Will | NS&I number, product names, holder number, statements. | Executors can claim using NS&I death claim procedures. |

Premium Bonds | Sole ownership | Usually covered by a Will | Holder number, NS&I number, approximate value. | Premium Bonds may remain in prize draws for a limited period after death. |

Cash kept at home | Sole ownership Varies | Usually covered by a Will | Location, approximate amount, safe details, trusted contact. | Executors must secure and record cash for estate valuation. |

Foreign currency cash or account | Sole ownership Joint ownership Varies | Depends on ownership structure | Currency, bank, country, account number, balances. | Exchange rates and overseas procedures may affect probate valuation. |

Investments | ||||

Stocks and shares ISA | Sole ownership Trust or nominee ownership | Usually covered by a Will | Provider, account number, holdings, nominee details. | ISA tax status ends on death, subject to continuing administration rules and spouse APS. |

Listed shares | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Company, number of shares, registrar, certificates or platform. | Valuation at death is needed nominee platforms have their own transfer process. |

Unit trusts, OEICs or investment funds | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Fund manager, account number, fund names, platform details. | Executors may need probate before sale or transfer. |

Investment platform or brokerage account | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Platform, account ID, holdings, linked bank, adviser. | Nominee holdings are administered through the platform after death. |

Gilts or government bonds | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Gilt name, nominal value, account or nominee details. | Accrued interest and market value may be needed for probate. |

Corporate bonds | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Issuer, ISIN, nominal value, broker or platform. | Liquidity and valuation can vary by bond and market. |

Employee shares or share options | Sole ownership Trust or nominee ownership Varies | Depends on ownership structure | Employer, scheme rules, option grant, vesting and exercise dates. | Scheme rules may set death, vesting and exercise deadlines. |

Business interests | ||||

Private company shares | Sole ownership Joint ownership Trust or nominee ownership | Depends on ownership structure | Company name, number and class of shares, articles, shareholders' agreement. | Articles or shareholders' agreements may restrict transfers on death. |

Sole trader business assets | Sole ownership | Usually covered by a Will | Business name, assets, stock, debts, contracts, accountant. | Executors may need urgent authority to preserve trading value. |

Partnership interest | Varies | Depends on ownership structure | Partnership agreement, capital account, profit share, partners, accountant. | Partnership agreement may control death payments, continuation and valuation. |

LLP member interest | Varies | Depends on ownership structure | LLP agreement, members, capital account, profit share, filings. | LLP agreement may limit transfer and set buyout terms on death. |

Business premises | Sole ownership Joint ownership Trust or nominee ownership Varies | Depends on ownership structure | Title or lease, mortgage, tenant or occupier, business use. | Business property relief or lease obligations may be important. |

Business stock and inventory | Sole ownership Varies | Depends on ownership structure | Stock list, storage sites, valuation method, insurance. | Perishable, seasonal or insured stock may require quick executor action. |

Copyright, patents or trade marks | Sole ownership Joint ownership Trust or nominee ownership Varies | Depends on ownership structure | Registration numbers, licences, royalties, agents, renewal dates. | Rights may generate royalties and need renewals or licence management. |

Royalties and residual income | Sole ownership Trust or nominee ownership Varies | Depends on ownership structure | Payers, contracts, collecting societies, works, payment history. | Executors need contract and collecting society details to collect future income. |

Personal possessions | ||||

Car, motorcycle or van | Sole ownership Joint ownership Varies | Usually covered by a Will | Registration, V5C, finance, insurer, keys, location. | DVLA, insurance and finance providers may need notification after death. |

Boat, yacht or personal watercraft | Sole ownership Joint ownership Varies | Depends on ownership structure | Registration, mooring, insurer, finance, keys, maintenance records. | Mooring fees, insurance and registration can continue after death. |

Jewellery and watches | Sole ownership Varies | Usually covered by a Will | Description, photos, valuations, receipts, storage location. | Specific gifts should identify items clearly to avoid disputes. |

Art, antiques and collectibles | Sole ownership Varies | Usually covered by a Will | Description, artist or maker, provenance, valuation, storage. | Professional valuation may be needed for inheritance tax and insurance. |

Furniture and household contents | Sole ownership Varies | Usually covered by a Will | Inventory, photos, valuable items, storage units, insurance. | A separate letter of wishes can help allocate lower-value personal items. |

Clothing and personal effects | Sole ownership Varies | Usually covered by a Will | Important items, sentimental gifts, storage location. | Specific sentimental items should be described clearly or covered in wishes. |

Books, records and media collections | Sole ownership Varies | Usually covered by a Will | Collection description, rare items, catalogue, valuation. | Specialist collections may need valuation and careful storage. |

Firearms or licensed weapons | Sole ownership Varies | Usually covered by a Will | Certificate details, storage location, police force, serial numbers. | Executors must comply with firearms licensing and secure storage rules. |

Pets and companion animals | Sole ownership Varies | Usually covered by a Will | Pet details, microchip, vet, insurance, preferred carer. | A Will can appoint a recipient funds for care need careful drafting. |

Horses or livestock | Sole ownership Joint ownership Varies | Depends on ownership structure | Passports, microchips, location, keepers, insurance, vet. | Immediate welfare, livery and regulatory obligations must be managed. |

Pensions and insurance | ||||

Workplace or private pension death benefits | Beneficiary nomination Trust or nominee ownership Varies | May pass outside a Will | Provider, scheme number, nomination form, beneficiaries, adviser. | Scheme trustees or administrators often decide payment using nomination forms. |

State Pension arrears | Varies | May pass outside a Will | National Insurance number, DWP correspondence, payment account. | Any unpaid amounts may be handled through DWP bereavement processes. |

Defined benefit pension survivor benefits | Beneficiary nomination Varies | May pass outside a Will | Scheme, membership number, spouse or dependant details, nominations. | Benefits are governed by scheme rules, not simply by the Will. |

Life insurance policy | Sole ownership Trust or nominee ownership Beneficiary nomination Varies | May pass outside a Will | Insurer, policy number, trust status, beneficiaries, sum assured. | Policies written in trust usually pay outside the estate and Will. |

Death-in-service benefit | Beneficiary nomination Trust or nominee ownership Varies | May pass outside a Will | Employer, scheme administrator, nomination form, benefit level. | Often discretionary and paid by trustees or scheme administrators. |

Investment bond or insurance bond | Sole ownership Joint ownership Trust or nominee ownership Beneficiary nomination Varies | Depends on ownership structure | Provider, policy number, segments, trust status, adviser. | Trust ownership or beneficiary terms may override the Will. |

Pre-paid funeral plan | Varies | May pass outside a Will | Provider, plan number, funeral director, covered services. | Tell executors where plan documents are kept because funeral decisions come early. |

Digital assets | ||||

Online bank or e-money account | Sole ownership Varies | Usually covered by a Will | Provider, account email, customer ID, linked bank. | Record provider details, but do not put passwords in the Will. |

Cryptocurrency and tokens | Sole ownership Trust or nominee ownership Varies | Usually covered by a Will | Exchange, wallet type, asset list, access instructions location. | Lost private keys or seed phrases can make assets unrecoverable. |

NFTs and digital collectibles | Sole ownership Trust or nominee ownership Varies | Usually covered by a Will | Blockchain, wallet, marketplace, collection, access instructions location. | Ownership and value depend on wallet access and marketplace evidence. |

Domain names | Sole ownership Trust or nominee ownership Varies | Depends on ownership structure | Domain, registrar, renewal date, account email, business use. | Missed renewals can cause loss of a valuable website or email address. |

Website or monetised online content | Sole ownership Trust or nominee ownership Varies | Depends on ownership structure | Hosting, CMS, domain, ad networks, affiliate accounts, analytics. | Income may stop if hosting, domain or payment accounts lapse. |

Social media accounts | Varies | May pass outside a Will | Platforms, usernames, legacy contact settings, account wishes. | Platform terms may control memorialisation, deletion or access. |

Email accounts | Varies | May pass outside a Will | Providers, usernames, recovery contacts, important linked accounts. | Email access is often essential for finding online assets, but terms restrict access. |

Cloud storage, photos and files | Varies | May pass outside a Will | Providers, account emails, important folders, sharing wishes. | Service terms and privacy rules may limit executor access. |

Online marketplace or seller account balance | Sole ownership Varies | Depends on ownership structure | Platform, store name, balances, linked bank, open orders. | Open orders, refunds and customer obligations may need prompt handling. |

Loyalty points and reward schemes | Varies | May pass outside a Will | Scheme, membership number, points balance, expiry rules. | Scheme terms decide whether points transfer, expire or are cancelled. |

Other | ||||

Beneficial interest in a trust | Trust or nominee ownership | May pass outside a Will | Trust deed, trustees, benefit type, letters of wishes. | Trust deed determines rights beneficiary may not own the underlying assets. |

Loans or debts owed to you | Sole ownership Joint ownership Varies | Usually covered by a Will | Borrower, agreement, balance, repayment terms, security. | Executors need evidence to collect or forgive debts properly. |

Expected inheritance from another estate | Varies | Depends on ownership structure | Estate name, solicitor, executor, expected amount, documents. | Rights may depend on whether the first estate has vested or been varied. |

Personal injury or litigation claim | Sole ownership Varies | Depends on ownership structure | Solicitor, claim number, defendant, insurer, status, deadlines. | Some claims survive death and need legal review by executors. |

Tenancy deposit or rent deposit | Sole ownership Joint ownership Varies | Depends on ownership structure | Deposit scheme, tenancy address, landlord, certificate, amount. | Deposit recovery depends on tenancy terms and scheme rules. |

Allotment, club or membership rights | Varies | May pass outside a Will | Organisation, membership number, rules, fees, transfer terms. | Many memberships are personal and non-transferable under their rules. |

Safe deposit box contents | Sole ownership Joint ownership Varies | Depends on ownership structure | Provider, box number, key location, authorised users. | Contents must be inventoried and valued before distribution. |

Assets held by nominee or bare trustee | Trust or nominee ownership | Depends on ownership structure | Nominee, declaration of trust, underlying assets, beneficiary. | Beneficial ownership may pass by Will even if legal title is elsewhere. |

Assets subject to hire purchase or finance | Varies | Depends on ownership structure | Finance provider, agreement, balance, asset, settlement figure. | The estate may not own the asset outright until finance is settled. |

Jointly owned assets | Joint ownership | Depends on ownership structure | Co-owners, ownership shares, joint tenancy or tenancy in common. | Survivorship can override Will gifts for joint tenancy assets. |

Residuary estate | Varies | Usually covered by a Will | Main beneficiaries, substitute beneficiaries, proportions, exclusions. | A residue clause helps catch assets not specifically listed in the Will. |

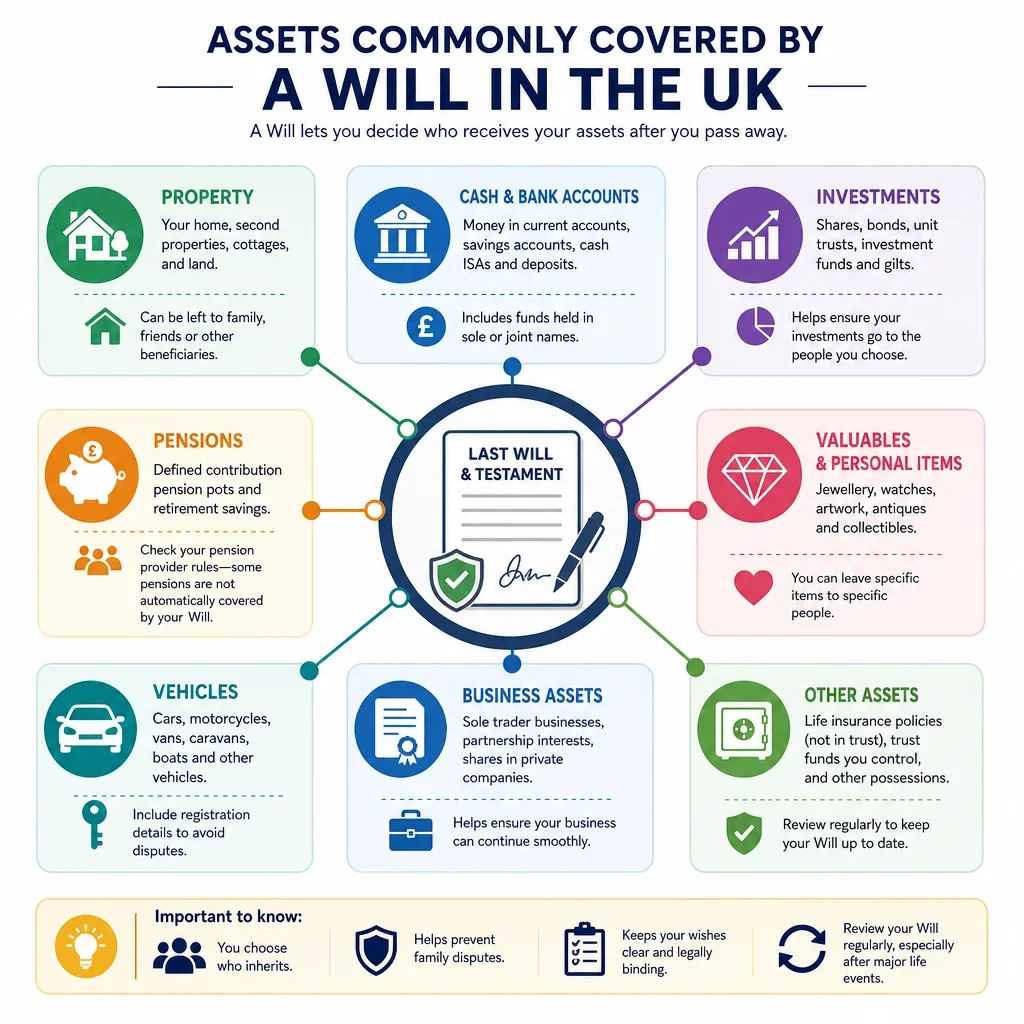

What Assets Should You List When Making A Will In The UK?

A UK Will can usually deal with assets owned in your sole name, including your home, savings, investments, personal possessions and business interests. However, some valuable assets may not pass under your Will at all, so it is important to record both the asset and how it is owned.

Which Assets May Pass Outside A Will?

- Jointly owned property and accounts may pass automatically to the surviving joint owner if held as joint tenants, rather than under the Will.

- Pension death benefits and many life policies often depend on scheme rules, trust wording or beneficiary nominations, so nominations should be kept up to date.

- Trust assets are usually controlled by trustees and the trust deed, not by the beneficiary\'s Will.

- Foreign assets may be affected by local succession and tax rules, so UK advice may need to be coordinated with local advice.

What Information Helps Executors Deal With An Estate?

Executors need enough detail to identify assets without exposing unnecessary security information. Useful details include property addresses, account providers, policy numbers, share registrars, business details, vehicle registration numbers, storage locations and the existence of digital accounts or crypto wallets. Passwords and seed phrases should not be placed directly in the Will because a Will may become public after probate.

Why Does Ownership Structure Matter For A Will?

The same asset type can be treated differently depending on whether it is owned solely, jointly, through a company, in trust, or with a beneficiary nomination. For example, a share of a home held as tenants in common can usually be left by Will, while a joint tenancy normally passes by survivorship. This makes checking ownership records an essential step before relying on a Will to pass a particular asset.

FAQs

You Might Also Be Interested In